|

시장보고서

상품코드

2072683

비디오 콘텐츠 마케팅 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Video Content Marketing Services Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

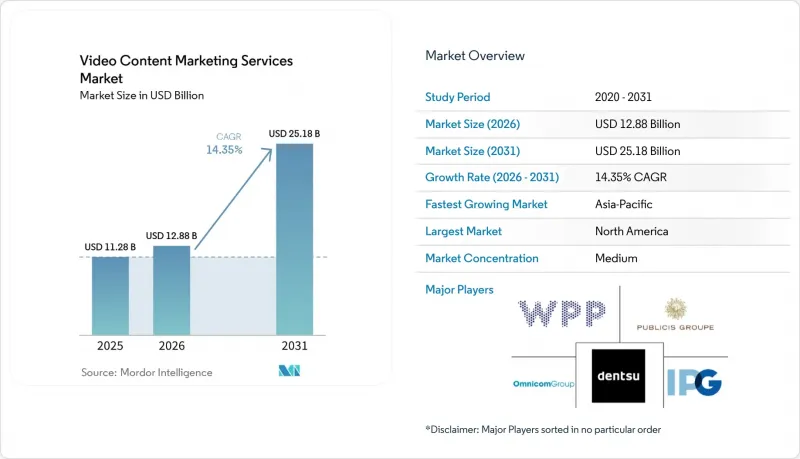

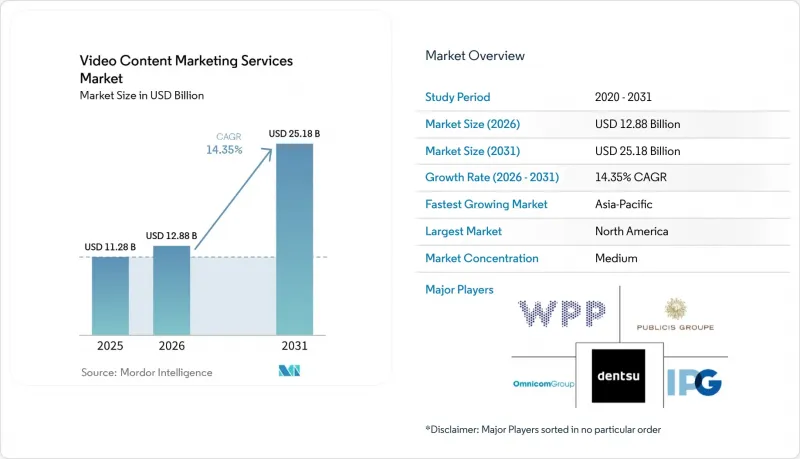

Mordor Intelligence에 의하면, 비디오 콘텐츠 마케팅 서비스 시장 규모는 2025년에 112억 8,000만 달러로 평가되었고, 2026년 128억 8,000만 달러로 추정되고, 2031년까지 251억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 14.35%를 나타낼 전망입니다.

본 보고서는 서비스 유형별(전략 및 컨설팅, 컨텐츠 아이디어 구상 및 각본 작성 등), 동영상 유형별(해설 동영상, 튜토리얼 및 하우투 동영상 등), 동영상 길이별(숏폼 동영상, 롱폼 동영상), 최종 사용자 산업 분야별(소매 및 전자상거래, 소비재 및 미용, BFSI 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 비디오 콘텐츠 마케팅 서비스 시장 동향 및 인사이트

단편 동영상에 대한 예산 배분 증가

비디오 콘텐츠 마케팅 서비스 시장에서 숏폼 동영상은 단순한 보조적 전술에서 소셜 및 성과 기반 마케팅 전략의 핵심으로 그 위상이 변화하고 있습니다. Wistia의 보고서에 따르면, 2026년에는 전 세계 마케팅 예산의 57%에 숏폼 동영상 전용 예산 항목이 포함될 것이며, 60초 미만의 동영상은 다른 컨텐츠 형식에 비해 노출당 참여도가 2.5배 더 높았다고 합니다. 이러한 변화로 인해 외부 위탁에 대한 수요가 증가하고 있습니다. 이는 플랫폼별 단편 동영상 프로그램의 경우 반복적인 편집, 다양한 화면비, 빈번한 업데이트 주기가 필요하며, 많은 사내 팀에서는 이를 대규모로 유지하기 어렵기 때문입니다. IAB에 따르면, 2026년 미국의 소셜 동영상 관련 지출은 13% 증가했으며, 이는 지속적인 관리 실행에 의존하는 형식으로의 예산 전환 속도를 뒷받침하는 것입니다. 브랜드가 하나의 원본 자산에서 4-6가지 플랫폼별 편집 버전을 제작하는 가운데, 컨텐츠의 버전 관리, 최적화, 배포를 효율적으로 수행할 수 있는 제공업체가 비디오 콘텐츠 마케팅 서비스 시장에서 더 많은 지속적인 업무를 수주하고 있습니다.

AI를 활용한 제작 및 버전 관리에 대한 기업 수요 증가

기업 구매 담당자들은 비디오 콘텐츠 마케팅 서비스 시장에서 AI 기반 워크플로우를 활용하여 인력을 늘리지 않고도 제작량을 확대되고 있습니다. Goldcast와 Redpoint의 조사에 따르면, 2025년에는 B2B 마케터의 89%, 경영진의 94%가 동영상을 전략적으로 중요하게 여기고 있으며, 75%에 가까운 이들이 동영상 제작 예산을 증액했습니다. 첨단 AI 동영상 전략을 도입한 조직은 동영상 제작량을 늘릴 가능성이 4.5배 더 높으며, CIO의 77%는 AI를 활용한 동영상 제작 솔루션이라면 가격이 비싸더라도 지불할 의향이 있다고 응답했습니다. 이러한 수요로 인해, 단순한 자동화 솔루션을 판매하는 것이 아니라 AI 생성, 승인 워크플로우, 브랜드 관리, 출력 품질 검사를 결합한 서비스를 제공하는 기업들이 혜택을 보고 있습니다. 그 결과, 기업 계약 분야에서 속도, 버전 관리, 거버넌스가 하나로 어우러져 중요시되는 시장 환경이 조성되고 있습니다.

'월드 가든' 전반적으로 존재하는 ROI 귀속의 격차

ROI 귀속과 관련된 격차가 해소되지 않는 것은 비디오 콘텐츠 마케팅 서비스 시장의 지출에 단기적인 걸림돌이 되고 있습니다. 주요 플랫폼에서는 여전히 노출과 전환을 별도의 시스템으로 측정하고 있으며, 그 결과 동일한 매출에 대해 여러 채널이 성과를 주장하게 되어 크로스 채널 평가가 복잡해지고 있습니다. 그 때문에 대리점이나 서비스 제공업체는 재무 부서나 조달 부서에 대해 퍼널 업스트림 단계에서 동영상의 진정한 가치를 입증하기가 어려워지고 있습니다. 실제로 이 문제로 인해 성과 연동형 가격 책정에 대한 신뢰가 떨어지게 되어, 컨텐츠 양만으로 정당화되어야 할 계약 규모에 미치지 못할 가능성이 있습니다. 고객사가 ROI를 더욱 엄격하게 검토하는 가운데, 더 강력한 분석 기능, 테스트 프레임워크, 측정 거버넌스를 갖춘 공급업체일수록 수익성을 유지하기 쉬운 입장에 있습니다.

부문별 분석

2025년, 동영상 제작은 비디오 콘텐츠 마케팅 서비스 시장 규모의 34.22%를 차지했으며, 여전히 최대 서비스 카테고리로서의 위상을 유지했습니다. 이 지위는 구조적인 것이며, 전략, SEO, 배포, 홍보 업무의 모든 것이 제작물을 기반으로 하는 자산에 의존하고 있기 때문입니다. 라이브 촬영, 편집, 포스트 프로덕션은 여전히 상업용 동영상 프로그램과 분리하기 어렵기 때문에 이 부문은 계속해서 대기업, 대행사 및 브랜드 직영 업체로부터의 지출을 유치하고 있습니다. 한편, AI를 활용한 도구를 통해 일부 정형화된 제작 업무의 비용이 절감되고 있으며, 이에 따라 서비스 제공업체가 기본 업무의 가격을 책정하는 방식이나 프리미엄 업무와의 차별화를 꾀하는 방식에 변화가 생기고 있습니다.

비디오 콘텐츠 마케팅 서비스 시장에서 애니메이션 및 모션 그래픽스는 2031년까지 연평균 성장률(CAGR) 16.12%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 서비스 유형이 될 전망입니다. 애니메이션을 활용한 해설 영상이나 제품 비주얼은 SaaS, 헬스케어 및 기타 규제 대상 분야에서 복잡한 실사 촬영에 의존하지 않고도 정보를 명확하게 전달하는 데 도움이 되기 때문에 수요가 증가하고 있습니다. 또한, 구매자가 일회성 프로젝트가 아닌 상시 이용형 서비스 계약으로 전환함에 따라, 전략 및 컨설팅, 컨텐츠 아이디어 창출 및 대본 작성, 동영상 SEO, 배포 및 홍보 분야도 확대되고 있습니다. 이러한 변화는 비디오 콘텐츠 마케팅 서비스 업계에서 단순한 창작물 판매가 아닌, 제작과 검색 노출도 향상, 재사용, 캠페인 관리를 결합한 서비스 제공업체가 높이 평가받고 있음을 보여줍니다.

2025년, 비디오 콘텐츠 마케팅 서비스 시장에서 브랜드 스토리텔링 및 홍보 동영상은 29.56%의 점유율을 차지하며 가장 큰 동영상 장르가 되었습니다. 이러한 지속력은 커넥티드 TV, 유튜브, 프로그래매틱 동영상 광고 등에서 브랜드 자산에 대한 기업의 지속적인 투자에 힘입은 것입니다. 이 형식은 긴 구매 주기를 통해 브랜드 정체성을 표현하고 브랜드 인지도 구축이라는 주요 역할을 담당하고 있기 때문에 여전히 중요한 위치를 차지하고 있습니다. 덴츠는 2025년에 숏폼을 포함한 디지털 동영상의 경우, 주의 집중의 질이 최적화된다면 선형 TV에 필적하는 수년에 걸친 브랜드 구축 효과를 가져올 수 있다고 보고했습니다.

비디오 콘텐츠 마케팅 서비스 시장에서 해설 동영상은 2031년까지 연평균 성장률(CAGR) 15.89%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 동영상 장르가 될 전망입니다. 성장이 가장 두드러지는 분야는 기업이 복잡한 제품 컨셉을 영업, 마케팅, 고객 성공 각 분야에서 활용할 수 있는 단순한 자산으로 간소화해야 하는 분야입니다. 제품 데모 동영상이나 튜토리얼 형식도 온보딩 지원, 지원 서비스에 대한 의존도 감소, 제품 보급 촉진을 위해 확대되고 있습니다. 이러한 구성은 비디오 콘텐츠 마케팅 서비스 시장이 장기적인 브랜드 스토리텔링과 구매자의 실질적인 의문을 해결해 주는 실용성 높은 형식의 균형을 맞추고 있음을 보여줍니다.

지역별 분석

지역별로 보면, 2025년에는 북미가 매출 점유율의 34.56%를 차지했으나, 아시아태평양은 지역별 중 가장 높은 연평균 성장률(CAGR)인 16.52%를 나타낼 것으로 전망됩니다. 2025년에도 북미는 비디오 콘텐츠 마케팅 서비스 시장에서 여전히 가장 규모가 큰 지역 부문으로 자리매김했습니다. 이 지역은 기업들의 넉넉한 마케팅 예산, IT 및 SaaS 구매자들의 강력한 수요, 그리고 대규모 컨텐츠 제작 사업을 전개하는 대형 지주회사 네트워크의 존재 등 여러 이점을 누리고 있습니다. 옴니콤은 2025년 11월 인터퍼블릭 인수를 완료함으로써 세계 유수의 마케팅 및 영업 기업을 탄생시켰을 뿐만 아니라, 기업 고객을 대상으로 한 대규모 관리형 동영상 제작 역량을 확대했습니다. 미국은 여전히 지역 수요의 대부분을 차지하고 있지만, 캐나다에서는 B2B 기술 동영상 서비스 부문에서 견조한 성장세를 보였습니다. 또한, 미국 브랜드 활동을 지원하는 니어쇼어 제작 역량이 확대됨에 따라 멕시코의 중요성도 커졌습니다.

아시아태평양은 비디오 콘텐츠 마케팅 서비스 시장에서 가장 빠르게 성장하고 있는 지역 부문입니다. 일본의 디지털 동영상 광고 시장은 2025년에 1조 275억 엔(67억 6,000만 달러)을 넘어선 것으로 평가되었으며, CARTA 홀딩스, 덴츠, 덴츠 디지털, 세프테니는 2026년에는 1조 1,783억 엔(78억 6,000만 달러)에 달할 것으로 예측했습니다. 사이버 에이전트의 보고서에 따르면, 일본 국내 동영상 광고 시장 전체 규모는 2025년에 8,855억 엔(58억 3,000만 달러)에 달한 것으로 평가되었으며, 2026년에는 1조 437억 엔(69억 6,000만 달러)에 이를 것으로 전망하고 있습니다. 한편, 세로형 동영상 광고는 2,049억 엔(13억 5,000만 달러)으로 성장하여, 스마트폰용 동영상 광고의 29.1%를 차지했습니다. 중국, 인도, 한국, 호주에서도 숏폼 영상, 라이브 커머스, 다국어 현지화에 대한 수요가 확대되고 있으며, 이는 성장을 뒷받침하고 있습니다.

유럽에서는 독일, 영국, 프랑스를 필두로 비디오 콘텐츠 마케팅 서비스 시장이 꾸준한 성장세를 보였습니다. 이 국가들에서는 자동차, 소비재, 금융 서비스 분야의 광고주들이 프리미엄 브랜드 동영상에 대한 투자를 지속하고 있습니다. 영국은 브랜드 스토리텔링과 애니메이션 제작의 중요한 거점으로 자리매김하고 있지만, 2026년 EU AI법 제50조의 시행이 다가옴에 따라 유럽의 마케터들은 AI 생성 동영상에 대한 공개와 관련해 더욱 엄격한 감시를 받게 되었습니다. 남미는 브라질과 아르헨티나를 필두로 여전히 신흥 기회 시장이며, 수요는 주로 소비재, 소매, 소셜 커머스 캠페인과 관련이 있었습니다. 중동 및 아프리카은 아직 발전의 초기 단계에 머물러 있지만, UAE, 사우디아라비아, 남아프리카공화국, 나이지리아, 이집트에서는 모바일 우선 동영상 시청 및 컨텐츠에 대한 투자가 증가함에 따라 광고주들의 관심이 계속해서 높아지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the video content marketing services market size was valued at USD 11.28 billion in 2025 and estimated to grow from USD 12.88 billion in 2026 to reach USD 25.18 billion by 2031, at a CAGR of 14.35% during the forecast period (2026-2031).

This report is Segmented by Service Type (Strategy and Consulting, Content Ideation and Scripting, and More), Video Type (Explainer Videos, Tutorial and How-To Videos, and More), Video Size (Short-Form Videos, and Long-Form Videos), End-User Industry (Retail and E-Commerce, Consumer Goods and Beauty, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Video Content Marketing Services Market Trends and Insights

Rising Short-Form Video Budget Reallocation

Short-form video has moved from a supporting tactic to the center of social and performance planning in the video content marketing services market. Wistia reported that 57% of marketing budgets globally included a dedicated short-form video line item in 2026, and videos under 60 seconds generated 2.5x more engagement per impression than other content formats.This shift is raising outsourced demand because platform-native short-form programs need repeated edits, multiple aspect ratios, and frequent refresh cycles that many internal teams cannot sustain at scale. The IAB stated that social video spending in the United States rose 13% in 2026, which confirms the pace of budget movement toward formats that rely on continuous managed execution. As brands create 4 to 6 platform-specific cuts from one source asset, providers that can version, optimize, and distribute content efficiently are capturing more recurring work in the video content marketing services market.

Growing Enterprise Demand for AI-Assisted Production and Versioning

Enterprise buyers are using AI-assisted workflows in the video content marketing services market to expand output without matching headcount growth. Goldcast and Redpoint found that 89% of B2B marketers and 94% of C-suite executives viewed video as important to strategy in 2025, and nearly 75% were increasing video production budgets. Organizations using advanced AI video strategies were 4.5 times more likely to increase video creation output, and 77% of CIOs said they were willing to pay a premium for AI-enhanced video production solutions. This demand is rewarding service providers that pair AI generation with approval workflows, brand controls, and output quality checks rather than selling automation alone. The result is a market environment where enterprise contracts increasingly value speed, versioning, and governance together.

Persistent ROI Attribution Gaps Across Walled Gardens

Persistent ROI attribution gaps remain a near-term brake on spending in the video content marketing services market. Large platforms still measure exposure and conversion through separate systems, which lets multiple channels claim credit for the same sale and complicates cross-channel evaluation. That makes it harder for agencies and service providers to prove the full value of upper-funnel video to finance and procurement teams. In practice, the problem reduces confidence in outcome-based pricing and can keep contract sizes below what content volume alone would justify. Providers with stronger analytics, testing frameworks, and measurement governance are better positioned to defend margins as clients scrutinize ROI more closely.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Creator-Led And Employee-Led Video Campaigns

- Rising Adoption of Video for B2B Education, Product Demos, and Webinar Repurposing

- High-Volume Creative Refresh Requirements Raising Delivery Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Video production accounted for 34.22% of the video content marketing services market size in 2025, which kept it as the largest service category. That position is structural because strategy, SEO, distribution, and promotional work all depend on production output as their starting asset. The segment continued to attract enterprise, agency, and direct-brand spending because live capture, editing, and post-production remain difficult to remove from commercial video programs. At the same time, AI-assisted tools are reducing the cost of some routine production tasks, which is changing how providers price base execution and differentiate premium work.

Animation and motion graphics is projected to grow at 16.12% CAGR through 2031 in the video content marketing services market, making it the fastest-growing service type. Demand is rising because animated explainers and product visuals help SaaS, healthcare, and other regulated categories communicate clearly without relying on complex live-action shoots. Strategy and consulting, content ideation and scripting, video SEO, and distribution and promotion are also expanding as buyers move toward always-on service contracts instead of isolated projects. This shift shows that the video content marketing services industry is rewarding providers that combine production with discoverability, repurposing, and campaign management rather than selling creative output alone.

Branded storytelling and promotional videos represented 29.56% share in the video content marketing services market in 2025, which made them the largest video type. Their staying power comes from continued enterprise spending on brand equity across connected TV, YouTube, and programmatic video placements. This format remains important because it carries the main burden of expressing brand identity and building recall across long buying cycles. Dentsu reported in 2025 that digital video, including short-form, could deliver multi-year brand-building effects comparable to linear TV when attention quality was optimized.

Explainer videos are projected to grow at 15.89% CAGR through 2031 in the video content marketing services market, making them the fastest-growing video type. Growth is strongest where companies need to reduce complex product ideas into simple assets that can work across sales, marketing, and customer success. Product demonstration videos and tutorial formats are also expanding because they support onboarding, support deflection, and product adoption. This mix shows that the video content marketing services market is balancing long-term brand storytelling with high-utility formats that answer practical buyer questions.

Complete Report Scope:

- By Service Type

- Strategy and Consulting

- Content Ideation and Scripting

- Video Production

- Animation and Motion Graphics

- Video SEO and Metadata Optimization

- Distribution and Promotion

- Other Service Types

- By Video Type

- Explainer Videos

- Product Demonstration Videos

- Tutorial and How-To Videos

- Branded Storytelling and Promotional Videos

- Other Video Types (Educational and Webinar, etc.)

- By Video Size

- Short-Form Videos

- Long-Form Videos

- By End-User Industry

- Retail and E-commerce

- Consumer Goods and Beauty

- Media and Entertainment

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Other End-User Industries (Education, Travel and Hospitality, Industrial, Automotive)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

By geography, North America held 34.56% revenue share in 2025, yet Asia-Pacific is on track for the highest regional CAGR of 16.52%. North America remained the largest regional segment in the video content marketing services market in 2025. The region benefits from dense enterprise marketing budgets, strong demand from IT and SaaS buyers, and the presence of major holding company networks with large content production operations. Omnicom completed its acquisition of Interpublic in November 2025, creating the world's leading marketing and sales company and expanding large-scale managed video capacity for enterprise clients. The United States continued to account for most regional demand, while Canada showed solid momentum in B2B technology video services. Mexico also gained relevance as nearshore production capacity expanded in support of U.S. brand work.

Asia-Pacific is the fastest-growing regional segment in the video content marketing services market. Japan's digital video advertising market exceeded JPY 1.0275 trillion (USD 6.76 billion) in 2025, and CARTA Holdings, Dentsu, Dentsu Digital, and Septeni forecast it would reach JPY 1.1783 trillion (USD 7.86 billion) in 2026. CyberAgent reported that Japan's broader domestic video advertising market stood at JPY 885.5 billion (USD 5.83 billion) in 2025 and would rise to JPY 1.0437 trillion (USD 6.96 billion) in 2026, while vertical video advertising grew to JPY 204.9 billion (USD 1.35 billion) and represented 29.1% of smartphone video advertising. China, India, South Korea, and Australia are also supporting growth as short video, live commerce, and multilingual localization demand expand across the region.

Europe showed steady growth in the video content marketing services market, led by Germany, the United Kingdom, and France, where automotive, consumer goods, and financial services buyers continue to invest in premium brand video. The United Kingdom remained an important center for branded storytelling and animation work, while European marketers also faced tighter scrutiny around AI-generated video disclosure as Article 50 of the EU AI Act moved toward enforcement in 2026. South America remained an emerging opportunity led by Brazil and Argentina, with demand tied mainly to consumer goods, retail, and social commerce campaigns. The Middle East and Africa stayed earlier in development, but the UAE, Saudi Arabia, South Africa, Nigeria, and Egypt continued to attract more advertiser interest as mobile-first video consumption and content investment increased.

- WPP plc

- Publicis Groupe S.A.

- Omnicom Group Inc.

- Dentsu Group Inc.

- Interpublic Group of Companies, Inc.

- Accenture plc

- S4 Capital plc

- Adobe Inc.

- Brightcove Inc.

- Kaltura, Inc.

- Vimeo.com, Inc.

- Vidyard Inc.

- Wistia, Inc.

- Lemonlight Media, Inc.

- Wyzowl Limited

- Demo Duck, LLC

- Epipheo, Inc.

- Yum Yum Videos LLC

- VeracityColab, LLC

- webdew, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Short-Form Video Budget Reallocation

- 4.2.2 Growing Enterprise Demand for AI-Assisted Production and Versioning

- 4.2.3 Expansion of Creator-Led and Employee-Led Video Campaigns

- 4.2.4 Rising Adoption of Video for B2B Education, Product Demos, and Webinar Repurposing

- 4.2.5 Growth of Shoppable Video and Retail Media Video Workflows

- 4.2.6 Acceleration of AI Dubbing and Multilingual Localization for Mid-Market Expansion

- 4.3 Market Restraints

- 4.3.1 Persistent ROI Attribution Gaps Across Walled Gardens

- 4.3.2 High-Volume Creative Refresh Requirements Raising Delivery Complexity

- 4.3.3 Tightening AI Disclosure and Synthetic Media Compliance Rules

- 4.3.4 Platform Algorithm Volatility Reducing Predictability of Organic Reach

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Strategy and Consulting

- 5.1.2 Content Ideation and Scripting

- 5.1.3 Video Production

- 5.1.4 Animation and Motion Graphics

- 5.1.5 Video SEO and Metadata Optimization

- 5.1.6 Distribution and Promotion

- 5.1.7 Other Service Types

- 5.2 By Video Type

- 5.2.1 Explainer Videos

- 5.2.2 Product Demonstration Videos

- 5.2.3 Tutorial and How-To Videos

- 5.2.4 Branded Storytelling and Promotional Videos

- 5.2.5 Other Video Types (Educational and Webinar, etc.)

- 5.3 By Video Size

- 5.3.1 Short-Form Videos

- 5.3.2 Long-Form Videos

- 5.4 By End-User Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 Consumer Goods and Beauty

- 5.4.3 Media and Entertainment

- 5.4.4 IT and Telecom

- 5.4.5 BFSI

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Other End-User Industries (Education, Travel and Hospitality, Industrial, Automotive)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Qatar

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 WPP plc

- 6.4.2 Publicis Groupe S.A.

- 6.4.3 Omnicom Group Inc.

- 6.4.4 Dentsu Group Inc.

- 6.4.5 Interpublic Group of Companies, Inc.

- 6.4.6 Accenture plc

- 6.4.7 S4 Capital plc

- 6.4.8 Adobe Inc.

- 6.4.9 Brightcove Inc.

- 6.4.10 Kaltura, Inc.

- 6.4.11 Vimeo.com, Inc.

- 6.4.12 Vidyard Inc.

- 6.4.13 Wistia, Inc.

- 6.4.14 Lemonlight Media, Inc.

- 6.4.15 Wyzowl Limited

- 6.4.16 Demo Duck, LLC

- 6.4.17 Epipheo, Inc.

- 6.4.18 Yum Yum Videos LLC

- 6.4.19 VeracityColab, LLC

- 6.4.20 webdew, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment