|

시장보고서

상품코드

2072621

항공우주 TIC 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aerospace TIC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

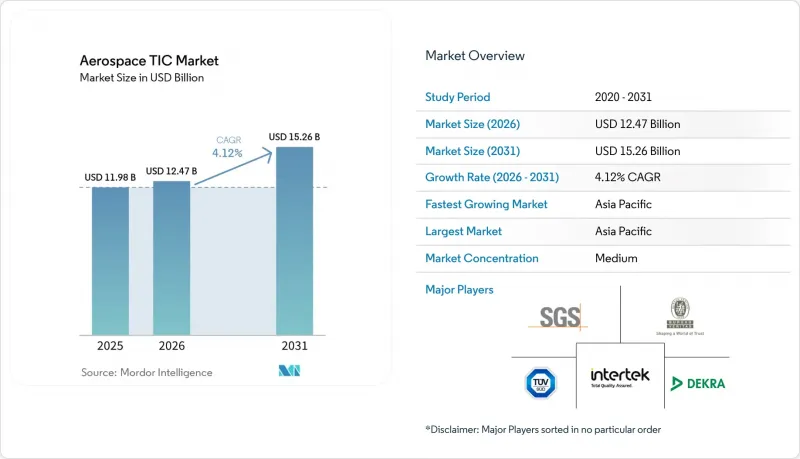

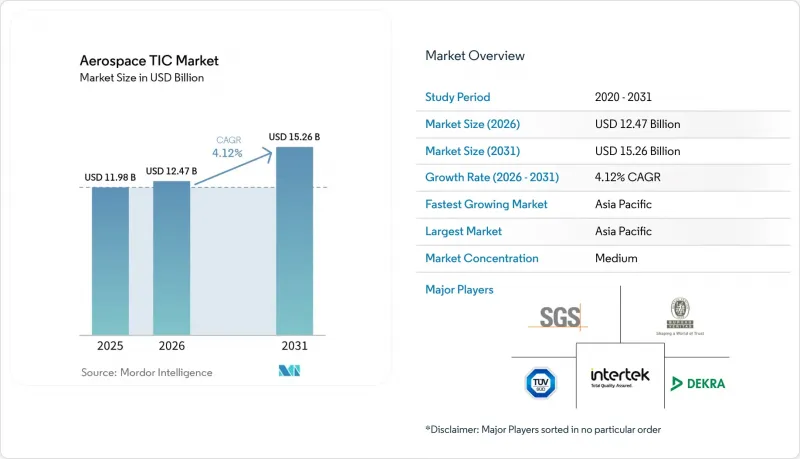

Mordor Intelligence에 의하면, 항공우주 TIC 시장 규모는 2025년 119억 8,000만 달러로 평가되었고, 2026년에는 124억 7,000만 달러로 추정되고, 2031년까지 152억 6,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 4.12%로 성장할 전망입니다.

본 보고서는 서비스 유형별(시험, 검사, 인증), 조달 방식별(사내 수행, 외부 위탁), 서비스 제공 방식별(온사이트, 오프사이트 및 실험실, 원격 및 디지털) 및 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항공우주 TIC 시장 동향 및 인사이트

상용 항공기 생산 증가와 기체 교체

항공우주 TIC 시장은 주요 항공기 제조업체 양측 모두에서 여전히 유례없이 높은 수준을 유지하고 있는 상업용 항공기 생산 기반 덕분에 계속해서 성장세를 이어가고 있습니다. 에어버스는 2025년에 793대의 상업용 항공기를 인도할 예정이며, 상업용 항공기 수주 잔고는 8,754대라고 보고했습니다. 한편, 보잉은 2025년에 600대의 상업용 항공기를 인도할 예정이며, 2026년 1월 기준으로 6,820억 달러 규모의 미인도 주문 잔고를 보고했습니다. 또한 에어버스는 2026년 1분기 민간 항공기 수주 총량이 2025년 1분기의 280대에서 408대로 증가했다고 보고했으며, 민간 항공기 수주 잔고가 9,037대로 늘어났다고 밝혔습니다. 이 미결 주문에 포함된 각 항공기는 자재 허용 기준, 초도품 검사, 인수 시험 및 공급업체 감사와 같은 일련의 과정을 거치기 때문에 항공우주 분야의 TIC 시장에는 단기적인 납품 급증보다는 수년 단위의 수익 기반이 마련됩니다. 또한, 생산 속도 증가로 인해 TIC에 대한 수요는 단순 생산 대수만으로는 예상되는 것보다 훨씬 빠르게 증가할 것입니다. 이는 새로운 공구, 대체 조달처 및 공정 변경이 각각 동일한 항공기 제품군에 대해 추가적인 적합성 확인 주기를 초래하기 때문입니다.

점차 강화되는 내공성, 안전성 및 공급업체 품질에 관한 요건

항공우주 TIC 시장은 주요 항공 관할 구역에서 항공기 감항성 및 공급업체 품질에 대한 감독이 강화되고 있는 점도 호재로 작용하고 있습니다. FAA는 공급업체와 관련된 생산 품질 문제를 계기로, 2026년 5월 26일부터 발효되는 항공 적합성 지시(AD)를 발표하고, 특정 에어버스 A319, A320 및 A321 기체에 대한 두께 검사를 의무화했습니다. EASA 역시 동일한 동체 패널 문제와 관련하여 AD 2026-0055R1을 발령함으로써, 여러 규제 당국 간에 동시에 병행되는 규정 준수 요구 사항이 발생할 수 있음을 시사하고 있습니다. 또한, EASA는 2026년 3월에 '생산 조직용 사용자 가이드'를 업데이트하여 적층 가공(AM) 평가 체크리스트를 추가하는 한편, 공식적인 공급업체 품질 요건을 새로운 생산 분야로까지 확대했습니다. 항공우주 분야의 TIC 시장은 공급업체 차원의 가시성을 높이는 이러한 광범위한 변화의 혜택을 누리고 있습니다. 이는 FAA 및 EASA의 기술 이행 절차(TIP)에 따른 국경을 넘는 검증에는 여전히 방대한 양의 문서, 감사 지원 및 수출용 품질 증빙 자료가 필요하기 때문입니다.

Nadcap 인증 및 FAA·EASA 승인 실험실의 긴 리드타임

인증 시험 기관의 긴 리드타임은 여전히 항공우주 TIC 시장에 있어 가장 시급한 제약 요인으로 남아 있습니다. 퍼포먼스 리뷰 인스티튜트(PRI)가 운영하는 Nadcap은 24개의 주요 공정 인증 프로그램을 포괄하고 있으며, 많은 OEM 및 1차 공급업체 프로그램에 참여를 목표로 하는 공급업체들에게 실질적인 진입점이 되고 있습니다. 초기 인증에는 여전히 엄격한 요건이 적용되므로, 공급업체는 일상적인 고객 프로그램에 참여하기 전에 사내 준비 작업, 프로세스 증거 정비, 감사 준비 및 지속적인 적합성 유지를 수행해야 합니다. 일부 확립된 사례에서 감사 주기가 18개월로 연장된 것은 어느 정도 완화 조치가 되기는 하지만, 신규 시장 진출기업의 진입 과정을 단축하는 것도 아니고, 이용 가능한 시험 정원 부족 문제를 해결하는 것도 아닙니다. 항공기 생산이 인증된 시험 역량의 확대 속도보다 빠르게 증가하고 있기 때문에 항공우주 TIC 시장은 인증, 인가 및 공급업체 승인을 지연시키는 시험 대기 목록으로 인한 일정상의 위험에 계속해서 직면하고 있습니다.

부문별 분석

2025년, 시험 분야는 항공우주 시험·검사·인증(TIC) 시장 점유율의 61.81%를 차지하며 핵심 서비스 분야로서의 위상을 유지했습니다. 이 부문은 활발한 항공기 생산 프로그램과 밀접하게 연계된 비파괴 검사, 재료 시험 및 환경 시뮬레이션 업무를 기반으로 하고 있었습니다. 이러한 기반의 견고함은 구조 하중 시험, 피로 사이클 시험, 초음파 검사 및 항공기 제조의 모든 단계에서 여전히 필수로 요구되는 기타 절차에 대해 수년에 걸쳐 확립된 요구 사항에서 비롯됩니다. 검사 서비스는 주요 인증 단계 사이에 지속적으로 자리 잡고 있었으며, 특히 항공 적합성 제한 문서에 따라 공식 검사 주기가 정의된 정비·수리·정비(MRO) 분야에서 두드러졌습니다. 이러한 기존 기반 덕분에, 새로운 항공기 개념으로 인해 향후 인증 업무 부담이 증가하고 있음에도 불구하고, 항공우주 TIC 시장은 여전히 주로 시험 및 검사에 의존하고 있습니다.

형식 인증 시장은 2031년까지 연평균 성장률(CAGR) 4.25%를 나타낼 것으로 예측되며, 항공우주 TIC 시장에서 가장 빠르게 성장하는 서비스 유형이 될 전망입니다. eVTOL 기체, 모어 일렉트릭 기체, 하이브리드 전기 추진 기체, 수소 연료 기체는 기존의 민간 및 국방용 플랫폼을 넘어 형식 인증 범위를 확대되고 있습니다. FAA의 파워드리프트 프레임워크와 EASA의 SC-VTOL 패스웨이는 사업자가 보다 광범위한 확장에 착수하기 전에 광범위한 시험과 증거를 요구하는 공식적인 절차를 마련했습니다. 도레이의 NCAMP 인증 캠페인 역시, 재료 수준의 승인만으로도 장기간에 걸친 실험실 프로그램이 진행될 수 있기 때문에 인증 작업이 첫 비행보다 훨씬 이전부터 시작된다는 점을 보여주었습니다. 이러한 추세로 인해, 특히 규제 체계가 아직 형성 중인 분야에서 항공우주 TIC 산업의 적용 범위가 확대되고 있습니다.

지역별 분석

아시아태평양은 2025년에 항공우주 TIC 시장 점유율의 41.92%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 4.83%로 성장할 것으로 전망되어, 가장 규모가 크고 가장 빠르게 성장하는 지역 시장이 되고 있습니다. 해당 지역은 인도, 중국, 한국, 일본에서의 제조 활동 확대의 혜택을 받고 있으며, 이에 따라 인증 및 감독이 필요한 공급업체, 부품, 생산 공정의 수가 증가하고 있습니다. 인도에서는 2026년 2월, 타타 어드밴스드 시스템즈(Tata Advanced Systems)가 카르나타카주에서 인도 최초의 민간 부문 에어버스 H125 헬리콥터 최종 조립 라인을 개설한 것이 최근 수요 동향을 보여주는 가장 명확한 징후 중 하나가 되었습니다. 이러한 움직임에 따라 현지 생산이 최종 조립 단계로 더욱 진전됨에 따라, 공급업체 인증, 초기 제품 검사 및 인증 지원에 대한 새로운 수요가 대두되었습니다. 또한, 아시아태평양은 현지 프로그램이 더욱 엄격한 생산 및 정비 규정 준수 체계 하에서 운영될 것으로 기대되는 만큼, 항공우주 TIC 시장에서 그 중요성이 커지고 있습니다.

북미와 유럽은 OEM 및 공급업체로 구성된 견고한 생태계와 성숙한 규제 기관의 지원을 바탕으로, 항공우주 TIC 시장에서 2위의 규모를 차지하고 있습니다. 북미에서는 보잉사가 2025년에 민간 항공기 600대를 인도하였고, 2026년 1월에는 6,820억 달러 규모의 수주 잔고를 보고했는데, 이 모든 요인이 시험 및 검사 수요의 지속을 뒷받침하고 있어 시장은 계속해서 활기를 띠고 있습니다. 또한, 미국은 첨단 항공 모빌리티 인증 분야에서도 계속해서 중심적인 역할을 수행하고 있으며, FAA가 주도하는 에어택시 및 파워리프트 항공기 관련 노력은 기존의 고정익 항공기 프로그램과는 다른 업무 흐름을 만들어내고 있습니다. 유럽에서는 EASA가 2026년 3월에 '생산 조직 승인(POA)'에 관한 지침을 갱신하고, 유인 VTOL 항공기에 대한 공식적인 운용 체계를 수립함으로써 규제 범위를 확대하였으며, 이를 통해 공급업체의 품질 향상과 인증 활동이 촉진되었습니다.

중동 및 아프리카 및 남미는 항공우주 TIC 시장에서 여전히 비교적 작은 비중을 차지하고 있지만, 두 지역 모두 항공기 대수 증가 및 현지 생산 확대 노력에 따른 수요가 국지적으로 나타나고 있습니다. 아랍에미리트(UAE)에서 Strata Syensqo사가 보잉 777X 프로그램의 시험용 부품을 위해 탄소섬유 프리프레그 소재를 대규모로 생산한 사례는 이 지역의 항공용 복합재료 관련 활동이 얼마나 전문적인 소재 시험 및 공정 인증에 대한 수요를 창출하는지를 보여주었습니다. 아프리카에서는 여전히 MRO 주도의 경향이 강하며, 2025년 이집트항공(EGYPTAIR)이 첫 번째 에어버스 A350-900을 인도받은 것은 신형 와이드바디 기단에 대한 추가 점검 및 지원 요건을 부각시켰습니다. 남미에서는 브라질이 엠브라에르의 민간 및 방위 분야 활동을 통해 지역 수요의 중심지 역할을 계속하고 있으며, 국제적인 납품 프로그램에서는 수출 규정 준수 및 제3자에 의한 제품 검증이 여전히 중요한 요소로 남아 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the aerospace TIC market size is expected to increase from USD 11.98 billion in 2025 to USD 12.47 billion in 2026 and reach USD 15.26 billion by 2031, advancing at a CAGR of 4.12% during 2026-2031.

This report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House, and Outsourced), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Aerospace TIC Market Trends and Insights

Rising Commercial Aircraft Production and Fleet Renewal

The aerospace TIC market continues to draw strength from a commercial production base that remains unusually full for both major aircraft manufacturers. Airbus delivered 793 commercial aircraft in 2025 and reported a commercial backlog of 8,754 aircraft, while Boeing delivered 600 commercial aircraft in 2025 and reported a company backlog of USD 682 billion in January 2026. Airbus also reported 408 gross commercial aircraft orders in Q1 2026, up from 280 in Q1 2025, and said its commercial backlog had risen to 9,037 aircraft. Each aircraft in these backlogs passes through a chain of materials allowables, first-article inspection, acceptance testing, and supplier audits, which gives the aerospace TIC market a multi-year revenue base rather than a short-term delivery spike. Rate ramp-ups also raise TIC demand faster than unit output alone suggests, because new tools, substitute sources, and process changes each create additional conformance cycles around the same aircraft family.

Tightening Airworthiness, Safety, and Supplier Quality Mandates

The aerospace TIC market is also being driven forward by stricter airworthiness and supplier-quality oversight in key aviation jurisdictions. The FAA issued an airworthiness directive effective May 26, 2026, requiring thickness inspections on certain Airbus A319, A320, and A321 aircraft following a supplier-related production quality issue. EASA issued AD 2026-0055R1 on the same fuselage-panel issue, demonstrating how parallel compliance demands can arise across multiple regulators simultaneously. EASA also updated its User Guide for Production Organizations in March 2026, adding additive manufacturing assessment checklists and extending formal supplier-quality expectations into a newer production area. The aerospace TIC market is benefiting from this broader shift toward supplier-level visibility because cross-border validation under the FAA and EASA Technical Implementation Procedures still requires substantial documentation, audit support, and export-facing quality evidence.

Long Lead Times At Nadcap-Accredited and FAA-EASA-Recognized Labs

Long lead times at accredited laboratories remain the most immediate constraint on the aerospace TIC market. Nadcap, administered by the Performance Review Institute, covers 24 critical process accreditation programs and serves as a practical entry point for suppliers seeking to participate in many OEM and tier-1 programs. First-time accreditation is still demanding, because suppliers need internal readiness work, process evidence, audit preparation, and sustained conformance before they can enter routine customer programs. The move to 18-month audit intervals in some established cases offers limited relief, but it does not shorten the path for new entrants or solve the shortage of available testing slots. As aircraft production ramps faster than accredited capacity expands, the aerospace TIC market continues to face schedule risk from testing queues that delay qualification, certification, and supplier approvals.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Use of Composites and Advanced Materials

- Growing Outsourcing of Capex-Intensive Qualification Work

- High Cost and Schedule Burden of Multi-Authority Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testing retained 61.81% of the aerospace testing, inspection, and certification (TIC) market share in 2025, maintaining its position as the core service block. The segment remained anchored in non-destructive testing, materials testing, and environmental simulation work that moved directly with active aircraft production programs. Its depth stemmed from long-established requirements for structural load testing, fatigue cycling, ultrasonic inspection, and other procedures that remain mandatory at every aircraft build stage. Inspection services continued to sit between major qualification milestones, especially in maintenance, repair, and overhaul settings where airworthiness limitation documents define formal inspection intervals. This installed base means the aerospace TIC market still depends primarily on testing and inspection, even as newer aircraft concepts broaden future certification workloads.

Certification is projected to grow at a 4.25% CAGR through 2031, making it the fastest-growing service type in the aerospace TIC market. eVTOL aircraft, more-electric aircraft, hybrid-electric propulsion, and hydrogen-fueled aircraft are expanding the scope of type certification beyond traditional commercial and defense platforms. The FAA's powered-lift framework and EASA's SC-VTOL pathway have established formal pathways that require extensive testing and evidence before operators can move toward broader deployment. Toray's NCAMP qualification campaign also showed that certification work begins well before first flight, because material-level acceptance can generate long laboratory programs on its own. That pattern is widening the addressable scope of the aerospace TIC industry, especially in categories where regulatory pathways are still taking shape.

Complete Report Scope:

- By Service Type

- Testing

- Inspection

- Certification

- By Sourcing Type

- In-house

- Outsourced

- By Mode of Service Delivery

- On-site

- Off-site / Laboratory

- Remote / Digital

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

Asia-Pacific held 41.92% of the aerospace TIC market share in 2025 and is projected to grow at a 4.83% CAGR through 2031, making it both the largest and fastest-growing regional market. The region benefits from expanding manufacturing activity in India, China, South Korea, and Japan, which increases the number of suppliers, components, and production processes that need qualification and oversight. India provided one of the clearest recent demand signals when Tata Advanced Systems inaugurated the country's first private-sector helicopter final assembly line for the Airbus H125 in Karnataka in February 2026. That step added fresh need for supplier qualification, first-article inspection, and certification support as local manufacturing moved deeper into final assembly. Asia-Pacific is also becoming more important to the aerospace TIC market because local programs are increasingly expected to operate within stronger production and maintenance compliance frameworks.

North America and Europe formed the second-largest combined block in the aerospace TIC market, supported by deep OEM-supplier ecosystems and mature regulatory institutions. North America remained active because Boeing delivered 600 commercial aircraft in 2025 and reported a company backlog of USD 682 billion in January 2026, both of which support sustained testing and inspection demand. The United States also remains central to advanced air mobility certification, where FAA air-taxi and powered-lift activities are creating workstreams distinct from legacy fixed-wing programs. In Europe, EASA widened the regulatory perimeter through updated Production Organization Approval guidance in March 2026 and formal operating frameworks for manned VTOL-capable aircraft, which increased supplier quality and certification activity.

Middle East and Africa and South America remain smaller parts of the aerospace TIC market, but both regions show pockets of demand tied to fleet growth and localized manufacturing ambitions. In the UAE, Strata Syensqo's large-scale production of carbon fiber prepreg materials for Boeing 777X program test components demonstrated how regional aerocomposites activity can create specialized materials-testing and process-qualification needs. Africa has remained more MRO-led, and EGYPTAIR's first Airbus A350-900 delivery in 2025 highlighted additional inspection and support requirements for newer widebody fleets. In South America, Brazil continues to anchor regional demand through Embraer's commercial and defense activity, where export compliance and third-party product validation remain important to international delivery programs.

- SGS SA

- Bureau Veritas SA

- TUV SUD AG

- Intertek Group plc

- DEKRA SE

- TUV Rheinland AG

- TUV NORD AG

- DNV AS

- Applus Services, S.A.

- Element Materials Technology Group Limited

- Eurofins Scientific SE

- UL LLC

- CSA Group Testing & Certification Inc.

- MISTRAS Group, Inc.

- NTS Technical Systems

- AeroTec Inc.

- IRISNDT Limited

- Applied Technical Services, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Commercial Aircraft Production and Fleet Renewal

- 4.2.2 Tightening Airworthiness, Safety, and Supplier Quality Mandates

- 4.2.3 Growing Outsourcing of Capex-Intensive Qualification Work

- 4.2.4 Expanding Use of Composites and Advanced Materials

- 4.2.5 Certification Demand From More-Electric Aircraft and Advanced Air Mobility Platform

- 4.2.6 Cybersecurity and Software Assurance Becoming Part of Airworthiness

- 4.3 Market Restraints

- 4.3.1 Long Lead Times at Nadcap-Accredited and FAA-EASA-Recognized Labs

- 4.3.2 High Cost and Schedule Burden of Multi-Authority Compliance

- 4.3.3 Scarcity of Aerospace Auditors, DERs, and Specialized Test Talent

- 4.3.4 Export-Control and Data-Residency Frictions in Cross-Border Verification

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Mode of Service Delivery

- 5.3.1 On-site

- 5.3.2 Off-site / Laboratory

- 5.3.3 Remote / Digital

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 Turkey

- 5.4.4.4 Rest of Middle East

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Egypt

- 5.4.5.3 Rest of Africa

- 5.4.6 South America

- 5.4.6.1 Brazil

- 5.4.6.2 Argentina

- 5.4.6.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SGS SA

- 6.4.2 Bureau Veritas SA

- 6.4.3 TUV SUD AG

- 6.4.4 Intertek Group plc

- 6.4.5 DEKRA SE

- 6.4.6 TUV Rheinland AG

- 6.4.7 TUV NORD AG

- 6.4.8 DNV AS

- 6.4.9 Applus Services, S.A.

- 6.4.10 Element Materials Technology Group Limited

- 6.4.11 Eurofins Scientific SE

- 6.4.12 UL LLC

- 6.4.13 CSA Group Testing & Certification Inc.

- 6.4.14 MISTRAS Group, Inc.

- 6.4.15 NTS Technical Systems

- 6.4.16 AeroTec Inc.

- 6.4.17 IRISNDT Limited

- 6.4.18 Applied Technical Services, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment