|

시장보고서

상품코드

2072665

남미의 카톤 보드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

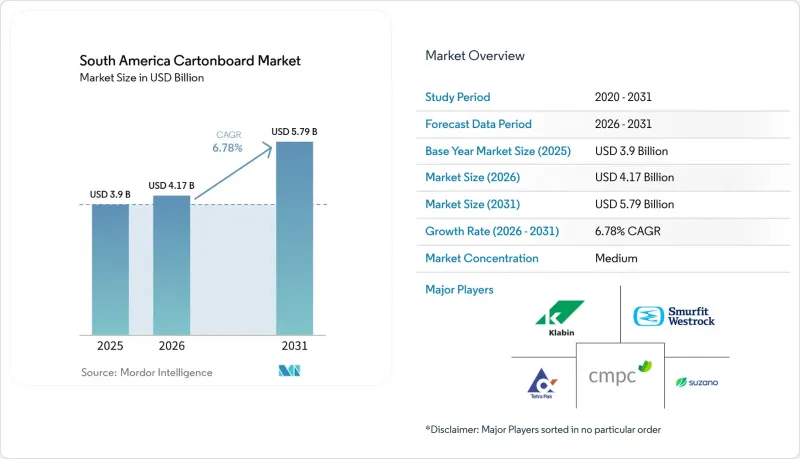

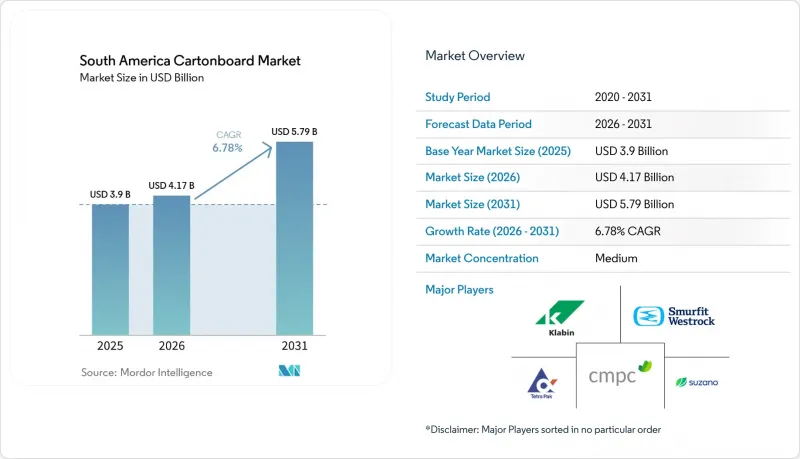

Mordor Intelligence에 의하면, 남미의 카톤 보드 시장 규모는 2025년 39억 달러로 평가되었고, 2026년에는 41억 7,000만 달러로 추정되고, 2026-2031년 CAGR 6.78%로 성장을 지속할 전망이며, 2031년에는 57억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 등급별(솔리드 표백 카톤 보드, 솔리드 미표백 카톤 보드, 접이식 상자용 카톤 보드 등), 포장 형태별(접이식 상자, 액체 포장, 슬리브 및 트레이 등), 최종 사용자 산업별(식품, 음료 등), 그리고 지역별(브라질, 아르헨티나, 콜롬비아, 칠레, 페루 및 기타 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

남미의 카톤 보드 시장 동향 및 분석

플라스틱 대체 의무화와 브랜드의 지속가능성 목표

규제로 인해 플라스틱 대체는 남미의 카톤 보드 시장 전반에서 브랜드의 자발적인 노력에서 규정 준수 과제로 전환되었습니다. 브라질의 제12,688호 정령은 플라스틱 포장을 위한 전국적인 역물류 시스템을 구축하고, 2026년까지 플라스틱 재활용률 32%를 의무화하며, 2040년까지 50%로 끌어올리는 로드맵을 마련했으며, 2026년부터 대기업에 대해 신규 플라스틱 포장재에 최소 22%의 재활용 소재를 포함하도록 의무화했으나, 종이 및 카톤 보드 포장은 명시적으로 적용 대상에서 제외되었습니다. 콜롬비아 법률 제2232호 및 결의안 제1407호, 칠레 법률 제21.368호, 그리고 페루의 재활용 가능·생분해성 식기 관련 규제안은 섬유계 소재 포장재와 규정 준수가 더 어려운 플라스틱 제품 간의 정책적 격차를 확대시켰습니다. 이러한 변화로 인해 브랜드 소유자는 규제 대상이 되는 개별 제품뿐만 아니라, 보다 광범위한 SKU 포트폴리오의 재설계를 요구받고 있습니다. 이는 지역의 포장 시스템과 조달 기준이 점점 더 포트폴리오 차원에서 관리되고 있기 때문입니다. 또한 이러한 추세는 외식 산업, 의료 관련 2차 포장, 브랜드 이미지 제고와 마찬가지로 재활용 가능성 주장이 중요시되는 특정 화장품 라인에서 카톤 보드 용기의 채택 확대를 촉진하고 있습니다. 남미의 카톤 보드 시장에 있어 이는 정책에 뒷받침된 수요의 하한선을 형성하여, 다른 많은 포장재에 비해 일시적인 소비 둔화의 영향을 덜 받게 하고 있습니다.

포장 식품 수요와 소매업의 현대화

가공식품에 대한 수요와 현대적인 소매업 형태의 꾸준한 확산에 힘입어, 남미의 카톤 보드 시장에서는 여전히 견고한 수요 기반이 유지되고 있습니다. Empapel의 보고서에 따르면, 2025년 카톤 보드 생산량은 75만 6,000톤에 달했으며, 생산 구성에서 식품 포장이 여전히 가장 큰 최종 용도 분야를 차지했습니다. 같은 소식통에 따르면, 2026년 1월 카톤 보드 출하량은 사상 최고치인 34만 7,000톤에 달했으며, 이는 예측 기간 초반부터 견조한 수주 추세를 시사하는 것이었습니다. 또한 ABRE의 보고서에 따르면, 2025년 브라질의 포장재 총 생산량은 0.3% 감소했으나, 식품 및 위생용품의 포장량은 대체로 안정적인 양상을 보였으며, 이는 생활필수품 포장 분야에서 카톤 보드가 수행하는 방어적 역할을 뒷받침하는 결과였습니다. 브라질을 제외한 페루, 콜롬비아, 칠레에서는 소매업의 체계화가 진행되고 있으며, 이에 따라 각 브랜드 제조업체들은 단순한 연포장재에서 벗어나, 매장에서의 존재감을 높이고 보다 명확한 브랜드 차별화를 가능하게 하는 인쇄된 카톤 보드 상자로의 전환을 촉진하고 있습니다. 이러한 구조로 인해 남미의 카톤 보드 시장은 여전히 생활 필수품 소비에 힘입어 성장하고 있는 한편, 고부가가치 그래픽이나 편의성이 높은 포장 형태, 그리고 더욱 정교한 사양이 요구되는 용도 분야에서 컨버터의 이익률 향상을 위한 여지도 남아 있습니다.

버진 펄프 및 재생 섬유의 원가 변동

원자재 비용의 변동은 남미의 카톤 보드 시장에서 생산자와 가공업체에게 여전히 가장 시급한 이익률 위협 요인으로 남아 있습니다. 이러한 압박은 순수 펄프의 가격에서만 비롯된 것은 아닙니다. 환율 변동에 따라, 많은 가공업체들이 여전히 필요로 하는 수입 카톤 보드, 화학약품, 특수 원자재의 현지 통화 기준 비용도 변동하기 때문입니다. 재생 섬유의 경우, 회수 품질이나 입수 가능성은 소비 패턴과 비공식 회수 시스템의 조직화 진행 속도에 좌우되기 때문에 불확실성이 더욱 커지고 있습니다. 비렐루드사는 2026년 1분기 중간 보고서에서 카톤 보드 품질 향상을 위한 투자를 지속하고 있음에도 불구하고 가격 측면에서 어려움을 겪고 있다고 밝혔습니다. 이는 공급 측의 자신감과 단기적인 가격 상황의 긴장이 공존할 수 있음을 보여줍니다. 마이어-멜른호프사 역시 2026년에 고정비 절감, 프로세스 통합, 구조 조정에 계속 중점을 두고 있으며, 이는 비용이 판매 가격보다 더 빠르게 변동할 수 있는 시장에서 규율 있는 대응이 필요함을 반영하고 있습니다. 이러한 원가 변동이 수입품의 공격적인 가격 책정과 겹치게 되면, 현지 제지 회사는 가격 결정력을 상실하고, 가공업체는 원가 전가 여지가 좁아지는 상황에 직면하게 됩니다.

부문별 분석

2025년, 남미의 카톤 보드 시장에서 접이식 카톤 보드 시트는 41.81%의 점유율을 차지했습니다. 한편, 남미의 카톤 보드 시장에서 무지 표백 카톤 보드 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 8.09%로 확대될 것으로 전망됩니다. 접이식 카톤 보드는 식품, 의약품 외부 포장 및 개인 위생 용품 포장 분야에서 인쇄 적합성, 강성, 비용 면에서 균형을 잘 갖추고 있어, 계속해서 주요 대량 판매 등급으로서의 입지를 유지했습니다. 또한, 브라질의 통합 제지 공장을 통해 현지 생산 등급의 원료를 공급할 수 있게 된 점도 그 위상을 강화하는 데 기여했습니다. 이를 통해 구매자는 전적으로 수입에 의존하는 조달 모델보다 리드타임과 운전자금을 보다 효과적으로 관리할 수 있게 되었습니다. 솔리드 표백 카톤 보드의 성장세가 더욱 가속화되고 있는 것은 의약품 및 화장품 포장 분야에서 더 높은 백색도, 선명한 인쇄 재현성, 그리고 홀로그래픽 가공, 엠보싱 가공, 위조 방지 가공과의 호환성이 점점 더 요구되고 있기 때문입니다. 비렐루드사의 '에볼루션 프로그램'에 따라 2024-2027년 14억 스웨덴 크로나(1억 2,880만 달러)를 투자하여 퀴네세크 공장과 에스카나바 공장의 솔리드 블리치드 보드 생산 설비를 업그레이드할 계획입니다. 이는 전 세계 공급업체들이 남미 지역의 솔리드 블리치드 보드에 대한 수요가 지속될 것으로 전망하고 있음을 보여줍니다.

화이트 라이닝 칩보드는 비용을 중시하는 식품 및 음료용 2차 포장 분야에서 계속해서 사용되고 있으며, 특히 재생 섬유의 경제성이 저비용 등급 구성을 가능하게 하는 분야에서 그 수요가 나타나고 있습니다. 무표백 솔리드 보드는 고급 그래픽이나 밝은 흰색 표면보다 구조적 강도가 요구되는 산업용 및 대량 생산 용도에서 여전히 중요한 역할을 하고 있습니다. 액체 포장용 카톤 보드와 푸드서비스용 카톤 보드는 단순히 카톤 보드공급 가능성뿐만 아니라, 차단 화학, 위생 기준 준수, 그리고 가공업체의 공정 관리에 좌우되기 때문에 남미의 카톤 보드 산업에서 가장 전문성이 높은 분야로 꼽히고 있습니다. 의약품 및 고급 식품 포장재에 대한 규정 준수 요건 또한 추적성 및 인쇄 성능에 대한 기준을 높이고 있으며, 이에 따라 더 높은 사양의 표백 카톤 보드 및 고급 접이식 용지 등급으로의 가치 전환이 서서히 진행되고 있습니다. 2026년 초 현재 예정보다 앞서 진행되고 있는 마이어-멜른호프사의 'Fit-For-Future' 프로그램은 유럽 공급업체들이 해당 지역의 중급 용도를 뒷받침하는 재생 카톤 보드 등급 분야에서 앞으로도 수출 경쟁력 향상을 목표로 삼을 것임을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the south america cartonboard market size is expected to grow from USD 3.9 billion in 2025 to USD 4.17 billion in 2026 and is forecast to reach USD 5.79 billion by 2031 at 6.78% CAGR over 2026-2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, and More), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Food, Beverage, and More), and Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

South America Cartonboard Market Trends and Insights

Plastic Substitution Mandates And Brand Sustainability Targets

Regulation has moved plastic substitution from a voluntary brand agenda into a compliance issue across the South America cartonboard market. Brazil's Decree 12,688 created a national reverse logistics system for plastic packaging, required a 32% plastic recycling rate in 2026, set a path to 50% by 2040, and imposed a minimum 22% recycled-content obligation in new plastic packaging from 2026 for larger companies, while paper and cardboard packaging remained explicitly exempt. Colombia's Law 2232, Resolution 1407, Chile's Ley 21.368, and Peru's draft recyclable and biodegradable tableware regulation widened the policy gap between fiber-based formats and harder-to-comply plastic items. That shift is pushing brand owners to redesign broader SKU portfolios rather than only the units directly covered by regulation, because regional packaging systems and procurement standards are increasingly managed at portfolio level. It also supports stronger carton adoption in foodservice, healthcare-adjacent secondary packaging, and selected beauty lines where recyclability claims now matter alongside brand presentation. For the South America cartonboard market, this creates a policy-backed demand floor that is less exposed to short consumer slowdowns than many other packaging materials.

Packaged Food Demand And Retail Modernization

Processed food demand and the steady spread of modern retail formats continue to give the South America cartonboard market a reliable volume base. Empapel reported 756,000 tonnes of paperboard production in 2025, and food packaging remained the single largest end-use area within that output mix. The same source showed that January 2026 carton shipments reached a record 347,000 tonnes, which signaled firm order flow at the start of the forecast period. ABRE also reported that Brazil's overall packaging production volume slipped 0.3% in 2025, yet food and hygiene packaging volumes remained broadly stable, which confirmed cartonboard's defensive role in essential-goods packaging. Outside Brazil, retail formalization in Peru, Colombia, and Chile is encouraging branded suppliers to move from simpler flexible formats toward printed cartons that improve shelf presence and support clearer brand differentiation. This mix keeps the South America cartonboard market tied to staple consumption while still leaving room for higher-value graphics, convenience formats, and stronger converter margins in better specified applications.

Virgin Pulp And Recovered Fiber Cost Volatility

Input cost volatility remains the most immediate margin threat for producers and converters in the South America cartonboard market. The pressure does not come only from virgin pulp pricing, because exchange-rate swings also change the local-currency cost of imported board, chemicals, and specialty inputs that many converters still need. Recovered fiber adds a second layer of uncertainty because collection quality and availability move with consumption patterns and with the speed at which informal recovery systems become more organized. Billerud described prices as challenged in its first-quarter 2026 interim report even while it continued to fund board upgrades, which shows how supply-side confidence can coexist with tight near-term pricing conditions. Mayr-Melnhof likewise kept its 2026 focus on fixed-cost reduction, process harmonization, and structural adjustments, which reflected the need for discipline in a market where costs can move faster than selling prices. When those cost swings meet aggressive imported offers, local mills lose pricing power and converters face narrower pass-through windows.

Other drivers and restraints analyzed in the detailed report include:

- Beverage And Dairy Carton Demand In Aseptic And Chilled Formats

- Pharmaceutical And Healthcare Packaging Demand With Traceability And Hygiene Needs

- Competition From Flexible Plastic And Lightweight Alternative Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard held 41.81% of the South America cartonboard market share in 2025, while the South America cartonboard market size for solid bleached board is projected to expand at 8.09% CAGR from 2026 to 2031. Folding boxboard remained the core volume grade because it balanced printability, stiffness, and cost across food, pharmaceutical outer-carton, and personal care packaging. Its position was also reinforced by the availability of locally produced grades from integrated Brazilian mills, which helped buyers manage lead time and working-capital needs more effectively than fully import-dependent sourcing models. Solid bleached board is rising faster because pharmaceutical and cosmetics packs increasingly require higher whiteness, cleaner print reproduction, and better compatibility with holographic, embossed, and anti-counterfeit finishing. Billerud's Evolution Program is allocating SEK 1.4 billion (USD 128.8 million) across 2024-2027 to upgrade its Quinnesec and Escanaba mills for solid bleached board production, which shows that global suppliers expect durable SBS demand in South America.

White-lined chipboard continues to serve cost-sensitive secondary packaging in food and beverage, especially where recycled fiber economics support a lower-cost grade mix. Solid unbleached board remains relevant in industrial and bulk uses that need structural strength more than premium graphics or bright white surfaces. Liquid packaging board and food service board sit at the most specialized end of the South America cartonboard industry because they depend on barrier chemistry, hygiene compliance, and converter process control rather than only board availability. Compliance needs in pharmaceutical and premium food packs are also raising the bar for traceability and print performance, which supports gradual value migration toward better specified bleached and premium folding grades. Mayr-Melnhof's Fit-For-Future program, which remained ahead of schedule in early 2026, suggests that European suppliers will keep targeting export competitiveness in recycled cartonboard grades that feed the region's mid-tier applications.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- By Geography

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

List of Companies Covered in this Report:

- Klabin S.A.

- Suzano S.A.

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Tetra Pak International S.A.

- SIG Group AG

- Empresas CMPC S.A.

- Mayr-Melnhof Karton AG

- Papeles y Cartones S.A.

- Cartones America S.A.

- Sonoco Products Company

- Ibema Companhia Brasileira de Papel

- BO Packaging S.A.

- Industrias VANNI S.A.

- PAPELERA DEL SUR S.A.

- CORRUGADORA NACIONAL CRANSA S.A.

- INPACO S.A.I.C.E.I.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Plastic Substitution in Food and Consumer Packaging

- 4.3.2 Aseptic Beverage Carton Demand in Dairy and Juice

- 4.3.3 Premiumization in Beauty, Personal Care, and Healthcare Cartons

- 4.3.4 Growth in Shelf-Ready and E-Commerce Folding Cartons

- 4.3.5 Foodservice Board Adoption for Delivery and Takeaway

- 4.3.6 Export-Oriented Certification and Traceability Needs

- 4.4 Market Restraints

- 4.4.1 Competition From Flexible Plastics in Barrier-Sensitive Uses

- 4.4.2 Volatility in Pulp, Energy, and Starch Costs

- 4.4.3 Low-Priced Asian Folding Board Imports

- 4.4.4 Liquid-Carton Recycling and EPR Friction

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Colombia

- 5.4.4 Chile

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Klabin S.A.

- 6.4.2 Suzano S.A.

- 6.4.3 Smurfit Westrock plc

- 6.4.4 Graphic Packaging International, LLC

- 6.4.5 Tetra Pak International S.A.

- 6.4.6 SIG Group AG

- 6.4.7 Empresas CMPC S.A.

- 6.4.8 Mayr-Melnhof Karton AG

- 6.4.9 Papeles y Cartones S.A.

- 6.4.10 Cartones America S.A.

- 6.4.11 Sonoco Products Company

- 6.4.12 Ibema Companhia Brasileira de Papel

- 6.4.13 BO Packaging S.A.

- 6.4.14 Industrias VANNI S.A.

- 6.4.15 PAPELERA DEL SUR S.A.

- 6.4.16 CORRUGADORA NACIONAL CRANSA S.A.

- 6.4.17 INPACO S.A.I.C.E.I.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment