|

시장보고서

상품코드

2072579

드론 배터리 시스템 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2030년)Drone Battery Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

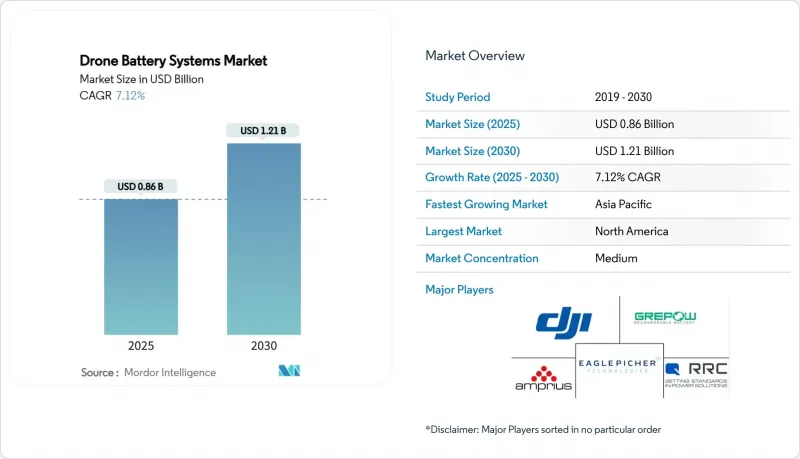

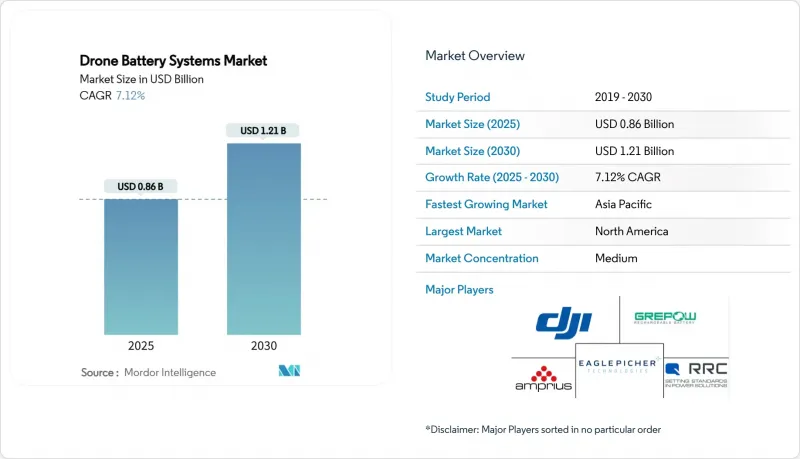

Mordor Intelligence에 의하면, 드론 배터리 시스템 시장 규모는 2025년에 8억 6,000만 달러로 평가되었습니다. 2030년까지 12억 1,000만 달러에 이를 것으로 예측되며, CAGR은 7.12%를 나타낼 전망입니다.

본 보고서는 배터리 화학 조성(리튬 폴리머, 기타), 용량 범위(3,000 mAh 이하, 3,001-10,000 mAh, 기타), 드론 카테고리(민간용, 업무용/기업용, 기타), 용도(항공 촬영·측량, 정밀 농업, 기타), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 드론 배터리 시스템 시장 동향 및 인사이트

고에너지 리튬 이온 배터리의 와트시당 비용 절감

중국의 양극재 제조업체가 대규모 생산을 통해 350 Wh/kg을 달성하는 NMC 811 배합을 표준화함에 따라, 셀 가격은 계속해서 하락하고 있습니다. 원광석에서 완제품 팩에 이르기까지의 수직 통합을 통해 물류 비용이 절감됨에 따라, 전문 사업자들은 배터리 운영 예산을 15-20% 절감할 수 있게 되었습니다. 2만 1,700형 원통형 배터리의 양산화를 통해 포장 효율이 향상되어, 구조를 재설계하지 않고도 비행 시간을 연장할 수 있게 되었습니다. 와트시당 비용이 낮아짐에 따라, 기체 소유주들은 안전성을 높이는 동시에 임무 시간을 연장할 수 있는 중복성을 중시하는 듀얼 배터리 아키텍처를 점점 더 많이 채택하고 있습니다.

비행 시간 연장이 필요한 BVLOS 임무의 도입 확대

EASA의 위험 기반 체계에 따라 지역별 BVLOS 비행 회랑이 승인됨에 따라, 상업용 사업자들은 2시간 이상 비행이 가능한 배터리를 채택해야 합니다. 500에이커 규모의 농지를 운영하는 농업 기업에서는 2만mAh를 초과하는 배터리 팩이 요구되며, 점검 회사에서는 외딴 지역에서의 가동 중단 시간을 최소화하는 모듈식 핫스왑 유닛이 채택되고 있습니다. 소프트웨어 기반 전력 관리 알고리즘이 전류 소비를 동적으로 조절하여, 장시간 호버링이나 상승 단계에서도 셀을 보호합니다. 이러한 규제 동향은 미국에서도 마찬가지이며, FAA의 직선형 인프라 점검 면제 조치에 따라 대용량 배터리 팩의 채택이 촉진되고 있습니다.

불소계 전해액에 대한 PFAS 규제 강화

EU가 제안한 퍼플루오로알킬 물질 및 폴리플루오로알킬 물질의 사용 금지로 인해, 제조업체들은 불소화 염 및 바인더의 대체재를 찾아야만 하는 상황에 놓여 있으며, 이로 인해 단기적인 생산 비용이 8-12% 증가하게 될 것입니다. 검사 기관은 개정된 UN-38.3 운송 규정에 따라 열폭주 거동을 검증해야 하며, 이로 인해 인증 절차가 장기화되어 제품 출시가 최대 9개월 지연될 가능성이 있습니다. 소규모 셀 조립 제조업체들은 파일럿 규모의 용매 회수 라인 도입으로 인해 자본 수요가 증가하고 있으며, 배합 변경 프로그램에 필요한 자금을 조달하지 못할 경우 시장에서 철수할 위험도 일부 존재합니다. 북미 규제 당국도 유사한 규제를 검토하고 있으며, 이에 따라 전 세계 공급업체들은 국경 간 판매가 중단되지 않도록 비불소계 화학물질에 대한 사전 인증 절차를 진행하고 있습니다. 불소 무함유 전해액에 대한 장기 계약을 조기에 체결한 기업은 2027년에 규제가 시행될 경우, 가격 협상에서 유리한 입지를 확보할 가능성이 있습니다.

부문별 분석

리튬 폴리머(Li-Po)는 확립된 생산 라인과 입증된 안전성 덕분에 2024년 드론 배터리 시스템 시장에서 54.91%의 점유율을 차지했습니다. 이 부문에서 에너지 밀도가 점진적으로 향상됨에 따라(현재 약 300 Wh/kg 수준), 전문가용 드론에 대한 수요가 유지되고 있습니다. 연평균 성장률(CAGR) 9.41%가 예상되는 리튬-황 전지는 희귀 금속을 포함하지 않는 양극재를 사용하여 500 Wh/kg 달성을 목표로 하는 기업들에게 매력적인 선택지입니다. 초기 비행 시험에서 3시간의 비행 능력이 확인되어, 상용화 준비가 완료되었음을 시사하고 있습니다. 실리콘 음극 리튬 이온 배터리는 기존의 조립 설비를 활용하면서 에너지 효율을 20-30% 향상시킴으로써, 현행 모델과 차세대 모델을 잇는 가교 역할을 할 것입니다. 연료전지 하이브리드는 순간적인 고토크 출력과 수소를 이용한 장시간 주행 능력을 결합하여, 틈새 시장인 중량물 운반 임무에 활용됩니다.

기체 소유자는 원료 리스크를 헤지하기 위해 화학 조성의 다양화를 중시하고 있습니다. 각 OEM 업체들은 셀 유형에 구애받지 않는 파워트레인 설계를 점점 더 적극적으로 추진하고 있으며, 새로운 화학 성분이 성숙 단계에 도달하면 원활한 업그레이드가 가능해질 것입니다. 이러한 모듈성은 기술 노후화에 대한 우려를 줄여주며, 드론 배터리 시스템 산업의 수년에 걸친 조달 주기에서 결정적인 요인으로 작용하고 있습니다.

3,001-1만 mAh 범위의 배터리 팩은 2024년 출하량의 43.65%를 차지하며, 측량 및 촬영 업무에서 비행 지속 시간과 관리 가능한 충전 시간 간의 균형을 맞추었습니다. 2만mAh를 초과하는 모듈은 BVLOS 규제 확대에 따라 통로 점검 및 파이프라인 모니터링을 지원하며, 연평균 성장률(CAGR) 7.32%로 성장할 것으로 전망됩니다. 3,000mAh 이하의 배터리는 비행 시간보다 휴대성을 중시하는 민간용 드론에 사용되는 반면, 1만 1-2만 mAh 모델은 정밀 농업 분야에서 중거리 용도로 활용되고 있습니다.

지능형 열 제어 및 능동형 균형 기능을 통해 대용량 팩의 실용 방전 깊이가 향상되고, 사이클 수명이 연장됩니다. 집중형 교환 스테이션을 도입한 사업자들은 표준화된 대용량 형태를 사용함으로써 가동 중단 시간이 12% 감소했다고 보고하고 있으며, 이를 통해 그 경제성이 입증되었습니다.

지역별 분석

2024년에는 북미가 매출의 33.93%를 차지했습니다. 이는 견조한 상업적 도입에 더해, 인프라 점검용 BVLOS(시야 외 비행) 면제를 인정하는 FAA(연방항공청)의 명확한 지침에 힘입은 결과입니다. Amprius 등 국내 전지 개발 기업들은 드론 OEM 업체들과 협력하여 400 Wh/kg의 실리콘 음극 팩을 상용화함으로써, 이 분야의 선도적 입지를 더욱 공고히 하고 있습니다. 캐나다는 광범위한 자원 분야를 활용하여 장거리 정찰 비행을 통한 검사 운영을 실시하고 있는 반면, 멕시코의 물류 기업들은 지방 소포 배송 노선에 대한 검사 운영에 주력하고 있습니다.

아시아태평양은 2030년까지 연평균 성장률(CAGR) 11.67%를 기록하며 가장 높은 성장률을 보일 것으로 전망됩니다. 중국에서는 2029년까지 운용 중인 드론이 370만 대에 달할 것으로 예상되며, 이에 따라 지능형 배터리 및 현지 재활용 능력에 대한 막대한 수요가 발생할 것으로 보입니다. 일본의 시스템 통합 업체들은 인력 부족을 보완하기 위해 자동화 시스템을 도입하고, 배터리 상태를 실시간으로 알려주는 스마트 팩 그리드를 채택하고 있습니다. 인도의 농업 기술(애그리테크) 이니셔티브에서는 드론 구매에 대해 보조금이 지급되고 있으며, 이에 따라 국내 배터리 조립 제조업체들은 혹독한 현장 환경에 대응할 수 있는 6S 규격 배터리 팩의 표준화를 추진하고 있습니다.

유럽에서는 규제 측면에서의 선도적 역할과 제조업체의 유연성 사이에서 균형이 잡혀 있습니다. 도심항공모빌리티(UAM)(UAM)에 적용되는 유럽항공안전청(EASA)의 규정에 따라, 배터리 팩 제조업체는 과열 시 강제 종료 프로토콜을 포함하여 더 높은 안전 여유를 확보해야 합니다. 독일과 프랑스는 산업용도를 우선시하는 반면, 북유럽의 업체들은 한랭지용 전해액 혼합물 개발을 주도하고 있습니다. EU가 도입할 예정인 ‘'배터리 여권'관련 제도로 인해 상세한 수명 주기 추적이 요구됨에 따라, 드론 배터리 시스템 시장 전반에서 재사용 및 재활용 사업에 대한 투자가 가속화되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the drone battery systems market size is USD 0.86 billion in 2025 and is forecasted to reach USD 1.21 billion by 2030, reflecting a 7.12% CAGR.

This report is Segmented by Battery Chemistry (Lithium-Polymer, and More), Capacity Range (Less Than 3, 000 MAh, 3, 001 To 10, 000 MAh, and More), Drone Category (Consumer, Professional/Enterprise, and More), Application (Aerial Imaging and Survey, Precision Agriculture, and More), and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Drone Battery Systems Market Trends and Insights

Falling Cost per Watt-Hour of High-Energy Lithium-Ion Cells

Cell prices continue to retreat because Chinese cathode producers standardize NMC 811 formulations that deliver 350 Wh/kg at scale. Vertical integration from raw ore to finished pack trims logistics overhead, allowing professional operators to shave 15-20% off battery operating budgets. Mass production of 21,700 cylindrical formats offers higher packing efficiency, raising flight time without structural redesigns. As the cost per watt-hour sinks, fleet owners increasingly adopt redundancy-focused dual-battery architectures that enhance safety while extending mission duration.

Growing Adoption of BVLOS Missions Requiring Extended Endurance

EASA's risk-based framework now greenlights regional BVLOS corridors, pushing commercial operators to specify batteries capable of 2+ hour sorties. Agricultural enterprises covering 500-acre fields demand packs exceeding 20,000 mAh, and inspection firms embrace modular hot-swap units that minimize downtime in remote areas. Software-defined power management algorithms dynamically balance current draw, protecting cell health during prolonged hover or climb phases. The regulatory momentum is mirrored in the United States, where FAA exemptions for linear infrastructure inspection encourage larger-capacity packs.

PFAS Restrictions Tightening on Fluorinated Electrolytes

The EU's proposed ban on per- and polyfluoroalkyl substances compels manufacturers to replace fluorinated salts and binders, adding 8-12% to near-term production costs. Test laboratories must verify thermal-runaway behavior under the revised UN-38.3 transport rules, lengthening certification cycles and delaying product launches by as much as nine months. Smaller cell assemblers face higher capital needs for pilot-scale solvent-recovery lines, and some risk of market exit if they cannot fund reformulation programs. North American regulators are weighing parallel limits, prompting global suppliers to pre-qualify non-fluorinated chemistries to keep cross-border sales uninterrupted. Early adopters that lock in long-term contracts for fluorine-free electrolytes may gain pricing leverage once the rules enter force in 2027.

Other drivers and restraints analyzed in the detailed report include:

- National Postal Fleets Scaling E-Commerce Drone Delivery

- Rapid Take-Up of Heavy-Lift Cargo Drones with Hybrid Powertrains

- Lithium-Price Volatility Hitting Pack Makers' Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-polymer (Li-Po) held 54.91% of the drone battery systems market share in 2024 because of well-established production lines and proven safety profiles. The segment's incremental advances in energy density, now near 300 Wh/kg, sustain demand for professional-grade drones. Lithium-sulfur, projected to post a 9.41% CAGR, appeals to operators targeting 500 Wh/kg without rare-metal cathodes; early flight tests show three-hour sortie capability, signaling commercial readiness. Silicon-anode lithium-ion bridges current and next-generation offerings by delivering 20-30% energy gains while using existing assembly equipment. Fuel-cell hybrids serve niche heavy-lift missions where instant high-torque output pairs with hydrogen for cruise endurance.

Fleet owners value chemistry diversification to hedge raw-material risks. OEMs increasingly design powertrains that are agnostic to cell type, enabling seamless upgrades as new chemistries mature. This modularity reduces obsolescence concerns, a decisive factor in multiyear procurement cycles for the drone battery systems industry.

Packs in the 3,001 to 10,000 mAh bracket represented 43.65% of 2024 shipments, balancing flight endurance with manageable recharge times for survey and imaging tasks. Modules above 20,000 mAh are set to grow at 7.32% CAGR as BVLOS regulation spreads, supporting corridor inspections and pipeline monitoring. Sub-3,000 mAh batteries cater to consumer drones where portability trumps duration, while 10,001 to 20,000 mAh models fill mid-range roles in precision agriculture.

Intelligent thermal control and active balancing unlock higher usable depth-of-discharge in large packs, extending cycle life. Operators deploying centralized swap stations note a 12% reduction in downtime when using standardized high-capacity formats, confirming the economic case.

Complete Report Scope:

- By Battery Chemistry

- Lithium-Polymer (Li-Po)

- Lithium-ion (Li-ion)

- Lithium High-Voltage (LiHV)

- Lithium-Sulfur (Li-S)

- Fuel-Cell/Hybrid Battery Systems

- By Capacity Range

- Less than 3,000 mAh

- 3,001 to 10,000 mAh

- 10,001 to 20,000 mAh

- Greater than 20,000 mAh

- By Drone Category

- Consumer (Less than 2 kg)

- Professional/Enterprise (2 to 25 kg)

- Heavy-Lift Cargo (Greater than 25 kg)

- By Application

- Aerial Imaging and Survey

- Precision Agriculture

- Logistics and Last-Mile Delivery

- Emergency Response

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- Turkey

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America controlled 33.93% of sales in 2024, underpinned by robust commercial adoption and clear FAA guidelines that certify BVLOS waivers for infrastructure inspection. Domestic cell innovators such as Amprius collaborate with drone OEMs to field 400 Wh/kg silicon-anode packs, further anchoring regional leadership. Canada leverages its widespread resources sector to pilot long-range inspection flights, while Mexican logistics firms experiment with rural parcel corridors.

Asia-Pacific is projected to register the fastest 11.67% CAGR through 2030. China expects 3.7 million active drones by 2029, spurring enormous demand for intelligent batteries and localized recycling capacity. Japanese integrators deploy automation to offset labor shortages, adopting smart-pack grids that signal state-of-health in real time. India's agri-tech initiatives subsidize drone purchases, encouraging domestic battery assemblers to standardize 6S-rated packs compatible with rugged field conditions.

Europe balances regulatory thought leadership with manufacturer agility. EASA's frameworks for urban air mobility push pack makers toward higher safety margins, including mandatory over-temperature shutdown protocols. Germany and France prioritize industrial applications, while Nordic operators pioneer cold-weather electrolyte blends. The EU's forthcoming battery passport scheme prompts detailed lifecycle tracking, accelerating investment in second-life and recycling ventures across the drone battery systems market.

- SZ DJI Technology Co., Ltd.

- Shenzhen Grepow Battery Co., Ltd.

- Amprius Technologies, Inc.

- Intelligent Energy Limited

- BYD Company Limited

- Murata Manufacturing Co., Ltd.

- Saft Groupe SAS

- Parrot Drones SAS

- Autel Robotics Co., Ltd.

- Hextronics LLC

- Quantum-Systems GmbH

- Dongguan Victory Battery Technology Co., Ltd.

- EaglePicher Technologies, LLC

- RRC power solutions GmbH

- Epsilor-Electric Fuel Ltd.

- Plug Power Inc.

- SES AI Corporation

- Inventus Power, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Falling cost per watt-hour of high-energy lithium-ion cells

- 4.2.2 Growing adoption of beyond-visual-line-of-sight (BVLOS) missions that require more than double the usual endurance

- 4.2.3 National postal fleets scaling e-commerce drone delivery

- 4.2.4 Rapid take-up of heavy-lift cargo drones that integrate hybrid fuel-cell powertrains

- 4.2.5 Surging investment in silicon-anode and lithium-sulfur battery start-ups

- 4.2.6 Rising demand for quick-swap battery stations that maximise commercial drone fleet uptime

- 4.3 Market Restraints

- 4.3.1 PFAS restrictions tightening on fluorinated electrolytes

- 4.3.2 Lithium-price volatility hitting pack makers' margins

- 4.3.3 Airport U-space rules capping battery weight classes

- 4.3.4 Recycling logistics lag for small-format drone packs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-Polymer (Li-Po)

- 5.1.2 Lithium-ion (Li-ion)

- 5.1.3 Lithium High-Voltage (LiHV)

- 5.1.4 Lithium-Sulfur (Li-S)

- 5.1.5 Fuel-Cell/Hybrid Battery Systems

- 5.2 By Capacity Range

- 5.2.1 Less than 3,000 mAh

- 5.2.2 3,001 to 10,000 mAh

- 5.2.3 10,001 to 20,000 mAh

- 5.2.4 Greater than 20,000 mAh

- 5.3 By Drone Category

- 5.3.1 Consumer (Less than 2 kg)

- 5.3.2 Professional/Enterprise (2 to 25 kg)

- 5.3.3 Heavy-Lift Cargo (Greater than 25 kg)

- 5.4 By Application

- 5.4.1 Aerial Imaging and Survey

- 5.4.2 Precision Agriculture

- 5.4.3 Logistics and Last-Mile Delivery

- 5.4.4 Emergency Response

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 United Arab Emirates

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SZ DJI Technology Co., Ltd.

- 6.4.2 Shenzhen Grepow Battery Co., Ltd.

- 6.4.3 Amprius Technologies, Inc.

- 6.4.4 Intelligent Energy Limited

- 6.4.5 BYD Company Limited

- 6.4.6 Murata Manufacturing Co., Ltd.

- 6.4.7 Saft Groupe SAS

- 6.4.8 Parrot Drones SAS

- 6.4.9 Autel Robotics Co., Ltd.

- 6.4.10 Hextronics LLC

- 6.4.11 Quantum-Systems GmbH

- 6.4.12 Dongguan Victory Battery Technology Co., Ltd.

- 6.4.13 EaglePicher Technologies, LLC

- 6.4.14 RRC power solutions GmbH

- 6.4.15 Epsilor-Electric Fuel Ltd.

- 6.4.16 Plug Power Inc.

- 6.4.17 SES AI Corporation

- 6.4.18 Inventus Power, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment