|

시장보고서

상품코드

2072684

동남아시아의 LED 칩 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Southeast Asia LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

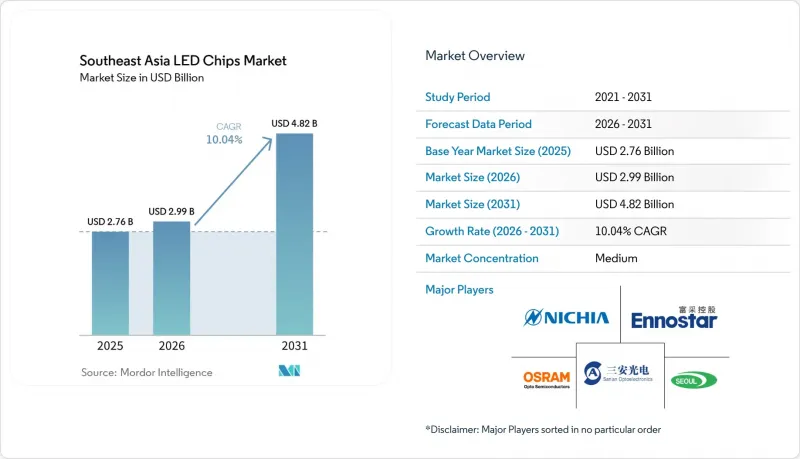

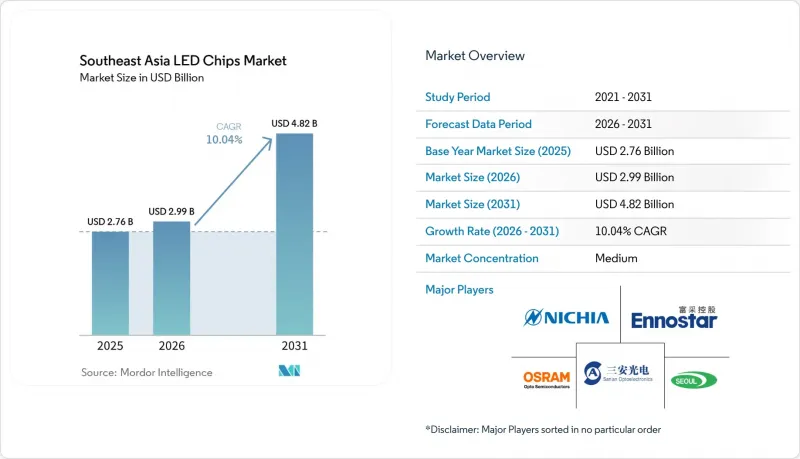

Mordor Intelligence에 의하면, 동남아시아의 LED 칩 시장 규모는 2025년에 27억 6,000만 달러로 평가되었고, 2026년 29억 9,000만 달러로 추정되고, 2031년까지 48억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 예측 기간 CAGR은 10.04%를 나타낼 전망입니다.

본 보고서는 LED 칩 기술별(기존 LED, Mini-LED, Micro-LED), 반도체 소재별(GaN/InGaN, AlGaInP, 기타 반도체 소재), 용도별(일반 조명, 자동차, 백라이트 및 디스플레이, 소비자용 전자기기, 산업용 및 특수 조명) 및 국가별로 분류되어 있습니다. 시장 전망은 금액 기준(백만 달러)으로 제시되어 있습니다.

동남아시아의 LED 칩 시장 동향 및 인사이트

에너지 절약형 조명에 대한 정부의 인센티브 확대

정책에 뒷받침된 효율화 노력은 동남아시아의 LED 칩 시장에서 여전히 가장 뚜렷한 단기 수요 견인 요인으로 작용하고 있습니다. 싱가포르의 '에너지 효율화 지원금'은 2026년 4월부터 2027년 3월까지 연장된 후, 2028년 3월까지 모든 부문으로 확대되어, 사전 승인을 받은 LED 조명 기기에 투자하는 중소기업에 대해 최대 70%의 지원이 이루어지고 있습니다. 이 프로그램이 중요한 이유는 구매 비용을 절감할 뿐만 아니라, 대상 조명 시스템에 대해 더 높은 기술 기준을 설정함으로써 고성능 칩에 대한 수요를 높이고 있다는 점에 있습니다. 지역 차원에서는 아세안 에너지 센터(ASEAN Energy Centre)가 비방향성 LED 램프에 대해 1와트당 80루멘이라는 조화로운 MEPS(최저 에너지 성능 기준) 도입을 추진하고 있으며, 이에 따라 회원국들은 보다 일관된 효율 기준으로 전환해 나가고 있습니다. 이러한 규제가 더욱 일관되게 시행됨에 따라, 교체 주기는 단순한 램프 교체에서 더 우수한 칩 구성을 갖춘 고효율 시스템으로의 전환으로 바뀌고 있습니다. 이러한 추세에 따라 동남아시아의 LED 칩 시장은 보다 지속 가능한 판매량 기반을 확보하게 될 것입니다. 왜냐하면 정책에 의한 수요는 소비자의 변덕스러운 전자기기 지출에 비해 단기적인 소비 주기에 대한 의존도가 낮기 때문입니다.

자동차용 LED 헤드램프의 채택 확대

자동차 분야는 동남아시아의 LED 칩 시장에서 가장 사양 주도형 수요원으로 부상하고 있습니다. 이 부문은 예측 기간 동안 이미 가장 빠르게 성장하고 있는 용도이며, 그 이유는 단순히 LED 교체에 그치지 않고, 더 높은 밀도와 정밀도를 갖춘 칩 어레이가 필요한 적응형 조명 및 픽셀화된 조명 시스템으로의 전환에 있습니다. ams OSRAM의 2026년 제품 및 전략에 관한 최신 정보에 따르면, 자동차용 조명 플랫폼은 이 회사의 디지털 포토닉스 전환 과정에서 특히 픽셀화된 조명 및 지능형 조명 아키텍처 분야에서 핵심 성장 영역으로 자리매김하고 있습니다. 이 회사가 2026년 3월에 EVIYOS 플랫폼을 기반으로 한 초고효율 마이크로 LED 어레이를 출시한 것도, 자동차 등급 칩 개발이 인접한 고부가가치 용도로 파급되고 있음을 보여주며, 이 설계 경로의 성숙도를 입증하고 있습니다. 자동차 제조업체들이 주류 플랫폼에 더욱 정교한 헤드램프 기능을 도입함에 따라, 수요는 열 안정성, 빔 정밀도 및 장기 인증 주기를 충족하는 칩으로 이동하고 있습니다. 이러한 변화로 인해 진입 장벽이 높아지면서, 동남아시아의 LED 칩 시장에서 표준 조명 분야보다 자동차 분야가 더 큰 수익원이 되고 있습니다.

에피택셜 웨이퍼 제조에 필요한 막대한 설비 투자

자본 집약성은 동남아시아 LED 칩 시장에서 현지 공급을 더욱 확대하는 데 있어 여전히 주요 장애물로 남아 있습니다. Mordor Intelligence가 실시한 아시아태평양의 LED 에피택시 장비에 관한 조사에 따르면, 계측, 배기가스 처리, 웨이퍼 핸들링을 포함할 경우, 첨단 200mm 배치형 MOCVD 장비 1대당 여전히 수백만 달러 규모의 투자가 필요한 것으로 나타났습니다. 아세안 시장에 새로 진출하는 기업들에게 있어 이러한 비용 부담은 큰 장벽이 됩니다. 왜냐하면 해당 지역 수요 전망이 대만, 한국, 중국만큼 명확하지 않기 때문입니다. 인센티브 제도를 통해 초기 비용의 일부가 상쇄된다 하더라도, 팹은 여전히 장기간에 걸친 감가상각 주기, 서비스 계약 및 소모품 비용을 부담해야 합니다. 이 때문에 그린필드 투자는 주춤한 상태이며, 에피택시 생산 능력은 자금력이 풍부하고 고객과 확고한 관계를 구축하고 있는 기존 기업에 계속 집중되어 있습니다. 또한, 이는 동남아시아의 LED 칩 시장에서 조립, 패키징 및 하류 설계 분야에서는 강력한 성장이 예상되는 반면, 업스트림 웨이퍼 제조 분야에서는 비슷한 수준의 성장세가 나타나지 않을 것임을 의미합니다. 그 결과, 공급망은 지속적으로 개선되고 있지만, 핵심인 칩 제조 능력에 대해서는 여전히 제한된 지역의 주요 기업들에 크게 의존하고 있는 상황입니다.

부문별 분석

2025년에는 기존 LED가 매출의 82.34%를 차지했으며, 동남아시아 LED 칩 시장에서 확고한 중심적 지위를 유지했습니다. 이러한 위상은 상업용 및 주거용 조명 수요의 강세를 반영한 것이며, 대규모 교체 프로그램에서는 성숙된 형광체 변환 플랫폼이 여전히 비용, 신뢰성 및 발광 효율 면에서 최적의 균형을 제공합니다. 또한, 이 부문은 아세안 전역에서 효율 기준의 적용이 강화된 데서도 혜택을 보았습니다. 이는 업그레이드가 이미 조달 및 규정 준수 요건을 충족하는 검증된 제품에서 시작되는 경우가 많았기 때문입니다. 실질적으로는 동남아시아 LED 칩 시장의 기술 구성이 지속적으로 변화하고 있었음에도 불구하고, 이로 인해 기존 제품의 판매량에 대한 견고한 하한선이 확보되었습니다.

미니 LED는 동남아시아의 LED 칩 산업에 있어 전략적으로 중요한 과도기적 역할을 담당하고 있습니다. 이미 확립된 GaN 공급망과 매우 가까운 위치에 있기 때문에 기존의 제조 노하우를 활용해 규모를 확대할 수 있을 뿐만 아니라, 디스플레이 백라이트나 프리미엄 조명 시스템과 같이 더 높은 이익률을 기대할 수 있는 분야로 진출하는 것도 가능해집니다. 마이크로 LED는 2031년까지 연평균 성장률(CAGR)이 12.04%에 달하는 가장 빠르게 성장하고 있는 기술 하위 부문으로, 이는 동남아시아의 LED 칩 시장이 이미 기존 조명의 범위를 넘어 발전하고 있음을 보여줍니다. 특히 자동차 및 첨단 디스플레이 분야의 이용 사례에서 화소 제어, 휘도 밀도, 소형 광학 설계를 중시하는 용도에서 가장 큰 수요가 발생하고 있습니다. ams OSRAM의 기업 로드맵에 따르면, 당초 지능형 자동차 조명용으로 개발된 마이크로 LED 플랫폼이 현재는 인접한 포토닉스 분야로 확대되고 있으며, 이는 동남아시아 LED 칩 시장에서 설명되고 있는 보다 광범위한 전환 경로를 뒷받침하는 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the southeast asia LED chips market size was valued at USD 2.76 billion in 2025 and is estimated to grow from USD 2.99 billion in 2026 to reach USD 4.82 billion by 2031, at a CAGR of 10.04% during the forecast period 2026-2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN / InGaN, Algainp, and Other Semiconductor Materials), Application (General Lighting, Automotive, Backlighting / Displays, Consumer Electronics, and Industrial / Specialty Lighting), and Country. The Market Forecasts are Provided in Terms of Value (USD Million).

Southeast Asia LED Chips Market Trends and Insights

Expanding Government Incentives for Energy-Efficient Lighting

Policy-backed efficiency upgrades remain the clearest near-term demand driver for the Southeast Asia LED chips market. Singapore's Energy Efficiency Grant was extended from April 2026 to March 2027 and then expanded to all sectors through March 2028, with support of up to 70% for SMEs that invest in pre-approved LED lighting equipment.That program matters not only because it lowers purchase cost, but also because it sets a higher technology floor for qualifying lighting systems, which lifts demand for better-performing chips. At the regional level, the ASEAN Center for Energy has been pushing harmonized MEPS for non-directional LED lamps at 80 lumens per watt, which is helping member states move toward a more consistent efficiency baseline.As those rules are enforced more consistently, replacement cycles are shifting from simple lamp swaps toward higher-efficacy systems with a better chip mix. That dynamic gives the Southeast Asia LED chips market a more durable volume base because policy demand is less dependent on short consumer cycles than discretionary electronics spending.

Growth in Automotive LED Headlamp Adoption

Automotive is becoming the most specification-driven demand center in the Southeast Asia LED chips market. The segment is already the fastest-growing application in the forecast period, and the reason is not just LED replacement, but the move toward adaptive and pixelated lighting systems that require denser and more precise chip arrays. ams OSRAM's 2026 product and strategy updates show that automotive lighting platforms are now being treated as a core growth area within its digital photonics transition, especially in pixelated and intelligent lighting architectures. The company's March 2026 launch of an ultra-efficient micro-LED array built on its EVIYOS platform also shows how automotive-grade chip development is spilling into adjacent high-value uses, which confirms the maturity of this design path. As vehicle makers push more advanced headlamp functions into mainstream platforms, demand is shifting toward chips that support thermal stability, beam precision, and long qualification cycles. That change raises entry barriers and gives the Southeast Asia LED chips market a stronger profit pool in automotive than in standard illumination.

High Capital Expenditure for Epitaxial Wafer Fabrication

Capital intensity remains a major barrier to deeper local supply expansion in the Southeast Asia LED chips market. Mordor Intelligence's coverage of Asia-Pacific LED epitaxy equipment shows that advanced 200 mm batch MOCVD tools still require multi-million-dollar investment per unit when metrology, abatement, and wafer handling are included. That cost burden is difficult for new entrants in ASEAN markets because demand visibility is not yet as deep as it is in Taiwan, South Korea, or China. Even when incentive programs offset part of the upfront cost, fabs still need to absorb long depreciation cycles, service contracts, and consumable expenses. This slows greenfield investment and keeps epitaxial capacity concentrated among well-funded incumbents with established customer relationships. It also means the Southeast Asia LED chips market can grow strongly in assembly, packaging, and downstream design without seeing the same pace of expansion in upstream wafer fabrication. The result is a supply chain that keeps improving, but still depends heavily on a limited group of regional leaders for core chip-making capacity.

Other drivers and restraints analyzed in the detailed report include:

- Rising Penetration of Smart Homes and IoT-Enabled Lighting

- Accelerating Urban Infrastructure Projects Across ASEAN Capitals

- Price Volatility in Key Raw Materials Such as Gallium and Indium

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional LEDs accounted for 82.34% of revenue in 2025, which kept them firmly at the center of the Southeast Asia LED chips market. That position reflected the strength of commercial and residential lighting demand, where mature phosphor-converted platforms still offer the best mix of cost, reliability, and efficacy for large replacement programs. The segment also benefited from stricter efficiency enforcement across ASEAN, because upgrades often began with established products that already met procurement and compliance requirements. In practical terms, that gave conventional products a strong volume floor even as the technology mix in the Southeast Asia LED chips market continued to shift.

Mini-LED occupies a transitional role that is strategically important for the Southeast Asia LED chips industry. It sits close enough to established GaN supply chains to scale through existing manufacturing know-how, but it also opens access to better-margin uses in display backlighting and premium lighting systems. Micro-LED is the fastest-growing technology sub-segment, with a 12.04% CAGR through 2031, which shows that the Southeast Asia LED chips market is already moving beyond the limits of conventional illumination. The strongest pull is coming from applications that value pixel control, brightness density, and compact optical design, especially in automotive and advanced display use cases. Company roadmaps from ams OSRAM show that micro-LED platforms first developed for intelligent automotive lighting are now being carried into adjacent photonics uses, which supports the wider migration path described in the Southeast Asia LED chips market.

Complete Report Scope:

- By LED Chip Technology

- Conventional LEDs

- Mini-LED

- Micro-LED

- By Semiconductor Material

- GaN / InGaN

- AlGAInP

- Other Semiconductor Materials

- By Application

- General Lighting

- Automotive

- Backlighting / Displays

- Consumer Electronics

- Industrial / Specialty Lighting

- By Country

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of Southeast Asia

List of Companies Covered in this Report:

- Nichia Corporation

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Epistar Corporation

- Cree LED, Inc.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- HC SemITek Corporation

- Everlight Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Lumileds Holding B.V.

- Bridgelux, Inc.

- Kingbright Electronic Co., Ltd.

- Opto Tech Corporation

- Lextar Electronics Corporation

- Dominant Opto Technologies Sdn. Bhd.

- NationStar Optoelectronics Co., Ltd.

- AIXTRON SE

- Coherent Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Government Incentives for Energy-Efficient Lighting

- 4.2.2 Rising Penetration of Smart Homes and IoT-Enabled Lighting

- 4.2.3 Accelerating Urban Infrastructure Projects Across ASEAN Capitals

- 4.2.4 Growth in Automotive LED Headlamp Adoption

- 4.2.5 Localization of Mini-LED Backlight Supply Chains

- 4.2.6 Emerging Micro-LED Pilot Production in Singapore and Malaysia

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for Epitaxial Wafer Fabrication

- 4.3.2 Price Volatility in Key Raw Materials such as Gallium and Indium

- 4.3.3 Supply-Demand Imbalance for Trained Optoelectronics Workforce

- 4.3.4 Environmental Compliance Costs for Wastewater and Chemical Disposal

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

- 5.4 By Country

- 5.4.1 Indonesia

- 5.4.2 Malaysia

- 5.4.3 Philippines

- 5.4.4 Singapore

- 5.4.5 Thailand

- 5.4.6 Vietnam

- 5.4.7 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Osram Opto Semiconductors GmbH

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Epistar Corporation

- 6.4.5 Cree LED, Inc.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 San'an Optoelectronics Co., Ltd.

- 6.4.9 HC SemiTek Corporation

- 6.4.10 Everlight Electronics Co., Ltd.

- 6.4.11 Toyoda Gosei Co., Ltd.

- 6.4.12 Lumileds Holding B.V.

- 6.4.13 Bridgelux, Inc.

- 6.4.14 Kingbright Electronic Co., Ltd.

- 6.4.15 Opto Tech Corporation

- 6.4.16 Lextar Electronics Corporation

- 6.4.17 Dominant Opto Technologies Sdn. Bhd.

- 6.4.18 NationStar Optoelectronics Co., Ltd.

- 6.4.19 AIXTRON SE

- 6.4.20 Coherent Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment