|

시장보고서

상품코드

2072553

필리핀의 윤활유 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Philippines Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

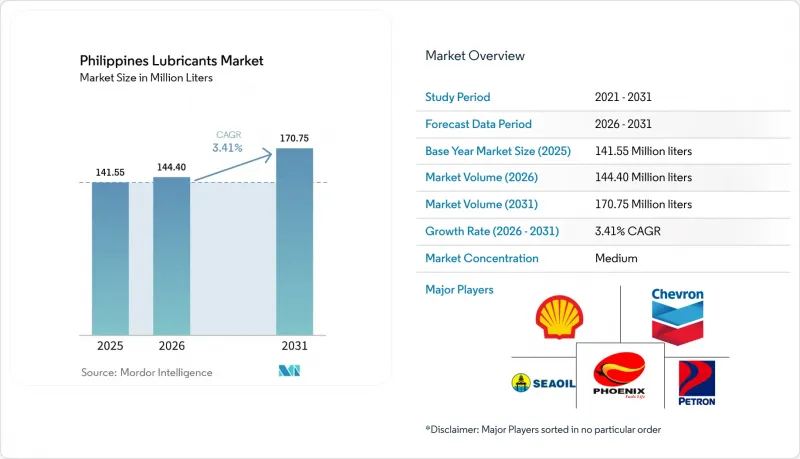

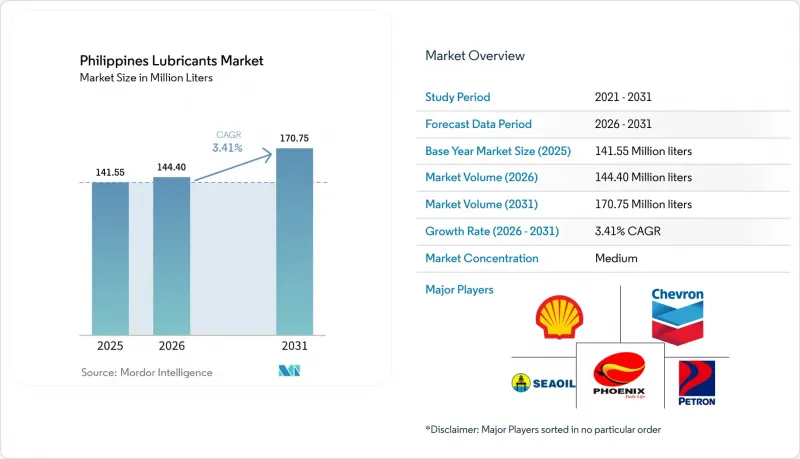

Mordor Intelligence에 의하면, 필리핀의 윤활유 시장 규모는 2025년에 1억 4,155만 리터로 평가되었습니다. 2026년 1억 4,440만 리터에서 2031년까지 1억 7,075만 리터에 이를 것으로 추정되고 예측 기간(2026-2031년)에서 CAGR 3.41%로 성장하고 있습니다.

본 보고서는 제품 유형(자동차용 엔진 오일, 산업용 엔진 오일, 그리스, 금속 가공유, 터빈 오일, 기타), 최종 사용자 산업(자동차, 선박, 항공우주, 중장비, 산업용), 기유 유형(광물유계 윤활유, 합성 윤활유, 반합성 윤활유, 기타)별로 분류되어 있습니다. 시장 전망은 수량(리터) 기준으로 제시되어 있습니다.

필리핀의 윤활유 시장 동향 및 인사이트

늘어나는 대형 건설 프로젝트(Build-Better-More)

2024년의 1조 5,450억 필리핀 페소(266억 달러)에 달하는 지출액은 GDP의 5.8%에 해당했으며, 대규모 도로, 철도, 교량 건설을 뒷받침했습니다. 이로 인해 굴삭기, 크레인, 콘크리트 믹서가 가혹한 가동 주기로 계속 가동되고 있습니다. 장비 소유주들은 오일 교환 주기를 단축하고 있어, 아연 함량이 높은 작동유와 극압 그리스에 대한 수요가 증가하고 있습니다. 바탄-카비테 인터링크 교량 및 메트로 마닐라 지하철 등의 프로젝트에는 그을음 억제를 위해 그룹 II 기유 혼합에 의존하는 1,000대의 중장비가 필요합니다. 그러나 선거를 앞두고 자본 지출이 일시 중단됨에 따라 2025년 1-3분기 지출은 GDP의 4.2%로 축소되었으며, 윤활유 수주량은 분기마다 큰 변동을 보이고 있습니다. 여러 지역에 창고망을 갖춘 공급업체, 특히 쉘의 10개 창고와 페트론의 2만 1,000개 판매 거점 네트워크는 재고를 유연하게 조정할 수 있는 최적의 입장에 있습니다. 또한, 새로운 철도 노선과 관련된 발전 프로젝트 역시 터빈 오일 수요를 끌어올리며 프리미엄 부문을 강화하고 있습니다.

산업의 디지털화가 예측 유지보수용 윤활유 수요를 견인하고 있습니다.

정부의 “'인더스트리 4.0'프로그램과 첨단 제조 센터에서는 센서가 장착된 기계의 도입을 촉진하고 있으며, 이로 인해 수명이 긴 합성 유압유가 선호되고 있습니다. 2024년 기준으로 IoT를 활용한 유지보수 시스템을 도입한 공장은 불과 14.9%에 불과했으나, 전자 및 금속 가공 산업의 선도 기업들은 이미 ASTM D943 검사를 통해 1만 시간 이상의 내구 시간이 인증된 OEM 승인 무아연 오일을 지정하고 있습니다. ““Chevron Clarity”또는 이와 동등한 제품들은 상당히 높은 프리미엄 가격이 책정되어 있으며, 대부분의 경우 오일 품질 분석 서비스가 포함되어 있습니다. 중소규모 제조업체들은 여전히 광물유 기반 AW 68 작동유를 기본으로 사용하고 있기 때문에 쉘(Shell) 등공급업체들은 합성유로의 업셀링을 도모하기 위해 이동식 유질 분석 차량을 도입하고 있습니다. 이 비즈니스 모델은 재고량 확대와 마찬가지로 기술 인력의 증원에 달려 있습니다.

전기차와 하이브리드차의 보급 확대

RA 11697에 따른 수입 관세 및 부가가치세(VAT) 면제를 배경으로, 전기차 등록 대수는 2023년 1만 3,000대에서 2024년 중반에는 2만 1,000대로 급증했으며, 정부는 2040년까지 전기차 판매 비중을 50%로 늘리는 것을 목표로 하고 있습니다. 충전소는 멜라르코, 쉘 리차지, AC 에너지를 주축으로 2024년에 800곳을 돌파했습니다. 하이브리드 차량은 여전히 엔진 오일을 사용하지만, 그 사용량은 내연기관 차량의 약 60-70% 수준에 그칩니다. 반면, 완전 배터리식 전기차의 경우 엔진 오일이 필요하지 않습니다. 각 공급업체들은 전용 절연 냉각유를 출시함으로써 위험을 분산하고 있지만, 이러한 전환으로 인해 필리핀의 윤활유 시장의 연평균 성장률(CAGR)은 0.6포인트 하락할 것으로 예측됩니다.

부문별 분석

자동차 엔진 오일은 2025년 판매량의 33.78%를 차지했지만, 하이브리드 차량의 오일 교환 주기가 길어짐에 따라 성장 곡선은 점차 정체되는 추세를 보였습니다. 변속기 오일은 승용차에 자동변속기가 널리 보급됨에 따라 수혜를 입고 있으며, 2024년 매출의 48%를 차지했습니다. 그리스, 금속 가공용 오일, 터빈용 오일, 변압기용 오일은 여전히 틈새 시장이지만, 수익성이 높은 부문으로, 공급업체들이 부가가치가 높은 산업용 혼합 제품으로의 전환을 가속화하는 요인이 되고 있습니다. 필리핀의 윤활유 시장에서 산업용 엔진 오일 시장 규모는 2031년까지 다른 어떤 제품군보다 빠른 속도로 성장할 것으로 전망됩니다. 산업용 엔진 오일은 연평균 성장률(CAGR) 3.15%로 자동차용 등급을 상회하는 성장이 예상되며, 그 원동력은 2만 9,853 MW의 설비 용량과 고분진 부하 대응 배합이 필수적인 24시간 가동 발전기의 운영입니다.

중소규모 사업자는 위조품 피해를 입기 쉬운 대량 판매·저이익률의 자동차용 오일, 기술 지원이 필요한 소량 판매·고사양의 산업용 혼합유 중 하나를 선택해야 합니다. SEAOIL의 전략은 두 가지 측면을 모두 아우르고 있으며, 700곳 이상의 판매 거점을 활용하여 소매 수요를 촉진하는 동시에, 압착 플랜트용 ISO VG 150-320 기어 오일을 판매하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

제8장 CEO가 직면하는 중요 전략적 과제

KTHAccording to Mordor Intelligence, the philippines lubricants market size was valued at 141.55 million liters in 2025 and is estimated to grow from 144.40 million liters in 2026 to reach 170.75 million liters by 2031, at a CAGR of 3.41% during the forecast period (2026-2031).

This report is Segmented by Product Type (Automotive Engine Oil, Industrial Engine Oil, Greases, Metalworking Fluids, Turbine Oil, and More), End-User Industry (Automotive, Marine, Aerospace, Heavy Equipment, and Industrial), and Base Stock Type (Mineral Oil-Based Lubricants, Synthetic Lubricants, Semi-Synthetic Lubricants, and More). The Market Forecasts are Provided in Terms of Volume (liters).

Philippines Lubricants Market Trends and Insights

Increasing Construction Mega-Projects (Build-Better-More)

The PHP 1.545 trillion (USD 26.6 billion) outlay in 2024, equal to 5.8% of GDP, underwrites large road, rail, and bridge builds that keep excavators, cranes, and concrete mixers running in punishing duty cycles. Equipment owners shorten drain intervals, inflating demand for high-zinc hydraulic fluids and extreme-pressure greases. Projects such as the Bataan-Cavite Interlink Bridge and Metro Manila Subway require thousands of heavy machines that rely on Group II base-oil blends for soot control. Yet capital-outlay pauses before elections pared spending to 4.2% of GDP in Q1-Q3 2025, swinging lubricant orders sharply from quarter to quarter. Suppliers with multi-regional depots, notably Shell's 10 warehouses and Petron's 21,000-outlet network, are best placed to flex inventories. Power projects tied to new rail lines also lift turbine-oil pull-through, reinforcing the premium segment.

Industrial Digitalization Boosting Predictive-Maintenance Grade Lubricants

Government Industry 4.0 programs and the Advanced Manufacturing Center spur adoption of sensor-equipped machinery that favors longer-life synthetic hydraulics. Only 14.9% of factories had deployed IoT maintenance by 2024, but early movers in electronics and metalworking already specify OEM-approved zinc-free oils rated beyond 10,000 hours in ASTM D943 testing. Chevron Clarity and equivalents command sizeable premiums and often bundle oil-analysis services. Small and medium manufacturers still default to mineral-based AW 68 fluids, so vendors such as Shell push mobile oil-analysis vans to up-sell synthetics, a model that hinges on scaling technical staff as much as stock volume.

Growing Penetration of Electric and Hybrid Vehicles

EV registrations jumped from 13,000 in 2023 to 21,000 by mid-2024 on the back of import-duty and VAT exemptions under RA 11697, and the government targets a 50% EV sales mix by 2040. Charging stations surpassed 800 sites in 2024, anchored by Meralco, Shell Recharge, and AC Energy. Hybrids still use engine oil but at roughly 60-70% of internal-combustion volume; full battery EVs eliminate it. Suppliers hedge by launching specialized dielectric-cooling fluids, yet the transition is expected to shave 0.6 percentage points off the Philippines lubricants market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Ride-Hailing and Motorcycle Fleets Demanding High-Temperature 4T Oils

- OEM-Backed Low-Viscosity Synthetic Oils with Extended-Warranty Pull-Through

- Proliferation of Counterfeit/Adulterated Lubricants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive Engine Oil, while still accounting for 33.78% of 2025 volume, faces a gradually flattening curve as hybrids lengthen drain intervals. Transmission fluids benefit from automatic-transmission uptake in passenger cars, now 48% of 2024 sales. Greases, metalworking, turbine, and transformer oils remain niche but margin-rich pockets, reinforcing supplier moves toward value-added industrial blends. The Philippines lubricants market size for Industrial Engine Oil is projected to grow faster than any other product family through 2031. Industrial Engine Oil is poised to outpace automotive grades at a 3.15% CAGR, fueled by 29,853 MW of installed power capacity and around-the-clock genset operations that mandate high-soot-load formulations.

Smaller players must pick sides: high-volume, low-margin automotive oils vulnerable to counterfeits, or low-volume, high-spec industrial blends that require technical support. SEAOIL's strategy spans both, leveraging 700+ stations for retail pull while marketing ISO VG 150-320 gear oils to crushing plants.

Complete Report Scope:

- By Product Type

- Automotive Engine Oil

- Industrial Engine Oil

- Transmission Fluids

- Gear Oil

- Brake Fluids

- Hydraulic Fluids

- Greases

- Process Oil (Including Rubber Process Oil and White Oil)

- Metalworking Fluids

- Turbine Oil

- Transformer Oil

- Other Product Types

- By End-user Industry

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

- Marine

- Aerospace

- Heavy Equipment

- Construction

- Mining

- Agriculture

- Industrial

- Power Generation

- Metallurgy and Metalworking

- Textiles

- Oil and Gas

- Other End-Use Industries

- Automotive

- By Base Stock Type

- Mineral Oil-Based Lubricants

- Synthetic Lubricants

- Semi-Synthetic Lubricants

- Bio-Based Lubricants

List of Companies Covered in this Report:

- BP plc

- Chevron Corporation

- China Petroleum & Chemical Corporation

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil International

- Idemitsu Kosan (ENEOS)

- Liqui Moly

- Motul

- Petron Corporation

- PETRONAS Lubricant International

- Phoenix Petroleum

- PTT Lubricants

- Rainchem International Inc.

- Repsol

- Saudi Arabian Oil Co.

- SEAOIL Philippines, Inc.

- Shell plc

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing construction mega-projects (Build-Better-More)

- 4.2.2 Industrial digitalization boosting predictive-maintenance grade lubricants

- 4.2.3 Rapid growth of ride-hailing and motorcycle fleets demanding high-temperature 4T oils

- 4.2.4 OEM-backed low-viscosity synthetic oils with extended-warranty pull-through

- 4.2.5 E-commerce live-selling and quick-lube bay expansion widening retail access

- 4.3 Market Restraints

- 4.3.1 Growing penetration of electric and hybrid vehicles

- 4.3.2 Proliferation of counterfeit/adulterated lubricants

- 4.3.3 Tightening used-oil circular-economy compliance costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 End-User Trends

- 4.6.1 Automotive Industry

- 4.6.2 Manufacturing Industry

- 4.6.3 Power Generation Industry

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.2 Industrial Engine Oil

- 5.1.3 Transmission Fluids

- 5.1.4 Gear Oil

- 5.1.5 Brake Fluids

- 5.1.6 Hydraulic Fluids

- 5.1.7 Greases

- 5.1.8 Process Oil (Including Rubber Process Oil and White Oil)

- 5.1.9 Metalworking Fluids

- 5.1.10 Turbine Oil

- 5.1.11 Transformer Oil

- 5.1.12 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.1.1 Passenger Vehicles

- 5.2.1.2 Commercial Vehicles

- 5.2.1.3 Two-Wheelers

- 5.2.2 Marine

- 5.2.3 Aerospace

- 5.2.4 Heavy Equipment

- 5.2.4.1 Construction

- 5.2.4.2 Mining

- 5.2.4.3 Agriculture

- 5.2.5 Industrial

- 5.2.5.1 Power Generation

- 5.2.5.2 Metallurgy and Metalworking

- 5.2.5.3 Textiles

- 5.2.5.4 Oil and Gas

- 5.2.5.5 Other End-Use Industries

- 5.2.1 Automotive

- 5.3 By Base Stock Type

- 5.3.1 Mineral Oil-Based Lubricants

- 5.3.2 Synthetic Lubricants

- 5.3.3 Semi-Synthetic Lubricants

- 5.3.4 Bio-Based Lubricants

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 BP plc

- 6.4.2 Chevron Corporation

- 6.4.3 China Petroleum & Chemical Corporation

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FUCHS

- 6.4.6 Gulf Oil International

- 6.4.7 Idemitsu Kosan (ENEOS)

- 6.4.8 Liqui Moly

- 6.4.9 Motul

- 6.4.10 Petron Corporation

- 6.4.11 PETRONAS Lubricant International

- 6.4.12 Phoenix Petroleum

- 6.4.13 PTT Lubricants

- 6.4.14 Rainchem International Inc.

- 6.4.15 Repsol

- 6.4.16 Saudi Arabian Oil Co.

- 6.4.17 SEAOIL Philippines, Inc.

- 6.4.18 Shell plc

- 6.4.19 TotalEnergies

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-Need Assessment