|

시장보고서

상품코드

2072692

미국의 자궁근종 치료 기기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Uterine Fibroids Treatment Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

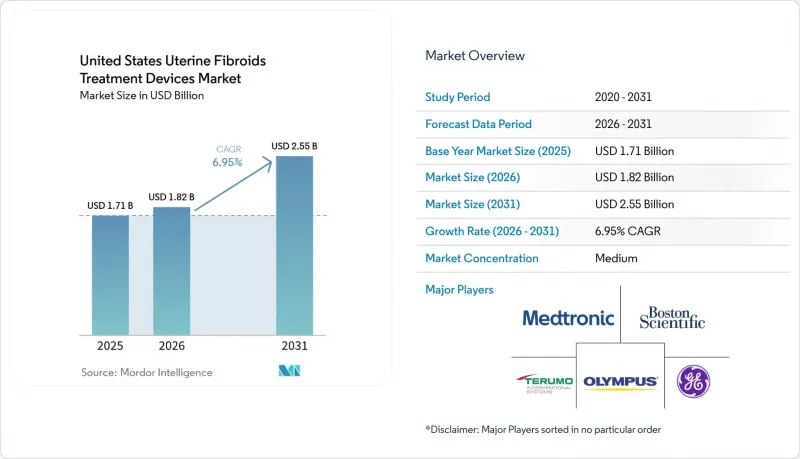

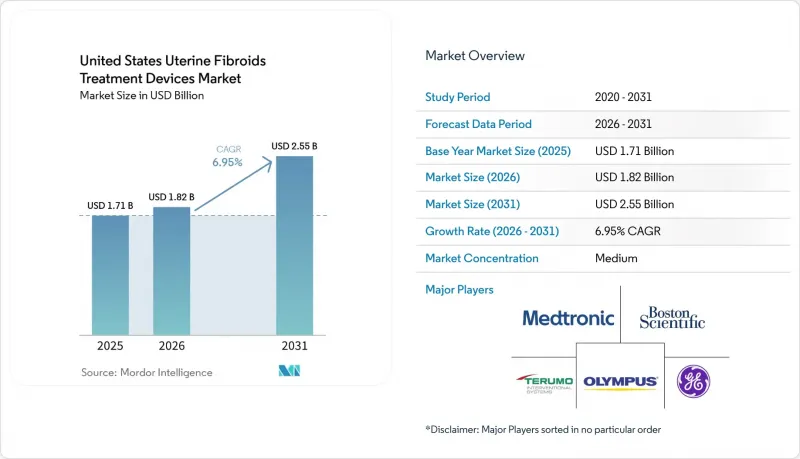

Mordor Intelligence에 의하면, 미국의 자궁근종 치료 기기 시장 규모는 2025년 17억 1,000만 달러로 평가되었고, 2026년 18억 2,000만 달러로 추정되고, 2031년까지 25억 5,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 6.95%를 나타낼 전망입니다.

본 보고서는 기술별(외과적, 복강경, 절제술, 색전술), 치료법별(침습적 치료, 저침습적 치료, 비침습적 치료) 및 최종 사용자별(병원, 외래수술센터(ASC), 진료소형 산부인과 클리닉, 중재적 방사선학 센터)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 자궁근종 치료 기기 시장 동향 및 인사이트

자궁 보존 치료의 선호도

자궁 보존 치료에 대한 환자의 선호도는 미국 자궁근종 치료 기기 시장 전반의 소개 동향에 변화를 가져오고 있으며, 특히 자궁 적출술을 고려하기 전에 여러 치료 옵션을 제공하게 된 의료 시스템에서 두드러지게 나타납니다. 2025년 『JAMA Network Open』에 게재된 연구에 따르면, 자궁근종 치료 내원 건수 중 자궁 적출술이 여전히 73.4%를 차지한 반면, 자궁동맥색전술(UFE)은 고작 3.5%에 그치고 있어, 의료기기 주도형 치료법으로의 대체 여지가 아직 크다는 점이 밝혀졌습니다. 이러한 수요 양상은 자궁을 보존한 채 증상을 관리하고자 하는 가임기 여성들 사이에서 더욱 두드러지며, 자궁근종이 더 이른 시기에, 그리고 더 심각한 상태로 발병하는 집단에서는 그 중요성이 더욱 커집니다. 미국의 자궁근종 치료 기기 시장에서 이러한 경향은 특정 치료법만을 우대하는 것은 아닙니다. 왜냐하면 RFA, 색전술, 집속 초음파에 대한 관심이 동시에 높아지고 있기 때문입니다. 그 결과, 제조업체 입장에서는 동일한 치료 과정 내에서 서로 다른 환자 프로파일과 의료 환경에 대응할 수 있는 보다 광범위한 사업 확장의 길이 열리고 있습니다.

복강경 RFA에 대한 보험 적용 범위 확대

보험 환급은 복강경 고주파 절제술(RFA)의 주요 상업적 장벽 중 하나였으나, 현재 보험 적용 범위 확대는 미국 자궁근종 치료 기기 시장의 가장 시급한 성장 동력 중 하나가 되고 있습니다. Medica가 발표한 지침에 따르면, 자궁근종에 대한 복강경 RFA가 대상에 포함되어 있으며, ACOG(미국 산부인과 학회)의 프랙티스 불레틴 228호 역시 의료 제공업체 및 보험사가 사용하는 임상 의사결정 프레임워크에서 이 시술을 계속해서 지지하고 있습니다. 보험 적용 범위가 확대됨에 따라, 더 많은 사례가 외래수술센터(ASC)나 진료소에서의 시술로 전환될 수 있게 되며, 이로 인해 절제술 도입에 따른 시스템적 장벽이 낮아지고, 미국의 자궁근종 치료 기기 시장의 상업적 영향력이 확대될 것입니다. 이러한 변화는 막대한 설비 투자가 필요한 대형 시스템에만 의존하는 것이 아니라, 소형 기기나 일회용 기구를 개발한 제조업체에게도 유리하게 작용합니다. CMS 요금표에 관한 규정과 지역별 보험 적용 절차가 여전히 시술의 경제성을 좌우하고 있기 때문에 비록 이미 임상적 근거가 확보된 경우라 하더라도 보험 급여의 실행은 단기적인 보급에 있어 여전히 핵심적인 과제로 남아 있습니다.

MRgFUS에 대한 불균등한 상환

MRgFUS는 미국 자궁근종 치료 기기 시장에서 여전히 임상적으로 중요한 위치를 차지하고 있지만, 보험사들은 관련 CPT 코드를 계속해서 '임상시험 중'으로 분류되고 있기 때문에 상업적인 보급은 여전히 제한적입니다. Cigna나 Blue Shield의 보험 정책, 그리고 이와 유사한 보험사들의 입장으로 인해, 치료 건수의 대부분은 대체 자금 조달 및 연구 경로가 보다 현실적인 대학 부속 병원에 집중되고 있습니다. FDA 승인과 광범위한 보험 적용 사이의 이러한 격차는 임상적 가치가 명확한 경우에도 시장 전환을 지연시키고 있습니다. 미국 자궁근종 치료 기기 시장에서 이는 비침습적 플랫폼이 기술적 우위를 광범위한 상업적 판매량으로 연결하지 못하고 있음을 의미합니다. 더 강력한 비용 대비 효과에 대한 근거가 광범위하게 인정받기 전까지는 MRgFUS는 광범위한 일상 진료보다는 특정 의료기관에서 더 중요한 위치를 차지하는 데 그칠 가능성이 높습니다.

부문별 분석

2025년, 미국 자궁근종 치료 기기 시장에서 외과적 시술은 31.23%의 점유율을 차지했으며, 매출 기준 최대 기술 부문으로서의 위상을 유지했습니다. 이 지위는 증상을 근본적으로 해소해 주며, 의료계에서도 널리 인정받고 있는 자궁적출술 및 근종적출술에 의해 지속적으로 뒷받침되고 있습니다. 2025년 『JAMA Network Open』의 분석에 따르면, 미국 전역의 자궁근종 치료 중 73.4%를 자궁적출술이 차지했으며, 이는 수술 건수가 여전히 치료 방식의 주류를 이루고 있는 이유를 보여줍니다. 광범위한 보험 적용 범위와 확립된 병원 업무 흐름 역시 미국 자궁근종 치료 기기 시장 전반에서 수술의 중요성을 유지하는 요인 중 하나입니다. 복강경 수술 기술은 도입 곡선상 외과 수술과 절제술의 중간에 위치하며, 외래 진료 시설에서의 다빈치 시스템 도입이 확대됨에 따라 로봇 보조 자궁근종 절제술이 더욱 확산되고 있습니다.

미국의 자궁근종 치료 기기 시장에서 절제술 기술 시장 규모는 2031년까지 연평균 성장률(CAGR) 7.41%로 확대될 것으로 예상되며, 가장 빠르게 성장하는 기술 그룹이 될 전망입니다. 이러한 성장은 Gynesonics 인수 이후 Hologic이 추진해 온 듀얼 플랫폼 RFA 전략과, 경자궁경부 및 복강경 시술 워크플로우에 대한 의료진의 수용도가 높아지고 있음을 반영합니다. Sonata의 피보탈 임상시험에서는 일상 활동으로 복귀하기까지의 중앙값이 2.2일인 것으로 보고되었으며, 이는 생활에 지장을 덜 주는 치료법을 선호하는 환자들의 의향과 일치합니다. MRgFUS 및 USgHIFU는 여전히 절제술 시장의 일부를 차지하고 있지만, 보험 급여 제한으로 인해 미국 자궁근종 치료 기기 시장에 대한 기여도는 여전히 제한적입니다. 색전술은 임상적으로 확립된 기법이며, Merit의 Embosphere에 관한 데이터는 소모품 중심의 포트폴리오 구성에서 의료진의 강력한 지지가 지속되고 있음을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the united states uterine fibroids treatment devices market size is projected to expand from USD 1.71 billion in 2025 and USD 1.82 billion in 2026 to USD 2.55 billion by 2031, registering a CAGR of 6.95% between 2026 to 2031.

This report is Segmented by Technology (Surgical, Laparoscopic, Ablation, and Embolization Techniques), Mode of Treatment (Invasive Treatment, Minimally Invasive Treatment, Non-Invasive Treatment), and End User (Hospitals, Ambulatory Surgical Centers, Office-Based Gynecology Clinics, Interventional Radiology Centers). The Market Forecasts are Provided in Terms of Value (USD).

United States Uterine Fibroids Treatment Devices Market Trends and Insights

Uterus-Preserving Treatment Preference

Patient preference for uterus-sparing care has changed referral behavior across the United States uterine fibroids treatment devices market, especially in health systems that now offer multiple procedural alternatives before hysterectomy is considered. A 2025 JAMA Network Open study showed that hysterectomy still represented 73.4% of fibroid treatment encounters, while UFE accounted for only 3.5%, which shows how much room remains for device-led treatment substitution. This demand pattern is stronger among reproductive-age women who want symptom control without losing the uterus, and it matters even more in populations where fibroids appear earlier and with greater severity. In the United States uterine fibroids treatment devices market, that preference does not benefit only one modality because it lifts interest in RFA, embolization, and focused ultrasound at the same time. The result is a broader expansion path for manufacturers that can fit different patient profiles and care settings inside the same treatment journey.

Payer Expansion for Lap-RFA

Reimbursement has been one of the main commercial barriers for laparoscopic radiofrequency ablation, so payer coverage gains are now one of the most immediate growth supports for the United States uterine fibroids treatment devices market. Medica's published policy covers laparoscopic RFA for uterine fibroids, and ACOG Practice Bulletin 228 continues to support the procedure in the clinical decision framework used by providers and payers. As coverage improves, more cases can move into ASC and office-based settings, which lowers system friction for ablation adoption and broadens the commercial reach of the United States uterine fibroids treatment devices market. This shift also favors manufacturers that built compact or single-use tools rather than relying only on large installed-capital systems. CMS fee schedule rules and local coverage processes continue to shape procedure economics, so reimbursement execution remains central to near-term adoption even when clinical support is already in place.

Uneven Reimbursement for MRgFUS

MRgFUS remains clinically relevant in the United States uterine fibroids treatment devices market, but commercial uptake is still limited because payers continue to classify the relevant CPT codes as investigational. Cigna, Blue Shield policies, and similar payer positions keep most volumes concentrated in academic centers where alternative funding or research pathways are more realistic. That gap between FDA approval and broad reimbursement slows market conversion even when the clinical value proposition is clear. In the United States uterine fibroids treatment devices market, this means non-invasive platforms have not translated their technology profile into wide commercial volume. Until a stronger cost-effectiveness case is accepted at scale, MRgFUS will likely remain more important in select centers than in broad routine care.

Other drivers and restraints analyzed in the detailed report include:

- Shift To Office and ASC Hysteroscopy Workflows

- Hologic Portfolio Expansion After Sonata Integration

- Fertility And Pregnancy Evidence Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surgical techniques held 31.23% of the United States uterine fibroids treatment devices market share in 2025, which kept surgery as the largest technology category by revenue. That position remained supported by hysterectomy and myomectomy, which continue to offer definitive symptom resolution and strong institutional familiarity. A 2025 JAMA Network Open analysis found that hysterectomy represented 73.4% of fibroid treatment encounters nationally, which shows why surgical volume still anchors the technology mix. Broad insurance coverage and well-established hospital workflows also helped preserve surgical relevance across the United States uterine fibroids treatment devices market. Laparoscopic Techniques stayed between surgery and ablation in the adoption curve, with robotic-assisted myomectomy gaining ground as da Vinci access expands across outpatient sites.

The United States uterine fibroids treatment devices market size for ablation techniques is projected to grow at a 7.41% CAGR through 2031, making it the fastest-growing technology group. This growth reflects Hologic's dual-platform RFA position after the Gynesonics integration and rising physician comfort with transcervical and laparoscopic workflows. The Sonata pivotal study reported a 2.2-day median return to normal activity, which aligns with patient preference for lower-disruption treatment paths. MRgFUS and USgHIFU remain part of the ablation opportunity, but reimbursement limits still restrict their contribution to the United States uterine fibroids treatment devices market. Embolization Techniques remain clinically established, and Merit's Embosphere data continue to support strong physician loyalty in a consumable-driven part of the portfolio mix.

Complete Report Scope:

- By Technology

- Surgical Techniques

- Hysterectomy

- Myomectomy

- Laparoscopic Techniques

- Laparoscopic Myomectomy

- Myolysis

- Ablation Techniques

- Laparoscopic Radiofrequency Ablation

- Transcervical Radiofrequency Ablation

- MRI-guided Focused Ultrasound

- Ultrasound-guided High-intensity Focused Ultrasound

- Embolization Techniques

- Uterine Fibroid Embolization

- Embolic Microspheres

- PVA Particles

- Surgical Techniques

- By Mode of Treatment

- Invasive Treatment

- Open Surgery

- Robotic-assisted Surgery

- Minimally Invasive Treatment

- Laparoscopic Procedures

- Hysteroscopic Procedures

- Uterine Artery Embolization

- Non-invasive Treatment

- MR-guided Focused Ultrasound

- Ultrasound-guided High-intensity Focused Ultrasound

- Invasive Treatment

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Office-based Gynecology Clinics

- Interventional Radiology Centers

List of Companies Covered in this Report:

- Axora Medical, Inc.

- Boston Scientific

- Conmed

- Cook Group

- The Cooper Companies

- GE HealthCare Technologies Inc.

- Hologic

- INSIGHTEC Ltd.

- Intuitive Surgical, Inc.

- Johnson & Johnson MedTech

- Karl Storz

- Medtronic

- Merit Medical Systems

- Minerva Surgical

- Olympus

- Profound Medical

- Richard Wolf

- Siemens Healthineers

- Stryker

- Terumo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Uterus-Preserving Treatment Preference

- 4.2.2 Payer Expansion for Lap-RFA

- 4.2.3 Shift To Office and ASC Hysteroscopy Workflows

- 4.2.4 Hologic Portfolio Expansion After Sonata Integration

- 4.2.5 Transradial UFE Workflow Improvements

- 4.2.6 Imaging-Integrated Non-Incisional Ablation Platforms

- 4.3 Market Restraints

- 4.3.1 Uneven Reimbursement for MRgFUS

- 4.3.2 Fertility And Pregnancy Evidence Gaps

- 4.3.3 Rural Interventional Radiology Access Shortage

- 4.3.4 Morcellation-Related Safety Controls

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Surgical Techniques

- 5.1.1.1 Hysterectomy

- 5.1.1.2 Myomectomy

- 5.1.2 Laparoscopic Techniques

- 5.1.2.1 Laparoscopic Myomectomy

- 5.1.2.2 Myolysis

- 5.1.3 Ablation Techniques

- 5.1.3.1 Laparoscopic Radiofrequency Ablation

- 5.1.3.2 Transcervical Radiofrequency Ablation

- 5.1.3.3 MRI-guided Focused Ultrasound

- 5.1.3.4 Ultrasound-guided High-intensity Focused Ultrasound

- 5.1.4 Embolization Techniques

- 5.1.4.1 Uterine Fibroid Embolization

- 5.1.4.2 Embolic Microspheres

- 5.1.4.3 PVA Particles

- 5.1.1 Surgical Techniques

- 5.2 By Mode of Treatment

- 5.2.1 Invasive Treatment

- 5.2.1.1 Open Surgery

- 5.2.1.2 Robotic-assisted Surgery

- 5.2.2 Minimally Invasive Treatment

- 5.2.2.1 Laparoscopic Procedures

- 5.2.2.2 Hysteroscopic Procedures

- 5.2.2.3 Uterine Artery Embolization

- 5.2.3 Non-invasive Treatment

- 5.2.3.1 MR-guided Focused Ultrasound

- 5.2.3.2 Ultrasound-guided High-intensity Focused Ultrasound

- 5.2.1 Invasive Treatment

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Office-based Gynecology Clinics

- 5.3.4 Interventional Radiology Centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Axora Medical, Inc.

- 6.3.2 Boston Scientific Corporation

- 6.3.3 CONMED Corporation

- 6.3.4 Cook Medical

- 6.3.5 CooperSurgical, Inc.

- 6.3.6 GE HealthCare Technologies Inc.

- 6.3.7 Hologic, Inc.

- 6.3.8 INSIGHTEC Ltd.

- 6.3.9 Intuitive Surgical, Inc.

- 6.3.10 Johnson & Johnson MedTech

- 6.3.11 KARL STORZ SE & Co. KG

- 6.3.12 Medtronic

- 6.3.13 Merit Medical Systems, Inc.

- 6.3.14 Minerva Surgical, Inc.

- 6.3.15 Olympus Corporation

- 6.3.16 Profound Medical Corp.

- 6.3.17 Richard Wolf GmbH

- 6.3.18 Siemens Healthineers AG

- 6.3.19 Stryker Corporation

- 6.3.20 Terumo Interventional Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment