|

시장보고서

상품코드

2072634

증발 가스(BOG) 압축기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2030년)Boil-off Gas (BOG) Compressor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

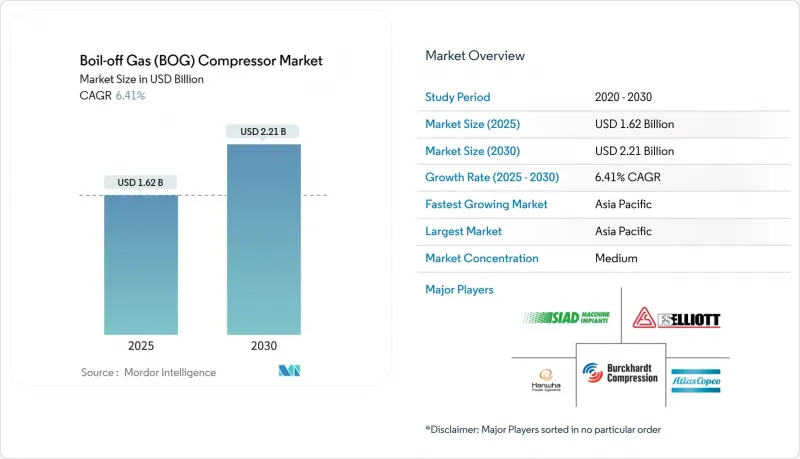

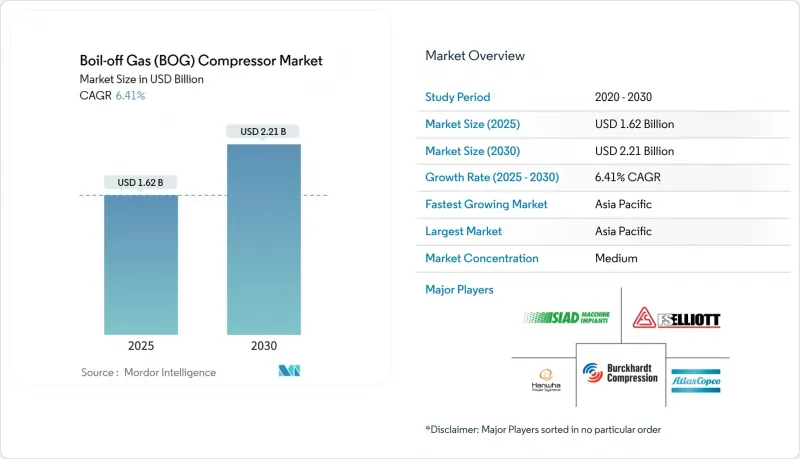

Mordor Intelligence에 의하면, 증발 가스(BOG) 압축기 시장 규모는 2025년에 16억 2,000만 달러로 평가되었고, 예측 기간(2025-2030년) CAGR 6.41%로 성장을 지속할 전망이며, 2030년에는 22억 1,000만 달러에 이를 전망입니다.

본 보고서는 압축기 유형별(원심식, 왕복동식, 스크류식, 기타), 용도별(LNG 운반선, 육상 LNG 터미널, LNG 저장 시설, FLNG 및 FSRU, 산업용 및 기타), 최종 사용자 산업별(해운 및 선박, 석유 및 가스, 유틸리티 및 발전, 석유화학 및 산업용, 기타), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류되어 있습니다.

세계의 증발 가스(BOG) 압축기 시장 동향 및 분석

LNG 무역 확대와 신규 터미널

액화천연가스(LNG) 거래량은 2024년에 4억 1,000만 톤을 넘어섰으며, 카타르와 미국 멕시코만 연안의 새로운 액화 프로젝트에 힘입어 2030년까지 전 세계 생산 능력은 연간 1억 2,000만 톤 증가할 것으로 예측됩니다. 새로운 액화 또는 재기화량 1톤당 그에 상응하는 보일오프 가스 처리가 필요하기 때문에 증발 가스(BOG) 압축기 시장은 뚜렷한 성장이 예상됩니다. 카타르 에너지의 '노스 필드 사우스' 프로젝트만 해도 2024년에 24기의 원심식 압축기 트레인이 발주된 것으로 나타나, 메가 프로젝트가 수년에 걸친 설비 수주 잔고를 확보하고 있는 실태가 여실히 드러나고 있습니다. 아시아태평양은 계속해서 중요한 역할을 수행하고 있으며, 2024년에는 중국에서 3개의 수입 터미널이 가동을 시작할 예정이고, 인도의 페트로넷 LNG사는 다헤지의 처리 능력을 연간 500만 톤 확대할 계획입니다. 수주 주기는 일반적으로 최종 투자 결정 후 12-18개월 뒤에 발생하기 때문에 2024-2025년 체결된 EPC 계약 수주가 2027년까지의 압축기 납품을 뒷받침하게 될 것입니다.

확대되는 LNG 운반선 및 FSRU 선단

이 조선소는 2024년에 신규 LNG 운반선 42척을 인도할 예정이며, 2028년까지 인도 예정인 선박으로 168척의 수주 잔고를 보유하고 있습니다. 전 세계 LNG 수송 능력이 지속적으로 확대되는 가운데, 이 선단의 확장은 LNG 운반선 시장 전체 수요를 더욱 부추기고 있습니다. 신조 선박에는 보일오프 압축을 이용하여 탱크 압력을 0.5-1.5 바르 범위 내로 유지하는 듀얼 연료 엔진이 탑재되어 있습니다. 2025년 1월에 발효되는 IMO 에너지 효율 설계 지수(EEDI) 3단계에 따라, 부분 부하 운전 시 보조 부하를 줄여주는 가변 속도 전기 구동 시스템의 중요성이 더욱 커지고 있습니다. 2024년에는 독일, 필리핀, 베트남을 대상으로 7기의 부유식 저장 및 재기화 설비(FSRU)가 발주되었으며, 각 설비에는 전용 보일오프 처리 라인이 장착되어 있습니다. LNG 운반선 및 FSRU는 20,000시간마다 대규모 정비가 필요하며, 이로 인해 4-5년에 걸친 지속적인 서비스 시장이 형성되어 신조선 사이클 사이의 OEM 수익을 안정시키는 역할을 하고 있습니다.

극저온 설비의 높은 CAPEX 및 OPEX

연간 500만 톤 규모의 터미널용 원심식 압축기 1대의 비용은 800만-1,200만 달러인 반면, 더 소형인 왕복동식 패키지형 압축기는 300만-500만 달러입니다. 3-5년마다 씰, 베어링, 임펠러를 교체해야 하며, 이로 인해 초기 자본 비용의 15%가 운영비에 추가됩니다. 신흥 시장의 구매자들은 통화 약세와 수출 신용 한도 부족으로 어려움을 겪고 있으며, 이로 인해 인식되는 자본 리스크가 더욱 증폭되고 있습니다. 또한, 인증을 받은 극저온 기술자의 임금은 일반 압축기 정비사에 비해 40-60% 높기 때문에 인건비도 장벽이 되고 있습니다. 리스 계약은 자본 부담을 OEM에 전가하지만, 15년 동안 총 소유 비용을 8-12% 상승시켜 버립니다.

부문별 분석

2024년, 원심식 유닛은 증발 가스(BOG) 압축기 시장 점유율의 51.5%를 차지한 것으로 평가되었으며, 2030년까지 연평균 성장률(CAGR) 7.1%로 확대될 것으로 전망됩니다. 이러한 장점은 일일 증발 손실률이 탱크 용적의 0.3%를 초과하는 등, 처리량이 많고 연속 운전이 필요한 용도에 적합하기 때문입니다. 전동 구동으로의 전환에 따라 원심식 압축기의 가동 범위가 확대되고 있습니다. 이는 가변속 모터가 저부하 시 발생할 수 있는 서지 위험을 줄이기 위함입니다. 2024년에 출시된 아트라스코프코의 ZH+ 시리즈는 자기 베어링을 채택함으로써 유지보수 주기를 16,000시간으로 두 배로 늘렸으며, 15년 동안 총 소유 비용을 22% 절감했습니다. 왕복식 압축기는 산업용 가스 등 압력비가 8:1 이상이어야 하는 분야에서 여전히 중요한 역할을 수행하고 있는 반면, 스크류식 압축기는 컴팩트하고 오일 프리 방식의 패키지가 선호되는 해양 및 벙커링과 같은 틈새 시장에 대응하고 있습니다.

디지털화에 따라 원심식, 왕복동식, 스크류식 등 각 모델에 공통된 원격 모니터링 기능이 탑재되면서 제품 간의 경계가 모호해지고 있습니다. 부르크하르트 컴프레션(Burkhardt Compression)사의 ePiston 시스템은 연속적인 압력 감지 기능을 활용하여 밸브의 정비 주기를 30% 연장하고 있습니다. 원심식 1단 압축과 왕복동식 부스터를 결합한 하이브리드 구성은 터미널이 설비를 과도하게 설계하지 않고도 변동하는 보일오프 가스에 대응할 수 있도록 지원하며, 이러한 추세로 인해 증발 가스(BOG) 압축기 시장에서 점유율이 점차 확대될 것으로 예측됩니다.

지역별 분석

아시아태평양은 2024년에 전 세계 매출의 36.2%를 차지한 것으로 평가되었으며, 2030년까지 연평균 7.4%의 복합 성장률을 기록하며 확대될 것으로 전망됩니다. 중국 옌청(Yancheng) LNG 터미널에는 총 용량 120만 m³의 저장 탱크 6기가 설치되어 있으며, 피크 시간대의 보일오프를 관리하기 위해 12기의 원심식 압축기 트레인이 필요합니다. 인도의 재기화 계획에 따라 자이가르(Jaigarh), 담라(Dhamra), 카키나다(Kakinada)에 새로운 터미널이 건설될 예정이며, 이에 따라 압축기의 지속적인 조달이 예상됩니다. 한국에서 석탄에서 가스로의 전환에 따라 기존 발전소 저장 시설의 증기 처리 능력 확충이 필요한 반면, 일본의 터미널 개보수를 통해 계절별 송출의 유연성이 확보될 것입니다. 동남아시아에서는 필리핀과 베트남의 FSRU(부유식 재기화 설비)를 통해 새로운 성장 기회가 창출되고 있으며, 호주의 액화천연가스 수출은 대용량 원심분리기 유닛의 안정적인 교체 시장을 유지하고 있습니다.

북미에서는 미국 멕시코만 연안의 수출 터미널 확장이 주를 이루고 있습니다. Venture Global의 프라크민스 시설에서는 2024년에 18기의 전동 구동식 원심분리기 트레인이 도입되었습니다. 캐나다에서는 허가가 나자마자 브리티시컬럼비아주에서 프로젝트가 이어질 가능성이 있습니다. 러시아산 파이프라인 가스의 대체에 대한 유럽의 시급한 수요로 인해, 독일과 네덜란드에서는 FSRU 도입이 진행되고 있으며, 영국은 2027년까지 그레인 섬의 처리 능력을 연간 200만 톤으로 확대할 계획입니다. EU의 산업 배출 지침 개정에 따라 전동 구동 시스템이 권장되고 있으며, 이는 유럽 대륙의 조달 사양에 영향을 미치고 있습니다.

중동에서는 카타르의 노스필드 사우스 확장 프로젝트가 주를 이루고 있으며, 2024년에 24대의 원심분리기가 조달되었습니다. 아랍에미리트(UAE)의 ADNOC Gas는 같은 해, 루와이스 LNG 프로젝트를 위해 8기의 설비를 엘리엇 그룹에 2억 2,000만 달러에 발주했습니다. 아프리카의 코랄 사우스 FLNG나 모잠비크의 향후 육상 프로젝트는 치안 문제와 인프라 부족으로 인해 제약을 받고 있어, 산발적인 수요가 예상됩니다. 남미에서는 브라질의 프레솔트층이나 아르헨티나의 바카 무에르타 개발에서 제한적인 기회가 나타나고 있지만, 자금 조달 문제로 인해 일정이 지연되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the boil-off gas compressor market size is estimated at USD 1.62 billion in 2025, and is expected to reach USD 2.21 billion by 2030, at a CAGR of 6.41% during the forecast period (2025-2030).

This report is Segmented by Compressor Type (Centrifugal, Reciprocating, Screw, and Others), Application (LNG Carriers, Onshore LNG Terminals, LNG Storage, FLNG and FSRU, and Industrial and Others), End-User Industry (Maritime/Shipping, Oil and Gas, Utilities and Power Generation, Petrochemicals and Industrial, and Others), and Geography (North America, Europe, Asia-Pacific, and More).

Global Boil-off Gas (BOG) Compressor Market Trends and Insights

LNG Trade Expansion & New Terminals

Liquefied natural gas trade surpassed 410 million t in 2024, and new liquefaction projects in Qatar and the U.S. Gulf Coast will lift global capacity by 120 million t pa by 2030. Each tonne of new liquefaction or regasification volume demands parallel boil-off handling, giving the boil-off gas compressor market clear line-of-sight growth. QatarEnergy's North Field South project alone ordered 24 centrifugal trains in 2024, highlighting how mega-projects lock in multi-year equipment backlogs. Asia-Pacific stays pivotal, with three Chinese import terminals online in 2024 and India's Petronet LNG expanding Dahej capacity by 5 million t pa. Order cycles typically trail final investment decisions by 12-18 months, so EPC awards in 2024-2025 underpin compressor deliveries through 2027.

Growing LNG Carrier & FSRU Fleet

Shipyards handed over 42 new LNG carriers in 2024 and hold an orderbook of 168 vessels for handover through 2028. This growing fleet expansion is also reinforcing demand across the LNG carriers market as global LNG transportation capacity continues to increase. Each newbuild integrates dual-fuel engines that rely on boil-off compression to keep tank pressure in the 0.5-1.5 bar envelope. The IMO Energy Efficiency Design Index Phase 3, effective January 2025, raises the premium on variable-speed electric drives that trim auxiliary load at partial operating points. Seven floating storage regasification units were contracted in 2024 for Germany, the Philippines, and Vietnam, each fitted with dedicated boil-off trains. Carriers and FSRUs require major overhauls every 20,000 hours, creating a four-to-five-year rolling service market that cushions OEM revenue between newbuild cycles.

High CAPEX & OPEX of Cryogenic Units

A single centrifugal train for a 5 million t pa terminal costs USD 8-12 million, while smaller reciprocating packages run USD 3-5 million. Over three to five years, seals, bearings, and impellers need replacement, adding 15% of the original capital to operating expense. Emerging-market buyers grapple with currency depreciation and scarce export-credit lines, magnifying perceived capital risk. Labor compounds the hurdle because certified cryogenic technicians command 40-60% wage premiums over general compressor mechanics. Leasing arrangements transfer capital burden to OEMs but inflate total cost of ownership by 8-12% over 15 years.

Other drivers and restraints analyzed in the detailed report include:

- Tighter Methane-Emission Regulations

- Shift to Electric-Drive BOG Packages

- LNG-Price Volatility Delaying FIDs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal units captured 51.5% of the boil-off gas compressor market share in 2024 and are forecast to expand at a 7.1% CAGR through 2030. This dominance stems from their suitability for high-throughput, continuous-duty service where boil-off rates exceed 0.3% of tank volume per day. The shift toward electric drives widens centrifugal operating windows because variable-speed motors mitigate surge risk at low loads. Atlas Copco's ZH+ series, launched in 2024, leverages magnetic bearings to double maintenance intervals to 16,000 hours and cut total ownership cost by 22% over 15 years. Reciprocating compressors remain relevant where pressure ratios above 8:1 are mandatory, such as industrial gas applications, while screw machines cater to offshore and bunkering niches, favoring compact, oil-free packages.

Digitalization blurs product boundaries because centrifugal, reciprocating, and screw models now carry common remote-monitoring overlays. Burckhardt Compression's ePiston system uses continuous pressure sensing to stretch valve overhaul intervals by 30%. Hybrid configurations that marry centrifugal first-stage compression with reciprocating boosters help terminals handle variable boil-off without oversizing equipment, a trend expected to secure incremental share within the boil-off gas compressor market.

Complete Report Scope:

- By Compressor Type

- Centrifugal

- Reciprocating (Piston)

- Screw

- Others

- By Application

- LNG Carriers

- Onshore LNG Terminals

- LNG Storage

- FLNG and FSRU

- Industrial and Others

- By End-User Industry

- Maritime/Shipping

- Oil and Gas

- Utilities and Power Generation

- Petrochemicals and Industrial

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific generated 36.2% of global revenue in 2024 and is projected to compound at 7.4% annually to 2030. China's Yancheng LNG terminal will house six storage tanks totaling 1.2 million m3 and require 12 centrifugal trains to manage peak boil-off. India's regasification blueprint involves new terminals at Jaigarh, Dhamra, and Kakinada, supporting sustained compressor procurement. South Korea's coal-to-gas pivot demands additional vapor-handling at existing power-plant storage, while Japan's terminal upgrades ensure seasonal send-out flexibility. Southeast Asia offers frontier growth via FSRUs in the Philippines and Vietnam, and Australia's liquefaction exports keep a steady replacement market for high-capacity centrifugal units.

U.S. Gulf Coast export-terminal expansions dominate North America. Venture Global's Plaquemines facility installed 18 electric-drive centrifugal trains in 2024. Canada may follow with projects in British Columbia once permitting clears. Europe's urgency to replace Russian pipeline gas has driven FSRU deployments in Germany and the Netherlands, and the United Kingdom plans to enlarge Isle of Grain capacity by 2 million t pa by 2027. EU Industrial Emissions Directive updates favor electric-drive systems, influencing continental procurement specifications.

The Middle East centers on Qatar's North Field South expansion, which procured 24 centrifugal trains in 2024. ADNOC Gas in the United Arab Emirates awarded Elliott Group USD 220 million for eight trains at Ruwais LNG the same year. Africa's Coral South FLNG and Mozambique's future onshore projects offer sporadic demand, constrained by security and infrastructure deficits. South America presents selective opportunities in Brazil's pre-salt and Argentina's Vaca Muerta developments, though financing obstacles extend timelines.

- Atlas Copco

- Burckhardt Compression

- Elliott Group

- Siemens Energy

- Baker Hughes

- Hanwha Power Systems

- Wartsila

- Tamrotor Marine Compressors

- IHI Corp.

- SIAD Macchine Impianti

- MAN Energy Solutions

- Kobelco

- Neuman & Esser

- Ebara Corp.

- Termomeccanica Industrial Compressors

- Howden Group

- BORSIG ZM Compression

- Barber-Nichols

- Gardner Denver (Ingersoll Rand)

- Cryostar

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LNG trade expansion & new terminals

- 4.2.2 Growing LNG carrier & FSRU fleet

- 4.2.3 Tighter methane-emission regulations

- 4.2.4 Shift to electric-drive BOG packages

- 4.2.5 Legacy-asset retrofit wave

- 4.2.6 Export-credit green-finance criteria

- 4.3 Market Restraints

- 4.3.1 High CAPEX & OPEX of cryogenic units

- 4.3.2 LNG-price volatility delaying FIDs

- 4.3.3 Compression-free re-liquefaction tech

- 4.3.4 Skilled cryogenic-maintenance gap

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Compressor Type

- 5.1.1 Centrifugal

- 5.1.2 Reciprocating (Piston)

- 5.1.3 Screw

- 5.1.4 Others

- 5.2 By Application

- 5.2.1 LNG Carriers

- 5.2.2 Onshore LNG Terminals

- 5.2.3 LNG Storage

- 5.2.4 FLNG and FSRU

- 5.2.5 Industrial and Others

- 5.3 By End-User Industry

- 5.3.1 Maritime/Shipping

- 5.3.2 Oil and Gas

- 5.3.3 Utilities and Power Generation

- 5.3.4 Petrochemicals and Industrial

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Atlas Copco

- 6.4.2 Burckhardt Compression

- 6.4.3 Elliott Group

- 6.4.4 Siemens Energy

- 6.4.5 Baker Hughes

- 6.4.6 Hanwha Power Systems

- 6.4.7 Wartsila

- 6.4.8 Tamrotor Marine Compressors

- 6.4.9 IHI Corp.

- 6.4.10 SIAD Macchine Impianti

- 6.4.11 MAN Energy Solutions

- 6.4.12 Kobelco

- 6.4.13 Neuman & Esser

- 6.4.14 Ebara Corp.

- 6.4.15 Termomeccanica Industrial Compressors

- 6.4.16 Howden Group

- 6.4.17 BORSIG ZM Compression

- 6.4.18 Barber-Nichols

- 6.4.19 Gardner Denver (Ingersoll Rand)

- 6.4.20 Cryostar

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

(주말 및 공휴일 제외)