|

시장보고서

상품코드

2072614

기업 VSAT 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Enterprise VSAT System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

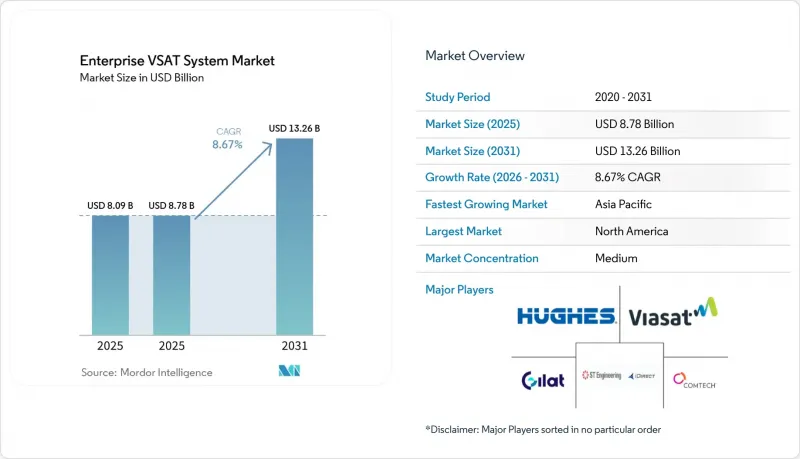

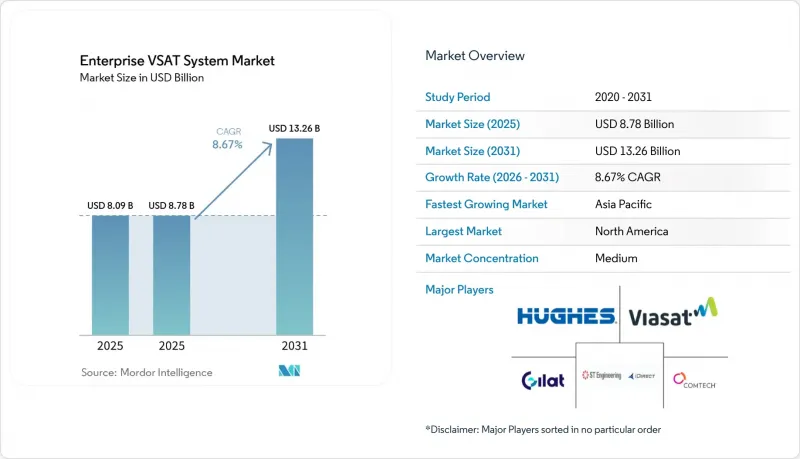

Mordor Intelligence에 의하면, 기업 VSAT 시스템 시장 규모는 2025년 80억 9,000만 달러로 평가되었고, 2026년에는 87억 8,000만 달러로 추정되고, 2031년까지 132억 6,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 8.67%로 성장할 전망입니다.

본 보고서는 구성 요소별(하드웨어 및 서비스), 플랫폼 규모별(소형 지구국, 중형 지구국, 대형 지구국), 주파수 대역별(Ku 대역, C 대역, Ka 대역 등), 최종 사용자 산업별(석유 및 가스, 해운, 정부 및 국방, 은행 및 금융 서비스, 통신 및 IT, 광업 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 기업 VSAT 시스템 시장 동향 및 인사이트

원격지 및 해상 거점에서의 광대역 접속 수요 급증

현재 해양 시추, 외딴 지역에서의 광업, 원양 항해 업무에서는 광섬유나 휴대전화 회선으로는 제공하기 어려운 대칭형 저지연 통신 회선이 요구되고 있습니다. Petrobras의 자회사인 Transpetro는 2025년 초 26척의 선박에 대해 하이브리드형 VSAT 및 Starlink로의 업그레이드를 완료했으며, 항로 최적화를 통해 3-5%의 연료 절감 효과를 달성했습니다. 모비스타 아르헨티나는 2026년 2월 기준으로 바카 무에르타 셰일 지역의 계약업체를 대상으로 한 위성 통신 계약 건수가 전년 대비 40% 증가했다고 보고했습니다. 인터이언은 페트로나스의 부유식 LNG 시설에 3중 중복화된 터미널을 도입함으로써, 막대한 가동 중단 손실을 피하기 위해 과잉 설비를 구축하려는 해당 부문의 태도를 여실히 드러냈습니다. ITU의 무선 규제 체계에 따라 라이선스 발급 절차가 간소화됨에 따라, 새로운 기업 VSAT 시스템 시장 진출은 승인 절차의 장기화를 초래하지 않고 확대될 수 있게 되었습니다.

디지털 유전 및 스마트 선박 분야의 노력이 VSAT 보급을 가속화하고 있습니다.

센서를 광범위하게 활용한 시추 프로그램과 데이터 기반 선단 운영을 통해, 연결성은 생산을 촉진하는 요소로 변화하고 있습니다. ST Engineering iDirect는 Solutions by stc와 제휴하여, 사우디아라비아의 900억 달러 규모 디지털 경제 이니셔티브의 일환으로 유정 및 정유시설를 모니터링하고 있습니다. SES와 Viasat Energy는 아시아태평양의 해양 플랫폼을 대상으로 150밀리초 미만의 서비스를 도입하여 로봇의 실시간 제어를 가능하게 했습니다. 퍼시픽 베이신(Pacific Basin)과 미쓰이 OSK 라인즈(Mitsui OSK Lines) 등 해운사들은 IMO의 사이버 보안 지침을 준수하고, 예정에 없던 입항을 최대 30% 줄이기 위해 2025년에 NexusWave를 통해 시스템 개조를 완료했습니다. 이해관계자들이 대역폭을 단순한 운영 비용이 아닌 성능 향상의 수단으로 인식하게 됨에 따라, 기업 VSAT 시스템 시장이 그 혜택을 누리고 있습니다.

지상 통신 수단에 비해 높은 설비 투자(Capex) 및 운영 비용(Opex)

VSAT의 하드웨어, 설치 공사비 및 텔레포트 운영 비용은 광섬유나 5G를 이용할 수 있는 지역에서 여전히 지상형 통신 수단보다 높습니다. 2024년 부품 부족으로 인해 갈륨비소(GaAs) LNA의 가격이 28.50달러에서 175달러로 급등했습니다. 공개 자료에 따르면, 콤텍과 KVH의 분기 영업 비용은 각각 1억 3,624만 달러와 3,096만 달러로, 24시간 365일 네트워크 운영에 따른 고정비 부담이 두드러지게 나타나고 있습니다. 외곽 지역의 사용자들은 이 비싼 요금을 감수하고 있지만, 도시 지역의 기업들은 경제성을 신중하게 검토하고 있으며, 이것이 기업 VSAT 시스템 시장의 보급 확대를 저해하는 요인이 되고 있습니다.

부문별 분석

2025년에는 단말기 초기 구매로 인해 하드웨어가 수익의 대부분을 차지한 것으로 평가된 반면, 매니지드 서비스의 연평균 성장률(CAGR)은 9.98%로 하드웨어를 상회했습니다. 조직들이 대역폭, 사이버 보안, 규제 준수를 운영 비용(OPEX)에 포함시키면서, 서비스 계약을 통한 기업 VSAT 시스템 시장 규모는 확대되고 있습니다. L3Harris와 Comtech의 5650C2/MP 모뎀은 멀티오빗 로밍을 간소화하고 사내 기술 요구 사항을 줄여줍니다. 현재 각 벤더사는 오케스트레이션, 설치, 티켓 관리 포털을 번들로 제공하고 있으며, 경쟁의 초점은 정가에서 총소유비용(TCO)으로 옮겨가고 있습니다. 통합 사업자는 대용량 계약을 활용하여 고객을 대역폭 변동으로부터 보호하고, 지속적인 수익원을 강화하고 있습니다. 하드웨어 혁신은 계속되고 있으며, 휴즈(Hughes)의 HM400 기내 모뎀은 ISR(정보·감시·정찰) 항공기를 대상으로 하고 있지만, 이 제품의 출시는 점점 더 장기 서비스 계약으로 이어지는 관문 역할을 하고 있습니다.

따라서 기업 VSAT 시스템 시장은 보다 광범위한 IT 아웃소싱 동향을 반영하고 있습니다. 기업은 공급업체를 통합하고, 가동 시간과 관련된 SLA 책임을 단일 창구로 집중시키는 것을 선호합니다. 이에 대응하여 벤더는 지역 설치 업체를 인수하고 네트워크 운영 센터에 투자함으로써 도입까지 걸리는 시간을 단축하고, 지역에 관계없이 지원을 표준화하고 있습니다. 서비스 포트폴리오가 성숙해짐에 따라, 차별화의 핵심은 사이버 보안 오버레이와 DevOps 툴체인에 위성 링크를 통합하는 API 액세스에 있습니다.

중형 지구국(1.2-2.4m)은 이득과 비용의 균형이 잘 잡혀 있어, 2025년에는 45.67%의 시장 점유율을 차지했습니다. 1.2m 미만의 소형 단말기는 연평균 성장률(CAGR) 9.63%로 성장하고 있으며, 기계식 짐벌이 필요 없이 갑판이나 차량에 평평하게 장착할 수 있는 전자식 스티어링 어레이의 이점을 누리고 있습니다. 소형 안테나용 기업 VSAT 시스템 시장 규모는 해운 및 방위 분야 고객들이 공기 저항 감소, 신속한 설치, 유지보수 비용 절감을 우선시함에 따라 확대되고 있습니다. Orbit사의 'OrBeam MIL' 및 Egatel사의 레트로핏 패널은 기존 모뎀 생태계에 원활하게 통합되어 교체에 따른 부담을 최소화하는 제품의 한 예입니다.

대형 텔레포트용 파라볼라 안테나는 게이트웨이와 대역폭 허브에 여전히 필수적이지만, 기업의 요구는 이동성을 지원하는 폼 팩터로 전환되고 있습니다. 퓨즈(Hughes)사와 QEST사의 위상 배열 안테나는 2024년에 다중 위성 추적 기술을 실증함으로써, 단일 패널로 GEO, MEO, LEO 각 네트워크를 아우를 수 있는 미래를 시사하고 있습니다. 이 아키텍처는 링크의 내결함성을 높이는 동시에, 좁은 선박의 돛대 위 설치 공간을 절약합니다.

지역별 분석

북미는 방위 조달 및 셰일가스 개발을 배경으로 2025년 매출의 34.56%를 차지했으나, 도시 지역의 광섬유 및 5G 인프라가 포화 상태에 이르러 추가적인 성장을 저해하고 있습니다. Viasat의 통합 Ka-밴드 서비스는 캐나다, 미국, 멕시코에 걸친 국경을 초월한 계약상의 마찰을 해소하고, 해당 지역에서의 사업 확장을 가속화하고 있습니다. 2025년부터 2026년에 걸쳐 길라트(Gilat)사와 L3 해리스(L3 Harris)사가 미국 국방부로부터 여러 건의 계약을 수주한 사실은 위성을 통한 이중화 전략의 가치를 입증하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 8.78%를 나타낼 것으로 전망되며, 가장 빠르게 성장하고 있는 지역입니다. 인도, 인도네시아, 말레이시아의 국영 석유 기업들은 지상 통신이 닿지 않는 곳에 위치한 자산의 디지털화를 추진하고 있습니다. SES의 O3b mPOWER를 통한 저지연 연결은 해저 로봇의 운용과 실시간 데이터 공유를 가능하게 하고 있으며, 한편 퍼시픽 베이슨(Pacific Basin)과 미쓰이 OSK 라인(Mitsui OSK Lines)은 IMO의 사이버 복원력 규정을 준수하기 위해 이미 전 선단에 관련 장비를 완비했습니다. 인도네시아의 BRIsat은 은행 네트워크가 국내 위성을 활용하여 농촌 지역의 섬들을 포괄하고 있는 실제 사례를 보여주고 있습니다.

유럽에서는 광섬유망이 잘 구축되어 있어 위성 통신의 광범위한 보급은 제한되고 있지만, 북해의 석유 시추 시설, 발트해 항로, 국방 분야의 기동성 등 특수한 이용 사례가 틈새 시장의 성장을 뒷받침하고 있습니다. 국제전기통신연합(ITU)이 국경을 초월한 방해 행위에 대해 공식적으로 비난한 것은 유럽 대륙의 위성 자산이 지닌 지정학적 민감성을 여실히 드러내고 있습니다. 중동에서는 사우디아라비아의 디지털 경제 비전이 현지 통신 사업자와 전 세계 모뎀 공급업체간의 제휴를 통해 전국적인 확산을 추진하고 있습니다. 오만샛의 소프트웨어 정의 위성, 에스하일샛의 북아프리카 진출, 그리고 코트디부아르에서 유텔샛의 'KONNECT' 계약에 따르면, 신흥 경제국들이 위성을 '유니버설 브로드밴드' 실현을 위한 가장 빠른 경로로 간주하고 있음을 뒷받침하고 있습니다.

남미에서는 브라질의 프레솔트층 자원과 아르헨티나의 셰일 혁명이 호재로 작용하고 있습니다. 아나텔(Anatel)이 2026년 3월에 라이선스를 승인함에 따라 비아샛(Viasat)은 브라질 전역을 커버할 수 있게 되었으며, 한편 트랜스페트로(Transpetro)의 하이브리드 단말기 도입 초기 성과는 구체적인 연료비 절감 효과를 보여주고 있습니다. 아프리카는 여전히 보급률이 낮은 미개척 시장입니다. MTN 코트디부아르와 Eutelsat 간의 용량 계약은 전망이 밝지만, 규제의 파편화와 구매력 제한으로 인해 기업용 VSAT 시스템 시장의 단기 성장 곡선은 완만해지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the enterprise VSAT system market size is expected to increase from USD 8.09 billion in 2025 to USD 8.78 billion in 2026 and reach USD 13.26 billion by 2031, growing at a CAGR of 8.67% over 2026-2031.

This report is Segmented by Component (Hardware and Services), Platform Size (Small Earth Station, Medium Earth Station, and Large Earth Station), Frequency Band (Ku-Band, C-Band, Ka-Band and More), End-User Industry (Oil and Gas, Maritime, Government and Defense, Banking and Financial Services, Telecom and IT, Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise VSAT System Market Trends and Insights

Surging Demand for Broadband Connectivity in Remote and Offshore Sites

Operations in offshore drilling, remote mining, and blue-water shipping now demand symmetric, low-latency links that fiber and cellular often cannot deliver. Petrobras subsidiary Transpetro completed hybrid VSAT and Starlink upgrades across 26 vessels in early 2025, achieving 3-5% fuel savings through optimized routing. Movistar Argentina noted 40% year-over-year growth in satellite subscriptions among contractors in the Vaca Muerta shale as of February 2026. Intellian equipped a Petronas floating LNG unit with triple-redundant terminals, underscoring the sector's willingness to over-provision to avoid costly downtime. ITU radio-regulation frameworks have streamlined licensing, so new enterprise VSAT system market deployments can scale without protracted approvals.

Digital-Oilfield and Smart-Shipping Initiatives Accelerating VSAT Uptake

Sensor-rich drilling programs and data-driven fleet operations convert connectivity into a production enabler. ST Engineering iDirect works with Solutions by stc to monitor wells and refineries under Saudi Arabia's USD 90 billion digital economy initiative. SES and Viasat Energy introduced sub-150 ms services to offshore platforms in Asia-Pacific, enabling real-time robot control. Shipping lines such as Pacific Basin and Mitsui O.S.K. Lines finalized NexusWave retrofits in 2025 to comply with IMO cyber guidelines and cut unplanned dry-dock visits by up to 30%. The enterprise VSAT system market is benefiting as stakeholders treat bandwidth as a performance lever rather than a utility overhead.

High Capex and Opex Relative to Terrestrial Alternatives

VSAT hardware, installation labor, and teleport overhead still exceed terrestrial equivalents where fiber or 5G are present. Component shortages in 2024 pushed gallium arsenide LNA prices from USD 28.50 to USD 175. Public filings show Comtech and KVH carried quarterly operating expenses of USD 136.24 million and USD 30.96 million, respectively, highlighting the fixed-cost burden of 24/7 network operations. While remote users accept the premium, urban enterprises weigh the economics carefully, curbing wider uptake within the enterprise VSAT system market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of HTS Constellations Lowering Bandwidth Cost

- Growth of Cloud-Based Enterprise Applications Requiring Always-On Links

- Spectrum Congestion and Licensing Hurdles in Key Bands

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware-dominated revenue in 2025 thanks to up-front terminal purchases, yet managed offerings are outpacing boxes at 9.98% CAGR. The enterprise VSAT system market size for service contracts is rising as organizations fold bandwidth, cybersecurity, and regulatory compliance into OPEX. L3Harris and Comtech's 5650C2/MP modem simplifies multi-orbit roaming, lowering in-house skill demands. Vendors now bundle orchestration, installation, and ticketing portals, shifting competition toward total cost of ownership rather than sticker price. Integrators leverage bulk capacity deals to shield customers from bandwidth volatility, deepening recurring revenue streams. Hardware innovation continues, Hughes' HM400 airborne modem targets ISR aircraft, but product releases increasingly act as on-ramps to long-term service agreements.

The enterprise VSAT system market, therefore, reflects broader IT outsourcing trends. Enterprises consolidate suppliers, preferring a single throat to choke for uptime SLAs. Vendors respond by acquiring regional installers and investing in network operations centers, shrinking time-to-deploy and standardizing support across geographies. As service portfolios mature, differentiation leans on cybersecurity overlays and API access that integrate satellite links into DevOps toolchains.

Medium earth stations (1.2-2.4 m) balanced gain and cost to win 45.67% share in 2025. Small terminals under 1.2 m, advancing at 9.63% CAGR, benefit from electronically steered arrays that mount flush on decks and vehicles without mechanical gimbals. The enterprise VSAT system market size for compact antennas grows as maritime and defense customers prioritize reduced wind drag, faster installation, and lower maintenance. Orbit's OrBeam MIL and Egatel's retrofit panels exemplify offerings that slide into existing modem ecosystems, minimizing swap-out friction.

Large teleport dishes remain essential for gateways and bandwidth hubs, but enterprise appetite skews toward mobility-ready form factors. Hughes and QEST's phased array proved multi-satellite tracking in 2024, signaling a future where a single panel can roam across GEO, MEO, and LEO networks. This architecture enhances link resiliency while containing topside real estate on cramped vessel masts.

Complete Report Scope:

- By Component

- Hardware

- Services

- By Platform Size

- Small Earth Station (Less Than 1.2 m)

- Medium Earth Station (1.2-2.4 m)

- Large Earth Station (Greater Than 2.4 m)

- By Frequency Band

- Ku-Band

- C-Band

- Ka-Band

- Other Frequency Band

- By End-User Industry

- Oil and Gas

- Maritime

- Government and Defense

- Banking and Financial Services

- Telecom and IT

- Mining

- Energy and Utilities

- Retail

- Other End-User Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America contributed 34.56% of 2025 revenue, underpinned by defense procurement and shale activity, yet urban saturation of fiber and 5G caps incremental growth. Viasat's unified Ka-band service eliminates cross-border contract friction across Canada, the United States, and Mexico, accelerating regional deployments. Multiple U.S. Department of Defense contracts awarded to Gilat and L3Harris during 2025-2026 reinforce the strategic value of satellite redundancy.

Asia-Pacific is the fastest-growing territory with an 8.78% CAGR outlook. National oil companies in India, Indonesia, and Malaysia are digitizing assets that sit beyond terrestrial reach. SES's O3b mPOWER low-latency links empower subsea robot operations and live data collaboration, while Pacific Basin and Mitsui O.S.K. Lines have already outfitted full fleets to meet IMO cyber-resilience rules. Indonesia's BRIsat illustrates how banking networks exploit domestic satellites to blanket rural archipelagos.

Europe's fiber richness restrains broad adoption, yet specialty use cases, North Sea rigs, Baltic shipping, defense mobility, sustain niche growth. The ITU's public censure of cross-border jamming spotlights the geopolitical sensitivity of continental satellite assets. In the Middle East, Saudi Arabia's digital economy vision drives nationwide deployments through partnerships between local telcos and global modem vendors. OmanSat's software-defined satellite, Es'hailSat's North Africa extension, and Eutelsat's KONNECT deal in Cote d'Ivoire confirm that emerging economies view satellite as the quickest route to universal broadband.

South America benefits from Brazil's pre-salt assets and Argentina's shale revolution. Anatel's March 2026 license approvals permit Viasat to blanket Brazil, while Transpetro's early success with hybrid terminals illustrates tangible fuel savings. Africa remains an under-penetrated frontier; capacity deals such as MTN Cote d'Ivoire's with Eutelsat show promise, but fragmented regulation and limited purchasing power moderate the near-term curve of the enterprise VSAT system market.

- Hughes Network Systems LLC

- ViaSat Inc.

- Gilat Satellite Networks Ltd.

- Comtech Telecommunications Corp.

- ST Engineering iDirect

- Newtec

- ND SatCom GmbH

- KVH Industries Inc.

- Signalhorn Trusted Networks GmbH

- CPI International Inc.

- Advantech Wireless Technologies Inc.

- Paradise Datacom LLC

- Satpro M&C Tech Co. Ltd.

- Intellian Technologies Inc.

- Isotropic Systems Ltd.

- Elbit Systems Ltd.

- L3Harris Technologies Inc.

- Ultra Electronics Antennas Group

- Satcom Direct Inc.

- Cobham Satcom

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Broadband Connectivity in Remote and Offshore Sites

- 4.2.2 Digital-Oilfield and Smart-Shipping Initiatives Accelerating VSAT Uptake

- 4.2.3 Expansion of HTS Constellations Lowering Bandwidth Cost

- 4.2.4 Growth of Cloud-Based Enterprise Applications Requiring Always-On Links

- 4.2.5 Emergence of Flat-Panel Electronically Steered Antennas Reducing Installation Footprint

- 4.2.6 Proliferation of 5G Non-Terrestrial Network Standards Unlocking Enterprise-Grade Service Classes

- 4.3 Market Restraints

- 4.3.1 High Capex and Opex Relative to Terrestrial Alternatives

- 4.3.2 Spectrum Congestion and Licensing Hurdles in Key Bands

- 4.3.3 Escalating Cyber-Attacks on Satellite Ground Segment

- 4.3.4 RF Component Supply-Chain Risk Amid Geopolitical Frictions

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Bargaining Power of Buyers

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Services

- 5.2 By Platform Size

- 5.2.1 Small Earth Station (Less Than 1.2 m)

- 5.2.2 Medium Earth Station (1.2-2.4 m)

- 5.2.3 Large Earth Station (Greater Than 2.4 m)

- 5.3 By Frequency Band

- 5.3.1 Ku-Band

- 5.3.2 C-Band

- 5.3.3 Ka-Band

- 5.3.4 Other Frequency Band

- 5.4 By End-User Industry

- 5.4.1 Oil and Gas

- 5.4.2 Maritime

- 5.4.3 Government and Defense

- 5.4.4 Banking and Financial Services

- 5.4.5 Telecom and IT

- 5.4.6 Mining

- 5.4.7 Energy and Utilities

- 5.4.8 Retail

- 5.4.9 Other End-User Industry

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Hughes Network Systems LLC

- 6.4.2 ViaSat Inc.

- 6.4.3 Gilat Satellite Networks Ltd.

- 6.4.4 Comtech Telecommunications Corp.

- 6.4.5 ST Engineering iDirect

- 6.4.6 Newtec

- 6.4.7 ND SatCom GmbH

- 6.4.8 KVH Industries Inc.

- 6.4.9 Signalhorn Trusted Networks GmbH

- 6.4.10 CPI International Inc.

- 6.4.11 Advantech Wireless Technologies Inc.

- 6.4.12 Paradise Datacom LLC

- 6.4.13 Satpro M&C Tech Co. Ltd.

- 6.4.14 Intellian Technologies Inc.

- 6.4.15 Isotropic Systems Ltd.

- 6.4.16 Elbit Systems Ltd.

- 6.4.17 L3Harris Technologies Inc.

- 6.4.18 Ultra Electronics Antennas Group

- 6.4.19 Satcom Direct Inc.

- 6.4.20 Cobham Satcom

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment