|

시장보고서

상품코드

2072650

미국의 비알코올성 지방간염(NASH) 바이오마커 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Non-alcoholic Steatohepatitis (NASH) Biomarkers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

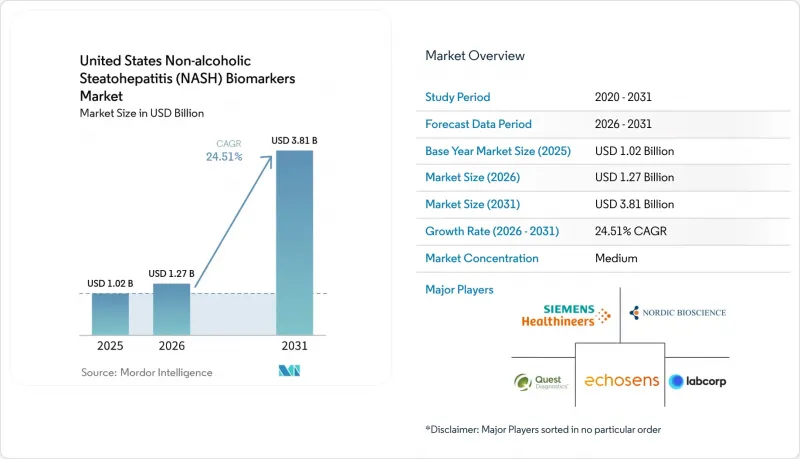

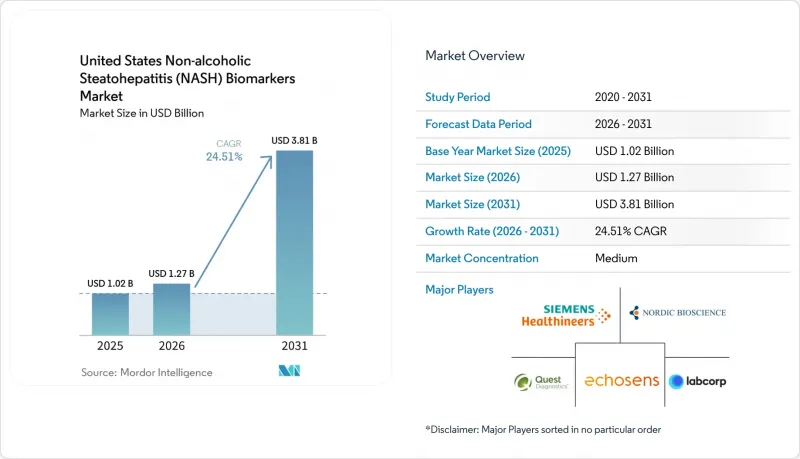

Mordor Intelligence에 의하면, 미국의 비알코올성 지방간염(NASH) 바이오마커 시장 규모는 2025년에 10억 2,000만 달러로 평가되었고, 2026년에는 12억 7,000만 달러로 추정되고, 2031년까지 38억 1,000만 달러에 이를 것으로 전망되며, 2026-2031년 CAGR 24.51%를 나타낼 것으로 예측됩니다.

본 보고서는 바이오마커 유형별(직접 섬유화 바이오마커, 간세포 손상 및 아포토시스 바이오마커, 대사 바이오마커 등), 용도별(임상 진단 및 병기 분류, 선별 검사 및 2차 위험도 계층화 등), 최종 사용자별(제약 업계 및 CRO 업계, 병원 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 비알코올성 지방간염(NASH) 바이오마커 시장 동향 및 인사이트

MASH 치료와 관련된 섬유화 검사 수요 증가

2024년 3월 FDA가 레스메틸롬을 승인함에 따라, 비간경변성 MASH 및 중등도에서 진행성 섬유증을 가진 환자를 대상으로 한 최초의 명확한 치료 연계형 검사 경로가 확립되었습니다. 생검에 대한 보편적인 요건이 없는 상태에서 실제 임상 현장에서 처방이 시작됨에 따라, 미국의 NASH 바이오마커 시장에서는 혈액 검사 및 영상 검사가 치료 적격성을 판단하는 실질적인 기준이 되었습니다. 이러한 변화가 중요한 이유는 검사가 주로 전문의의 정밀 검사나 임상시험에 국한되지 않고, 치료법 결정이 바이오마커 수요를 직접 견인하게 되었기 때문입니다. 추가적인 MASH 치료법이 상용화에 가까워짐에 따라, 승인될 때마다 비침습적 병기 분류 및 정기적인 재평가가 필요한 환자군이 확대될 것입니다. 이로 인해 미국 내 NASH 바이오마커 시장의 성장은 누적적인 양상을 띠게 될 것입니다. 왜냐하면 새로운 치료법이 추가될 때마다 진단, 치료 접근성, 그리고 사후 관리의 각 단계에서 검사 수요가 더욱 증가하기 때문입니다.

지침에 따른 비침습적 분류 절차

2025년 1월 AASLD 지침에서는 진행성 섬유화 평가에 있어 FIB-4를 1차 선택 혈액 검사로 규정하고, ELF를 단계적 지표로 사용하도록 정함으로써, 임상의들은 체계적인 선별 진단을 수행하기 위한 전국적인 틀을 확보하게 되었습니다. 해당 지침에서는 FIB-4의 기준치가 개정되었으며, 진행성 섬유증 양성 판정 시 풀 특이도가 0.94인 것으로 보고되어, 이는 1차 진료, 내분비학, 소화기내과 분야에서 더 광범위하게 활용되는 데 기여할 것으로 보입니다. 또한, AASLD는 섬유증의 시간 경과에 따른 진행 상황을 추적하기 위해 혈액 검사 마커를 사용하는 것에 반대하는 입장을 보이고 있으며, 이로 인해 미국 NASH 바이오마커 시장의 모니터링 분야에서 영상 진단 플랫폼이 성장할 여지가 남아 있습니다. EASL-EASD-EASO 2024년 지침은 FIB-4에 기반한 다단계 진단 경로(그 후 탄성영상 검사를 실시)를 통해 이러한 방향성을 재확인하는 한편, 고위험 MASH를 식별하기 위한 NIS2+의 유용성도 인정했습니다. 이러한 문서들은 종합적으로 대규모 의료 시스템 내 진단 경로의 불확실성을 완화하고, 검사 패널의 구성이나 플랫폼 간 경쟁 환경이 끊임없이 변화하는 상황에서도 검사 건수의 안정성을 높이고 있습니다.

독자적 패널에 대한 보험 보상금의 불균형

미국의 NASH 바이오마커 시장에서 다수의 독자적으로 개발된 바이오마커 패널의 경우, 상업적 성장세가 보험 급여 승인 속도를 앞지르고 있습니다. 테네시주의 블루크로스 블루쉴드는 몇 가지 간 섬유화 검사 패널을 보험 적용 대상에서 제외하고 있는 반면, CMS는 FIB-4 및 영상 탄성영상 검사 결과가 불확실한 경우에만 적용을 제한하는 MolDX 프레임워크를 제안했습니다. 2026년, CMS는 NASHnext를 위한 초기 가격 책정 체계를 수립했으나, GENFIT사는 이 조치를 완전한 상환 체계의 확립이라기보다는 초기 단계의 이정표라고 설명했습니다. 또한, 새롭게 등장한 분자 검사나 단백질체학 검사 역시 규모를 확대하기 전에 CLIA 및 MolDX의 기술 평가 요건을 충족해야 하므로, 분석 성능이 유망하더라도 도입이 지연되는 요인이 되고 있습니다. 따라서 개발 기업 입장에서는 수요 전망은 서 있지만, 수익 실현은 고르지 못한 상황이며, 특히 보험사가 자체 패널 검토에 앞서 여전히 보다 단순한 1차 치료 경로를 우선시하는 경우에는 이러한 경향이 두드러집니다.

부문별 분석

2025년, 미국의 NASH 바이오마커 시장 규모 중 직접적인 섬유화 바이오마커가 33.31%를 차지했습니다. 이는 전문의에 의한 검사, 위험도 계층화 및 임상시험 선별 과정에서 이러한 바이오마커들이 확립된 역할을 수행하고 있음을 반영합니다. 이러한 우위는 FIB-4, ELF, PRO-C3 및 이미 간내과 진료와 임상시험 설계에 정착된 독자적인 복합 패널에 대한 임상 현장의 폭넓은 인지도에 기반을 두고 있습니다. AASLD 및 EASL의 지침도 이러한 입장을 지지하고 있습니다. 왜냐하면 두 프레임워크 모두에서 섬유화를 평가하는 도구가 환자 진료 과정의 초기 단계에 위치해 있어, 이에 따라 의뢰 및 치료 결정에 밀접하게 관여하고 있기 때문입니다. 지멘스 헬스인이어스는 Atellica IM 및 ADVIA Centaur 시스템에서 ELF의 자동화를 실현함으로써 이 분야를 강화했으며, 로슈는 cobas에서 Elecsys PRO-C3를 출시함으로써 일상 검사에서의 확장성을 높였습니다. CK-18이나 M30과 같은 간세포 손상 및 세포사멸 마커는 탐색적 연구나 CRO 현장에서는 여전히 중요하지만, 미국의 NASH 바이오마커 업계에서 이러한 마커를 활용한 일상적인 임상 경로는 섬유화에 초점을 맞춘 검사에 비해 아직 충분히 확립되지 않았습니다.

대사 및 리포믹스 바이오마커 시장은 2031년까지 연평균 성장률(CAGR) 26.38%로 확대될 것으로 예상되며, 이에 따라 미국 NASH 바이오마커 시장에서 가장 빠르게 성장하는 부문으로 자리매김하고 있습니다. OWLiver 및 관련 지질 기반 접근법은 지질 프로파일링과 대사 변수를 결합함으로써, 고위험군 MASH를 임상적으로 유용한 정확도로 식별할 수 있음이 입증되었으며, 이로 인해 업스트림 단계에서의 사례 발견에 있어 그 중요성이 더욱 부각되고 있습니다. 단백질체학 모델도 급속히 발전하고 있으며, 혈청 단백질 위험 점수 및 보다 광범위한 다중 단백질 시그니처가 섬유화의 각 단계에서 강력한 예측 성능을 보여주고 있습니다. 염증 마커와 유전체 패널은 여전히 농축 분석 및 치료 반응 예측 분야에서 더 널리 사용되고 있으며, 이러한 분야에서는 일상적인 보험 적용이 시작되기 전부터 이미 의뢰인들이 여러 분석 대상 물질을 포괄하는 분석의 심도를 중요시해 왔습니다. 영상 바이오마커는 미국 NASH 바이오마커 업계에서 여전히 규제의 영향을 가장 많이 받는 분야입니다. 이는 FibroScan VCTE 및 cT1과 관련된 FDA의 조치가 모니터링 도구와 혈액 검사 기반 패널 간의 경쟁 관계에 직접적인 영향을 미치기 때문입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the united states non-Alcoholic steatohepatitis (NASH) biomarkers market size is projected to be USD 1.02 billion in 2025, USD 1.27 billion in 2026, and reach USD 3.81 billion by 2031, growing at a CAGR of 24.51% from 2026 to 2031.

This report is Segmented by Biomarker Class (Direct Fibrosis Biomarkers, Hepatocyte Injury and Apoptosis Biomarkers, Metabolic Biomarkers, and More), Application (Clinical Diagnosis and Staging, Screening and Secondary Risk Stratification, and More), and End User (Pharmaceutical and CRO Industry, Hospitals and More). Market Forecasts are Provided in Terms of Value (USD).

United States Non-alcoholic Steatohepatitis (NASH) Biomarkers Market Trends and Insights

Rising MASH Therapy-Linked Fibrosis Testing Demand

The FDA approval of resmetirom in March 2024 created the first clear therapy-linked testing pathway for patients with non-cirrhotic MASH and moderate-to-advanced fibrosis. Because prescribing moved into real clinical practice without a universal biopsy requirement, blood-based and imaging-based tests became the practical gatekeepers for treatment eligibility in the United States NASH biomarkers market. That shift matters because a therapy decision now drives biomarker demand directly, rather than leaving testing tied mainly to specialist workups or clinical trials. As additional MASH therapies move closer to commercialization, each approval will widen the pool of patients needing non-invasive staging and repeat reassessment. This makes growth in the United States NASH biomarkers market cumulative, since every new treatment adds another layer of testing demand across diagnosis, access, and follow-up.

Guideline-Backed Non-Invasive Triage Pathways

The AASLD January 2025 guidance established FIB-4 as the preferred first-tier blood-based test for advanced fibrosis assessment, with ELF used as a sequential marker, which gave clinicians a national framework for structured triage. The same guidance stated revised FIB-4 thresholds and reported pooled specificity of 0.94 for ruling in advanced fibrosis, which supports broader use across primary care, endocrinology, and gastroenterology. AASLD also advised against using blood-based markers for tracking fibrosis progression over time, which leaves room for imaging platforms to expand within the monitoring portion of the United States NASH biomarkers market. The EASL-EASD-EASO 2024 guideline reinforced this direction through a multi-step pathway based on FIB-4, followed by elastography, and it also recognized NIS2+ for identifying at-risk MASH. Together, these documents reduce pathway ambiguity for large health systems and make testing volumes more durable even as the competitive mix of panels and platforms continues to change.

Uneven Payer Reimbursement For Proprietary Panels

Commercial momentum has outpaced reimbursement alignment for many proprietary biomarker panels in the United States NASH biomarkers market. Blue Cross Blue Shield of Tennessee has excluded several hepatic fibrosis panels from coverage, while CMS proposed a MolDX framework that limits coverage to settings where FIB-4 and imaging elastography are indeterminate. In 2026, CMS established an initial pricing framework for NASHnext, but GENFIT described that step as an early milestone rather than full reimbursement maturity. Emerging molecular and proteomic tests also face CLIA and MolDX technical assessment requirements before they can scale, which slows onboarding even when analytical performance is promising. This leaves developers with demand visibility but uneven revenue realization, especially when payer policy still favors simpler first-line pathways before proprietary panels are considered.

Other drivers and restraints analyzed in the detailed report include:

- Pharma And CRO Biomarker-Enrichment Spending

- Demand For Repeatable Biopsy-Sparing Monitoring

- Biopsy Still Anchors Some Confirmatory Decisions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct fibrosis biomarkers held 33.31% of the United States NASH biomarkers market size in 2025, which reflects their established role in specialist workups, risk stratification, and trial screening. This lead rests on the broad clinical familiarity of FIB-4, ELF, PRO-C3, and proprietary composite panels that are already embedded in hepatology practice and trial design. AASLD and EASL guidance supports that position because both frameworks place fibrosis-oriented tools early in the patient pathway, which keeps them close to referral and treatment decisions. Siemens Healthineers strengthened this class through automated ELF availability on Atellica IM and ADVIA Centaur systems, and Roche added routine lab scalability with the Elecsys PRO-C3 launch on cobas. Hepatocyte injury and apoptosis markers such as CK-18 and M30 remain relevant in exploratory and CRO settings, but their routine clinical pathway is still less established than fibrosis-focused tests in the United States NASH biomarkers industry.

Metabolic and lipidomic biomarkers are projected to expand at a 26.38% CAGR through 2031, which makes them the fastest-growing class within the United States NASH biomarkers market. OWLiver and related lipid-based approaches have shown clinically useful discrimination of at-risk MASH through combined lipid profiling and metabolic variables, which improves their relevance for upstream case finding. Proteomic models have also advanced quickly, with a serum protein risk score and broader multi-protein signatures posting strong validation performance across fibrosis stages. Inflammatory markers and genomic panels are still more common in enrichment and response-prediction work, where sponsors value multi-analyte depth even before routine reimbursement is available. Imaging biomarkers remain the most regulation-sensitive modality in the United States NASH biomarkers industry, because FDA movement on FibroScan VCTE and cT1 directly affects how monitoring tools compete with blood-based panels.

Complete Report Scope:

- By Biomarker Class

- Direct fibrosis biomarkers

- Hepatocyte injury and apoptosis biomarkers

- Metabolic and lipidomic biomarkers

- Inflammatory biomarkers

- Genomic and transcriptomic biomarkers

- Imaging biomarkers

- Others

- By Application

- Clinical diagnosis and staging

- Screening and secondary risk stratification

- Therapeutic monitoring and response assessment

- Other Applications

- By End User

- Pharmaceutical and CRO industry

- Hospitals and clinics

- Diagnostic laboratories and reference labs

- Other End Users

List of Companies Covered in this Report:

- BioPredictive

- CIMA Sciences

- DiaPharma Group

- Echosens

- Fibronostics

- Fujifilm Healthcare Americas

- GENFIT

- HistoIndex

- LabCorp

- Mayo Clinic Laboratories

- Nordic Bioscience

- PacificDx

- PathAI

- Perspectum

- Prometheus Laboratories

- Quest Diagnostics

- Roche

- Siemens Healthineers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising MASH therapy-linked fibrosis testing demand

- 4.2.2 Guideline-backed non-invasive triage pathways

- 4.2.3 Pharma and CRO biomarker-enrichment spending

- 4.2.4 Demand for repeatable biopsy-sparing monitoring

- 4.2.5 VA and IDN liver-pathway deployment

- 4.2.6 Automated assays and AI-assisted readouts

- 4.3 Market Restraints

- 4.3.1 Uneven payer reimbursement for proprietary panels

- 4.3.2 Biopsy still anchors some confirmatory decisions

- 4.3.3 Obesity-related elastography and discordance limits

- 4.3.4 NASH to MASH coding and terminology transition

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Biomarker Class

- 5.1.1 Direct fibrosis biomarkers

- 5.1.2 Hepatocyte injury and apoptosis biomarkers

- 5.1.3 Metabolic and lipidomic biomarkers

- 5.1.4 Inflammatory biomarkers

- 5.1.5 Genomic and transcriptomic biomarkers

- 5.1.6 Imaging biomarkers

- 5.1.7 Others

- 5.2 By Application

- 5.2.1 Clinical diagnosis and staging

- 5.2.2 Screening and secondary risk stratification

- 5.2.3 Therapeutic monitoring and response assessment

- 5.2.4 Other Applications

- 5.3 By End User

- 5.3.1 Pharmaceutical and CRO industry

- 5.3.2 Hospitals and clinics

- 5.3.3 Diagnostic laboratories and reference labs

- 5.3.4 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 BioPredictive

- 6.3.2 CIMA Sciences

- 6.3.3 DiaPharma Group

- 6.3.4 Echosens

- 6.3.5 Fibronostics

- 6.3.6 Fujifilm Healthcare Americas

- 6.3.7 GENFIT

- 6.3.8 HistoIndex

- 6.3.9 Labcorp

- 6.3.10 Mayo Clinic Laboratories

- 6.3.11 Nordic Bioscience

- 6.3.12 PacificDx

- 6.3.13 PathAI

- 6.3.14 Perspectum

- 6.3.15 Prometheus Laboratories

- 6.3.16 Quest Diagnostics

- 6.3.17 Roche Diagnostics

- 6.3.18 Siemens Healthineers

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment