|

시장보고서

상품코드

2072570

생약 의약품 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Herbal Medicinal Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

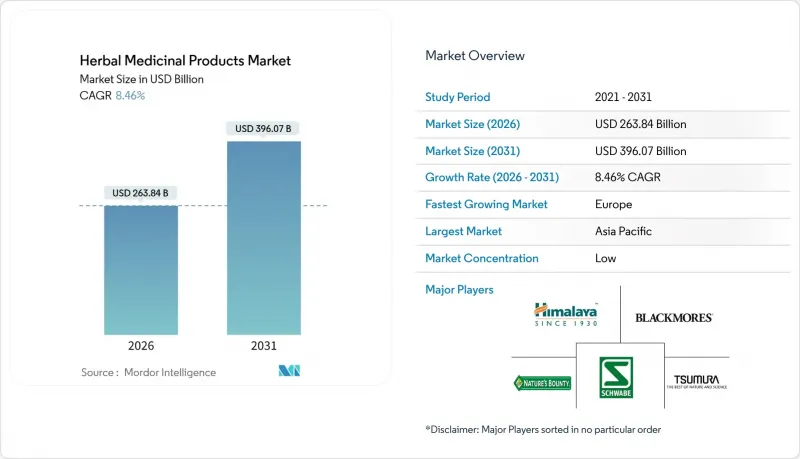

Mordor Intelligence에 의하면, 생약 의약품 시장 규모는 2026년에 2,638억 4,000만 달러로 추정되고 예측 기간(2026-2031년)에서 CAGR 8.46%로 확대되어 2031년에는 3,960억 7,000만 달러에 이를 전망입니다.

본 보고서는 제품 유형(생약 의약품, 허브 영양보조식품, 기타), 원료(잎, 뿌리·뿌리줄기, 기타), 제형(정제 및 캡슐, 분말·과립, 기타), 유통 채널(병원·소매 약국, 기타), 약용 식물 유형(알로에 베라, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 생약 의약품 시장 동향 및 인사이트

전 세계 소비자들은 천연 유래의 식물성 일반의약품으로 전환하고 있습니다.

2023년 전 세계 판매 데이터에 따르면, 경제의 불확실성 속에서도 식물성 건강기능식품은 견조한 성장세를 보였으며, 예방적 건강 관리를 추구하는 모든 연령층에서 지속적인 수요가 두드러지게 나타났습니다. 사이리움이나 비트루트 등의 성분에 대한 과학적 근거가 점점 더 확고해지고 있는 점은 구매에 대한 신뢰감을 높여주고 있습니다. 유럽의 소비자 행동도 이러한 추세를 반영하고 있으며, 규제 체계는 기존의 지식을 제한하지 않으면서 증거에 기반한 효능 표기를 장려하고 있습니다. 이러한 지속적인 소비 행태의 변화가 생약 의약품 시장의 꾸준한 성장을 뒷받침하고 있습니다.

선진 규제 당국이 제품 출시까지 걸리는 기간을 단축하고 있습니다.

2024년에 개정된 “"신규 식품 성분 신고(NDN)" 이 지침을 통해 기업들은 마스터 파일을 참조할 수 있게 되었으며, 개발 주기를 최대 2년까지 단축할 수 있게 되었습니다. 중국의 “"전통 중국 의학 규제 과학(TCM Regulatory Science)" 이 이니셔티브에서는 AI를 활용해 신청 서류 평가 과정을 신속하게 진행하고 있어, 소규모 혁신가들에게 더 많은 기회가 열리고 있습니다. FDA의 자원 제약으로 인해 심사가 지연될 가능성은 있지만, 전반적으로 규제 투명성이 높아지고 있는 점이 생약 의약품 시장에 호재로 작용하고 있습니다.

원료 위조와 공급 충격

빌베리, 크랜베리, 톱야자에서 발생하는 경제적 위조는 브랜드 평판을 훼손할 뿐만 아니라, 진위 여부를 확인하기 위한 DNA 바코딩에 대한 투자를 불가피하게 만들고 있습니다. 기후 변화로 인한 수확 차질이 더욱 심화되면서 가격이 급등하고 있으며, 이는 생약 의약품 시장 전체의 이익률을 압박하고 있습니다.

부문별 분석

2025년, 허브 영양보조식품은 생약 의약품 시장 점유율의 22.56%를 차지하며, 캡슐이나 정제에 대한 소비자의 신뢰가 확고히 자리 잡았음을 반영했습니다. 기능성 식음료 시장은 소비자들이 식물 유래 성분을 개별 정제 형태가 아닌 일상적인 식습관에 접목하기 시작함에 따라, 2031년까지 연평균 성장률(CAGR) 8.29%를 나타낼 것으로 전망됩니다. 현재 스포츠 영양 브랜드에서는 합성 자극제의 대체재로 아슈와간다, 동충하초, 로디올라를 수분 보충 음료에 배합하고 있습니다. 이러한 변화로 인해 이용 장면이 확대되면서, 소매업체들은 레디 투 드링크(RTD) 유형의 제품에 더 많은 진열 공간을 할당하도록 장려받고 있습니다.

발효 기술과 정밀 추출 기술을 통해 생리활성 성분이 안정화됨에 따라, 제조업체는 풍미가 뛰어난 제품에서 일관된 함량을 보장할 수 있게 되었습니다. 이러한 발전은 효모를 이용해 알테피린 C 등의 주요 화합물을 생산함으로써 원료 부족을 완화하고, 공급 안정성을 높이고 있습니다. 이익률 향상 가능성이 높아짐에 따라 마케팅 비용이 증가하고, 소비자 도달 범위가 확대됨에 따라 기능성 식품은 향후 생약 의약품 시장 확대의 주요 원동력으로서의 역할을 강화하고 있습니다.

2025년에는 이미 자리 잡은 녹차 및 은행나무 제품 파이프라인 덕분에, 잎이 생약 의약품 시장 규모의 20.93%를 차지했습니다. 꽃과 나무 껍질은 특정 효능이 인정받는 안토시아닌, 살리신, 프로안토시아니딘을 풍부하게 함유하고 있어, 현재 7.38%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 수확 기간이 제한적이고 특수한 가공 공정이 필요하기 때문에 프리미엄 가격이 책정되어, 수량이 중간 정도라 하더라도 수익을 끌어올리고 있습니다.

추출 기술의 발전으로 섬세한 꽃이나 나무 껍질의 성분을 효과적으로 추출할 수 있게 되었으며, 한편 지속가능성 관련 인증은 윤리적인 조달에 대해 구매자에게 안심감을 주고 있습니다. 각 브랜드는 테루아르와 계절의 이야기를 전면에 내세우며, 높은 가격 책정의 정당성을 강조하고 있습니다. 소비자들이 틈새 시장의 생리활성 물질을 찾으면서, 수요는 과거에는 부차적인 것으로 여겨졌던 이러한 식물 부위로 이동하고 있으며, 이로 인해 생약 의약품 시장공급망이 다양화되고 평균 판매 가격도 상승하고 있습니다.

지역별 분석

북미는 투명성이 높은 규제 체계와 높은 재량 지출에 힘입어 2025년 생약 의약품 시장 매출의 28.94%를 차지했습니다. 개정된 FDA 지침에 따라 관료적 마찰이 완화되고 혁신이 촉진되고 있습니다. 소비자들은 2023년에 매출이 108% 증가한 비트루트 등, 과학적 근거에 기반한 식물성 제품을 점점 더 많이 선택했습니다.

아시아태평양은 전통 의학을 국가 의료 시스템에 통합하려는 정부의 이니셔티브에 힘입어, 2031년까지 연평균 성장률(CAGR) 7.90%라는 가장 높은 성장률을 달성할 것으로 전망됩니다. 중국의 전통 의학 정책과 인도의 영양 보조제 규제 확대는 스타트업과 다국적 기업 모두에게 동등한 기회를 제공합니다. 인도산 식물 유래 원료의약품은 전 세계 생약 의약품 공급망에서 중요한 차별화 요인으로 부상하고 있습니다. 일본의 인구 고령화는 인지 기능과 관절 건강을 지원하는 제제에 대한 수요를 높이고 있는 반면, 동남아시아의 생물 다양성은 원료 조달을 뒷받침하고 있습니다.

유럽에서는 기존 사용법 및 안전성에 관한 문서화의 균형을 도모하는 지침 2004/24/EC에 따라 꾸준한 성장이 이어지고 있습니다. 독일의 자연요법 문화가 지역 수요의 기반이 되고 있으며, 영국도 브렉시트 이후의 재편에도 불구하고 그 중요성을 유지하고 있습니다. 중동 및 아프리카의 신흥 시장에는 잠재력이 보이지만, 생약 의약품 시장에 본격적으로 진출하기 위해서는 인프라 및 규제 측면의 격차를 해소해야 합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

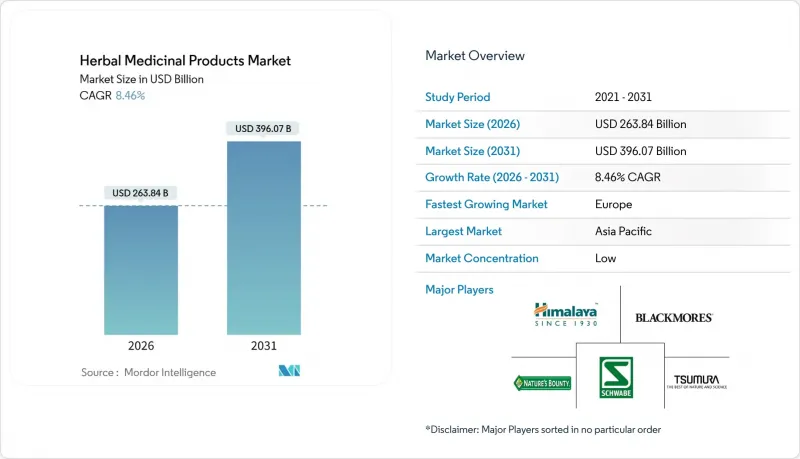

KTH 26.07.03According to Mordor Intelligence, the herbal medicinal products market size is estimated at USD 263.84 billion in 2026, and is expected to reach USD 396.07 billion by 2031, at a CAGR of 8.46% during the forecast period (2026-2031).

This report is Segmented by Product Type (Herbal Pharmaceuticals, Herbal Dietary Supplements, and More), Source (Leaves, Roots & Rhizomes, and More), Form (Tablets & Capsules, Powders & Granules, and More), Distribution Channel (Hospital & Retail Pharmacies, and More), Medicinal Plant Type (Aloe Vera, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Herbal Medicinal Products Market Trends and Insights

Consumers worldwide have shifted toward natural, plant-based OTC remedies

Global sales data from 2023 showed resilient growth for botanical supplements, even amid economic uncertainty, highlighting sustained demand across age groups seeking preventive wellness. Expanding scientific validation of ingredients such as psyllium and beetroot reinforces purchase confidence. European consumer behavior mirrors this trend as regulatory structures encourage evidence-based claims without restricting traditional knowledge. The ongoing behavioral pivot underpins steady expansion of the herbal medicinal products market.

Progressive regulators are shortening launch timelines

Revised New Dietary Ingredient Notification guidance in 2024 allows companies to reference Master Files, cutting development cycles by up to two years. China's Traditional Chinese Medicine Regulatory Science initiative employs AI for faster dossier evaluation, broadening opportunities for small innovators. While resource constraints at the FDA could slow inspections, overall regulatory clarity continues to buoy the herbal medicinal products market.

Raw-material adulteration & supply shocks

Economic adulteration of bilberry, cranberry, and saw palmetto undermines brand reputation and compels investment in DNA barcoding to confirm authenticity. Climate volatility further disrupts harvests, creating price spikes that compress margins across the herbal medicinal products market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid penetration of e-commerce and direct-to-consumer nutraceutical brands

- AI-driven platforms are mining phytochemical databases and predicting herb-drug interactions

- Fragmented global regulatory frameworks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Herbal dietary supplements captured 22.56% of the herbal medicinal products market share in 2025, reflecting mature consumer trust in capsules and tablets. Functional foods and beverages are charting a 8.29% CAGR to 2031 as shoppers fold botanicals into daily eating rituals rather than separate pill regimens. Sports-nutrition brands now blend ashwagandha, cordyceps, and rhodiola into hydration drinks to replace synthetic stimulants. This shift expands usage occasions and nudges retailers to allocate more shelf space to ready-to-consume formats.

Fermentation and precision-extraction technologies stabilize bioactive content, allowing manufacturers to promise consistent dosing in palatable products. These advances also mitigate raw-material shortages by producing key compounds such as artepillin C in yeast, boosting supply security. Higher margin potential fuels marketing spend that widens consumer reach, reinforcing functional foods' role as the primary engine of future herbal medicinal products market expansion.

Leaves generated 20.93% of the herbal medicinal products market size in 2025 thanks to entrenched green-tea and ginkgo pipelines. Flowers and bark now deliver the highest 7.38% CAGR because they contain dense anthocyanins, salicins, and proanthocyanidins prized for targeted benefits. Limited harvest windows and specialized processing underpin premium pricing that lifts revenue even on moderate volumes.

Enhanced extraction hardware unlocks delicate floral and woody matrices, while sustainability certifications reassure buyers about ethical sourcing. Brands highlight terroir and seasonal narratives to justify higher ticket sizes. As consumers seek niche bioactives, demand migrates toward these once-secondary plant parts, diversifying supply chains and elevating average selling prices in the herbal medicinal products market.

Complete Report Scope:

- By Product Type

- Herbal Pharmaceuticals

- Herbal Dietary Supplements

- Herbal Functional Foods & Beverages

- Herbal Cosmetics & Personal Care

- By Source (Plant Part)

- Leaves

- Roots & Rhizomes

- Whole Plant

- Fruits & Seeds

- Flowers & Bark

- By Form

- Tablets & Capsules

- Powders & Granules

- Liquid Extracts & Syrups

- Teas & Infusions

- Softgels & Gummies

- Topicals & Ointments

- By Distribution Channel

- Hospital & Retail Pharmacies

- Online / E-commerce

- Specialty Stores

- Hypermarkets & Supermarkets

- By Medicinal Plant Type

- Aloe vera

- Echinacea

- Turmeric (Curcuma longa)

- Ginseng

- Ginger

- Garlic

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America generated 28.94% of 2025 revenue for the herbal medicinal products market, benefiting from transparent regulatory frameworks and high discretionary spending. Updated FDA guidance cuts bureaucratic friction, enticing innovation. Consumers increasingly choose evidence-based botanicals such as beetroot, whose sales climbed 108% in 2023.

Asia-Pacific achieves the fastest 7.90% CAGR through 2031, propelled by government initiatives that integrate traditional medicine into national healthcare systems. China's ethnic-medicine policy and India's expanded nutraceutical rules create fertile ground for startups and multinationals alike. India active pharmaceutical ingredients from botanical sources are emerging as key differentiators in the global herbal medicine supply chain. Japan's demographic aging intensifies demand for cognitive and joint-support formulations, while Southeast Asian biodiversity supports raw-material sourcing.

Europe sustains steady growth under Directive 2004/24/EC, which balances traditional use with safety documentation. Germany's naturopathic culture anchors regional demand, and the UK maintains relevance despite post-Brexit realignment. Emerging markets in the Middle East and Africa show potential but face infrastructure and regulatory gaps that must be bridged to unlock fuller participation in the herbal medicinal products market.

- Beijing Tong Ren Tang Chinese Medicine Co. Ltd.

- Bio-Botanica Inc.

- Bionorica SE

- Blackmores Ltd.

- Dabur India Ltd.

- Dermapharm Holding SE (Arkopharma SA)

- Dr. Willmar Schwabe GmbH & Co. KG (Schwabe Group)

- Gaia Herbs

- Herb Pharm

- Herbalife International, Inc.

- Himalaya Global Holdings

- Naturalin Bio-Resources Co., Ltd.

- Nature's Way Brands, LLC

- Nestle Health Science (Nature's Bounty)

- Otsuka Holdings (Pharmavite LLC)

- Ricola AG

- Tsumura & Co.

- Viatris Inc. (Rottapharm Madaus)

- Vytalogy Wellness (Jarrow Formulas, Inc.)

- Weleda

- Zand Immunity

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Consumers Worldwide Have Shifted Toward Natural, Plant-Based OTC Remedies

- 4.2.2 Progressive Regulators Are Shortening Launch Timelines

- 4.2.3 Rapid Penetration Of E-Commerce And Direct-To-Consumer Nutraceutical Brands

- 4.2.4 AI-Driven Platforms Are Mining Phytochemical Databases And Predicting Herb-Drug Interactions

- 4.2.5 Sports-Nutrition And Functional-Food Companies Are Incorporating Adaptogens In Performance Beverages

- 4.2.6 Fermentation-Based Biomanufacturing Now Yields Consistent, Pharma-Grade Phytochemicals

- 4.3 Market Restraints

- 4.3.1 Raw-Material Adulteration & Supply Shocks

- 4.3.2 Fragmented Global Regulatory Frameworks

- 4.3.3 Climate-Driven Loss Of Wild Medicinal Plant Species

- 4.3.4 Emerging Synthetic-Biology Platforms Can Produce Bio-Identical Botanical Actives In Microbial Cell Factories

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product Type

- 5.1.1 Herbal Pharmaceuticals

- 5.1.2 Herbal Dietary Supplements

- 5.1.3 Herbal Functional Foods & Beverages

- 5.1.4 Herbal Cosmetics & Personal Care

- 5.2 By Source (Plant Part)

- 5.2.1 Leaves

- 5.2.2 Roots & Rhizomes

- 5.2.3 Whole Plant

- 5.2.4 Fruits & Seeds

- 5.2.5 Flowers & Bark

- 5.3 By Form

- 5.3.1 Tablets & Capsules

- 5.3.2 Powders & Granules

- 5.3.3 Liquid Extracts & Syrups

- 5.3.4 Teas & Infusions

- 5.3.5 Softgels & Gummies

- 5.3.6 Topicals & Ointments

- 5.4 By Distribution Channel

- 5.4.1 Hospital & Retail Pharmacies

- 5.4.2 Online / E-commerce

- 5.4.3 Specialty Stores

- 5.4.4 Hypermarkets & Supermarkets

- 5.5 By Medicinal Plant Type

- 5.5.1 Aloe vera

- 5.5.2 Echinacea

- 5.5.3 Turmeric (Curcuma longa)

- 5.5.4 Ginseng

- 5.5.5 Ginger

- 5.5.6 Garlic

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Beijing Tong Ren Tang Chinese Medicine Co. Ltd.

- 6.3.2 Bio-Botanica Inc.

- 6.3.3 Bionorica SE

- 6.3.4 Blackmores Ltd.

- 6.3.5 Dabur India Ltd.

- 6.3.6 Dermapharm Holding SE (Arkopharma SA)

- 6.3.7 Dr. Willmar Schwabe GmbH & Co. KG (Schwabe Group)

- 6.3.8 Gaia Herbs

- 6.3.9 Herb Pharm

- 6.3.10 Herbalife International, Inc.

- 6.3.11 Himalaya Global Holdings

- 6.3.12 Naturalin Bio-Resources Co., Ltd.

- 6.3.13 Nature's Way Brands, LLC

- 6.3.14 Nestle Health Science (Nature's Bounty)

- 6.3.15 Otsuka Holdings (Pharmavite LLC)

- 6.3.16 Ricola AG

- 6.3.17 Tsumura & Co.

- 6.3.18 Viatris Inc. (Rottapharm Madaus)

- 6.3.19 Vytalogy Wellness (Jarrow Formulas, Inc.)

- 6.3.20 Weleda

- 6.3.21 Zand Immunity

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment