|

시장보고서

상품코드

2072585

보안 인식 교육 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Security Awareness Training - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

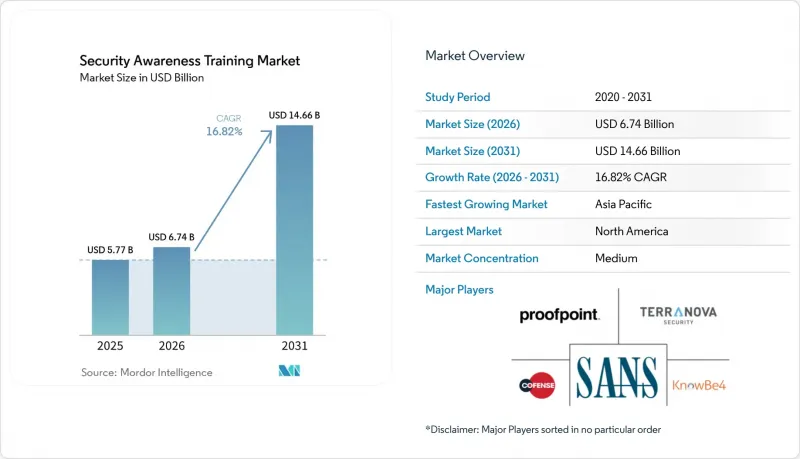

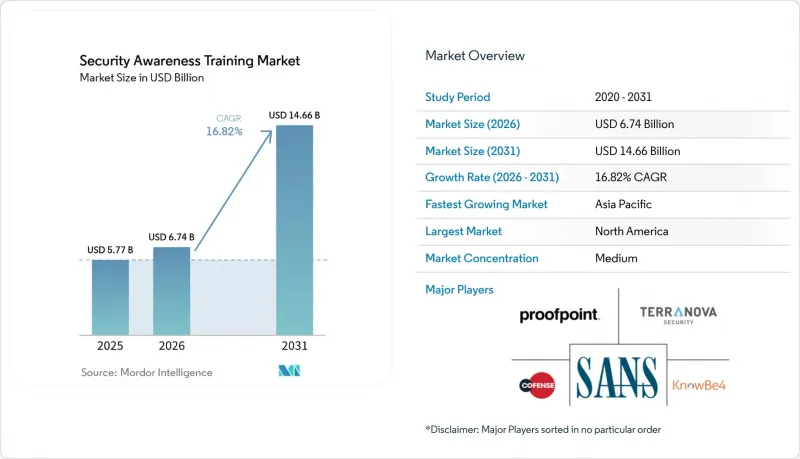

Mordor Intelligence에 의하면, 2026년 보안 인식 교육 시장 규모는 67억 4,000만 달러에 달할 것으로 예상됩니다. 2025년 57억 7,000만 달러에서 확대해, 2031년에는 146억 6,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년에 걸친 CAGR은 16.82%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 플랫폼 및 서비스), 제공 형태(클라우드 기반 및 On-Premise형), 조직 규모(중소기업 및 대기업), 업종(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 정부·국방, 기타) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 보안 인식 교육 시장 동향 및 인사이트

랜섬웨어 및 비즈니스 이메일 사기(BEC)로 인한 손실 급증

2024년 랜섬웨어 몸값 지불액은 평균 273만 달러에 달했으며, 2025년 1분기에는 제조업이 산업 분야 사고의 68%를 차지했습니다. FBI 기록에 따르면, 2016년부터 2021년까지 BEC로 인한 피해액은 430억 달러에 달했으며, 이로 인해 이사회 차원에서 직원 대상 경계 프로그램에 대한 긴급한 관심이 집중되고 있습니다. 의료 서비스 제공업체들은 사이버 공격으로 인해 하루 평균 약 200만 달러의 손실을 입고 있으며, 그 대부분은 인적 오류에서 비롯된 것입니다. Evolve Bank and Trust에서는 악성 링크를 단 한 번 클릭한 것만으로 33TB의 데이터가 유출되었으며, 이로 인해 직원의 부주의가 초래하는 대가가 얼마나 큰지 여실히 드러났습니다. 연중 빈번하게 교육을 실시하는 조직에서는 피싱 사기에 걸릴 확률이 34.3%에서 4.6%로 감소했으며, 이는 인적 위험 관리 플랫폼에 예산을 배분하는 것이 효과적임을 입증했습니다.

사이버 보험료의 급등으로 인해 직원들의 연수 실적 증명이 요구됨

지난 10년 동안 보험료는 급격히 상승했으며, 보험사들은 현재 보험을 인수하기 전에 철저한 보안 체계를 점검하고 있습니다. 보험 계약에서는 분기별 피싱 시뮬레이션 지표 및 수료증 제출이 일상화되어 있으며, 프로그램 참여 현황을 입증할 수 있는 기업에는 최대 20%의 보험료 할인이 적용됩니다. 2024년에는 중소기업의 82%가 랜섬웨어 피해를 입은 것으로 나타나, 보험사들이 중소기업을 대상으로 한 도입을 추진했습니다. 최소한의 보안 의식 기준을 충족한 기업은 더 폭넓은 보상 한도를 이용할 수 있을 뿐만 아니라, 정보 유출과 관련된 손실을 평균 540만 달러 절감했습니다. 손실 데이터 보고 도구를 통합할 수 있는 공급업체는 고객과 보험사 모두에게 더 큰 가치를 제공하며, 보안 인식 교육 시장에서 안정적인 수익원을 확보하고 있습니다.

과도한 의무적 훈련으로 인한 최종 사용자의 피로

Proofpoint의 조사에 따르면, 근로자의 68%는 위험을 인지하고 있음에도 불구하고 의도적으로 정책을 위반하고 있으며, 이는 모듈을 추가한다고 해도 안전한 행동으로 이어지지 않는 ‘포화점’에 도달했음을 보여줍니다. 세션 빈도가 너무 높으면 ‘체크박스식’ 대응을 초래하게 되며, 업무와의 연관성이 부족한 획일적인 컨텐츠는 직원들의 참여도를 저하시킵니다. 보안 팀은 직원들의 관심을 유지하기 위해 실시 빈도를 재검토하고, 시나리오를 개인별로 맞춤화해야 합니다. 그렇지 않으면 도입 지표가 하락하고, ROI도 감소하게 됩니다. 게이미피케이션을 도입한 시뮬레이션, 마이크로 레슨, 직책에 따른 스토리는 화면을 보는 총 시간을 단축하면서도 교육 효과를 회복하는 데 효과적임이 입증되었습니다.

부문별 분석

2025년, 보안 인식 교육 시장의 56.12%를 서비스가 차지했습니다. 이는 컨텐츠 현지화, 캠페인 조정, 행동 분석을 전문 파트너사에 외주하는 기업이 늘어난 데 힘입은 결과입니다. 관리형 프로그램에서는 최신 위협 인텔리전스를 바탕으로 모듈을 지속적으로 업데이트하고 있지만, 이는 많은 사내 팀에서는 감당하기 어려운 요구 사항입니다. 한편, 조직들이 관리상의 부담을 줄이기 위해 통합 콘솔을 표준화하고 있는 덕분에, 소프트웨어 플랫폼 시장은 연평균 성장률(CAGR) 19.14%를 기록하며 성장하고 있습니다. KnowBe4는 현재 AI가 제안하는 모듈과 보안 담당자의 부담을 줄여주는 자동 일정 관리 기능을 통해 6만 5,000개 고객사를 지원하고 있습니다. 하이브리드형 이용 형태도 점차 성숙해감에 따라, 기업들은 우선 매니지드 패키지를 도입한 뒤 역량이 향상된 단계에서 업무 부담을 사내 관리자에게 이관하고 있기 때문에 보안 인식 교육 시장에서는 두 가지 경로를 통한 수요가 지속되고 있습니다.

서비스 제공 기업들은 현지화의 심도, 업계별 맞춤형 시나리오 설계, 그리고 이메일 보안 텔레메트리에서 도출된 위협 인텔리전스 피드를 통해 차별화를 꾀하고 있습니다. 반면, 플랫폼 공급업체들은 사용자 경험 지표와 ID 관리 시스템부터 인사 기록에 이르기까지 폭넓은 연동 기능을 통해 경쟁하고 있습니다. 두 모델 모두 리스크 점수를 GRC 대시보드에 반영할 수 있도록 REST API 제공 범위를 확대되고 있습니다. 이러한 상호운용성의 필요성은 컨텐츠와 전문 서비스가 미묘한 문화적 적응에 있어 여전히 필수적임에도 불구하고, 플랫폼 중심의 미래를 촉진하고 있습니다.

2025년 기준으로 보안 인식 교육 시장 규모의 73.65%를 클라우드 제품이 차지했으며, 하이브리드 근무 방식이 정착됨에 따라 연평균 성장률(CAGR) 18.72%로 확대될 것으로 전망됩니다. 컨텐츠 자동 업데이트, 싱글 사인온, 모바일 앱을 통해 기존의 On-Premise형 학습 관리 시스템에 비해 수료율이 향상되고 있습니다. 기업의 이러닝에 관한 조사에 따르면, 67%의 기업이 모바일 제공을 통합하고 있으며, 수료율이 50% 향상되었습니다. On-Premise 방식의 도입은 데이터 주권에 관한 법률이나 에어갭 네트워크가 주류를 이루는 분야, 특히 국방 분야나 일부 공공기관에서 여전히 틈새 시장을 차지하고 있습니다.

현재 각 벤더사는 ‘분할 도입’ 방식을 제공합니다. 기밀성이 높은 데이터는 방화벽 내부에 그대로 보관된 채, 프런트엔드 포털은 공급업체의 멀티테넌트형 클라우드에서 운영됩니다. 이러한 아키텍처를 통해 정부 기관은 데이터 상주 요건을 충족하면서도 전 세계의 컨텐츠 파이프라인을 활용할 수 있게 됩니다. SaaS의 편의성과 규제 대상 호스트에 대한 제어 기능을 결합함으로써 이러한 추세가 지속되고 있으며, 보안 인식 교육 시장에서 클라우드의 핵심적인 역할이 더욱 강화되고 있습니다.

지역별 분석

북미는 조기 도입과 공급업체들의 집중적인 진출에 힘입어 2025년 보안 인식 교육 시장에서 37.78%의 점유율을 차지했습니다. 빈번한 시뮬레이션을 지속한 미국의 많은 도입 사례에서 피싱 피해를 입기 쉬운 사용자의 비율이 34.3%에서 4.6%로 감소했습니다. 사이버 보험 할인은 프로그램의 지속을 촉진하고 있지만, 컨텐츠 제공 빈도가 최적화되지 않을 경우 사용자의 피로감이 그 효과를 저해할 우려가 있습니다. 캐나다와 멕시코에서는 주요 인프라 사업자에 대한 규제 체계가 강화되는 가운데, 10%대 중반의 성장률을 보이고 있습니다.

아시아태평양은 디지털 정부 추진과 사고 발생 건수가 많은 점을 배경으로 연평균 성장률(CAGR) 18.61%를 기록하며 성장하고 있습니다. 이 지역은 2024년에 전 세계 사이버 공격의 31%를 차지했습니다. 홍콩에서는 피싱 관련 민원이 2배 이상 증가했으며, AI로 생성된 유인 메시지가 기업들의 위험 인식을 높이고 있습니다. 현지화, 이중 언어 모듈, 그리고 지역별 규정 준수 컨텐츠가 해외 및 국내 공급업체 모두의 매출 확대를 뒷받침하고 있습니다.

유럽은 금융 및 중요 인프라 전반에 걸쳐 최소한의 교육 기준을 정한 GDPR(EU 개인정보보호규정), NIS2, DORA 규제의 뒷받침을 받아 꾸준히 성장하고 있습니다. ENISA에 따르면, 기업들은 IT 예산의 9%를 정보 보안에 할당하고 있으며, 이는 안정적인 투자 파이프라인을 뒷받침하고 있습니다. 엄격한 데이터 개인정보 보호 규제를 준수해야 하므로, 개인의 행동과 관련된 분석에서는 규정 준수를 위해 데이터의 익명화 또는 집계 처리가 필요합니다. 이는 보안 인식 교육 시장에서 활동하는 제공업체들의 기능 로드맵에 영향을 미치고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.03According to Mordor Intelligence, security awareness training market size in 2026 is estimated at USD 6.74 billion, growing from 2025 value of USD 5.77 billion with 2031 projections showing USD 14.66 billion, growing at 16.82% CAGR over 2026-2031.

This report is Segmented by Component (Software Platforms and Services), Delivery Mode (Cloud-Based and On-Premise), Organization Size (Small and Medium-Sized Enterprises and Large Enterprises), Industry Vertical (BFSI, Healthcare and Life Sciences, Government and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Security Awareness Training Market Trends and Insights

Surge in Ransomware and Business-Email-Compromise (BEC) Losses

Ransomware payouts averaged USD 2.73 million in 2024, and manufacturing firms absorbed 68% of industrial incidents in Q1 2025. The FBI records BEC losses of USD 43 billion between 2016-2021, driving urgent board-level focus on employee vigilance programs. Healthcare providers lose an estimated USD 2 million daily to cyberattacks, with human error responsible for most breaches. A single click on a malicious link at Evolve Bank and Trust exposed 33 TB of data, underscoring the cost of inattentive staff. Organizations running year-long, high-frequency training saw phish-prone rates fall from 34.3% to 4.6%, validating budget shifts toward human-risk-management platforms.

Accelerating Cyber-Insurance Premium Hikes Requiring Employee Training Proof

Premiums climbed rapidly over the past decade, and insurers now run deep posture checks before issuing coverage. Policies routinely demand quarterly phishing-simulation metrics and certificates of completion, rewarding firms that can verify program engagement with premium discounts that reach 20%. SMB adoption is pushed by underwriters as 82% faced ransomware in 2024. Those meeting minimum awareness standards accessed broader coverage limits while cutting breach-related losses by USD 5.4 million on average. Providers able to integrate loss-data reporting tools enhance their value to both clients and carriers, carving out a secure revenue stream within the security awareness training market.

End-User Fatigue from Excessive Mandatory Trainings

Proofpoint research shows 68% of workers knowingly break policy despite being aware of the risk, illustrating a saturation point where more modules no longer translate into safer conduct. Over-frequent sessions can induce a checkbox mentality, and generic content that lacks job relevance erodes engagement. Security teams must rethink cadence and personalize scenarios to sustain attention; otherwise, adoption metrics slip, and ROI diminishes. Gamified simulations, micro-lessons, and role-specific stories have proven effective in restoring impact while trimming total screen time.

Other drivers and restraints analyzed in the detailed report include:

- Rapid SaaS Adoption by SMBs Pushing Cloud-Native Security Tools

- Expansion of Zero-Trust Architecture Programs Across Enterprises

- Budget Reallocations Toward XDR and SASE Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services captured 56.12% of the security awareness training market in 2025, buoyed by enterprises that outsource content localization, campaign orchestration, and behavioral analytics to specialist partners. Managed programs continuously refresh modules against live threat intel, a requirement that many internal teams cannot scale. Yet software platforms are climbing at a 19.14% CAGR as organizations standardize on centralized consoles to reduce administrative overhead. KnowBe4 now supports 65,000 customers with AI-suggested modules and automated scheduling that frees up security staff. Hybrid consumption is maturing: firms launch with managed packages, then shift workload to internal administrators once competence grows, sustaining dual-track demand in the security awareness training market.

The services cohort differentiates on the depth of localization, industry-specific scenario design, and threat intelligence feeds from mail-security telemetry. Platform vendors, by contrast, compete on user-experience metrics and breadth of integrations from identity systems to HR records. Both models increasingly offer REST APIs so risk scores can feed GRC dashboards. This interoperability imperative reinforces a platform-centric future, even as content and professional-services lines remain vital for nuanced cultural adaptation.

Cloud products represented 73.65% of the security awareness training market size in 2025 and are projected to rise at a 18.72% CAGR as hybrid work persists. Automatic content updates, single sign-on, and mobile apps raise completion rates compared with legacy on-premise learning-management systems. Corporate e-learning studies show 67% of firms integrate mobile delivery and achieve 50% higher pass-through rates. On-premise implementations still occupy niches where data-sovereignty laws or air-gapped networks prevail, notably in defense and certain public-sector agencies.

Vendors now offer split-deployment modes: sensitive payloads remain behind firewalls while front-end portals run in the vendor's multitenant cloud. Such architectures let governments meet residency mandates yet still exploit global content pipelines. The mix of SaaS ease and regulated-host controls sustains momentum, reinforcing the cloud's central role in the security awareness training market.

Complete Report Scope:

- By Component

- Software Platforms

- Services (Content Creation, Managed Programs, etc.)

- By Delivery Mode

- Cloud-Based

- On-Premise

- By Organization Size

- Small and Medium-sized Enterprises

- Large Enterprises

- By Industry Vertical

- BFSI

- Healthcare and Life Sciences

- Government and Defense

- IT and Telecom

- Retail and E-commerce

- Manufacturing

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Malaysia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held 37.78% of the security awareness training market in 2025, thanks to early adoption and dense vendor presence. Phish-prone levels fell from 34.3% to 4.6% in many U.S. deployments that maintained frequent simulations. Cyber-insurance discounts reinforce program continuation, yet user fatigue threatens efficacy if content cadence is not optimized. Canada and Mexico exhibit mid-teen growth as regulatory frameworks tighten around critical-infrastructure operators.

Asia-Pacific is expanding at a 18.61% CAGR on the back of digital-government pushes and high incident volume; the region absorbed 31% of global cyberattacks in 2024. Hong Kong saw phishing complaints more than double, with AI-generated lures raising risk awareness among enterprises. Localization, bilingual modules, and regional compliance content propel sales momentum for both global and domestic vendors.

Europe grows steadily, anchored by GDPR, NIS2, and DORA mandates that set minimum training standards across finance and critical infrastructure. ENISA notes that firms allocate 9% of IT budgets to information security, supporting stable investment pipelines. Strict data-privacy constraints do require adaptations; analytics tied to individual behavior must anonymize or aggregate data to comply, influencing feature roadmaps of providers active in the security awareness training market.

- KnowBe4 Inc.

- Proofpoint Inc.

- Cofense Inc.

- Terranova Security (Terranova WW Corp.)

- SANS Institute (Escal Institute of Advanced Technologies Inc.)

- Infosec Institute Inc.

- Hoxhunt Oy

- CybSafe Ltd.

- AwareGO ehf.

- Phished BV

- SoSafe GmbH

- Elevate Security Inc.

- Ninjio LLC

- Inspired eLearning LLC

- MediaPro Holdings LLC

- Security Innovation Inc.

- ThriveDX SA (Cyberbit legacy)

- Udemy Inc. (Cybersecurity Awareness Catalog)

- Arctic Wolf Networks Inc. (Managed SAT)

- Trend Micro Inc. (Phish Insight)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in ransomware and business-email-compromise (BEC) losses

- 4.2.2 Accelerating cyber-insurance premium hikes requiring employee training proof

- 4.2.3 Rapid SaaS adoption by SMBs pushing cloud-native security tools

- 4.2.4 Expansion of zero-trust architecture programs across enterprises

- 4.2.5 ISO/IEC 27001:2022 updates adding people-centric controls

- 4.2.6 Generative-AI-powered phishing kits lowering attack barriers

- 4.3 Market Restraints

- 4.3.1 End-user fatigue from excessive mandatory trainings

- 4.3.2 Budget reallocations toward XDR and SASE platforms

- 4.3.3 Inconsistent global privacy regulations limiting data analytics

- 4.3.4 Talent shortage in content-localization and cultural-nuance design

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Services (Content Creation, Managed Programs, etc.)

- 5.2 By Delivery Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Small and Medium-sized Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Government and Defense

- 5.4.4 IT and Telecom

- 5.4.5 Retail and E-commerce

- 5.4.6 Manufacturing

- 5.4.7 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Malaysia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 KnowBe4 Inc.

- 6.4.2 Proofpoint Inc.

- 6.4.3 Cofense Inc.

- 6.4.4 Terranova Security (Terranova WW Corp.)

- 6.4.5 SANS Institute (Escal Institute of Advanced Technologies Inc.)

- 6.4.6 Infosec Institute Inc.

- 6.4.7 Hoxhunt Oy

- 6.4.8 CybSafe Ltd.

- 6.4.9 AwareGO ehf.

- 6.4.10 Phished BV

- 6.4.11 SoSafe GmbH

- 6.4.12 Elevate Security Inc.

- 6.4.13 Ninjio LLC

- 6.4.14 Inspired eLearning LLC

- 6.4.15 MediaPro Holdings LLC

- 6.4.16 Security Innovation Inc.

- 6.4.17 ThriveDX SA (Cyberbit legacy)

- 6.4.18 Udemy Inc. (Cybersecurity Awareness Catalog)

- 6.4.19 Arctic Wolf Networks Inc. (Managed SAT)

- 6.4.20 Trend Micro Inc. (Phish Insight)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

(주말 및 공휴일 제외)