|

시장보고서

상품코드

2072572

알파 만노시도시스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2030년)Alpha Mannosidosis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

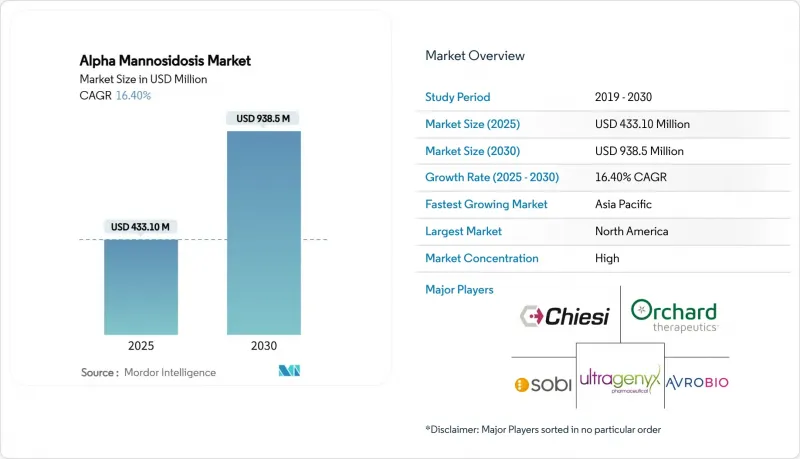

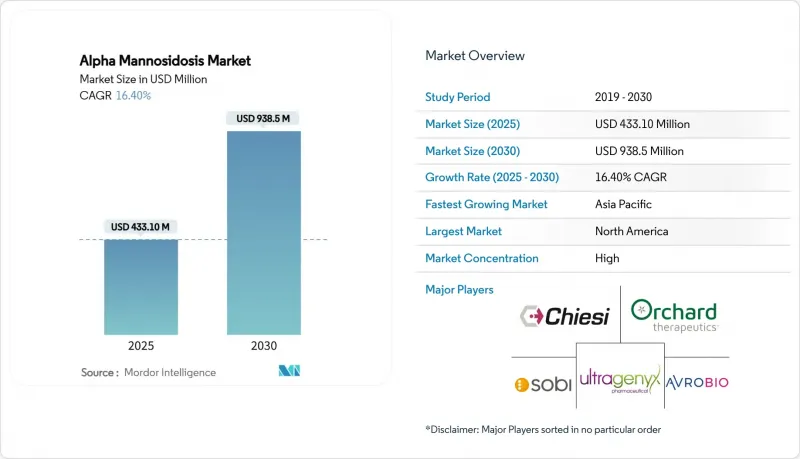

Mordor Intelligence에 의하면, 알파 만노시도시스 시장 규모는 2025년에 4억 3,310만 달러로 평가되었습니다. 예측 기간(2025-2030년) CAGR 16.40%로 성장을 지속하여, 2030년까지 9억 3,850만 달러에 이를 전망입니다.

본 보고서는 치료법별(효소 보충 요법, 조혈모세포 이식 등), 투여 경로별(정맥 내 주입, 외과적 이식을 통한 투여, 척수강 내/중추신경계로의 직접 투여 등), 그리고 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 알파 만노시도시스 시장 동향 및 인사이트

‘Velmanase Alfa’ ERT 승인 후 보급 현황

2024년 6월 람세데사가 FDA 승인을 획득함에 따라, 그동안 수입이나 자비적 사용에 의존해 왔던 미국 환자들이 이 약을 상업적으로 이용할 수 있게 되었습니다. 임상시험 데이터에 따르면, 52주 시점에서 혈청 올리고당이 77.6% 감소한 것으로 나타났으며, SPARKLE 레지스트리를 통해 15년에 걸친 예후를 추적함으로써 처방 의사의 신뢰를 한층 더 높일 수 있을 것입니다. 소아기 초기에 치료를 시작하는 것은 청력 및 면역 프로파일의 개선과 상관관계가 있으며, 이는 진단 후 신속한 치료를 권장하는 지침 개정으로 이어지고 있습니다. 주 1회 정맥 주사 투여에는 전문 시설이 필요하지만, 재택 간호 프로그램의 확대에 따라 병세가 안정된 환자의 이동 부담이 줄어들고 있습니다. 따라서 미국에서의 급속한 보급은 알파-만노시도시스 시장에 단기적으로 상당한 판매량을 더해줄 것입니다.

리소좀 축적증에 대한 신생아 선별검사의 시범 사업이 확대됩니다.

중국에서 실시된 대규모 시범 사업에서는 출생 1,512건당 1건의 비율로 리소좀 축적증이 발견되었으며, 차세대 염기서열 분석과 탠덤 질량 분석법을 활용한 리플렉스 검사의 유효성이 입증되었습니다. 뉴저지주에서 43만 8,515명의 신생아를 대상으로 실시된 이 사례는 미국 내에서의 운영상 실현 가능성을 보여주고 있습니다. 토스카나 주가 메타크로매틱 백질 이영양증을 선별 검사 대상에 포함시킨 것은 유럽의 보험사들이 희귀질환 검사 범위를 확대할 의향이 있음을 보여줍니다. 조기 발견을 통해 치료 시기를 증상이 나타나기 전 단계로 앞당길 수 있어, 치료 효과를 극대화하고 장기적인 비용을 절감할 수 있다는 주장은 현재 정책 입안자들 사이에서 공감을 얻고 있습니다. 더 많은 관할 구역에서 보편적 선별 검사가 법제화됨에 따라, 알파-만노시도시스 시장은 이전에는 진단받지 못했을 새로운 환자들을 확보하게 될 것입니다.

높은 연간 치료비와 가격 책정에 대한 반발

주 1회 벨마나제 알파 정맥 주사는 연간 65만 달러가 넘는 약제비를 초래하며, 이러한 부담은 단일 지불자 제도나 신흥 시장의 예산에 있어 큰 과제가 되고 있습니다. 렌멜디의 출시 가격인 425만 달러와 같은 유전자 치료의 기준가는 단 한 번의 치료로 완치되는 치료법에 대한 경제적 부담에 대한 우려를 키우고 있습니다. 중부 및 동유럽에서는 보험 적용을 받는 희귀질환 치료제가 20개 미만에 그치고 있어, 애초에 람제데를 도입했던 이 지역에서도 치료 접근성의 격차가 두드러지게 나타나고 있습니다. 보험사들은 지급을 장기적인 기능적 이익과 연계하는 성과 연계형 계약을 점점 더 요구하고 있으며, 이로 인해 재무적 위험이 제약사 측으로 다시 돌아오고 있습니다. 혁신적인 자금 조달 방안이 없다면, 높은 가격으로 인한 충격이 단기적인 보급을 제한하고, 알파-만노시도시스 시장의 성장을 둔화시킬 것입니다.

부문별 분석

2024년, 효소 보충 요법 부문은 알파-만노시도시스 시장의 82.4%를 차지했으며, 벨마나제 알파 시장 최초 진출이라는 우위가 그 기반이 되고 있습니다. 6가지 소아 질환의 지정과 벤처 캐피털의 자금 유입에 힘입어 유전자 치료 시장은 2030년까지 연평균 성장률(CAGR) 18.4%를 나타낼 것으로 예측되며, 시장에 혁신적인 변화를 가져올 것으로 전망됩니다. 조혈모세포 이식은 중증 신경학적 증상에 대해 임상적 유용성이 입증되었으며, 2000년 이후의 생존율은 86%에 달하고, 2000년 이전의 64%를 상회하고 있습니다. 청각학, 면역학, 물리치료를 포함한 다직종 협력을 통한 지원 치료는 표준 프로토콜이 정립됨에 따라 확대되고 있습니다. 약리학적 샤페론 후보 물질들은 잘못 접힌 리소좀 효소를 교정하는 것을 목표로 하고 있지만, 현재로서는 아직 어떤 후보 물질도 3상 임상시험 단계에 이르지 못했습니다.

신뢰할 수 있는 실제 레지스트리 데이터는 벨마나제 알파의 지속성을 입증하고 있으며, 지급 기관으로 하여금 지속적인 임상적 성과를 확신하게 하고 있습니다. 그러나 1회 투여형 AAV 벡터는 지속적인 수익 모델을 위협하고 있어, 키에시사는 차세대 연구에 자금을 지원하는 보조금을 통해 사업 다각화를 추진할 수밖에 없는 상황입니다. SmartPharm사의 유전자코딩 효소 플랫폼은 유전체에 영구적으로 통합하지 않고도 발현 기간을 연장할 수 있는 하이브리드 접근 방식을 제시하고 있습니다. 이러한 치료법들이 융합됨에 따라, 알파-만노시도시스 시장에서는 중추신경계(CNS)에 도달할 수 있는 능력과 간소화된 투여 일정을 모두 갖춘 치료법이 점점 더 높이 평가받게 될 것입니다.

지역별 분석

2024년 매출 점유율 41.3%를 차지한 유럽은 2018년 EMA의 벨마나제 알파 승인 및 확립된 희귀질환 의약품 보험급여 제도의 혜택을 받고 있습니다. 독일과 프랑스는 각각 100종 이상의 희귀질환 치료제를 보험 적용 대상으로 지정하여, 조기에 지속적으로 보급되도록 장려하고 있습니다. 반면, 중동부 유럽 국가들은 여전히 상환 경로가 제한적이라는 점에 어려움을 겪고 있으며, 접근성 격차가 해소되지 않은 채 남아 있습니다. MetabERN은 회원국 간의 임상 경로(치료 경로)를 통일하고, 국경을 초월한 지식 이전을 원활하게 하여 도입률 향상에 기여하고 있습니다.

북미는 현재 가장 빠르게 성장하고 있는 지역이며, FDA의 2024년 획기적인 승인을 계기로 2030년까지 연평균 성장률(CAGR)이 15.7%를 나타낼 것으로 전망됩니다. 미국에서는 희귀질환 치료제에 대한 인센티브와 뉴저지주에서 시행을 시작한 신생아 선별검사 인프라 확충 등이 활용되고 있습니다. 캐나다와 멕시코는 규제 심사 절차를 미국의 선례에 맞추고 있지만, 가격 책정 차이로 인한 장벽은 여전히 남아 있습니다. 초고비용 의약품을 둘러싼 공적인 논의로 인해 성과 연계형 자금 조달 모델에 대한 압박이 커지고 있지만, 획기적인 희귀질환 치료법에 대한 지불 주체의 관심은 여전히 지속되고 있습니다.

아시아태평양과 라틴아메리카는 장기적인 성장 잠재력을 지니고 있지만, 상환 제약과 주사 센터의 수용 능력 한계로 인해 그 성장세가 억제되고 있습니다. 중국에서 진행 중인 신생아 유전체 선별 검사의 시범 사업은 기술적 준비가 완료되었음을 보여주고 있으며, 리소좀 질환을 인구 규모로 검출하고 있습니다. 일본은 유전자 치료의 주요 임상시험에 적극적으로 참여하고 있으며, 전 세계적으로 승인 신청이 시작되면 일본 내 승인 절차가 가속화될 가능성이 있습니다. 각 지역 정부는 조기 발견의 경제적 타당성과 환자 1인당 치료비를 비교 검토하고 있으며, 가격이 정상화됨에 따라 단계적인 도입이 진행될 것으로 보입니다. 전반적으로, 지역별 이질성이 알파 만노시도시스 시장의 다양한 성장 패턴을 형성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the alpha mannosidosis market size is estimated at USD 433.10 million in 2025 and is expected to reach USD 938.50 million by 2030, at a CAGR of 16.40% during the forecast period (2025-2030).

This report is Segmented by Therapy Type (Enzyme Replacement Therapy, Hematopoietic Stem-Cell Transplantation, and More), Route of Administration (Intravenous Infusion, Surgical Transplant Administration, Intrathecal/CNS-direct Delivery, and More), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Alpha Mannosidosis Market Trends and Insights

Post-Approval Uptake of Velmanase Alfa ERT

Lamzede's June 2024 FDA approval unlocked commercial access for US patients who had relied on importation or compassionate use. Trial data showed a 77.6% reduction in serum oligosaccharides at 52 weeks, and the SPARKLE registry will track outcomes over 15 years, reinforcing prescriber confidence. Earlier pediatric initiation correlates with improved hearing and immune profiles, prompting guideline updates that advocate treatment soon after diagnosis.Weekly infusions require specialized centers, but growing home-care programs mitigate logistical burden for stable patients. Rapid US uptake thus adds meaningful near-term volume to the alpha-mannosidosis market.

Increasing Newborn-Screening Pilots for Lysosomal Storage Disorders

Large-scale pilots in China uncovered lysosomal storage disorders in 1 in 1,512 births, validating next-generation sequencing coupled with tandem-mass-spectrometry reflex testing. New Jersey's experience covering 438,515 newborns demonstrates operational feasibility in a US setting. Tuscany's inclusion of metachromatic leukodystrophy proves European payers' willingness to broaden rare-disease panels. Earlier detection shifts treatment to pre-symptomatic stages, maximizing therapeutic benefit and curbing long-term costs, arguments now resonating with policymakers. As more jurisdictions legislate universal screening, the alpha-mannosidosis market captures incremental patients who would previously have remained undiagnosed.

High Annual Treatment Cost & Pricing Pushback

Weekly velmanase alfa infusions translate into yearly drug spend above USD 650,000, a burden that challenges single-payer and emerging-market budgets. Gene-therapy benchmarks, such as Lenmeldy's USD 4.25 million launch price, heighten affordability concerns for one-time cures. Central and Eastern Europe report fewer than 20 reimbursed orphan medicines, underscoring access gaps within the very region that originally adopted Lamzede. Insurers increasingly demand outcome-based contracts linking payment to long-term functional benefits, shifting financial risk back to manufacturers. Without innovative financing, sticker shock will limit near-term uptake, slowing growth in the alpha-mannosidosis market.

Other drivers and restraints analyzed in the detailed report include:

- Gene-Therapy Pipeline Breakthroughs

- Expansion of Compassionate-Use & Early-Access Programs

- Limited Blood-Brain-Barrier Penetration of Current ERT

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The enzyme-replacement segment represented 82.4% of the alpha-mannosidosis market in 2024, anchored by velmanase alfa's first-to-market advantage. Gene therapies, buoyed by six pediatric-disease designations and venture-capital inflows, are forecast to post an 18.4% CAGR through 2030, setting a disruptive tone. Hematopoietic stem-cell transplants secure clinical relevance for severe neurologic phenotypes, with post-2000 survival at 86% versus 64% pre-2000. Supportive multidisciplinary care-including audiology, immunology, and physiotherapy-expands as standard protocols mature. Pharmacological-chaperone candidates seek to correct misfolded lysosomal enzymes, though none have yet reached pivotal trials.

Robust real-world registry data underscore velmanase alfa durability, convincing payers of sustained clinical return. However, single-dose AAV vectors threaten recurring-revenue models, compelling Chiesi to diversify via grants that fund next-generation research. SmartPharm's gene-encoded-enzyme platform illustrates hybrid approaches that could lengthen expression without permanent genome integration. As these modalities converge, the alpha-mannosidosis market will increasingly reward therapies that pair CNS reach with simplified administration schedules.

Complete Report Scope:

- By Therapy Type

- Enzyme Replacement Therapy

- Hematopoietic Stem-Cell Transplantation

- Gene Therapy

- Supportive & Adjunctive Care

- Investigational Pharmacological Chaperones

- By Route of Administration

- Intravenous Infusion

- Surgical Transplant Administration

- Intrathecal / CNS-direct Delivery

- Systemic Viral Vector Delivery

- Other Routes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

Europe, with a 41.3% revenue share in 2024, benefits from EMA's 2018 approval of velmanase alfa and well-established orphan-drug reimbursement mechanisms. Germany and France each reimburse more than 100 rare-disease medicines, fostering early and sustained uptake. In contrast, Central and Eastern Europe still struggle with limited reimbursement pathways, perpetuating unequal access gaps. MetabERN harmonizes clinical pathways across member states, easing cross-border knowledge transfer and bolstering adoption rates.

North America now represents the fastest-growing region, projected at a 15.7% CAGR through 2030, following the FDA's landmark 2024 green light. The United States leverages orphan-drug incentives and an expanding newborn-screening infrastructure exemplified by New Jersey's operational rollout. Canada and Mexico are aligning regulatory review procedures with US precedents, though differential pricing hurdles remain. Public debate over ultra-high-cost medicines intensifies pressure for outcome-based funding models, yet payer appetite for transformative rare-disease therapies persists.

Asia-Pacific and Latin America offer long-term upside, tempered by reimbursement constraints and limited infusion-center capacity. China's genomic newborn-screening pilot demonstrates technological readiness, recording lysosomal disorder detection at population scale. Japan participates actively in pivotal gene-therapy trials, which may accelerate domestic approval once global filings commence. Regional governments weigh the economic rationale of early detection against per-patient therapy costs, suggesting phased adoption as prices normalize. Collectively, geographic heterogeneity shapes a multi-speed growth pattern for the alpha-mannosidosis market.

- Chiesi Farmaceutici

- Sobi (Swedish Orphan Biovitrum)

- Orchard Therapeutics plc

- Avrobio

- Ultragenyx Pharmaceutical Inc.

- Regenxbio Inc.

- Rocket Pharmaceuticals Inc.

- M6P Therapeutics

- SmartPharm Therapeutics

- CSL Behring

- Takeda Pharmaceuticals

- JCR Pharmaceuticals

- Leadiant Biosciences

- ArmaGen Inc.

- Sangamo Therapeutics

- Astellas Gene Therapies

- Bluebird Bio

- Genethon

- Passage Bio

- Denali Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise In Post-Approval Uptake Of Lamzede (Velmanase Alfa) ERT

- 4.2.2 Increasing Newborn-Screening Pilots For Lysosomal Storage Disorders

- 4.2.3 Expansion Of Compassionate-Use & Early-Access Programs

- 4.2.4 Gene-Therapy Pipeline Breakthroughs (AAV & LNP Platforms)

- 4.2.5 Multi-Country Orphan-Drug Reimbursement Harmonization In EU

- 4.2.6 AI-Enabled Ultra-Rare-Disease Patient-Finding Algorithms

- 4.3 Market Restraints

- 4.3.1 High Annual Treatment Cost & Pricing Pushback

- 4.3.2 Limited Blood-Brain-Barrier Penetration of Current ERT

- 4.3.3 Scarce Long-Term Real-World Safety Data

- 4.3.4 Competition For Bone-Marrow Donor Matches Limiting HSCT Uptake

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy Type

- 5.1.1 Enzyme Replacement Therapy

- 5.1.2 Hematopoietic Stem-Cell Transplantation

- 5.1.3 Gene Therapy

- 5.1.4 Supportive & Adjunctive Care

- 5.1.5 Investigational Pharmacological Chaperones

- 5.2 By Route of Administration

- 5.2.1 Intravenous Infusion

- 5.2.2 Surgical Transplant Administration

- 5.2.3 Intrathecal / CNS-direct Delivery

- 5.2.4 Systemic Viral Vector Delivery

- 5.2.5 Other Routes

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East & Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East & Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Chiesi Farmaceutici S.p.A.

- 6.3.2 Sobi (Swedish Orphan Biovitrum)

- 6.3.3 Orchard Therapeutics plc

- 6.3.4 Avrobio Inc.

- 6.3.5 Ultragenyx Pharmaceutical Inc.

- 6.3.6 Regenxbio Inc.

- 6.3.7 Rocket Pharmaceuticals Inc.

- 6.3.8 M6P Therapeutics

- 6.3.9 SmartPharm Therapeutics

- 6.3.10 CSL Behring LLC

- 6.3.11 Takeda Pharmaceutical Company Ltd.

- 6.3.12 JCR Pharmaceuticals Co., Ltd.

- 6.3.13 Leadiant Biosciences Inc.

- 6.3.14 ArmaGen Inc.

- 6.3.15 Sangamo Therapeutics

- 6.3.16 Astellas Gene Therapies

- 6.3.17 Bluebird Bio Inc.

- 6.3.18 Genethon

- 6.3.19 Passage Bio

- 6.3.20 Denali Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment