|

시장보고서

상품코드

2072565

전자 약물전달 시스템 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2030년)Electronic Drug Delivery Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

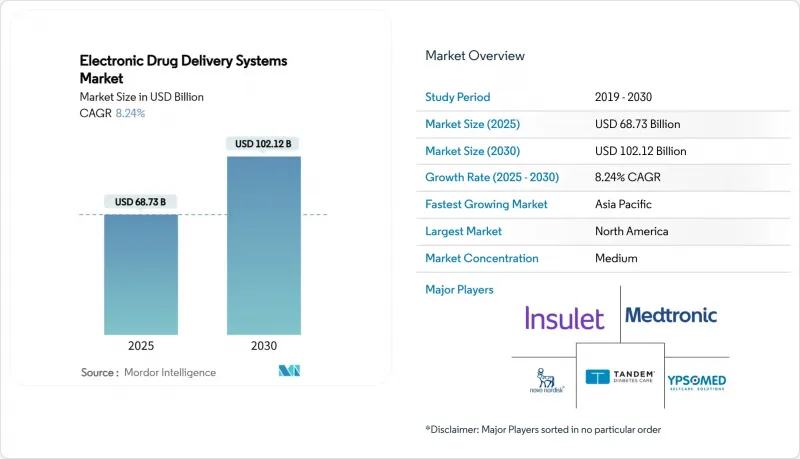

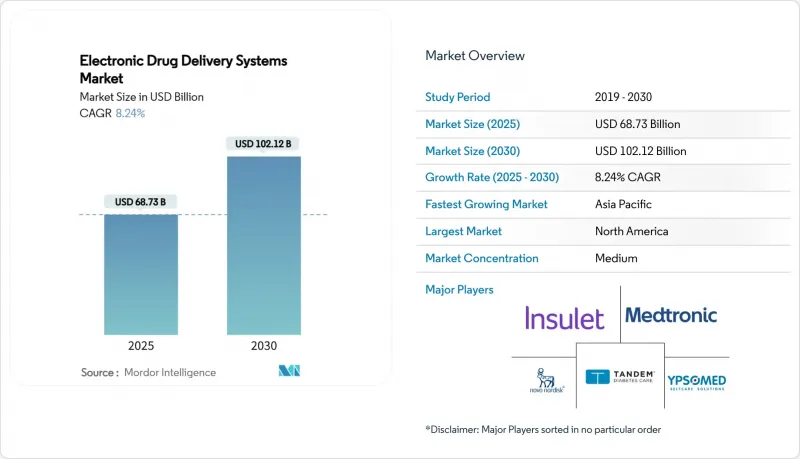

Mordor Intelligence에 의하면, 전자 약물전달 시스템 시장 규모는 2025년에 687억 3,000만 달러로 평가되었습니다. 2030년까지 1,021억 2,000만 달러에 이를 것으로 예상되며, 예측 기간 중 연평균 복합 성장률(CAGR)은 8.24%를 나타낼 전망입니다.

본 보고서는 제품 유형(인슐린 펌프, 웨어러블 주사기, 스마트 흡입기, 스마트 알약, 이식형 주입 펌프 등), 용도(당뇨병, 호흡기 질환 등), 최종 사용자(병원 및 진료소 등), 기술(전자식 등), 구성 요소(하드웨어 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 전자 약물전달 시스템 시장 동향 및 인사이트

당뇨병 및 만성 질환의 유병률 증가

5억 3,700만 명 이상의 성인이 당뇨병을 앓고 있으며, 그 수가 계속 증가하고 있기 때문에 지속적이고 자동화된 인슐린 투여는 치료에 있어 필수적인 축이 되고 있습니다. 7세 이상의 소아를 대상으로 한 MiniMed 780G 시스템의 FDA 승인은 질환 관리의 부담을 줄여주는 폐쇄 루프 솔루션에 대해 규제 당국이 도입의 길을 마련해 나가고 있음을 보여줍니다. 이와 유사한 추세가 통증 치료 분야에서도 나타나고 있는데, 이는 FDA가 애보트사의 ‘Proclaim’ 척수 자극 플랫폼을 당뇨병성 신경병증 치료 용도로 승인함에 따라, 전자 투여가 치료 분야의 경계를 넘어설 수 있음을 입증하고 있습니다. 고령화에 따라 만성 질환에 대한 치료 수요가 증가하는 가운데, 실제 임상 데이터를 통해 자동 투여 시스템이 수동 요법에 비해 당화 헤모글로빈 수치를 낮추는 것으로 확인되었습니다. 보험사들은 고가의 합병증으로 인한 입원을 방지하는 수단으로서 첨단 펌프와 센서를 점점 더 중요하게 여기고 있으며, 이로 인해 전자 약물 투여 시스템 시장의 구조적인 상승 추세가 확고해지고 있습니다.

웨어러블/패치형 펌프의 보급 확대

소형화된 체내 착용형 주사기는 내원 횟수를 줄이고 여러 번에 걸친 투여 요법을 간소화함으로써 환자의 기대를 새롭게 정의하고 있습니다. Enable Injections사는 자사 제품인 ‘enFuse’의 출시 후 4개월 만에 60%의 도입률을 달성했다고 보고했으며, 이는 눈에 띄지 않는 디자인이 이용 지속률을 높인다는 사실을 입증하고 있습니다. 해당 플랫폼을 통해 투여되는 피하 투여용 이사츠키맙의 3상 임상시험 데이터에 따르면, 정맥 내 투여 요법에 비해 비열등성이 확인되었을 뿐만 아니라 삶의 질(QOL) 지표도 개선된 것으로 나타나, 암 치료 분야에서 재택 생물학적 제제 투여로의 전환이 진행되고 있음을 시사하고 있습니다. 고점도 바이오의약품에 관한 BD와 Ypsomed의 제휴 등, 기존 주요 기업들이 시장 점유율을 지키기 위해 패치 기술을 중심으로 사업 재편을 추진하고 있음을 알 수 있습니다. 새로 공개된 FDA의 지침안은 성능 기준을 명확히 함으로써, 혁신 기업들에게 존재하던 규제상의 모호함을 해소하고 있습니다. 미국 보험사의 82%가 사용하기 편리한 웨어러블 펌프에 대한 보험 적용에 긍정적인 태도를 보이고 있으며, 보험사들의 도입이 가속화되고 있습니다.

의료기기 리콜 및 안전성과 관련된 소송 위험

2023년부터 2024년에 걸쳐 잇달아 발생한 클래스 I 인슐린 및 주입 펌프 리콜은 임상의들의 신뢰를 흔들었고, 막대한 비용이 소요되는 소송을 촉발했습니다. 배터리 수명 문제, 액체 누출, 막힘 등으로 인해 대규모 교체가 불가피하게 되었으며, FDA의 시판 후 감시가 강화되면서 신제품 심사 기간이 길어졌습니다. 법적 합의로 인해 보험료가 상승하면서 연구개발(R&D)에 대한 자본 배분이 압박을 받고 있습니다. 견고한 품질 관리 체계를 갖추지 못한 중소기업들은 존폐의 위기에 직면해 있으며, 시장 재편이 가속화되고 있습니다. 장기적으로는 엄격한 감독을 통해 안전성 기준이 향상될 전망이지만, 전자 약물전달 시스템 시장에 미치는 단기적인 부정적 영향은 여전히 지속되고 있습니다.

부문별 분석

인슐린 펌프는 2024년 매출의 27.32%를 차지하며, 수십 년에 걸친 임상적 검증과 보험 적용을 통해 그 효과가 입증되었습니다. 한편, 스마트 흡입기는 흡입용 코르티코스테로이드를 응급 치료제로 활용하는 ‘에어수프라(Airsupra)’ 병용 요법이 FDA로부터 획기적인 승인을 받은 데 힘입어 연평균 성장률(CAGR) 12.94%로 성장하고 있습니다. 이러한 규제상의 획기적인 변화는 사용 현황을 추적하고, 복약 순응도 데이터를 의료진에게 전송하는 센서 내장형 흡입기에 대한 연구 개발 투자를 촉진하고 있습니다. 또한, 고점도 생물학적 제제를 대상으로 한 제휴를 통해 웨어러블 주사기도 호조를 보이고 있는 반면, 자동 주사기는 응급 의료 분야에서 여전히 중요한 위치를 차지하고 있습니다. 호흡기 치료의 디지털화가 진행됨에 따라, 예측 기간 동안 스마트 흡입기를 활용한 전자 약물전달 시스템 시장 규모는 증분 달러 기준으로 펌프를 상회할 것으로 전망됩니다. 경쟁의 초점은 클라우드 연결성, 투여량 추적 정확도, 그리고 접근성 확대를 목표로 하는 사용량 기반 금융 모델에 집중되고 있습니다.

동시에 제품 라인업도 다양해지고 있습니다. 스마트 필은 마이크로 카메라와 원격 측정 기능을 통합하여, 한 번의 복용으로 표적 부위에 정확히 전달하고 진단을 동시에 수행하지만, 그 보급은 환자의 수용도와 보험 급여 적용 여부에 따라 좌우됩니다. 이식형 주입 펌프는 수술 없이도 작동 수명을 연장해 주는 에너지 수확 방식의 전원 공급 장치의 이점을 누리고 있으며, 종양학 및 통증 치료 분야에서 차별화된 가치를 약속합니다. 모든 분야에서 각 제조업체들은 견고한 하드웨어와 변화하는 생리적 징후에 맞추어 투여량을 조절하는 적응형 소프트웨어를 융합하기 위해 경쟁하고 있으며, 이를 통해 전자 약물전달 시스템 시장의 성능 기준을 재정의하고 있습니다.

당뇨병 분야는 통합형 CGM(연속 혈당 모니터링)과 펌프 생태계, 그리고 보험사를 위한 강력한 근거 기반에 힘입어 2024년 매출의 39.53%를 차지했습니다. 그러나 폐쇄 루프 방식의 척수 자극 장치와 실시간 신호 분석이 가능한 AI 제어형 통증 관리 임플란트 덕분에 신경 질환 분야가 연평균 성장률(CAGR) 10.34%로 가장 빠르게 성장하고 있습니다. Proclaim SCS 플랫폼의 적응증 확대를 통해 대상 임상 분야의 폭이 넓어졌음이 입증되었으며, 편두통 및 운동 장애 분야에서의 새로운 연구 개발이 촉진되고 있습니다. 개발 중인 기기가 규제상의 장벽을 극복한다면, 신경 질환 치료용 전자 약물전달 시스템 시장 규모는 2030년까지 두 배로 늘어날 전망입니다.

호흡기 질환 분야에서는 스마트 흡입기의 보급에 힘입어 꾸준한 성장이 이어지고 있습니다. 한편, 종양학 분야에서는 정맥 내 투여에서 체표 피하 투여로 전환이 진행되고 있으며, 이를 통해 병원의 수용 능력 절약과 환자의 편의성 향상이 실현되고 있습니다. 심혈관 질환 프로그램에서는 심부전 치료제의 투여량을 조절하기 위한 휴대용 펌프가 시험되고 있는 반면, 소화기 및 내분비계 질환 분야에서는 경구 투여형 센서 요법의 혜택을 가장 먼저 누리고 있습니다. 이처럼 치료 영역이 확대됨에 따라, 공급업체는 약물 카세트와 알고리즘 패키지를 교체할 수 있는 모듈형 플랫폼을 구축하여 제품 수명 주기 전반에 걸쳐 유연성을 확보해야 합니다.

지역별 분석

북미는 선진적인 지불자 제도, FDA의 적극적인 지침, 그리고 디지털 헬스의 깊은 확산에 힘입어 2024년 매출의 41.23%를 차지했습니다. 메디케어의 최신 지급 일정은 재택 치료의 적격성을 더욱 확고히 하고, 지역 내 수요 증가의 기반을 공고히 하고 있습니다. 또한, 제524B조의 엄격한 시행으로 인해 해당 지역은 사이버 보안 규정 준수 분야의 벤치마크가 되었으며, 간접적으로 전 세계 공급업체들의 설계 기준을 정립하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 10.89%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 중국에서는 스마트팜프의 생산 능력을 확대하고 있는 반면, 일본과 호주에서는 조화로운 심사 체계 하에서 AI 탑재 기기의 승인을 가속화하고 있습니다. 인도의 ‘아유슈만 바라트’ 디지털 헬스 인프라를 통해 현지 의료 제공업체들은 클라우드 기반 의료 서비스로 획기적인 전환을 이룰 수 있게 되었습니다. 지역 제조업체들은 국내 수요와 EU·미국의 기준을 모두 충족하는 설계를 점점 더 적극적으로 추진하고 있으며, 수출 준비가 차츰 갖춰지고 있습니다.

유럽에서는 규제를 중심으로 한 꾸준한 확대가 나타나고 있습니다. ‘의료기기 규정(MDR)’의 시행으로 인해 일부 일정이 지연되었지만, 결과적으로는 품질에 대한 평가를 높이는 동시에 BD와 Ypsomed의 제휴를 통해 고점도용 웨어러블 주사기의 보급을 촉진하고 있습니다. 중부 및 동유럽의 보험사들에서는 자동 인슐린 투여 기기에 대한 시범적인 보험 적용이 시작되면서, 대상 환자층이 확대되고 있습니다. 남미, 중동 및 아프리카에서는 신흥 시장 특유의 동향이 나타나고 있습니다. 도시 지역의 엘리트 계층은 최첨단 기술을 도입하고 있지만, 보다 광범위한 보급을 위해서는 비용 절감 모델과 공공 부문의 보상 제도 개혁이 시급히 요구되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.03According to Mordor Intelligence, the electronic drug delivery systems market size stands at USD 68.73 billion in 2025 and is projected to reach USD 102.12 billion by 2030, reflecting an 8.24% CAGR over the forecast period.

This report is Segmented by Product Type (Insulin Pumps, Wearable Injectors, Smart Inhalers, Smart Pills, Implantable Infusion Pumps, and More), Application (Diabetes, Respiratory Diseases, and More), End User (Hospitals & Clinics, and More), Technology (Electronic, and More), Component (Hardware and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Electronic Drug Delivery Systems Market Trends and Insights

Rising Diabetes & Chronic Disease Prevalence

More than 537 million adults live with diabetes, and the figure is climbing, making continuous, automated insulin delivery an essential therapeutic pillar. FDA clearance of the MiniMed 780G system for children as young as 7 shows how regulators are smoothing pathways for closed-loop solutions that lighten disease-management burdens. Similar momentum is visible in pain medicine after the FDA green-lit Abbott's Proclaim spinal cord stimulation platform for diabetic neuropathy, proving electronic delivery can cross therapeutic silos. Ageing populations amplify chronic-care volumes, and real-world data confirm automated delivery systems cut glycated-haemoglobin levels versus manual regimens. Payers increasingly view advanced pumps and sensors as a hedge against expensive, complication-driven admissions, cementing a structural upswing for the electronic drug delivery systems market.

Growing Adoption of Wearable/Patch Pumps

Miniaturised, on-body injectors are reshaping patient expectations by reducing clinic visits and simplifying multi-dose regimens. Enable Injections reported 60% uptake of its enFuse device within four months of launch, underlining how discreet form factors drive stickiness.Phase 3 data for subcutaneous isatuximab delivered via the same platform met non-inferiority against IV therapy while boosting quality-of-life metrics, signalling oncology's pivot toward at-home biologic administration. Partnerships such as BD-Ypsomed's alliance on high-viscosity biologics show incumbent players repositioning around patch technology to defend share. Newly issued FDA draft guidance clarifies performance benchmarks, trimming regulatory ambiguity for innovators. With 82% of US insurers expressing willingness to cover user-friendly wearable pumps, payers are accelerating adoption curves.

Device Recalls & Safety Litigation Exposure

A spate of Class I insulin and infusion pump recalls during 2023-24 rattled clinician confidence and triggered cost-intensive litigation. Battery life faults, fluid leaks, and occlusions forced large-scale replacements, tightening FDA post-market surveillance and elongating new-product review. Legal settlements inflate insurance premiums and redirect capital away from R&D. Smaller players lacking robust quality systems face existential threats, accelerating market consolidation. Over time, stringent oversight should raise baseline safety, yet near-term drag on the electronic drug delivery systems market persists.

Other drivers and restraints analyzed in the detailed report include:

- Favourable Reimbursement & Home-Care Push

- Miniaturisation & Smart-Mobile Connectivity

- High Device Cost & Reimbursement Gaps In Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Insulin pumps delivered 27.32% of 2024 revenue, validating decades of clinical proof and insurance coverage. Smart inhalers, however, are expanding at a 12.94% CAGR, propelled by the FDA's landmark approval of the Airsupra combination therapy that repositions inhaled corticosteroids as rescue medication. This regulatory milestone galvanises R&D investment in sensor-embedded inhalers that track usage and transmit adherence data to care teams. Wearable injectors are also gaining favourable momentum through partnerships targeting high-viscosity biologics, while auto-injectors sustain emergency-medicine relevance. The electronic drug delivery systems market size for smart inhalers is projected to outpace pumps in incremental dollar terms over the forecast window as respiratory care digitalises. Competitive jockeying centres on cloud connectivity, dose-tracking precision, and pay-per-use financing aimed at widening access.

The product landscape is simultaneously diversifying. Smart pills integrate micro-cameras and telemetry to perform targeted GI delivery and diagnostics in a single pass, though uptake hinges on patient acceptance and reimbursement clarity. Implantable infusion pumps benefit from energy-harvested power sources that extend functional life without surgery, promising differentiated value in oncology and pain medicine. Across categories, manufacturers race to blend robust hardware with adaptive software that tailors dosing to shifting physiological cues, redefining performance benchmarks for the electronic drug delivery systems market.

Diabetes retained 39.53% of 2024 revenue, supported by integrated CGM-pump ecosystems and strong payer evidence bases. Yet neurological disorders are climbing fastest at a 10.34% CAGR, thanks to closed-loop spinal cord stimulators and AI-modulated pain implants capable of real-time signal interpretation. On-label expansion of Proclaim SCS platforms validates a broader clinical addressable base, triggering fresh R&D in migraine and movement disorders. The electronic drug delivery systems market size for neurological applications is on track to double by 2030 if pipeline devices clear regulatory hurdles.

Respiratory disease applications continue stable growth underpinned by smart inhaler penetration, while oncology is pivoting from IV to on-body subcutaneous delivery, unlocking hospital-capacity savings and improved patient comfort. Cardiovascular programmes are testing ambulatory pumps for heart-failure medication titration, whereas GI and endocrine disorders are early beneficiaries of ingestible sensor therapy. This widening therapeutic canvas compels suppliers to architect modular platforms able to swap drug cassettes and algorithm packages, ensuring lifecycle flexibility.

Complete Report Scope:

- By Product Type

- Insulin Pumps

- Wearable Injectors

- Smart Inhalers

- Smart Pills

- Implantable Infusion Pumps

- Transdermal Patches

- Auto-Injectors

- Microneedle Patches

- By Application

- Diabetes

- Respiratory Diseases (Asthma, COPD)

- Pain Management

- Oncology

- Cardiovascular Diseases

- Neurological Disorders

- Gastro-intestinal Disorders

- Hormone Therapy

- By End User

- Hospitals & Clinics

- Ambulatory Surgery Centers

- Home-care Settings

- Specialty Clinics

- By Technology

- Electronic

- Connected / IoT-Enabled

- Closed-loop / AI-Based

- By Component

- Hardware

- Software & Algorithms

- Connectivity Platform

- Sensors & Power Modules

- Consumables / Cartridges

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America generated 41.23% of 2024 revenue, underpinned by advanced payer systems, proactive FDA guidance, and deep digital-health adoption. Medicare's latest payment schedule further cements home-based eligibility, solidifying a local demand runway. Tight enforcement of Section 524B also makes the region a bellwether for cybersecurity compliance, indirectly setting design norms for global vendors.

Asia-Pacific is the fastest-growing cluster at 10.89% CAGR. China scales production capacity for smart pumps, while Japan and Australia accelerate approvals for AI-enabled devices under harmonised review frameworks. India's Ayushman Bharat digital-health backbone positions local providers to leapfrog into cloud-connected care. Regional manufacturers increasingly design for both domestic need and EU/US standards, raising export readiness.

Europe shows steady, regulation-driven expansion. Implementation of Medical Device Regulation has elongated some timelines but ultimately boosts quality perception, aiding adoption of high-viscosity wearable injectors through BD-Ypsomed collaborations. Central- and Eastern-European payers begin pilot reimbursements for automated insulin delivery, widening the addressable cohort. South America, Middle East, and Africa display emerging-market dynamics: an urban elite adopts premium tech, but broader diffusion awaits cost-down models and public-sector reimbursement reform.

- Insulet

- Medtronic

- Novo Nordisk

- Tandem Diabetes Care

- Ypsomed

- Becton Dickinson & Co.

- Johnson & Johnson

- Abbott Laboratories

- Baxter

- Boston Scientific

- Bayer

- Pfizer

- GlaxoSmithKline

- AstraZeneca

- Enable Injections

- Amgen

- Eli Lilly and Company

- Solventum

- Roche

- Teva Pharmaceutical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diabetes & Chronic Disease Prevalence

- 4.2.2 Growing Adoption Of Wearable/Patch Pumps

- 4.2.3 Favourable Reimbursement & Home-Care Push

- 4.2.4 Miniaturisation & Smart-Mobile Connectivity

- 4.2.5 Mandatory Cybersecurity Updates For Connected Devices

- 4.2.6 Energy-Harvesting Micro-Batteries Enabling Long-Life Implants

- 4.3 Market Restraints

- 4.3.1 Device Recalls & Safety Litigation Exposure

- 4.3.2 High Device Cost & Reimbursement Gaps In Ems

- 4.3.3 Complex Multi-Jurisdiction Regulatory Pathways

- 4.3.4 Semiconductor Supply-Chain Volatility For MCUs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product Type

- 5.1.1 Insulin Pumps

- 5.1.2 Wearable Injectors

- 5.1.3 Smart Inhalers

- 5.1.4 Smart Pills

- 5.1.5 Implantable Infusion Pumps

- 5.1.6 Transdermal Patches

- 5.1.7 Auto-Injectors

- 5.1.8 Microneedle Patches

- 5.2 By Application

- 5.2.1 Diabetes

- 5.2.2 Respiratory Diseases (Asthma, COPD)

- 5.2.3 Pain Management

- 5.2.4 Oncology

- 5.2.5 Cardiovascular Diseases

- 5.2.6 Neurological Disorders

- 5.2.7 Gastro-intestinal Disorders

- 5.2.8 Hormone Therapy

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Home-care Settings

- 5.3.4 Specialty Clinics

- 5.4 By Technology

- 5.4.1 Electronic

- 5.4.2 Connected / IoT-Enabled

- 5.4.3 Closed-loop / AI-Based

- 5.5 By Component

- 5.5.1 Hardware

- 5.5.2 Software & Algorithms

- 5.5.3 Connectivity Platform

- 5.5.4 Sensors & Power Modules

- 5.5.5 Consumables / Cartridges

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Insulet Corporation

- 6.3.2 Medtronic plc

- 6.3.3 Novo Nordisk A/S

- 6.3.4 Tandem Diabetes Care

- 6.3.5 Ypsomed AG

- 6.3.6 Becton Dickinson & Co.

- 6.3.7 Johnson & Johnson (Janssen)

- 6.3.8 Abbott Laboratories

- 6.3.9 Baxter International

- 6.3.10 Boston Scientific

- 6.3.11 Bayer AG

- 6.3.12 Pfizer Inc.

- 6.3.13 GlaxoSmithKline plc

- 6.3.14 AstraZeneca plc

- 6.3.15 Enable Injections

- 6.3.16 Amgen Inc.

- 6.3.17 Eli Lilly and Company

- 6.3.18 Solventum

- 6.3.19 F. Hoffmann-La Roche Ltd

- 6.3.20 Teva Pharmaceutical Industries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment