|

시장보고서

상품코드

2072675

미국의 비PVC IV 백 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Non-PVC IV Bags - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

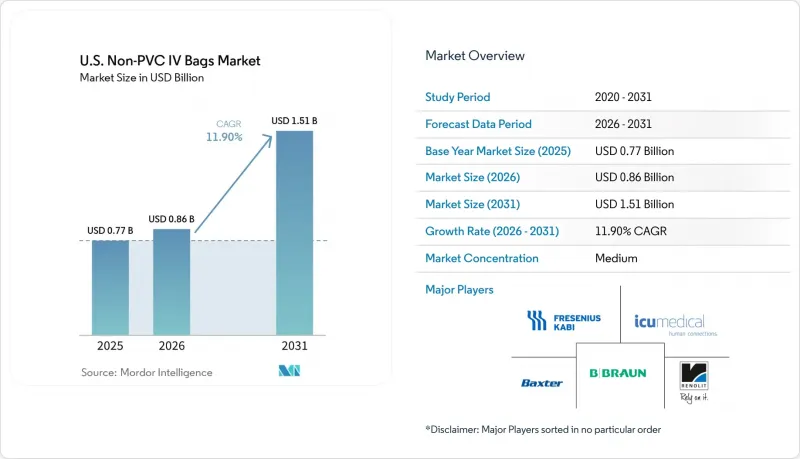

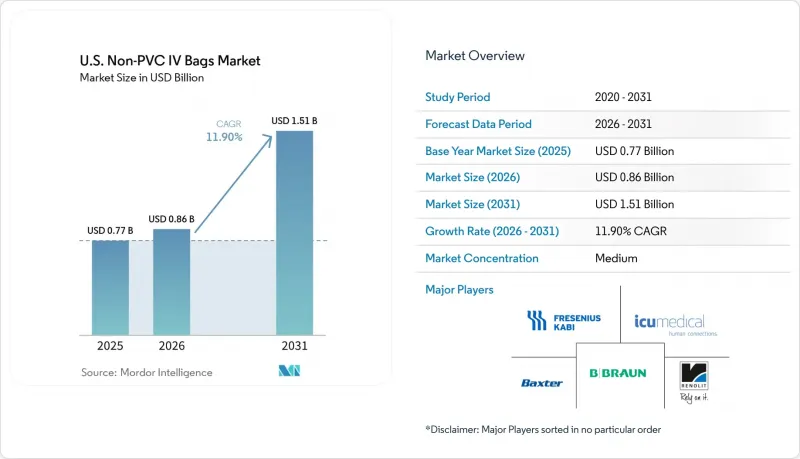

Mordor Intelligence에 의하면, 미국의 비PVC IV 백 시장 규모는 2025년에 7억 7,000만 달러로 평가되었고, 2026년에 8억 6,000만 달러로 추정되고, 2031년까지 15억 1,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 11.90%로 성장할 전망입니다.

본 보고서는 소재별(폴리프로필렌, 폴리올레핀 블렌드, EVA, 코폴리에스터 에테르, 기타), 챔버 구성별(싱글 챔버, 멀티 챔버), 용량별(100 mL 미만, 100-250 mL, 251-500 mL, 501-1,000 mL, 1,000 mL 이상), 내용물 유형별(액체, 냉동 혼합물), 최종 사용자별(병원, 전문 클리닉, 당일 수술센터(ASC), 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 비PVC IV 백 시장 동향 및 분석

고위험 환자 집단에서 DEHP/PVC의 단계적 폐지가 사양 변경을 촉진

각 주의 법률은 병원 및 공급업체에 대한 명확한 기준을 마련함으로써 미국의 비PVC IV 백 시장을 주도하고 있습니다. 2024년 9월에 제정된 캘리포니아주 AB 2300법은 2030년 이후부터 수액 용기에 DEHP의 사용을 금지하며, 다른 오르토프탈산 에스테르류로 대체하는 것도 금지하고 있습니다. 2026년 3월에 통과된 펜실베이니아주 상원 법안 804호도 이와 유사한 접근 방식을 취하고 있습니다. 이러한 규제는 가소제 용출 위험이 큰 신생아 관리, 암 치료 시의 정맥 주사, 그리고 장기 정맥 영양 공급에서 매우 중요합니다. 이러한 환자 집단을 위한 규격을 개정하는 병원들은 표준화를 용이하게 하기 위해 변경 내용을 더 광범위한 의약품 목록으로 확대하는 경우가 많으며, 이로 인해 시장 전반에 걸친 도입이 가속화되고 있습니다.

종양학 및 유해 약물과의 적합성에 대한 요구가 용기 선정 기준의 재정의로 이어지고 있습니다.

종양학 분야에서는 용기 선정 기준이 엄격해지고 유해 약제와의 호환성이 중요시됨에 따라, 비PVC 소재에 대한 수요가 증가하고 있습니다. 개정된 USP 기준에 따라, 초점은 비용에서 용기와 제제 간의 상호작용으로 옮겨졌습니다. 폴리프로필렌 다층 시스템과 같은 비PVC 소재는 화학적 안정성과 안전성 덕분에 선호되고 있습니다. ICU Medical이나 Fresenius Kabi와 같은 공급업체들은 중요한 용도를 위해 비PVC 제품을 포지셔닝하고, 이러한 사양을 일상 업무에 반영함으로써 시장 수요를 안정화하고 있습니다.

비PVC 수지 및 가공 비용의 높이가 보급률을 저해하고 있습니다.

도입 가속화의 주요 장애물은 비용이며, 고성능 비PVC 필름은 표준 PVC 소재보다 가격이 비쌉니다. 가방 제조업체들은 폴리프로필렌이나 첨단 EVA 구조와 같은 고가의 원자재뿐만 아니라, 설비에 대한 추가 투자로 인해 비용 증가에 직면해 있습니다. 병원이나 외래수술센터(ASC), 특히 고정 가격 계약을 체결한 소규모 시설에서는 이러한 비용 증가를 감당하는 데 어려움을 겪고 있습니다. 프리믹스 사용으로 인한 노동력 절감 및 취급 작업 감소와 같은 광범위한 경제적 이점은 예산 평가 과정에서 간과되기 쉬우며, 임상적 측면과 규정 준수 측면에서 강력한 근거가 있음에도 불구하고 전환 속도를 늦추고 있습니다. 미국의 비PVC IV 백 시장은 꾸준한 성장세를 보이고 있지만, 그 성장 속도는 재료의 안전성과 비용 압박 간의 균형에 달려 있습니다.

부문별 분석

2025년, EVA는 매출의 47.65%를 차지했으며, 미국의 비PVC IV 백 시장에서 주요 소재로 자리매김하고 있습니다. 이러한 장점은 다양한 약제와의 호환성, 검사 시 뛰어난 가시성, 그리고 안정적인 동결-해동 특성에서 비롯되며, 동결 항생제, 전해질 용액 및 혈액 호환성 제제에 가장 적합합니다. EVA의 범용성은 표준화된 봉투 형태를 뒷받침하며, 시장 내 기반으로서의 입지를 공고히 하고 있습니다.

폴리프로필렌 시장은 2031년까지 연평균 성장률(CAGR) 13.20%를 기록하며 성장할 전망이며, 종양학 및 다실식 비경구 영양 시스템과 같은 전문적인 용도에서 주목받고 있습니다. 이러한 장점으로는 유해 약제와의 호환성 및 고도의 다층 구조에 대한 적합성 등을 들 수 있습니다. 프레제니우스 카비사의 다층 수액백에 관한 특허와 같은 혁신은 이 소재가 고도의 임상 분야에서 수행하는 역할이 확대되고 있음을 여실히 보여주고 있습니다.

2025년에는 싱글 챔버 백이 매출의 65.55%를 차지했으며, 미국의 비PVC IV 백 시장에서 1위 자리를 유지했습니다. 수액 보충이나 일상적인 정맥 주사 투여 시 사용이 간편할 뿐만 아니라, 제조가 용이하고 간호 업무 흐름과도 잘 조화를 이루기 때문에 지속적인 우위를 보장하고 있습니다.

2031년까지 연평균 성장률(CAGR) 12.10%를 나타낼 것으로 예측되는 멀티 챔버 백은 비경구 영양 공급이나 항생제 병용 치료 시 '혼합 완료된 제품'에 대한 수요를 충족시키고 있습니다. 이 가방들은 무균 조제를 간소화하고, 조제 오류를 줄이며, 표준화된 업무 흐름에 부합함으로써 시장의 성장을 주도하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the u.S. non-PVC iV bags market size is projected to be USD 0.77 billion in 2025, USD 0.86 billion in 2026, and reach USD 1.51 billion by 2031, growing at a CAGR of 11.90% from 2026 to 2031.

This report is Segmented by Material (Polypropylene, Polyolefin Blends, EVA, Copolyester Ether, Others), Chamber Configuration (Single-Chamber, Multi-Chamber), Capacity (Below 100 ML, 100-250 ML, 251-500 ML, 501-1, 000 ML, Above 1, 000 ML), Content Type (Liquid, Frozen Mixtures), and End User (Hospitals, Specialty Clinics, Ascs, Others). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Non-PVC IV Bags Market Trends and Insights

DEHP/PVC Phase-Out in High-Risk Patient Cohorts Drives Specification Rewrites

State laws are driving the United States non-PVC IV bags market by setting clear standards for hospitals and suppliers. California's AB 2300, enacted in September 2024, bans DEHP in IV solution containers from 2030 and prohibits substitution with other ortho-phthalates. Pennsylvania's Senate Bill 804, passed in March 2026, follows a similar approach. These regulations are critical in neonatal care, oncology infusion, and long-term parenteral nutrition, where plasticizer migration risks are significant. Hospitals revising specifications for these patient groups often extend changes across broader formularies for easier standardization, accelerating the market's shift to system-wide adoption.

Oncology and Hazardous-Drug Compatibility Needs Redefine Container Selection Standards

In oncology, stricter container selection criteria emphasize compatibility with hazardous drugs, increasing the demand for non-PVC materials. Updated USP standards have shifted focus from cost to container interaction with formulations. Non-PVC options like polypropylene multilayer systems are preferred for their chemical stability and safety. Suppliers such as ICU Medical and Fresenius Kabi are positioning non-PVC formats for critical applications, embedding these specifications into routine practices and stabilizing market demand.

Higher Non-PVC Resin and Conversion Economics Constrain Adoption Rate

The primary barrier to faster adoption is cost, as advanced non-PVC films are priced higher than standard PVC materials. Bag manufacturers face increased expenses due to costly inputs like polypropylene and advanced EVA structures, along with additional investments in equipment. Hospitals and Ambulatory Surgical Centers (ASCs), particularly smaller facilities with fixed-price contracts, struggle to absorb these higher costs. The broader economic benefits of premix use, such as reduced labor and handling, are often overlooked in budget evaluations, slowing the transition despite strong clinical and compliance arguments. Growth in the United States non-PVC IV bags market remains steady, but the pace depends on balancing material safety with cost pressures.

Other drivers and restraints analyzed in the detailed report include:

- Ready-to-Administer and Premix Infusion Adoption Reshapes Compounding Economics

- Domestic Supply-Resilience Sourcing Accelerates Nearshoring Investment

- Drug-Container Compatibility and Validation Burden Slows Formulary Transitions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, EVA accounted for 47.65% of revenue, making it the leading material in the United States non-PVC IV bags market. Its dominance stems from broad drug compatibility, clear visibility for inspections, and stable freeze-thaw performance, making it ideal for frozen antibiotics, electrolyte solutions, and blood-compatible formulations. EVA's versatility supports standardized bag formats, reinforcing its position as the market's foundation.

Polypropylene, growing at a 13.20% CAGR through 2031, is gaining traction in specialized applications like oncology and multi-chamber parenteral nutrition systems. Its advantages include hazardous-drug compatibility and suitability for advanced multi-layer construction. Innovations like Fresenius Kabi's patent for multilayer infusion bags highlight the material's expanding role in premium clinical applications.

Single-chamber bags held 65.55% of revenue in 2025, maintaining their lead in the United States non-PVC IV bags market. Their straightforward use in fluid replacement and routine infusions, coupled with ease of manufacturing and alignment with nursing workflows, ensures their continued dominance.

Multi-chamber bags, projected to grow at a 12.10% CAGR through 2031, address the demand for ready-to-mix products in parenteral nutrition and antibiotic combinations. These bags simplify sterile preparation, reduce compounding errors, and align with standardized workflows, driving their growth in the market.

Complete Report Scope:

- By Material

- Polypropylene

- Polyolefin blends

- Ethylene Vinyl Acetate (EVA)

- Copolyester / Copolyester Ether

- Ethylene-Propylene Copolymer and Other Multilayer Films

- By Chamber Configuration

- Single-chamber bags

- Multi-chamber bags

- By Capacity

- Below 100 mL

- 100 mL to 250 mL

- 251 mL to 500 mL

- 501 mL to 1,000 mL

- Above 1,000 mL

- By Content Type

- Liquid Mixtures

- Frozen Mixtures

- By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Others

List of Companies Covered in this Report:

- Amcor plc

- B. Braun

- Baxter

- Central Admixture Pharmacy Services, Inc. (CAPS)

- Eastman Chemical Company

- Epic Medical Pte. Ltd.

- Fagron Sterile Services US

- Fresenius

- Hospira, Inc.

- ICU Medical

- Kraton

- Laboratorios Grifols, S.A.

- Otsuka Pharmaceutical Factory, Inc.

- Pfizer

- PolyCine GmbH

- RENOLIT

- Sealed Air Corporation

- Technoflex

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 DEHP/PVC Phase-Out in High-Risk Patient Cohorts

- 4.2.2 Oncology and Hazardous-Drug Compatibility Needs

- 4.2.3 Ready-To-Administer and Premix Infusion Adoption

- 4.2.4 Domestic Supply-Resilience Sourcing After IV Fluid Disruptions

- 4.2.5 USP <797>-Driven Container Validation in Sterile Compounding

- 4.2.6 State-Level Non-DEHP Compliance and Sustainability-Led Purchasing

- 4.3 Market Restraints

- 4.3.1 Higher Non-PVC Resin and Conversion Economics

- 4.3.2 Drug-Container Compatibility and Validation Burden

- 4.3.3 Installed-Base PVC Workflow Lock-in

- 4.3.4 Non-DEHP Versus Non-PVC Labeling Ambiguity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Polypropylene

- 5.1.2 Polyolefin blends

- 5.1.3 Ethylene Vinyl Acetate (EVA)

- 5.1.4 Copolyester / Copolyester Ether

- 5.1.5 Ethylene-Propylene Copolymer and Other Multilayer Films

- 5.2 By Chamber Configuration

- 5.2.1 Single-chamber bags

- 5.2.2 Multi-chamber bags

- 5.3 By Capacity

- 5.3.1 Below 100 mL

- 5.3.2 100 mL to 250 mL

- 5.3.3 251 mL to 500 mL

- 5.3.4 501 mL to 1,000 mL

- 5.3.5 Above 1,000 mL

- 5.4 By Content Type

- 5.4.1 Liquid Mixtures

- 5.4.2 Frozen Mixtures

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Specialty Clinics

- 5.5.3 Ambulatory Surgical Centers

- 5.5.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Amcor plc

- 6.3.2 B. Braun Medical Inc.

- 6.3.3 Baxter International Inc.

- 6.3.4 Central Admixture Pharmacy Services, Inc. (CAPS)

- 6.3.5 Eastman Chemical Company

- 6.3.6 Epic Medical Pte. Ltd.

- 6.3.7 Fagron Sterile Services US

- 6.3.8 Fresenius Kabi AG

- 6.3.9 Hospira, Inc.

- 6.3.10 ICU Medical, Inc.

- 6.3.11 Kraton Corporation

- 6.3.12 Laboratorios Grifols, S.A.

- 6.3.13 Otsuka Pharmaceutical Factory, Inc.

- 6.3.14 Pfizer Inc.

- 6.3.15 PolyCine GmbH

- 6.3.16 RENOLIT SE

- 6.3.17 Sealed Air Corporation

- 6.3.18 Technoflex

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment