|

시장보고서

상품코드

2072676

미국의 정형외과용 보조기 및 지지대 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Orthopedic Braces And Supports - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

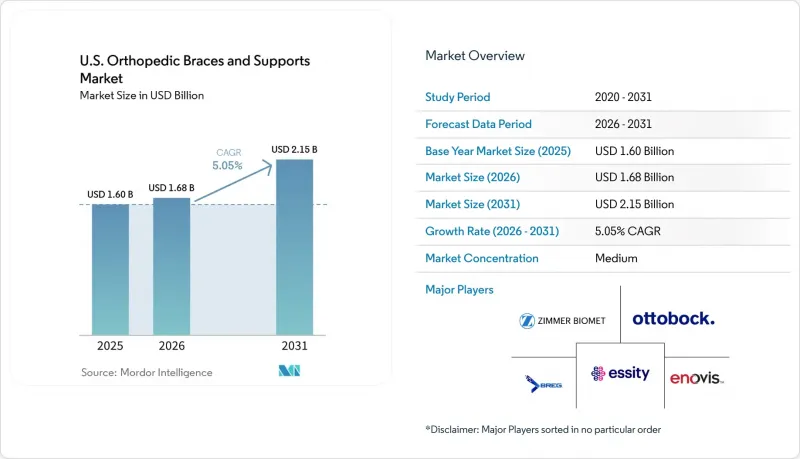

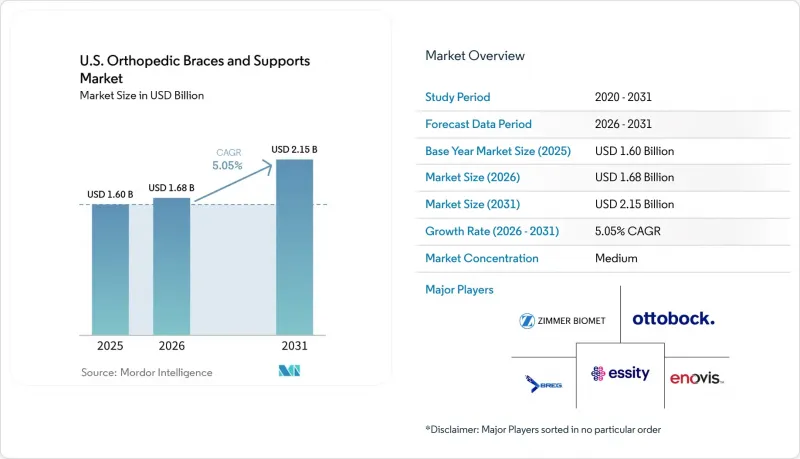

Mordor Intelligence에 의하면, 미국의 정형외과용 보조기 및 지지대 시장 규모는 2025년 16억 달러로 평가되었고, 2026년 16억 8,000만 달러로 추정되고, 2031년까지 21억 5,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 5.05%를 나타낼 전망입니다.

본 보고서는 제품별(무릎 보호대, 발목 및 발용, 등 및 척추용 등), 용도별(인대 손상, 예방 관리, 수술 후 재활, 퇴행성 관절염, 기타 만성 질환), 최종 사용자별(병원 및 외과 센터, 정형외과 클리닉, 재택 간호 등), 지역별로 분류되어 있습니다. 예측치는 금액(달러)으로 표시되어 있습니다.

미국의 정형외과용 보조기 및 서포터 시장 동향과 인사이트

미국의 인구 고령화와 퇴행성 관절염으로 인한 부담

미국에서는 노인을 대상으로 한 퇴행성 관절염의 부담이 심화되고 있으며, 이로 인해 무릎, 고관절, 허리 질환에 대한 장기적인 보조기 사용이 증가하고 있습니다. 2025년, 55세 이상 성인의 퇴행성 관절염 유병률은 10만 명당 1,973.19명으로, 다른 주요 시장을 상회했습니다. 75세 이상 성인의 53.9%가 관절염 진단을 받았으며, 45세 이상에서는 전체 환자의 88%를 차지함에 따라, 통증을 완화하고 관절 가동 범위를 유지해 주는 의료진이 처방하는 의료기기에 대한 수요가 증가하고 있습니다. 2030년까지 베이비붐 세대가 75세 이상이 됨에 따라, 정형외과용 보조기 및 서포터 시장은 지속적인 성장이 예상되며, 특히 무릎 하중 경감 보조기나 고관절 하중 경감 제품에서 이러한 추세가 두드러질 것으로 보입니다.

스포츠 및 근골격계 손상의 높은 발생률

미국에서 스포츠 활동 참여로 인해 인대, 발목, 무릎, 어깨 부상이 계속해서 증가하고 있습니다. 스포츠 관련 부상으로 인한 응급실 내원 건수는 2024년에 440만 건에 달했으며, 2023년 대비 17% 증가했습니다. 고등학교 스포츠 프로그램에서는 2024/25 학년도 동안 5,921건의 부상이 보고되었으며, 그중에서도 무릎과 발목의 인대 손상이 가장 많이 나타났습니다. 성인의 여가 활동, 특히 35세에서 60세 사이의 연령층에서 이루어지는 활동 역시 처방전이 필요한 등급의 보조기구에 대한 수요를 더욱 촉진하고 있으며, 이는 시장의 꾸준한 성장을 보장하고 있습니다.

보험 환급 격차와 환자의 본인 부담금

보험 환급과 관련된 과제는 임상적 권고 사항을 제품 도입으로 이어가는 데 있어 여전히 큰 장벽으로 남아 있습니다. 메디케어와 메디케이드는 정형외과용 보조기를 사용하는 환자, 특히 퇴행성 관절염, 만성 근골격계 질환 또는 수술 후 회복이 필요한 환자의 상당 부분을 보장하고 있습니다. 2026년 DMEPOS 요금표 개정에서 비경쟁 입찰 대상 보조기 품목의 가격이 2.0% 인상되었고, 보조기 관련 작업 코드 L4205는 2.7% 상승했으나, 이 모두 보조기 제조업체들이 직면한 원가 상승분을 따라잡지 못하고 있습니다. 보조 보험이나 본인 부담금은 고정 소득을 가진 환자, 특히 언로더형 무릎 보조기나 변형성 고관절증용 보조기와 같은 고가 제품의 경우, 도입을 지연시키는 요인이 되는 경우가 많습니다. 이 문제는 듀얼 엘리저블(메디케어와 메디케이드에 모두 가입한 사람)이나 저소득 지역에서 더욱 두드러지며, 보험 적용 범위의 제한과 의료 제공업체의 어려운 경영 상황으로 인해 잠재적 수요가 줄어들고 있습니다.

부문별 분석

2025년, 무릎 보조기 및 서포터는 시장 점유율의 36.11%를 차지했으며, 미국 정형외과용 보조기 및 서포터 시장의 주요 수익원이 되고 있습니다. 퇴행성 관절염 관리, 인대 손상 회복, 그리고 활동적인 성인층을 대상으로 한 예방적 사용 등 폭넓은 용도가 있어 자주 처방되고 있습니다. 이 부문은 저가형 일반 판매(OTC) 슬리브부터 1,000달러가 넘는 맞춤형 언로더 장치에 이르기까지 폭넓은 가격대를 아우르며, 판매량과 매출액 모두에서 성과를 거두고 있습니다.

'등 및 척추용 보조기'는 만성 요통, 수술 후 안정화, 그리고 업무로 인한 근육 긴장 완화를 위한 용도로 사용되면서 여전히 중요한 분야로 자리 잡고 있습니다. '발목 및 발용 보조기'는 염좌 관리 및 종골·경골 수술 후 회복에 대한 수요에 힘입어 중요한 위치를 차지하고 있습니다. 상지 보조기는 어깨, 손목, 팔꿈치 질환에 대한 체계적인 외래 치료를 바탕으로 2031년까지 연평균 성장률(CAGR) 6.06%를 기록하며 성장할 것으로 전망됩니다. 2026년 1월 스미스 앤 네퓨(Smith & Nephew)의 인테그리티 오르토페딕스(Integrity Orthopedics) 인수와, 2026년 바우어파인드(Bauerfind)사의 슬개골 추종형 보조기 'GenuTrain P3' 제품의 출시는 제품 라인업 확충을 위한 전략적 노력을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the u.S. orthopedic braces and supports market size is projected to expand from USD 1.60 billion in 2025 and USD 1.68 billion in 2026 to USD 2.15 billion by 2031, registering a CAGR of 5.05% between 2026 to 2031.

This report is Segmented by Product (Knee Braces, Ankle & Foot, Back & Spine, and More), Application (Ligament Injury, Preventive Care, Post-Operative Rehabilitation, Osteoarthritis, Other Chronic Conditions), End User (Hospitals & Surgical Centers, Orthopedic Clinics, Homecare, and More), and Geography. Forecasts are Provided in Value (USD).

U.S. Orthopedic Braces And Supports Market Trends and Insights

Aging US Population and Osteoarthritis Burden

The United States faces a significant osteoarthritis burden among older adults, driving long-term brace usage for knee, hip, and back conditions. In 2025, osteoarthritis incidence among adults aged 55 and older was 1,973.19 per 100,000, surpassing other major markets. With 53.9% of adults aged 75 and older diagnosed with arthritis and 88% of cases in those aged 45 and above, demand for clinician-directed devices that alleviate pain and maintain mobility is rising. As Baby Boomers age into the 75-plus bracket by 2030, the orthopedic braces and supports market will see sustained growth, particularly for unloader knee braces and hip offloading products.

High Sports and Musculoskeletal Injury Incidence

Sports participation in the United States continues to drive ligament, ankle, knee, and shoulder injuries. Emergency department visits for sports-related injuries reached 4.4 million in 2024, a 17% increase from 2023. High school programs reported 5,921 injuries during the 2024/25 academic year, with knee and ankle ligament injuries being most common. Adult recreational activities, especially among those aged 35 to 60, further contribute to demand for prescription-grade braces, ensuring steady market growth.

Reimbursement Gaps and Patient Out-of-Pocket Burden

Reimbursement challenges remain a significant barrier to converting clinical recommendations into product adoption. Medicare and Medicaid cover a substantial portion of patients using orthopedic braces, particularly those with osteoarthritis, chronic musculoskeletal conditions, or post-surgical recovery needs. The 2026 DMEPOS fee schedule update reflected a 2.0% increase for non-competitive-bidding orthotic items, while orthotic labor code L4205 rose by 2.7%, both trailing the rising costs faced by brace manufacturers. Co-insurance and deductibles often delay adoption for fixed-income patients, especially for premium devices like unloader knee and OA hip braces. This issue is more pronounced in dual-eligible and lower-income regions, where limited coverage and tight provider economics reduce addressable demand.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Non-Invasive Care and Post-Operative Rehabilitation

- 2026 Lower-Extremity Orthosis Code Expansion

- Commoditization Pressure in Soft Goods and OTC Channels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Knee Braces & Supports accounted for 36.11% of the market share in 2025, making them the primary revenue driver in the United States orthopedic braces and supports market. Their broad application in osteoarthritis management, ligament injury recovery, and preventive use among active adults ensures frequent prescriptions. The segment benefits from a wide price range, from low-cost OTC sleeves to custom unloader devices exceeding USD 1,000, capturing both volume and value.

Back & Spine Braces remain a key segment due to their use in chronic lumbar pain, post-surgical stabilization, and work-related strain. Ankle & Foot Braces hold a significant position, driven by demand for sprain management and recovery from calcaneal and tibial procedures. Upper-extremity Braces are projected to grow at a 6.06% CAGR through 2031, supported by structured outpatient care for shoulder, wrist, and elbow conditions. Smith+Nephew's acquisition of Integrity Orthopaedics in January 2026 and Bauerfeind's launch of the GenuTrain P3 patella tracking brace in 2026 highlight the strategic focus on expanding product offerings.

Complete Report Scope:

- By Product

- Knee Braces & Supports

- Ankle & Foot Braces

- Back & Spine Braces

- Upper-extremity Braces

- Hip & Pelvic Braces

- Others

- By Application

- Ligament Injury

- Preventive Care

- Post-operative Rehabilitation

- Osteoarthritis

- Other Chronic Conditions

- By End User

- Hospitals & Surgical Centers

- Orthopedic Clinics

- Homecare Settings

- Sports & Rehabilitation Centers

List of Companies Covered in this Report:

- 3M Company (Solventum)

- Aspen Medical Products, LLC

- Bauerfeind USA Inc.

- Becker Orthopedic, Inc.

- Bird & Cronin, LLC

- Breg

- DeRoyal Industries

- Embla Medical hf.

- Enovis Corporation

- Essity

- Fillauer

- Frank Stubbs Company, Inc.

- Hanger, Inc.

- McDavid, Inc.

- medi

- Mueller Sports Medicine, Inc.

- Orthofix

- Ottobock

- Weber Orthopedic LP. DBA Hely & Weber

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging U.S. Population and Osteoarthritis Burden

- 4.2.2 High Sports and Musculoskeletal Injury Incidence

- 4.2.3 Shift Toward Non-Invasive Care and Post-Operative Rehabilitation

- 4.2.4 Product Innovation in Lightweight, Breathable, Low-Profile Bracing

- 4.2.5 2026 Lower-Extremity Orthosis Code Expansion Supports Premiumization

- 4.2.6 Digital Ordering, Scanning, and DMEPOS Workflow Tools Improve Clean-Claim Conversion

- 4.3 Market Restraints

- 4.3.1 Reimbursement Gaps and Patient Out-of-Pocket Burden

- 4.3.2 Commoditization Pressure in Soft Goods and OTC Channels

- 4.3.3 Tight Custom-Fabricated Eligibility and Documentation Burden

- 4.3.4 Non-Rigid Supports Can Fall Outside Medicare Brace Benefit

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Reimbursement Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Knee Braces & Supports

- 5.1.2 Ankle & Foot Braces

- 5.1.3 Back & Spine Braces

- 5.1.4 Upper-extremity Braces

- 5.1.5 Hip & Pelvic Braces

- 5.1.6 Others

- 5.2 By Application

- 5.2.1 Ligament Injury

- 5.2.2 Preventive Care

- 5.2.3 Post-operative Rehabilitation

- 5.2.4 Osteoarthritis

- 5.2.5 Other Chronic Conditions

- 5.3 By End User

- 5.3.1 Hospitals & Surgical Centers

- 5.3.2 Orthopedic Clinics

- 5.3.3 Homecare Settings

- 5.3.4 Sports & Rehabilitation Centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 3M Company (Solventum)

- 6.3.2 Aspen Medical Products, LLC

- 6.3.3 Bauerfeind USA Inc.

- 6.3.4 Becker Orthopedic, Inc.

- 6.3.5 Bird & Cronin, LLC

- 6.3.6 Breg, Inc.

- 6.3.7 DeRoyal Industries, Inc.

- 6.3.8 Embla Medical hf.

- 6.3.9 Enovis Corporation

- 6.3.10 Essity Aktiebolag

- 6.3.11 Fillauer LLC

- 6.3.12 Frank Stubbs Company, Inc.

- 6.3.13 Hanger, Inc.

- 6.3.14 McDavid, Inc.

- 6.3.15 medi GmbH & Co. KG

- 6.3.16 Mueller Sports Medicine, Inc.

- 6.3.17 Orthofix Medical Inc.

- 6.3.18 Ottobock SE & Co. KGaA

- 6.3.19 Weber Orthopedic LP. DBA Hely & Weber

- 6.3.20 Zimmer Biomet Holdings, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment