|

시장보고서

상품코드

2072649

IT 및 기술 분야 인재 확보 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Talent Acquisition In IT And Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

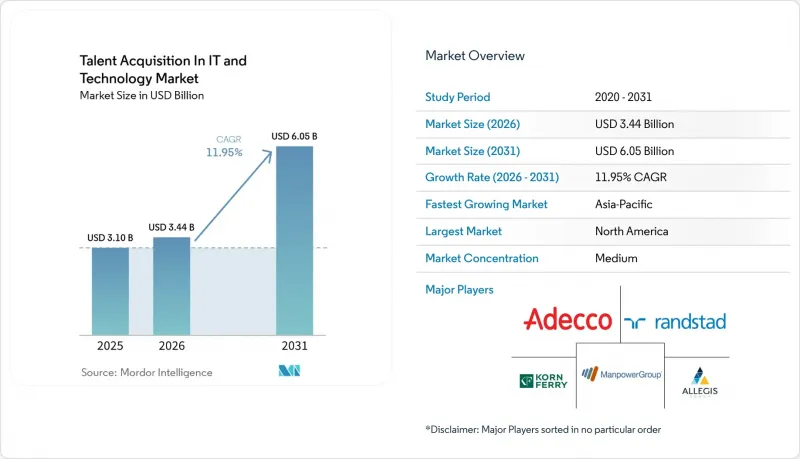

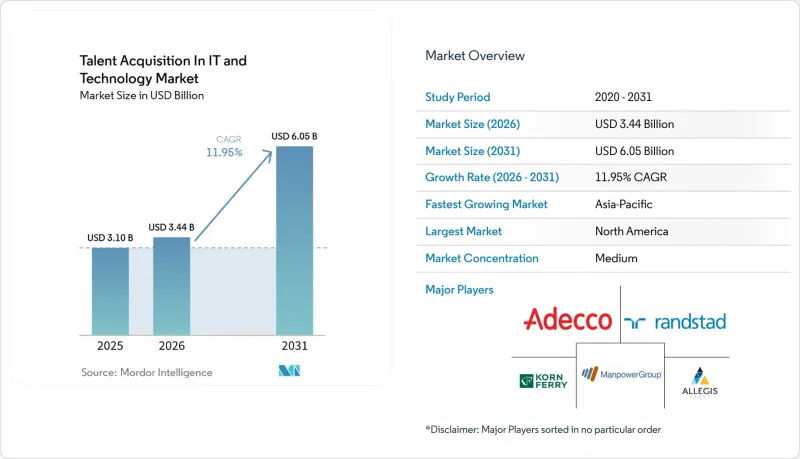

Mordor Intelligence에 의하면, IT 및 기술 분야 인재 확보 시장 규모는 2025년에 31억 달러로 평가되었고, 2026년 34억 4,000만 달러로 추정되고, 2031년까지 60억 5,000만 달러로 성장할 것으로 전망되며, 예측 기간(2026-2031년) CAGR은 11.95%로 추정되고 있습니다.

본 보고서는 구성 요소별(소프트웨어 솔루션, 서비스), 배포 방식별(온프레미스, 클라우드, 하이브리드), 기업 규모별(대기업, 중소기업), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 IT 및 기술 분야 인재 확보 시장 동향과 인사이트

신기술 분야의 기술 인력 부족 심화

디지털 투자가 확대됨에 따라 고용주가 충원을 필요로 하는 기술직의 수는 여전히 증가하고 있으며, 이는 IT 및 기술 분야 인재 확보 시장에서 꾸준한 수요를 뒷받침하고 있습니다. 미국의 기술 분야 고용은 2026년에 1.9% 증가할 것으로 예상되며, 약 12만 8,000개의 일자리가 창출될 전망입니다. 이로 인해 희소한 기술 역량을 두고 경쟁하는 고용주들의 채용 부담은 더욱 커지게 될 것입니다. 현재 고용주들은 단순한 이력서만으로는 평가하기 어려운 AI, 클라우드, 데이터, 보안 분야의 기술을 갖춘 후보자를 찾고 있기 때문에 채용 기준이 더욱 엄격해지고 있습니다. 그 결과, IT 및 기술 분야 인재 확보 시장에서는 단순히 광범위한 지원서를 접수하는 것뿐만 아니라, 정밀한 인재 발굴, 기술 평가, 체계적인 선발 워크플로우에 대한 수요가 높아지고 있습니다. 따라서 디지털 전환을 뒷받침하는 지출 사이클은 특히 기술 인재 채용 규모가 사내 채용 능력을 웃도는 속도로 증가하고 있는 분야에서 플랫폼 투자의 선행 지표 역할을 하고 있습니다.

기술 기업에서의 디지털 전환 가속화

신기술 분야의 인력 부족이 더욱 심화되고 있는 점도 IT 및 기술 분야 인재 확보 시장을 뒷받침하고 있습니다. 2026년에는 72%의 조직이 공석인 직책의 채용에 어려움을 겪고 있으며, AI 모델 개발 및 AI 소양은 조사 사상 처음으로 기존의 엔지니어링 기술을 제치고 확보하기 가장 어려운 역량으로 꼽혔습니다. 2026년 4월 기준으로, 미국 기술 관련 채용 공고의 71%에 AI 기술 요건이 명시되어 있으며, 이는 2023년의 10% 미만에서 크게 증가한 수치입니다. 이는 고용주 수요가 얼마나 급격하게 변화했는지를 보여줍니다. 이러한 변화는 AI 및 머신러닝 분야의 기술적 역량을 키워드 검색만으로는 확실하게 평가할 수 없기 때문에 평가 중심의 채용이 갖는 중요성을 부각시키고 있습니다. 따라서 IT 및 기술 분야 인재 확보 시장에서는 검증된 코딩 테스트, 구조화된 면접, 기술 벤치마킹을 기존의 지원자 추적 시스템과 결합한 플랫폼에 대한 수요가 증가하고 있습니다.

후보자 분석과 관련된 데이터 개인정보 보호 문제

후보자 분석의 유용성은 높아지고 있지만, 여러 채용 시스템에 걸친 거버넌스를 확보하는 것은 점점 더 어려워지고 있습니다. AI 도구가 채용 전형 및 평가 과정에서 더 큰 역할을 담당하게 됨에 따라, 고용주들은 의사 결정에 대한 설명, 심사 절차 관리, 그리고 지원자 대응의 투명성 확보에 대한 압박을 더욱 강하게 느끼고 있습니다. 2026년 조사 결과에 따르면, AI는 현재 고용주와 구직자 모두에 의해 일상적으로 활용되고 있으며, 자동화된 상호작용의 양이 증가함에 따라 이러한 시스템 운영에 대한 신뢰의 중요성이 부각되고 있습니다. 실무상의 과제는 후보자 데이터가 지원자 추적 시스템, CRM 도구, 면접용 소프트웨어, 분석 레이어 등을 동시에 거치는 경우가 많아 거버넌스가 제대로 작동하지 않을 위험이 높아진다는 점에 있습니다. 이로 인해 IT 및 기술 분야 인재 확보 시장 프로세스 중 일부가 지연되고 있습니다. 이는 구매 담당자들이 여러 시스템에 걸쳐 수동으로 모니터링해야 하는 단일 솔루션보다는 내장된 통제 기능과 감사 가능한 워크플로를 갖춘 공급업체를 점점 더 선호하고 있기 때문입니다.

부문별 분석

2025년에는 소프트웨어 솔루션이 매출의 72.84%를 차지했으며, IT 및 기술 분야 인재 확보 시장에서 가장 큰 비중을 차지했습니다. ATS 플랫폼, 후보자 관계 관리 도구, 면접 솔루션 및 평가 기술은 방대한 업무 흐름을 체계화하고 수동 심사를 줄여주기 때문에 기업 기술 분야의 채용 과정에서 여전히 핵심적인 인프라로 자리 잡고 있습니다. 고용주들이 AI, 머신러닝, 코딩 기술을 그 어느 때보다 엄격하게 검증하려 함에 따라, 소프트웨어 분야 수요는 기술 평가 및 면접 도구로 이동하고 있습니다. 2026년 4월 기준으로, 미국 기술 관련 채용 공고의 71%에서 AI 기술이 필수 요건으로 제시되고 있어, 보다 전문적인 선발 및 평가 도구의 필요성이 부각되고 있습니다.

이러한 변화는 제품 수요에도 영향을 미치고 있으며, 7,500문제 이상의 검증된 문제와 93%의 정확도를 자랑하는 AI 기반 표절 감지 기능을 갖춘 엔터프라이즈 제품군이 출시되고 있습니다. 한 도입 사례에서 구조화된 기술 평가를 통해 선별 과정의 오감지율이 10%에서 4%로 감소했습니다. 이는 구매자가 범용적인 필터링에만 의존하기보다는 기술 검증을 위해 더 많은 비용을 지불하는 것을 마다하지 않는 이유를 여실히 보여줍니다. 서비스 시장은 2026-2031년 연평균 성장률(CAGR) 12.46%로 확대될 것으로 예상되며, 이는 고용주들이 도입, 관리형 채용 지원, AI 워크플로우 거버넌스를 외부에 위탁함에 따라 IT 및 기술 분야 인재 확보 시장이 이 부문에서 더욱 빠르게 성장하고 있음을 보여줍니다. 많은 조직이 AI를 활용한 채용 시스템을 원하고 있는 반면, 이를 대규모로 도입·감시·개선할 수 있는 사내 전문 지식을 갖춘 조직은 훨씬 적기 때문에 서비스 계층의 중요성은 점점 더 커지고 있습니다.

2025년에는 클라우드 도입이 매출의 71.12%를 차지했으며, IT 및 기술 분야 인재 확보 시장에서 가장 큰 점유율을 기록했습니다. 클라우드는 신속한 도입, 구독형 가격 정책, 그리고 보다 광범위한 HCM 환경과의 손쉬운 통합을 지원하기 때문에 대기업 및 중견 기업의 구매자들에게 표준 아키텍처로 자리 잡았습니다. 주요 플랫폼 공급업체들은 클라우드 서비스 제공에 주력하고 있으며, 이로 인해 클라우드의 위상은 현대 채용 시스템에서 표준적인 구매 경로로서 더욱 공고해지고 있습니다. 신제품 출시, AI 기능, 워크플로우 업그레이드의 대부분이 기존 도입 환경이 아닌 클라우드 환경을 통해 먼저 제공되기 때문에 클라우드는 지속적인 우위를 유지하고 있습니다.

하이브리드 방식은 2026-2031년 연평균 성장률(CAGR) 13.92%로 확대될 것으로 예상되며, IT 및 기술 분야 인재 확보 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. 이러한 성장을 뒷받침하고 있는 것은 클라우드 수준의 성능을 요구하면서도 후보자 데이터의 저장 및 처리 장소에 대해 보다 강력한 관리가 필요한 규제 대상 분야의 고용주들입니다. 따라서 완전한 클라우드 전환이 반드시 허용되지 않는 금융 서비스, 국방, 공공 부문의 도입 환경에서 하이브리드 모델은 특히 중요해집니다. 온프레미스 배포는 주요 도입 방식으로서의 위상을 서서히 잃어가고 있지만, 레거시 환경이나 보다 현대적인 아키텍처로 단계적으로 전환하고 있는 조직에서는 여전히 중요한 역할을 수행하고 있습니다.

지역별 분석

2025년, 북미는 매출의 39.42%를 차지했으며, IT 및 기술 분야 인재 확보 시장에서 가장 큰 점유율을 기록했습니다. 이 지역은 기술 분야 고용주가 밀집해 있고, 지원자 추적 시스템을 성숙하게 활용하며, 채용 워크플로우에 AI를 조기에 도입했다는 등의 장점을 갖추고 있습니다. 2026년 2분기 미국 기술·IT 분야의 순고용 전망치는 41%로, 2026년 1분기 대비 8포인트 상승했습니다. 이는 인력 조정 기간을 거치면서 채용에 대한 자신감이 높아지고 있음을 보여줍니다. 또한, 고용주들이 니어쇼어 채용 모델을 확대하고 엔지니어 인력에 대한 보다 유연한 접근 방안을 모색하는 가운데, 캐나다와 멕시코도 이 지역 수요를 뒷받침하고 있습니다. 유럽은 인력 부족이 심각하고, AI를 활용한 채용과 관련된 규정 준수 요구가 높아지고 있어 여전히 중요한 시장으로 남아 있습니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 15.12%로 확대될 것으로 예상되며, IT 및 기술 분야 인재 확보 시장에서 가장 빠르게 성장하는 지역 부문이 될 전망입니다. 이러한 성장은 스타트업 설립, 기업의 디지털화, 그리고 주요 경제권 전반에 걸친 AI 및 첨단 소프트웨어 관련 직종의 지속적인 인력 부족에 힘입어 이루어지고 있습니다. 이 지역은 대상 노동력 기반이 넓다는 장점도 누리고 있지만, 고용주들은 여전히, 특히 AI 및 클라우드 관련 직종에서 전문 인재 확보를 둘러싼 치열한 경쟁에 직면해 있습니다. 2026년 싱가포르에서 시행된 인재 정책의 변경은 세계 최고 수준의 국제 인재 확보를 개선하는 것을 목적으로 하며, 지역 전체의 채용 활동을 뒷받침하는 동시에 국경을 넘어 사업을 전개하는 고용주들에게 채용 플랫폼의 가치를 한층 더 높여주고 있습니다.

남미는 여전히 북미, 유럽, 아시아태평양보다 규모는 작지만, 다국적 기업들이 비용 경쟁력이 있는 기술 인력의 채용을 확대함에 따라 수요가 점차 개선되고 있습니다. 브라질과 아르헨티나가 이 지역의 주요 거점으로 자리 잡고 있으며, 이 지역의 성장은 클라우드 도입 및 세계 역량 센터 구축과 점점 더 밀접하게 연관되어 있습니다. 중동은 여전히 신흥 시장이며, 사우디아라비아와 아랍에미리트가 디지털 경제 프로그램 및 기술 허브 개발을 통해 수요를 뒷받침하고 있습니다. 아프리카는 여전히 초기 단계 시장이지만, 나이로비, 라고스, 케이프타운 등의 도시에서 진행되는 채용 활동은 다국어 및 국경을 초월한 채용 워크플로우를 지원할 수 있는 플랫폼에 장기적인 기회를 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the talent acquisition in IT and technology market was valued at USD 3.1 billion in 2025 and is estimated to grow from USD 3.44 billion in 2026 to USD 6.05 billion by 2031, at a CAGR of 11.95% during the forecast period (2026-2031).

This report is Segmented by Component (Software Solutions, [applicant Tracking System (ATS), Candidate Relationship Management (CRM), Recruitment Marketing Suite, and More], and Services), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Talent Acquisition In IT And Technology Market Trends and Insights

Intensifying Skills Shortage in Emerging Technologies

Digital investment is still expanding the number of technical roles employers need to fill, which is supporting steady demand in the IT and technology talent acquisition market. U.S. tech employment was projected to grow by 1.9% in 2026, adding nearly 128,000 roles and reinforcing the hiring burden on employers competing for scarce technical skills. This hiring need is becoming more selective because employers now want candidates with AI, cloud, data, and security capabilities that are harder to validate through simple resume filters. As a result, the talent acquisition in IT and the technology market is benefiting from stronger demand for precision sourcing, technical assessment, and structured screening workflows rather than broad application intake alone. The spending cycle behind digital transformation is therefore acting as a leading signal for platform investment, especially where technology hiring volumes are rising faster than internal recruiting capacity.

Accelerating Digital Transformation Among Tech Employers

A sharper shortage of emerging technology skills is also driving talent acquisition in IT and technology market. Seventy-two percent of organizations had difficulty filling open roles in 2026, and AI model development and AI literacy moved ahead of traditional engineering skills as the hardest capabilities to source for the first time in the survey's history. AI skill requirements appeared in 71% of U.S. tech job postings by April 2026, up from less than 10% in 2023, which shows how quickly employer demand has shifted. This change underscores the importance of assessment-led hiring, as technical ability in AI and machine learning cannot be reliably screened through keyword searches alone. That is lifting demand in the IT and technology talent acquisition market for platforms that combine validated coding tests, structured interviews, and skill benchmarking with traditional applicant tracking.

Data Privacy Concerns in Candidate Analytics

Candidate analytics is becoming more useful, but it is also becoming harder to govern across multiple hiring systems. As AI tools take on a larger role in screening and evaluation, employers face greater pressure to explain decisions, maintain review controls, and make candidate handling more transparent. Findings in 2026 also show that AI is now used regularly by both employers and candidates, increasing the volume of automated interactions and underscoring the importance of confidence in how those systems operate. The practical challenge is that candidate data often flows through applicant tracking systems, CRM tools, interview software, and analytics layers simultaneously, creating more points where governance can break down. This slows parts of the talent acquisition in IT and technology market because buyers increasingly prefer vendors with built-in controls and auditable workflows over point solutions that require manual oversight across several systems.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Adoption of AI-Powered Recruitment Automation

- Rising Preference for Remote and Hybrid Work Models

- Volatility in Venture Capital Funding Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software solutions accounted for 72.84% of revenue in 2025, making them the largest component of the IT and technology talent acquisition market. ATS platforms, candidate relationship management tools, interview suites, and assessment technologies remain the core infrastructure for enterprise technology hiring because they organize high-volume workflows and reduce manual screening. Demand in software is shifting toward technical assessment and interview tools as employers seek to validate AI, machine learning, and coding skills with greater rigor. By April 2026, AI skills were required in 71% of U.S. tech job postings, underscoring the need for more specialized screening and evaluation tools.

This shift is affecting product demand, with an enterprise suite that includes more than 7,500 validated questions and AI-powered plagiarism detection with 93% accuracy. In one deployment, a structured technical assessment reduced false-positive screening flags from 10% to 4%, underscoring why buyers are willing to pay more for skill validation than to rely solely on generic filtering. Services are projected to expand at a 12.46% CAGR from 2026 to 2031, indicating that this part of talent acquisition in IT and technology market is growing faster as employers outsource implementation, managed recruiting support, and AI workflow governance. The service layer is becoming increasingly important because many organizations want AI-enabled recruiting systems, but far fewer have the internal expertise to implement, monitor, and refine them at scale.

Cloud deployment accounted for 71.12% of revenue in 2025, giving it the largest share of the talent acquisition market in IT and technology. Cloud has become the default architecture for enterprise and mid-market buyers because it supports faster deployment, subscription pricing, and easier integration with broader HCM environments. The largest platform vendors are focused on cloud delivery, further reinforcing cloud as the standard buying path for modern recruiting systems. This gives cloud a durable lead because most new product releases, AI features, and workflow upgrades are arriving first through cloud environments rather than legacy installations.

Hybrid deployment is projected to expand at a 13.92% CAGR from 2026 to 2031, making it the fastest-growing configuration in the IT and technology talent acquisition market. Growth is being supported by employers in regulated sectors that want cloud-scale performance but still need stronger control over where candidate data is stored or processed. That makes hybrid models especially relevant for financial services, defense, and public sector hiring environments where full cloud migration is not always acceptable. On-premises deployment continues to lose ground as a primary mode, but it still matters in legacy environments and for organizations gradually moving toward more modern recruiting architectures.

Complete Report Scope:

- By Component

- Software Solutions

- Applicant Tracking System (ATS)

- Candidate Relationship Management (CRM)

- Recruitment Marketing Suite

- Interview and Assessment Tools

- Onboarding Solutions

- Services

- Software Solutions

- By Deployment Mode

- On-Premises

- Cloud

- By Enteprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America accounted for 39.42% of revenue in 2025, giving the region the largest share of the IT and technology talent acquisition market. The region benefits from a dense concentration of technology employers, mature use of applicant tracking systems, and earlier deployment of AI in hiring workflows. A 41% U.S. tech and IT Net Employment Outlook for Q2 2026, up 8 points from Q1 2026, signals stronger hiring confidence after a period of workforce adjustment. Canada and Mexico are also supporting regional demand as employers expand nearshore hiring models and search for more flexible access to engineering talent. Europe remains an important market because shortages are severe and compliance expectations around AI-led hiring are rising.

Asia-Pacific is projected to expand at a 15.12% CAGR from 2026 to 2031, making it the fastest-growing regional segment in talent acquisition for the IT and technology market. Growth is being supported by start-up formation, enterprise digitization, and continuing shortages in AI and advanced software roles across major economies. The region also benefits from a large addressable workforce base, but employers still face strong competition for specialized talent, especially in AI and cloud roles. Talent policy changes in Singapore in 2026 were designed to improve access to top international talent, supporting broader regional hiring activity and making recruiting platforms more valuable to employers operating across borders.

South America remains smaller than North America, Europe, and the Asia-Pacific, but demand is improving as multinational employers expand hiring for cost-competitive technology talent. Brazil and Argentina are the main regional centers, and growth is tied increasingly to cloud adoption and the buildout of global capability centers. The Middle East is still an emerging market, with Saudi Arabia and the United Arab Emirates supporting demand through digital economy programs and technology hub development. Africa remains an early-stage market, though hiring activity in cities such as Nairobi, Lagos, and Cape Town is creating a longer-term opportunity for platforms that can support multilingual and cross-border recruiting workflows.

- Adecco Group AG

- Randstad N.V.

- ManpowerGroup Inc.

- Korn Ferry

- Hays plc

- Allegis Group Holdings Inc.

- Robert Half International Inc.

- Insight Global LLC

- Alexander Mann Solutions Ltd.

- GlobalLogic Inc.

- Infosys BPM Ltd.

- Wipro Ltd.

- TCS iON (Tata Consultancy Services Ltd.)

- SAP SE

- Workday Inc.

- Oracle Corporation

- iCIMS Inc.

- Lever Inc.

- HackerRank Inc.

- SmartRecruiters Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Digital Transformation Among Tech Employers

- 4.2.2 Intensifying Skills Shortage in Emerging Technologies

- 4.2.3 Mainstream Adoption of AI-Powered Recruitment Automation

- 4.2.4 Rising Preference for Remote and Hybrid Work Models

- 4.2.5 Expansion of Venture-Backed Tech Start-ups in Asia-Pacific

- 4.2.6 Increasing Compliance Requirements for Tech Hiring

- 4.3 Market Restraints

- 4.3.1 Data Privacy Concerns in Candidate Analytics

- 4.3.2 Volatility in Venture Capital Funding Cycles

- 4.3.3 High Switching Costs for Enterprise ATS Platforms

- 4.3.4 Fragmented Global Tech-Talent Regulations

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Intensity of Competitive Rivalry

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Threat of New Entrants

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Solutions

- 5.1.1.1 Applicant Tracking System (ATS)

- 5.1.1.2 Candidate Relationship Management (CRM)

- 5.1.1.3 Recruitment Marketing Suite

- 5.1.1.4 Interview and Assessment Tools

- 5.1.1.5 Onboarding Solutions

- 5.1.2 Services

- 5.1.1 Software Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By Enteprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Netherlands

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adecco Group AG

- 6.4.2 Randstad N.V.

- 6.4.3 ManpowerGroup Inc.

- 6.4.4 Korn Ferry

- 6.4.5 Hays plc

- 6.4.6 Allegis Group Holdings Inc.

- 6.4.7 Robert Half International Inc.

- 6.4.8 Insight Global LLC

- 6.4.9 Alexander Mann Solutions Ltd.

- 6.4.10 GlobalLogic Inc.

- 6.4.11 Infosys BPM Ltd.

- 6.4.12 Wipro Ltd.

- 6.4.13 TCS iON (Tata Consultancy Services Ltd.)

- 6.4.14 SAP SE

- 6.4.15 Workday Inc.

- 6.4.16 Oracle Corporation

- 6.4.17 iCIMS Inc.

- 6.4.18 Lever Inc.

- 6.4.19 HackerRank Inc.

- 6.4.20 SmartRecruiters Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment