|

시장보고서

상품코드

2072639

의료 분야 인지 기능 평가 및 트레이닝 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cognitive Assessment and Training In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

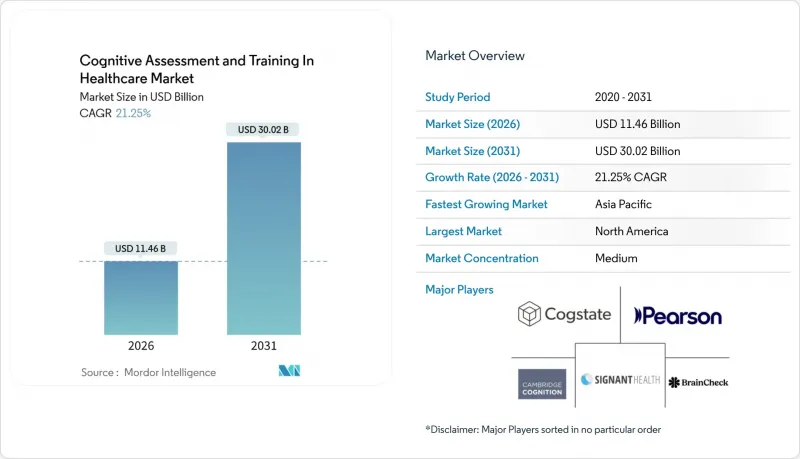

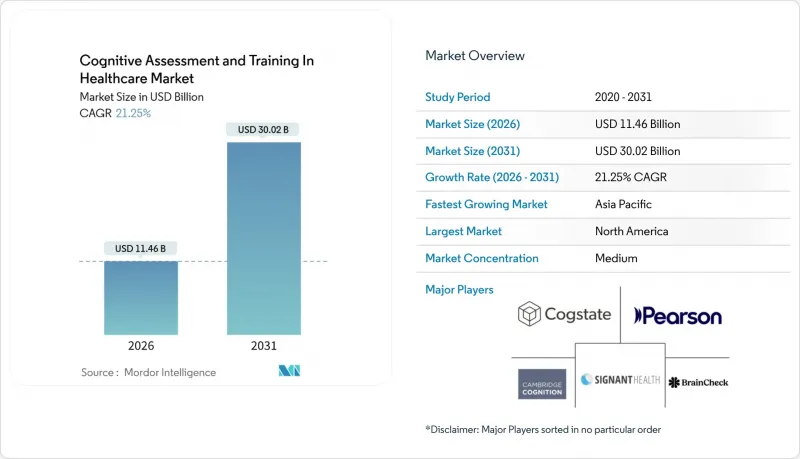

Mordor Intelligence에 의하면, 의료 분야 인지 기능 평가 및 트레이닝 시장 규모는 2026년에 114억 6,000만 달러로 추정되고, 예측 기간(2026-2031년) CAGR 21.25%로 확대될 전망이며, 2031년에는 300억 2,000만 달러에 이를 전망입니다.

본 보고서는 구성 요소별(솔루션, 서비스), 평가 유형별(스크리닝 및 진단, 임상시험 등), 제공 형태별(컴퓨터 기반 등), 용도별(치매 및 알츠하이머병, 외상성 뇌손상 등), 최종 사용자별(의료 제공업체, 보험사 등), 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의료 분야 인지 기능 평가 및 트레이닝 시장 동향과 인사이트

신경퇴행성 질환의 유병률 증가

2024년에는 5,500만 명이 치매를 앓고 있었으며, 전 세계 환자 수는 2030년까지 7,800만 명, 2050년까지 1억 3,900만 명에 달할 것으로 예측됩니다. 따라서 의료 시스템은 1차 의료 현장에서 예방적 인지 기능 선별 검사로 전환되고 있습니다. 2025년에는 디지털 검사를 통한 조기 발견으로 인해 중등도 치매로의 진행이 평균 18개월 지연되었으며, 환자 1인당 장기 요양 비용을 5만 달러 절감할 수 있었습니다. 제약 기업들은 미미한 유효성 징후를 포착하고 개발 기간을 최대 9개월 단축하기 위해 알츠하이머병 2상 임상시험에 이러한 도구를 도입하고 있습니다. 2024년, 치매로 인한 경제적 부담이 1조 3,000억 달러를 넘어섬에 따라, 고액의 시설 입소 돌봄을 미룰 수 있는 대규모 평가 프로그램에 대한 보험사 측의 지원이 활발해졌습니다. 그 결과, 의료 분야 인지 기능 평가 및 트레이닝 시장은 임상적 시급성과 경제적 인센티브 모두로부터 계속해서 혜택을 받고 있습니다.

디지털 헬스 및 m헬스 플랫폼의 급속한 확산

2024년 1월부터 2025년 12월 사이에, 인지 기능 평가용 디지털 기기 12종이 FDA 승인을 받았으며, 그중 5종은 스마트폰에서 완벽하게 작동합니다. 메디케어의 2025년 규정 변경에 따라, 원격 신경심리학 세션은 CPT 96132에 근거하여 보험 적용 대상이 되었으며, 지방에 거주하는 환자들의 병원 방문 부담이 줄어들었습니다. 영국의 MHRA(의약품 및 의료기기 규제청)는 현재, 선행 제품이 존재하는 경우 의료기기로서의 소프트웨어(SaaS)형 인지 기능 평가 도구에 대해, 완전한 임상시험 대신 알고리즘적 동등성을 근거로 삼는 것을 인정하고 있습니다. 매주 실시되는 자가 검사를 통해, 일회성 내원만으로는 파악할 수 없는 개인별 변동을 파악할 수 있어, 치료를 실시간으로 조정할 수 있게 됩니다. 이 기능은 바이오젠이 2024년에 레카네맙에 대한 승인을 신청했을 때, 디지털 평가 지표를 통해 종이 기반 척도보다 4개월 더 빨리 치료 효과가 확인된 점에서 매우 중요한 역할을 했습니다.

데이터 개인정보 보호 및 HIPAA/GDPR(EU 개인정보보호규정) 규정 준수 부담

2024년, 의료 분야의 정보 유출로 인한 평균 비용은 1,090만 달러에 달했으며, 시계열 인식 데이터 세트는 랜섬웨어의 매력적인 표적이 되고 있습니다. GDPR(EU 개인정보보호규정)에서는 인식 데이터를 '특별 카테고리 정보'로 취급하고 있으며, 공급업체는 암호화 및 제3자 감사를 도입해야 할 의무가 있습니다. 2024년에는 조사관에 의한 접근 제어 미비 사실이 드러남에 따라, 한 벤더가 HIPAA 위반으로 480만 달러의 벌금을 부과받는 사태가 발생했으며, 이에 따라 규정 준수 체제가 충분히 갖춰지지 않은 스타트업 기업에 대한 벤처 자금 조달이 주춤하고 있습니다. 소규모 D2C(소비자 직접 판매) 플랫폼의 경우, GDPR(EU 개인정보보호규정) 준수를 위한 호스팅 비용으로 발생하는 40-60%의 추가 비용을 부담하기보다는 유럽연합(EU) 시장에서 철수하는 사례가 적지 않습니다.

부문별 분석

서비스 부문의 매출액은 2031년까지 연평균 성장률(CAGR) 22.25%로 증가할 것으로 예상되며, 2025년에 61.55%의 점유율을 차지한 솔루션 부문과의 격차를 좁힐 전망입니다. 병원 네트워크 분야에서는 신경심리학자와 데이터 사이언스자의 부족이 지적되고 있으며, 소프트웨어, 해석, 전자건강기록(EHR) 통합을 하나의 패키지로 묶은 아웃소싱 계약이 활성화되고 있습니다. “'솔루션' 해당 부서는 오픈소스 대체 수단으로 인한 이익률 압박에 직면해 있는 한편, '서비스' 부서는 실행 가능한 인사이트를 제공함으로써 프리미엄 요금을 확립하고 있습니다. 가치 기반 의료 모델이 시간 경과에 따른 추적 관찰을 중시하게 됨에 따라, '서비스' 헬스케어 분야에서 해당 부문이 차지하는 인지 평가 및 훈련 시장 규모는 2031년까지 140억 달러를 넘어설 것으로 예측됩니다.

주요 매니지드 서비스 기업들은 비정상적인 점수를 실시간으로 경고하는 품질 보증 대시보드를 도입하고 있으며, 이 기능은 현재 제약 기업 스폰서들이 조달 기준의 상위 3개 항목으로 꼽고 있습니다. ACO(Accountable Care Organization)는 주간 인지 기능 업데이트 정보를 치매 치료 경로에 통합함으로써, 임상의의 업무 부담을 가중시키지 않으면서도 맞춤형 개입을 가능하게 하고 있습니다. 지불자의 품질 평가 지표가 발전함에 따라, 플랫폼과 전문가의 해석을 결합한 하이브리드형 공급업체가 의료 분야 인지 기능 평가 및 트레이닝 시장에서 소프트웨어 전문 공급업체를 능가하는 성장을 이룰 것으로 전망됩니다.

임상시험은 연평균 성장률(CAGR) 22.15%의 속도로 진행되고 있으며, 이는 규제 당국이 스마트폰 기반의 인지 기능 평가 지표를 수용하고 있음을 반영합니다. 스크리닝 및 진단 분야는 여전히 가장 큰 점유율을 차지하고 있지만, 보험 급여 제한으로 인해 임상시험 수요에 비해 성장세는 둔화될 전망입니다. 스폰서는 피험자 등록 기간을 단축하기 위해 검사 1회당 비용을 아낌없이 예산에 반영하고 있으며, 이로 인해 공급업체는 65%가 넘는 이익률을 유지하고 있습니다. 임상시험과 관련된 의료 분야 인지 기능 평가 및 트레이닝 시장 점유율은 2031년까지 25%에 근접할 가능성이 있습니다.

표준화는 네트워크 효과를 가져옵니다. 더 많은 스폰서가 동일한 디지털 검사 배터리를 채택함에 따라, 규제 당국은 그 심리 측정 특성에 익숙해지고 신뢰도는 더욱 높아질 것입니다. CRO(임상시험 수탁기관)는 턴키 솔루션에 인지 기능 검사 모듈을 통합하여, 디지털 엔드포인트를 단순한 부가 기능이 아닌 표준 구성 요소로 삼고 있습니다. 학술 컨소시엄도 집단 연구에 이러한 도구를 도입하고 있어, 시장의 선순환을 뒷받침하고 있습니다.

지역별 분석

북미는 2025년 매출의 38.45%를 차지했으며, 그 원동력은 메디케어의 원격 검사 보험 적용과 재향군인보건국이 900만 명의 수급자를 대상으로 실시하는 의무적 기초 검진입니다. 캐나다 온타리오주는 2027년까지 치매 검사의 디지털화를 위해 1억 5,000만 캐나다 달러의 예산을 편성했으나, 규제 당국의 승인 지연으로 인해 단기적인 성과가 제한되고 있습니다. 멕시코의 2025년 치매 대책 계획에서는 선별 검사가 우선시되고 있지만, 농촌 지역의 스마트폰 보급률이 낮아 초기 도입이 더딘 상황입니다. 기존 기업들은 보험사 네트워크와 수십 년에 걸친 검증 데이터를 활용하고 있으며, 이는 북미 의료 분야 인지 기능 평가 및 트레이닝 시장에서 신규 진출기업들에게 높은 진입 장벽으로 작용하고 있습니다.

아시아태평양은 2031년까지 22.22%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 중국에서는 65세 이상의 성인(1억 9,000만 명)을 대상으로 연 1회 인지 기능 검사를 의무화하고 있습니다. 인도는 2028년까지 1차 의료 센터를 통해 5,000만 건의 선별 검사를 실시하는 것을 목표로 하고 있습니다. 일본에서는 고령화가 진행되는 인구 구조와 300억 엔 규모의 디지털 헬스 기금 덕분에 재택 모니터링 도입이 촉진되고 있습니다. 호주에서는 기억 클리닉의 보급률이 42%에 달하지만, 절대적인 건수는 여전히 적은 임베디드니다. 한국의 국가 치매 계획에서는 2030년까지 80%의 커버리지를 목표로 하고 있으며, 연간 1,500만 건의 평가를 처리할 수 있는 플랫폼에 대한 수요가 발생하고 있습니다.

유럽, 중동 및 아프리카, 남미의 상황은 제각각입니다. 독일에서는 낮은 보험 환급률과 사전 승인 절차의 장벽이 1차 진료 현장에서의 도입을 가로막고 있습니다. 영국에서는 50개 진료소에서 디지털 검사 시범 사업이 진행되고 있지만, 예산 제약으로 인해 전국적인 확대가 지연되고 있습니다. 프랑스는 2029년까지 컴퓨터화된 도구를 포함한 조기 발견을 위한 인프라 구축에 4억 유로를 배정하고 있습니다. 아랍에미리트(UAE)와 사우디아라비아는 디지털 헬스 로드맵에 인지 기능 검사를 포함시키고 있지만, 인구 기반이 제한적이기 때문에 수익 창출 가능성에는 한계가 있습니다. 브라질에서는 재정 긴축으로 인해 공공 부문에서의 도입이 정체되어 있는 반면, 남아프리카공화국의 사립 병원에서는 유럽과 비슷한 수준의 도입률을 보이고 있습니다. 이러한 격차로 인해, EMEA(유럽·중동 및 아프리카)와 남미를 합친 '의료 분야 인지 기능 평가 및 트레이닝' 시장 성장률은 세계 평균보다 낮을 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the cognitive assessment and training in healthcare market size is estimated at USD 11.46 billion in 2026, and is expected to reach USD 30.02 billion by 2031, at a CAGR of 21.25% during the forecast period (2026-2031).

This report is Segmented by Component (Solutions, Services), Assessment Type (Screening & Diagnostics, Clinical Trials, and More), Delivery Mode (Computer-Based and More), Application (Dementia & Alzheimer's, Traumatic Brain Injury, and More), End-User (Healthcare Providers, Payers and More), and Geography (North America and More). Market Forecasts are Provided in Terms of Value (USD).

Global Cognitive Assessment and Training In Healthcare Market Trends and Insights

Growing Prevalence of Neuro-Degenerative Disorders

Fifty-five million people were living with dementia in 2024, and the global tally is expected to climb to 78 million by 2030 and 139 million by 2050. Health systems are therefore shifting toward proactive cognitive screening at primary-care touchpoints. Early detection through digital tests slowed progression to moderate dementia by 18 months on average in 2025, saving USD 50,000 per patient in long-term care outlays. Pharmaceutical sponsors embed these tools in Phase II Alzheimer's trials to capture subtle efficacy signals and shorten timelines by up to nine months. The economic burden of dementia exceeded USD 1.3 trillion in 2024, galvanizing payer support for large-scale assessment programs that can defer costly institutional care. As a result, the Cognitive Assessment and Training in Healthcare market continues to benefit from both clinical urgency and economic incentives.

Rapid Adoption of Digital Health & mHealth Platforms

Twelve digital devices for cognitive testing cleared the FDA between January 2024 and December 2025, five of which run entirely on smartphones. Tele-neuropsychology sessions are reimbursed under CPT 96132 following Medicare's 2025 rule change, removing travel friction for patients in rural areas. The United Kingdom's MHRA now permits software-as-a-medical-device cognitive tools to rely on algorithmic equivalence rather than full clinical trials when predicates exist. Weekly at-home tests capture intra-individual variability that one-off clinic visits miss, enabling real-time therapy adjustments. This capability was pivotal in Biogen's 2024 lecanemab filing, where digital endpoints revealed treatment effects four months earlier than paper scales.

Data-Privacy & HIPAA / GDPR Compliance Burden

Average breach costs in healthcare reached USD 10.9 million in 2024, making longitudinal cognitive datasets an attractive ransomware target. GDPR treats cognitive data as special-category information, forcing vendors to adopt encryption and third-party audits. A vendor paid USD 4.8 million in HIPAA fines in 2024 after investigators uncovered lax access controls, damping venture funding for startups without mature compliance infrastructures. Smaller direct-to-consumer platforms often exit the European Union rather than absorb the 40-60% premium for GDPR-compliant hosting.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Endorsement of Computerized Cognitive Tools

- Rising CNS Clinical-Trial Spend for Cognitive End-Points

- Limited Reimbursement Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is projected to climb at 22.25% CAGR through 2031, closing the gap with Solutions, which held 61.55% share in 2025. Hospital networks cite shortages of neuropsychologists and data scientists, prompting outsourced contracts that bundle software, interpretation, and EHR integration. Solutions face margin compression from open-source alternatives, while Services command premium rates for actionable insights. The Cognitive Assessment and Training in Healthcare market size captured by Services is expected to surpass USD 14 billion by 2031 as value-based care models reward longitudinal tracking.

Managed-service leaders employ quality-assurance dashboards that flag anomalous scores in real time, a feature pharmaceutical sponsors now list as a top-three procurement criterion. Accountable care organizations integrate weekly cognitive updates into dementia pathways, triggering personalized interventions without clinician bottlenecks. As payer quality metrics evolve, hybrid vendors that combine platforms with expert interpretation will outpace pure-play software providers in the Cognitive Assessment and Training in Healthcare market.

Clinical Trials are on pace for a 22.15% CAGR, reflecting regulators' acceptance of smartphone-based cognitive endpoints. Screening & Diagnostics still commands the largest slice, yet reimbursement constraints will slow growth relative to trial demand. Sponsors budget generous per-test fees to cut enrollment timelines, allowing vendors to sustain margins above 65%. The Cognitive Assessment and Training in Healthcare market share attached to Clinical Trials could approach 25% by 2031.

Standardization delivers network effects: as more sponsors adopt the same digital battery, regulators become familiar with its psychometrics, further boosting credibility. CROs embed cognitive testing modules into turnkey offerings, making digital endpoints a default rather than an add-on. Academic consortia also adopt these tools for population studies, reinforcing the market flywheel.

Complete Report Scope:

- By Component

- Solutions

- Services

- By Assessment Type

- Screening & Diagnostics

- Clinical Trials

- Academic & Research

- By Delivery Mode

- Computer-based Testing

- Mobile / App-based Testing

- Pen-and-Paper

- By Application

- Dementia & Alzheimer's

- Traumatic Brain Injury

- Learning Disabilities

- Mental Health Screening

- By End-User

- Healthcare Providers

- Payers

- Pharmaceutical & Biotech

- Home-care & Patients

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 38.45% of 2025 revenue, anchored by Medicare's remote-testing coverage and the Veterans Health Administration's compulsory baseline screening for 9 million beneficiaries. Canada's Ontario province budgeted CAD 150 million through 2027 to digitize dementia testing, yet slower regulatory clearance tempers short-term gains. Mexico's 2025 dementia plan prioritizes screening, but limited smartphone penetration in rural districts curbs early uptake. Incumbents leverage payer networks and decades of validation data, presenting high entry barriers for newcomers in the North American Cognitive Assessment and Training in Healthcare market.

Asia-Pacific will deliver the fastest 22.22% CAGR to 2031. China mandates annual cognitive tests for adults aged 65+, a cohort of 190 million. India targets 50 million screenings by 2028 via primary-care health centers. Japan's aging demographics and JPY 30 billion digital health fund fuel home-based monitoring adoption. Australia boasts 42% penetration among memory clinics, but absolute volumes remain modest. South Korea's national dementia plan aims for 80% coverage by 2030, creating demand for platforms that handle 15 million annual assessments.

Europe, the Middle East, Africa, and South America form a heterogeneous landscape. Germany's low reimbursement and prior-authorization hurdles deter primary-care adoption. The U.K. has piloted digital testing across 50 clinics, yet budget constraints delay national rollout. France allocates EUR 400 million through 2029 for early detection infrastructure, including computerized tools. The UAE and Saudi Arabia include cognitive testing in digital health roadmaps, but limited population bases cap revenue potential. Brazil's public-sector rollout is stalled by fiscal austerity, while South Africa's private hospitals mirror European adoption rates. These disparities will keep EMEA and South America's combined Cognitive Assessment and Training in Healthcare market growth below the global average.

- AnthroTronix

- BrainCheck

- BrainHQ

- Cambridge Cognition

- CogniFit

- Cogstate

- LearningRx

- Lumos Labs

- MedAvante-ProPhase

- Neurotrack

- NovaTech

- Oxford University Press (CANTAB)

- Pearson PLC

- Posit Science

- Savonix

- Signant Health

- VeraSci

- WCG Clinical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing prevalence of neuro-degenerative disorders

- 4.2.2 Rapid adoption of digital health & mHealth platforms

- 4.2.3 Regulatory endorsement of computerized cognitive tools

- 4.2.4 Rising CNS clinical-trial spend for cognitive end-points

- 4.2.5 Integration with wearable neuro-biomarker ecosystems

- 4.2.6 Employer-sponsored brain-wellness benefits

- 4.3 Market Restraints

- 4.3.1 Data-privacy & HIPAA / GDPR compliance burden

- 4.3.2 Limited reimbursement pathways

- 4.3.3 Cultural / linguistic bias in AI algorithms

- 4.3.4 Lack of harmonised clinical-validation standards

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Supplier Power

- 4.6.2 Buyer Power

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Assessment Type

- 5.2.1 Screening & Diagnostics

- 5.2.2 Clinical Trials

- 5.2.3 Academic & Research

- 5.3 By Delivery Mode

- 5.3.1 Computer-based Testing

- 5.3.2 Mobile / App-based Testing

- 5.3.3 Pen-and-Paper

- 5.4 By Application

- 5.4.1 Dementia & Alzheimer's

- 5.4.2 Traumatic Brain Injury

- 5.4.3 Learning Disabilities

- 5.4.4 Mental Health Screening

- 5.5 By End-User

- 5.5.1 Healthcare Providers

- 5.5.2 Payers

- 5.5.3 Pharmaceutical & Biotech

- 5.5.4 Home-care & Patients

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AnthroTronix

- 6.3.2 BrainCheck

- 6.3.3 BrainHQ

- 6.3.4 Cambridge Cognition

- 6.3.5 CogniFit

- 6.3.6 Cogstate

- 6.3.7 LearningRx

- 6.3.8 Lumos Labs

- 6.3.9 MedAvante-ProPhase

- 6.3.10 Neurotrack

- 6.3.11 NovaTech

- 6.3.12 Oxford University Press (CANTAB)

- 6.3.13 Pearson PLC

- 6.3.14 Posit Science

- 6.3.15 Savonix

- 6.3.16 Signant Health

- 6.3.17 VeraSci

- 6.3.18 WCG Clinical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment