|

시장보고서

상품코드

2072549

접객 로봇 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Hospitality Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

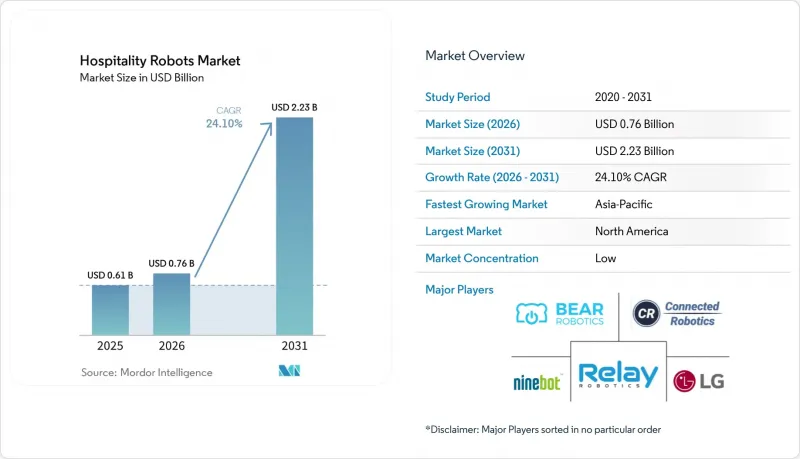

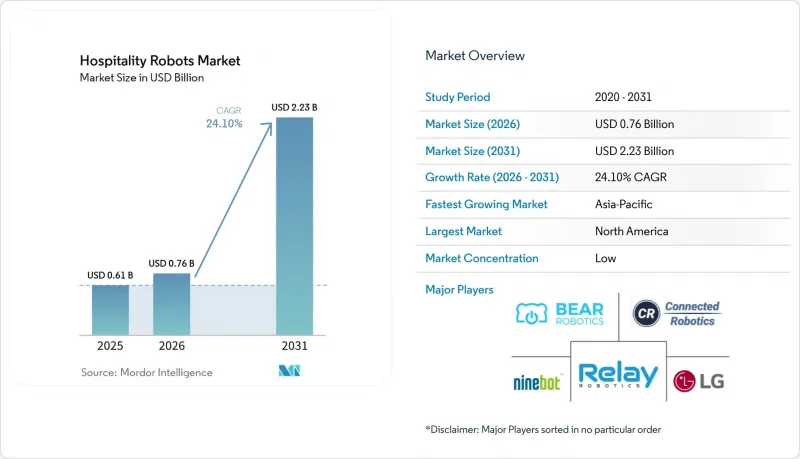

Mordor Intelligence에 의하면, 접객 로봇 시장 규모는 2025년에 6억 1,000만 달러로 평가되었습니다. 2026년 7억 6,000만 달러에서 2031년까지 22억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 24.10%를 나타낼 전망입니다.

본 보고서는 로봇의 유형(접수·이동 안내 로봇, 배송 로봇 등), 구성 요소(하드웨어, 소프트웨어, 서비스), 최종 사용자(호텔, 레스토랑·바 등), 도입 장소(프론트 오브 하우스 및 백 오브 하우스), 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 접객 로봇 시장 동향 및 인사이트

디지털 및 자동화 기술의 보급 확대

디지털 전환(DX) 프로그램의 확산에 따라, 기업들은 통일된 데이터 기반 서비스 모델을 추구하는 과정에서 로봇 도입을 추진하고 있습니다. 로봇을 클라우드 기반 호텔·호스피탈리티 관리 소프트웨어와 통합한 시설에서는 룸서비스 시간 준수율이나 하우스키핑 처리 시간 등 운영 지표에서 15%-30%의 개선을 보고하고 있습니다. 로봇 군 관리 대시보드를 통해 관리자는 실시간 위치 정보와 작업 상태를 파악할 수 있으며, 로봇과 인간 직원 간의 업무 부하 균형을 선제적으로 조정할 수 있게 됩니다. IoT 센서나 빌딩 관리 시스템이 API를 공개함에 따라, 로봇은 엘리베이터의 이용 현황, 연회장의 가동 현황, 환경 조건 등에 관한 상세한 정보를 파악할 수 있게 되었으며, 이를 통해 업무 효율이 향상되고 있습니다. 동시에, 탑재된 카메라와 LiDAR를 통해 수집된 데이터를 바탕으로 손님의 동선을 익명화한 히트맵이 생성되어, 사람의 개입이 가장 큰 가치를 창출하는 상황에 직원을 정확하게 배치할 수 있게 됩니다. 각 공급업체들은 이미지를 로컬에서 처리하는 엣지 AI 모듈을 강조하고 있으며, 이를 통해 지연 시간을 줄이는 동시에 유럽 및 아시아 일부 지역의 데이터 주권에 대한 우려에도 대응하고 있습니다.

팬데믹 이후 호텔·관광 업계의 인력 부족

2024년에도 외식·숙박 업계의 이직률은 2020년 이전 수준보다 76% 높은 상태를 유지했습니다. 그 결과, 경영진은 인력을 고부가가치 고객 응대 업무에 재배치하고, 복도 내 배달, 테이블 정리, 복도 청소기와 같은 반복적인 작업에는 로봇을 투입했습니다. 배달 로봇을 도입한 시설에서는 수작업으로 제공되는 룸서비스 횟수가 20%-35% 감소한 것으로 확인되었으며, 이에 따라 직원들은 프런트 데스크에서 추가 판매 및 로열티 프로그램 관리에 집중할 수 있게 되었습니다. 주방에서는 반자율형 프라이 스테이션이 근무 교대 사이의 공백 시간대에도 생산량을 유지하고, 서비스 피크 시간대에도 주문 처리 시간을 일정하게 유지함으로써, 서비스 기간 전반에 걸쳐 일관된 품질을 보장하고 있습니다. 이러한 생산성 향상을 통해, 이민 정책으로 인해 계절 근로자 공급이 부족해진 시장에서 인건비 상승 위험을 완화하고 서비스 품질을 안정적으로 유지할 수 있습니다.

소규모 사업자에게 있어 높은 초기 설비 투자(CAPEX)

로봇 1대당 구입 가격이 1만 5,000-5만 달러에 달하기 때문에 이익률이 극히 낮은 가족 경영 여관이나 독립 카페에게는 진입 장벽이 되고 있습니다. 구독형 로봇이나 수익 분배 모델과 같은 자금 조달 솔루션이 등장하고 있지만, 체인점 네트워크 외부의 도입 현황은 여전히 제각각입니다. 소규모 사업자에게는 교육에 드는 간접비라는 문제도 있습니다. 사내에 IT 팀이 없기 때문에 유지보수를 외부 통합 업체에 위탁하는 경우가 많으며, 그 결과 총 소유 비용이 증가하게 됩니다. 이러한 장벽에 대응하기 위해 각 업체들은 현재 다년 계약 서비스 플랜을 세트로 판매하고 있으며, 리스 플랜의 경우 지불액을 예상되는 인건비 절감액에 맞추어 조정하고 있지만, 경제적 관점에서는 여전히 여러 매장을 운영하는 대규모 시설이 더 유리한 상황입니다.

부문별 분석

2025년, 접객 로봇 시장에서 배송용 로봇은 39.05%의 점유율을 유지했으며, 빠른 투자 회수(ROI)와 워크플로우에의 손쉬운 통합이 두드러집니다. 한편, 보안 및 감시 플랫폼 시장은 능동적 감시를 도입한 시설에 대해 부동산 보험사가 우대 보험료를 적용하고 있다는 점이 호재로 작용함에 따라, 2031년까지 연평균 성장률(CAGR) 26.1%로 성장이 가속화될 것으로 예측됩니다. 이 로봇들은 로비와 주차장을 순찰하며, 360도 영상을 중앙 지휘 센터로 스트리밍하는 동시에, 수상한 움직임을 감지하면 실시간으로 경보를 발령합니다. 이와 동시에, 안내 로봇은 여행객들에게 다국어로 체크인 절차를 안내하고, 청소 로봇은 복도 청소와 회의실의 UV-C 소독을 담당하고 있습니다. CES 2024에서 Richtech사의 바텐더 로봇 ‘"ADAM"을 포함한 조리 로봇 시연이 진행된 것은 숙련된 기술이 요구되는 조리 업무에서도 로봇 기술의 가능성을 입증한 것입니다.

규제 체계의 강화로 인해 인간과 자율형 기계의 안전한 공존이 보장되고 있습니다. UL 3320 인증은 현재, 특히 북미에서 많은 풀서비스 호텔 체인의 조달 요건으로 자리 잡고 있으며, 이에 따라 해당 인증을 준수하는 공급업체의 경쟁 우위가 더욱 강화되고 있습니다. 안전 기준이 점차 정립됨에 따라, 시설 소유주들은 로봇의 도입이 더욱 확대될 것으로 전망하며, 로봇을 향후 스마트 호텔의 청사진에서 없어서는 안 될 핵심 요소로 자리매김하고 있습니다. 예측 기간 동안 배송, 보안, 청소, 안내 등 다양한 서비스 포트폴리오를 통해 공급업체는 특정 응용 분야 수요 변동으로부터 보호받게 되며, 부품 비용이 하락하더라도 안정적인 기여 이익률을 유지할 수 있게 됩니다.

2025년 지출 중 하드웨어가 59.12%를 차지했습니다. 이는 사업자가 로봇의 자율성에 필수적인 섀시, 배터리, 센서 어셈블리에 비용을 투자했기 때문입니다. 그러나 AI를 활용한 경로 최적화, 자연어 처리, 예측 유지보수 알고리즘이 물리적 자산의 가치를 극대화함에 따라 소프트웨어 부문이 가장 빠르게 성장하고 있으며, 연평균 성장률(CAGR)은 25.05%로 성장을 지속하고, 있습니다. 각 벤더사는 장비의 기능 수명을 연장하는 무선 업데이트(OTA)를 제공하고 있으며, 차량 관리 포털을 통해 기계적인 개조 없이 새로운 기능을 적용함으로써, 수익을 고수익률의 지속적인 라이선스 수입으로 전환하고 있습니다. 사업자에게 있어 분석 대시보드는 배송, 청소, 보안 등 각 부문의 차량 운영에 걸친 성과 지표를 통합하여, 인력 배치에 대한 의사결정에 도움이 되는 전사적인 인사이트를 제공합니다.

설치, 교육, 연중무휴 24시간 원격 지원을 포함하는 서비스 분야는 여전히 규모는 가장 작지만, 전략적으로 매우 중요합니다. 여러 시설을 보유한 호텔 그룹이 체인 전체에 로봇을 도입함에 따라, LiDAR 장치의 보정, PMS API 통합, 규정 준수 점검 조정이 가능한 인증 기술자에 대한 수요가 증가하고 있습니다. 지역 시스템 통합사업자와의 제휴를 통해 이러한 역량의 확충이 가속화되고 있습니다. 특히 라틴아메리카와 중동에서는 현지 지원을 통해 가동률이 높은 기간 동안 발생하는 가동 중단으로 인한 평판 위험을 줄이고 있습니다.

지역별 분석

북미가 37.70%라는 압도적인 점유율을 차지하고 있는 것은 초기부터 시범 도입 실적이 있었으며 벤처 캐피털의 강력한 지원을 받았음을 반영한 것입니다. 체인 계약을 통해 공급업체는 사업을 빠르게 확장할 수 있습니다. 예를 들어, Relay Robotics가 여러 시설에 도입한 솔루션은 로봇 API에 최적화된 호텔 엘리베이터의 이용률을 높이고 있습니다. 캐나다의 운영사는 인력 부족 시 발생할 수 있는 안전 문제를 해결하기 위해 도로변 시설의 주차장에 배치할 보안 로봇 개발에 주력하고 있습니다. 멕시코의 리조트 지역에서는 디지털 업셀링 안내를 표시하여 룸서비스 제공량을 확대하는 이중언어를 구사하는 배달 로봇이 활용되고 있습니다.

아시아태평양의 연평균 성장률(CAGR) 25.8%는 정책 지원, 제조 효율성, 그리고 고객의 기술 수용도가 결합되어 시장이 성장하고 있음을 보여줍니다. 중국에서는 3성급 이상의 호텔 대부분이 최소 한 대의 서비스 로봇을 도입하고 있으며, Ninebot과 같은 국내 브랜드들은 로봇을 통한 어메니티 제공을 일상화하기 위해 대도시권에서 마케팅 캠페인을 전개하고 있습니다. 일본에서는 고령화가 진행되면서 호텔 업계의 인력 부족이 심화되고 있으며, 비즈니스 호텔에서는 심야에 로봇이 라면 배달을 담당하게 되었습니다. 싱가포르의 창이 호스피탈리티 클러스터에서는 공항 시스템과 연동되는 다기능 안내 로봇의 시범 운영이 진행되고 있으며, 도착 게이트에서 호텔 로비까지 끊김 없이 이동할 수 있게 되었습니다.

유럽에서는 GDPR(EU 개인정보보호규정)에 기반한 개인정보 보호 요건과 환경 보호 요구 사항 간의 균형이 이루어지고 있습니다. 독일의 숙박 시설에서는 시설 내에서 데이터를 처리해야 한다는 요구가 제기되고 있어, 각 벤더사는 클라우드로의 업로드를 피할 수 있는 엣지 AI 모델 도입을 서둘러야 하는 상황에 놓여 있습니다. 프랑스의 부티크 호텔은 디자인 미학을 중시하며, 브랜드 테마에 맞추어 외관을 맞춤 설정할 수 있는 로봇을 선정하고 있습니다. 스페인의 해안가 리조트에서는 실외용 보안 로봇이 수영장 주변을 순찰하고 있어, 직원들은 투숙객과의 교류 활동에 전념할 수 있게 되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the hospitality robots market size was valued at USD 0.61 billion in 2025 and estimated to grow from USD 0.76 billion in 2026 to reach USD 2.23 billion by 2031, at a CAGR of 24.10% during the forecast period (2026-2031).

This report is Segmented by Robot Type (Reception and Mobile Guidance Robots, Delivery Robots, and More), Component (Hardware, Software, and Services), End-User (Hotels, Restaurants and Bars, Tand More), Deployment (Front-Of-House and Back-Of-House), and Geography (North America, South America, Europe, Asia Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Hospitality Robots Market Trends and Insights

Growing Penetration of Digital and Automation Technologies

Widespread digital transformation programs are pushing operators toward robotics as they seek unified, data-driven service models. Properties that integrate robots with cloud-based hotel and hospitality management software report 15%-30% uplifts in operational metrics such as room-service punctuality and housekeeping turnaround. Fleet-management dashboards provide managers with real-time location and task status, enabling proactive load balancing between robots and human staff. As IoT sensors and building-management systems expose their APIs, robots receive granular inputs on elevator availability, banquet hall occupancy, and environmental conditions, thereby improving task efficiency. At the same time, data captured through onboard cameras and lidar builds anonymized heat maps of guest traffic, allowing for the precise scheduling of staff where human touch delivers the most value. Suppliers highlight edge-AI modules that process images locally, reducing latency and addressing data-sovereignty concerns in Europe and parts of Asia.

Post-Pandemic Labour Shortages in Hospitality

Turnover rates remained 76% higher than pre-2020 levels in 2024 for food-service and lodging businesses. Managers consequently reassigned human staff to high-value interactions and deployed robots to handle repetitive workloads, including corridor deliveries, table busing, and corridor vacuuming. Properties using delivery robots have documented 20%-35% reductions in manual room-service runs, freeing attendants to focus on upselling or loyalty-program engagement at the front desk. In kitchens, semi-autonomous fry stations maintain output during shift gaps, ensuring consistent ticket times across service peaks, thereby maintaining consistency throughout service periods. These productivity gains mitigate wage-pressure risks and stabilize service quality in markets where immigration policy tightens the supply of seasonal workers.

High Upfront CAPEX for Small Operators

Purchase prices ranging from USD 15,000 to USD 50,000 per robot deter family-owned inns and independent cafes, which operate on razor-thin margins. Financing solutions are emerging in subscription robotics and revenue-sharing models, but adoption outside chain networks remains uneven. Small operators also face training overheads; lacking in-house IT teams, they often outsource maintenance to third-party integrators, thereby increasing the total cost of ownership. Vendors responding to this barrier now bundle multi-year service agreements, while leasing packages align payments with projected labor savings, yet the economics still favor larger properties with multi-unit rollouts.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Demand for Contact-less Guest Experiences

- Government Incentives for Service-Robot Adoption

- Interoperability and Integration Issues with Legacy PMS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Delivery units retained a 39.05% slice of the hospitality robots market in 2025, underscoring their rapid ROI and straightforward workflow integration. Security and surveillance platforms, however, are expected to accelerate at a 26.1% CAGR to 2031, buoyed by property insurers' favorable premiums for sites employing active monitoring. These robots patrol lobbies and parking structures, streaming 360-degree video to centralized command centers and triggering real-time alerts when they detect suspicious patterns. In parallel, reception robots guide travelers through multilingual check-in steps, while cleaning robots tackle corridor vacuuming and UV-C disinfection of meeting rooms. Demonstrations of food-preparation robots, including Richtech's ADAM bartender at CES 2024, validate robotics' potential even in skilled culinary tasks.

A tightening regulatory framework ensures safe cohabitation between humans and autonomous machines. UL 3320 certification now serves as a procurement prerequisite for many full-service hotel chains, particularly in North America, thereby reinforcing the competitive advantage of compliant vendors. As safety standards mature, property owners anticipate broader integration, positioning robots as an indispensable pillar of forthcoming smart-hotel blueprints. Throughout the forecast horizon, diversified portfolios delivery, security, cleaning, and guidance will insulate suppliers from demand swings in any one application cluster, supporting stable contribution margins even as component costs decline.

Hardware accounted for 59.12% of 2025 spending, as operators paid for chassis, battery, and sensor assemblies crucial to robot autonomy. Yet the software layer is scaling fastest, advancing at a 25.05% CAGR, because AI-driven route optimization, natural language processing, and predictive maintenance algorithms unlock the full value of physical assets. Vendors are packaging over-the-air updates that extend the functional life of units; fleet-management portals push new behaviors without mechanical alteration, shifting revenue toward high-margin recurring licenses. For operators, analytics dashboards consolidate performance metrics across delivery, cleaning, and security fleets, offering enterprise-wide insights that inform staffing decisions.

The services slice, including installation, training, and 24/7 remote support, remains the smallest but strategically critical. As multi-property hotel groups roll out robots chain-wide, demand rises for certified technicians able to calibrate lidar units, integrate PMS APIs, and coordinate compliance inspections. Partnerships with regional systems integrators accelerate this capability build-out, particularly in Latin America and the Middle East, where localized support mitigates reputational risk associated with downtime during high-occupancy periods.

Complete Report Scope:

- By Robot Type

- Reception and Mobile Guidance Robots

- Delivery Robots

- Cleaning Robots

- Food-Preparation Robots

- Security and Surveillance Robots

- By Component

- Hardware

- Software

- Services

- By End-User

- Hotels

- Restaurants and Bars

- Travel and Tourism Operators

- Recreational Facilities, Events and Attractions

- By Deployment

- Front-of-House

- Back-of-House

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America's dominant 37.70% share mirrors its history of early pilots and strong venture capital backing. Chain agreements allow suppliers to scale rapidly: Relay Robotics' multi-property installations improve the utilization of hotel elevators optimized for robot APIs. Canadian operators are focusing on security robots for parking lots at roadside properties, addressing safety concerns during labor shortages. Mexican resort corridors utilize bilingual delivery robots that enhance room-service basket sizes by displaying digital upsell prompts.

Asia Pacific's 25.8% CAGR underlines a convergence of policy support, manufacturing efficiencies, and guest tech affinity. In China, most three-star and above hotels deploy at least one service robot, and domestic brands such as Ninebot roll out metropolitan marketing campaigns to normalize robot-delivered amenities. Japan's aging population intensifies labor gaps in the hotel industry, and robots now handle late-night ramen deliveries in business hotels. Singapore's Changi hospitality cluster trials multi-function guidance robots that integrate with airport systems, creating seamless transitions from the arrival gate to the hotel lobby.

Europe balances GDPR-driven privacy requirements with environmental imperatives. German properties demand on-premise data processing, pushing vendors to enable edge-AI models that bypass cloud uploads. French boutique hotels emphasize design aesthetics, selecting robots with customizable exteriors that align with brand themes. Spain's coastal resorts deploy outdoor-rated security robots that patrol pool decks, freeing staff for guest-engagement activities.

- Relay Robotics Inc.

- LG Electronics Inc.

- Bear Robotics Inc.

- Ninebot Limited

- Connected Robotics Inc.

- Aethon Inc.

- SoftBank Robotics Group Corp.

- Knightscope Inc.

- Pudu Robotics Co. Ltd.

- Keenon Robotics Co. Ltd.

- PAL Robotics SL

- Tailos Inc.

- Robotemi Ltd.

- UBTECH Robotics Inc.

- Savioke Inc.

- Service Robots GmbH

- Innova Robotics and Automation

- OrionStar Robotics Co. Ltd.

- Cobalt Robotics Inc.

- Richtech Robotics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing penetration of digital and automation technologies

- 4.2.2 Post-pandemic labour shortages in hospitality

- 4.2.3 Declining sensor and component prices

- 4.2.4 Surge in demand for contact-less guest experiences

- 4.2.5 Government incentives for service-robot adoption

- 4.2.6 Edge-AI enabling real-time on-premise analytics

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX for small operators

- 4.3.2 Interoperability and integration issues with legacy PMS

- 4.3.3 Data-privacy concerns in guest-facing use-cases

- 4.3.4 Limited ROI outside tier-1 properties

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Robot Type

- 5.1.1 Reception and Mobile Guidance Robots

- 5.1.2 Delivery Robots

- 5.1.3 Cleaning Robots

- 5.1.4 Food-Preparation Robots

- 5.1.5 Security and Surveillance Robots

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By End-User

- 5.3.1 Hotels

- 5.3.2 Restaurants and Bars

- 5.3.3 Travel and Tourism Operators

- 5.3.4 Recreational Facilities, Events and Attractions

- 5.4 By Deployment

- 5.4.1 Front-of-House

- 5.4.2 Back-of-House

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 South-East Asia

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Relay Robotics Inc.

- 6.4.2 LG Electronics Inc.

- 6.4.3 Bear Robotics Inc.

- 6.4.4 Ninebot Limited

- 6.4.5 Connected Robotics Inc.

- 6.4.6 Aethon Inc.

- 6.4.7 SoftBank Robotics Group Corp.

- 6.4.8 Knightscope Inc.

- 6.4.9 Pudu Robotics Co. Ltd.

- 6.4.10 Keenon Robotics Co. Ltd.

- 6.4.11 PAL Robotics SL

- 6.4.12 Tailos Inc.

- 6.4.13 Robotemi Ltd.

- 6.4.14 UBTECH Robotics Inc.

- 6.4.15 Savioke Inc.

- 6.4.16 Service Robots GmbH

- 6.4.17 Innova Robotics and Automation

- 6.4.18 OrionStar Robotics Co. Ltd.

- 6.4.19 Cobalt Robotics Inc.

- 6.4.20 Richtech Robotics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment