|

시장보고서

상품코드

2072673

미국의 치과 진료 관리 소프트웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Dental Practice Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

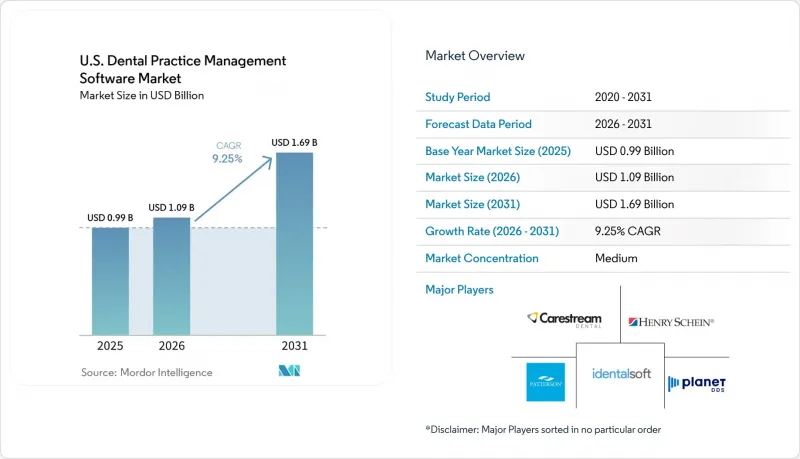

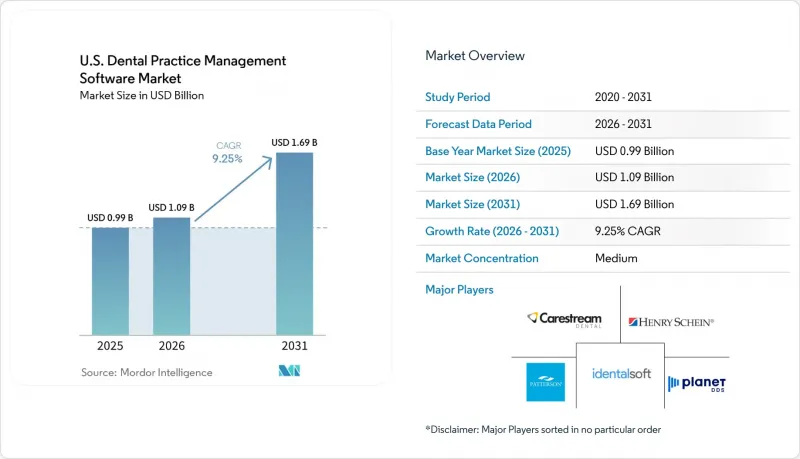

Mordor Intelligence에 의하면, 미국의 치과 진료 관리 소프트웨어 시장 규모는 2025년에 9억 9,000만 달러로 평가되었고, 2026년에 10억 9,000만 달러로 추정되고, 2031년까지 16억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 9.25%로 성장할 전망입니다.

본 보고서는 배포 모드별(웹 기반, 클라우드 기반, 온프레미스), 구독 모델별(영구 라이선스, SaaS), 용도별(커뮤니케이션, 일정 관리, 청구, 보험, 치료 계획, 영상 진단, 분석), 최종 사용자별(치과, 병원 및 전문 의료 센터, 학술 기관, 기타), 진료소 규모별(개인 개업, 소규모 그룹, 대규모 그룹, DSO)로 분류되고 있습니다. 시장 규모는 금액(달러)으로 표시되어 있습니다.

미국의 치과 진료 관리 소프트웨어 시장 동향 및 인사이트

서버 기반에서 브라우저 및 클라우드 플랫폼으로의 전환

기존 서버 환경에서 클라우드 기반 플랫폼으로의 전환은 미국 치과 진료 관리 소프트웨어 시장의 소프트웨어 구매 방식을 변화시키고 있습니다. 최신 클라우드 PMS 인프라를 도입한 조직에서는 IT 지원 티켓이 40-55% 감소하고, 주당 시스템 가동 중단 시간이 1시간 단축되었으며, 중대한 IT 사고가 83% 감소한 것으로 보고되었습니다. 구식 서버 환경에서는 시스템 간 연동 부족, 하드웨어 노후화, IT 환경의 비일관성으로 인해 치과 기관은 연간 수익의 8-12%에 해당하는 비용을 부담하게 됩니다. 클라우드 공급업체는 특히 통합 운영이 필요한 다중 거점 그룹에서 업데이트 간소화, 워크플로우 표준화, 기술 의존도 저감을 통해 지지를 넓혀가고 있습니다.

DSO의 표준화와 다중 거점 플랫폼의 가시성

DSO의 표준화에 따라, 미국의 치과 진료 관리 소프트웨어 시장에서는 반복적인 전환이 진행되고 있습니다. 데이터에 따르면, DSO에 소속된 치과의사의 29%가 2026년에 새로운 소프트웨어에 투자할 계획인 반면, DSO에 소속되지 않은 치과의사의 경우 16.3%에 그치고 있습니다. Planet DDS는 2025년까지 14,500개의 치과를 지원했으며, Sage Dental, Coast Dental, Altius Dental, Choice Healthcare와의 제휴를 통해 100곳 이상의 DSO에서 입지를 확대했습니다. 권장 플랫폼을 통해 DSO는 업무를 통합하고, 회수 현황, 이용 현황 및 의료 제공업체의 성과에 대한 통합된 관점을 제공할 수 있으므로, 엔터프라이즈 벤더에게 집중적인 성장 경로가 열리고 있습니다.

데이터 개인정보 보호, HIPAA 및 접근 권한과 관련된 규정 준수 비용

데이터 개인정보 보호 및 규정 준수 비용은 미국 치과 진료 관리 소프트웨어 시장에서 계속해서 도입의 큰 장벽으로 작용하고 있으며, 특히 전담 IT 팀이나 규정 준수 팀을 갖추지 못한 개인 개업의나 소규모 그룹 진료소의 경우 더욱 그러합니다. 구식 시스템의 경우, 기밀성이 높은 환자 데이터나 청구 데이터를 안전하게 처리하기 위해 암호화, 접근 제어, 감사 로그, 워크플로우 조정 등에 대한 추가 투자가 필요한 경우가 적지 않습니다. 대규모 DSO는 이러한 비용을 여러 거점에 분산시킬 수 있지만, 독립된 진료소는 제한된 수익 기반 내에서 이러한 비용을 부담해야 합니다. 의료 데이터 유출 1건당 평균 손해액은 1,093만 달러에 달하며, 사이버 보안은 치과 기관에 있어 최우선 과제가 되고 있습니다. 규제 준수 압박으로 인해 장기적인 시스템 업데이트 수요는 증가하고 있지만, 예산이 제한적인 진료소에서는 단기적인 구매가 미뤄지고 있습니다.

부문별 분석

2025년, 미국의 치과 진료 관리 소프트웨어 시장에서 온프레미스형 시스템은 43.65%를 차지했습니다. 이는 서버 아키텍처에 대한 미래 수요라기보다는 이미 확고히 자리 잡은 그 존재감을 반영한 것입니다. 클라우드 도입은 2031년까지 연평균 성장률(CAGR) 11.95%를 기록하며 성장할 것으로 예상되며, 시장 전체를 웃도는 속도로 확대될 전망입니다. 치과 병원이나 DSO(치과 진료소 운영 조직)는 서버 유지보수 부담 경감, 원격 접속 간소화, 워크플로우 통합 등의 이유로 클라우드 모델을 선호하고 있습니다. 클라우드 기반 PMS 환경을 도입한 조직에서는 IT 사고의 감소가 보고되고 있으며, 이로 인해 전환에 따른 운영상의 이점이 입증되고 있습니다.

온프레미스형 시스템은 점차 감소할 전망이지만, 기업 도입 측면에서는 도입 프로세스의 효율화와 일관된 워크플로우 구현 덕분에 클라우드 솔루션이 점점 더 선호되고 있습니다. 2025년에는 Sage Dental(140개 지점)과 Coast Dental(88개 지점) 같은 대기업들의 진출로 인해 클라우드 전환의 규모가 얼마나 큰지 여실히 드러났습니다. 구매자가 완전한 클라우드 플랫폼으로의 전환을 결정하거나 기존 시스템을 유지하기로 선택함에 따라, 웹 기반 시스템이 차지하는 중간 시장 점유율은 줄어들고 있습니다. 예측 기간 동안 시스템 업데이트 주기와 가동 시간 확보에 대한 요구가 '클라우드 퍼스트' 플랫폼에 대한 수요를 견인할 것으로 보입니다.

미국의 치과 진료 관리 소프트웨어 시장에서 2025년 매출의 59.76%를 구독 및 SaaS 모델이 차지할 것으로 예상되며, 2031년까지 연평균 성장률(CAGR)은 10.25%를 나타낼 것으로 전망됩니다. 각 공급업체들은 현재 Henry Schein One이 2026년에 출시할 예정인 'Dentrix Ascend' 패키지에서 볼 수 있듯이, 업데이트, 분석 기능, AI 도구를 정기 구독 요금제에 포함하고 있습니다. 구독 요금제는 진료소 입장에서는 초기 비용을 절감해 주는 동시에, 공급업체 입장에서는 시간이 지남에 따라 추가 기능을 단계적으로 제공함으로써 계약 기간 전체에 걸친 수익 가치를 높여줍니다. 또한, SaaS 모델은 업데이트와 새로운 기능을 안정적으로 제공할 수 있게 해주기 때문에 주요 수익 모델로 자리 잡고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the u.S. dental practice management software market size is projected to be USD 0.99 billion in 2025, USD 1.09 billion in 2026, and reach USD 1.69 billion by 2031, growing at a CAGR of 9.25% from 2026 to 2031.

This report is Segmented by Deployment Mode (Web-Based, Cloud-Based, On-Premise), Subscription Model (Perpetual License, SaaS), Application (Communication, Scheduling, Billing, Insurance, Treatment Planning, Imaging, Analytics), End-User (Dental Clinics, Hospitals & Specialty Centers, Academic Institutes, Others), and Practice Size (Solo, Small Group, Large Group, Dsos). Forecast in Value (USD)

U.S. Dental Practice Management Software Market Trends and Insights

Cloud Migration from Server-Based to Browser and Cloud Platforms

Cloud migration from traditional server setups to cloud-based platforms is transforming software purchasing in the United States dental practice management software market. Organizations using modern cloud PMS infrastructure report a 40-55% drop in IT support tickets, an hour less weekly system downtime, and 83% fewer critical IT incidents. Legacy server setups can cost dental organizations 8-12% of annual revenue due to disconnected systems, outdated hardware, and IT inconsistencies. Cloud vendors are gaining traction by simplifying updates, standardizing workflows, and reducing technical reliance, especially for multi-site groups requiring centralized operations.

DSO Standardization and Multi-Location Platform Visibility

DSO standardization is driving repeated migrations in the United States dental practice management software market. Data shows 29% of DSO-affiliated dentists plan to invest in new software in 2026, compared to 16.3% of non-DSO dentists. Planet DDS supported 14,500 practices by 2025, expanding its presence in 100+-location DSOs through partnerships with Sage Dental, Coast Dental, Altius Dental, and Choice Healthcare. Preferred platforms enable DSOs to consolidate operations, offering unified views of collections, utilization, and provider performance, creating a concentrated growth path for enterprise vendors.

Data Privacy, HIPAA, and Right-of-Access Compliance Costs

Data privacy and compliance costs remain a significant barrier to adoption in the United States dental practice management software market, particularly for solo and small-group practices without dedicated IT or compliance teams. Older systems often require additional investments in encryption, access controls, audit logs, and workflow adjustments to securely handle sensitive patient and claims data. Large DSOs can distribute these costs across multiple sites, while independent offices must absorb them within smaller revenue bases. A single healthcare data breach averages USD 10.93 million, keeping cybersecurity a top priority for dental organizations. Compliance pressures drive long-term replacement demand but delay near-term purchases for budget-constrained practices.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Verification, Analytics, and Workflow Automation

- Revenue-Cycle Optimization Under Reimbursement Pressures

- Legacy Data Migration, Retraining, and Workflow Disruption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, on-premise systems accounted for 43.65% of the United States dental practice management software market, reflecting their entrenched presence rather than future demand for server architecture. Cloud deployments are projected to grow at an 11.95% CAGR through 2031, outpacing the overall market. Practices and DSOs prefer cloud models for reduced server maintenance, simplified remote access, and integrated workflows. Organizations adopting cloud PMS environments report fewer IT incidents, supporting the operational benefits of migration.

While on-premise systems will decline gradually, enterprise rollouts increasingly favor cloud solutions for streamlined onboarding and consistent workflows. In 2025, major additions like Sage Dental (140 locations) and Coast Dental (88 locations) highlighted the scale of cloud conversions. Web-based systems occupy a shrinking middle ground as buyers commit to full cloud platforms or retain older setups. Over the forecast period, replacement cycles and uptime needs will drive demand toward cloud-first platforms.

Subscription and SaaS models captured 59.76% of 2025 revenue in the United States dental practice management software market, with a projected 10.25% CAGR through 2031. Vendors now bundle updates, analytics, and AI tools into recurring plans, as seen in Henry Schein One's 2026 launch of Dentrix Ascend packages. Subscription plans reduce upfront costs for practices and increase lifetime contract value for vendors by layering additional features over time. SaaS models also enable steady delivery of updates and new functionalities, making them the primary revenue model.

Complete Report Scope:

- By Deployment Mode

- Web-based

- Cloud-based

- On-premise

- By Subscription Model

- Perpetual License

- Subscription / SaaS

- By Application

- Patient Communication & Engagement

- Appointment Scheduling & Calendar

- Billing & Invoicing

- Insurance & Claims Management

- Treatment Planning & Charting

- Imaging & Diagnostics Integration

- Analytics & Business Intelligence

- By End-user

- Dental Clinics

- Hospitals & Specialty Dental Centers

- Academic & Research Institutes

- Others

- By Practice Size

- Solo Practices (1-2 ops)

- Small Group Practices (3-9 ops)

- Large Group Practices (10+ ops)

- Dental Service Organizations (DSOs)

List of Companies Covered in this Report:

- ABELDent Inc.

- ACE Dental Software

- Carestream Dental

- CD Newco, LLC

- Datacon Dental Systems, Inc.

- DentiMax LLC

- Dentisoft Technologies

- Exan Software ULC

- Good Methods Global Inc.

- Henry Schein One, LLC

- iDentalSoft, Inc.

- MacPractice, Inc.

- MOGO, Inc.

- NextGen Healthcare

- Open Dental Software, Inc.

- Oryx Dental Software LLC

- Patterson Companies

- Planet DDS, Inc.

- Practice-Web, Inc.

- tab32

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration from Server-Based to Browser-Native Platforms

- 4.2.2 DSO Standardization and Multi-Location Visibility Needs

- 4.2.3 AI-Enabled Verification, Analytics, and Workflow Automation

- 4.2.4 Revenue-Cycle Optimization Under Reimbursement Pressure

- 4.2.5 Medical-Dental Data Exchange Needs for Medically Complex Patients

- 4.2.6 Tech-Stack Standardization as A Valuation Lever in DSO Roll-Ups

- 4.3 Market Restraints

- 4.3.1 Data Privacy, HIPAA, and Right-of-Access Compliance Exposure

- 4.3.2 Legacy Data Migration, Retraining, and Workflow Disruption

- 4.3.3 Fragmented Interoperability with Medical Records and Payer Workflows

- 4.3.4 Small-Practice ROI Friction and Subscription-Stack Fatigue

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Deployment Mode

- 5.1.1 Web-based

- 5.1.2 Cloud-based

- 5.1.3 On-premise

- 5.2 By Subscription Model

- 5.2.1 Perpetual License

- 5.2.2 Subscription / SaaS

- 5.3 By Application

- 5.3.1 Patient Communication & Engagement

- 5.3.2 Appointment Scheduling & Calendar

- 5.3.3 Billing & Invoicing

- 5.3.4 Insurance & Claims Management

- 5.3.5 Treatment Planning & Charting

- 5.3.6 Imaging & Diagnostics Integration

- 5.3.7 Analytics & Business Intelligence

- 5.4 By End-user

- 5.4.1 Dental Clinics

- 5.4.2 Hospitals & Specialty Dental Centers

- 5.4.3 Academic & Research Institutes

- 5.4.4 Others

- 5.5 By Practice Size

- 5.5.1 Solo Practices (1-2 ops)

- 5.5.2 Small Group Practices (3-9 ops)

- 5.5.3 Large Group Practices (10+ ops)

- 5.5.4 Dental Service Organizations (DSOs)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 ABELDent Inc.

- 6.3.2 ACE Dental Software

- 6.3.3 Carestream Dental LLC

- 6.3.4 CD Newco, LLC

- 6.3.5 Datacon Dental Systems, Inc.

- 6.3.6 DentiMax LLC

- 6.3.7 Dentisoft Technologies

- 6.3.8 Exan Software ULC

- 6.3.9 Good Methods Global Inc.

- 6.3.10 Henry Schein One, LLC

- 6.3.11 iDentalSoft, Inc.

- 6.3.12 MacPractice, Inc.

- 6.3.13 MOGO, Inc.

- 6.3.14 NextGen Healthcare, Inc.

- 6.3.15 Open Dental Software, Inc.

- 6.3.16 Oryx Dental Software LLC

- 6.3.17 Patterson Companies, Inc.

- 6.3.18 Planet DDS, Inc.

- 6.3.19 Practice-Web, Inc.

- 6.3.20 tab32

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment