|

시장보고서

상품코드

2072699

미국의 바이오테크놀러지 및 의약품 서비스 아웃소싱 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)US Biotechnology And Pharmaceutical Services Outsourcing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

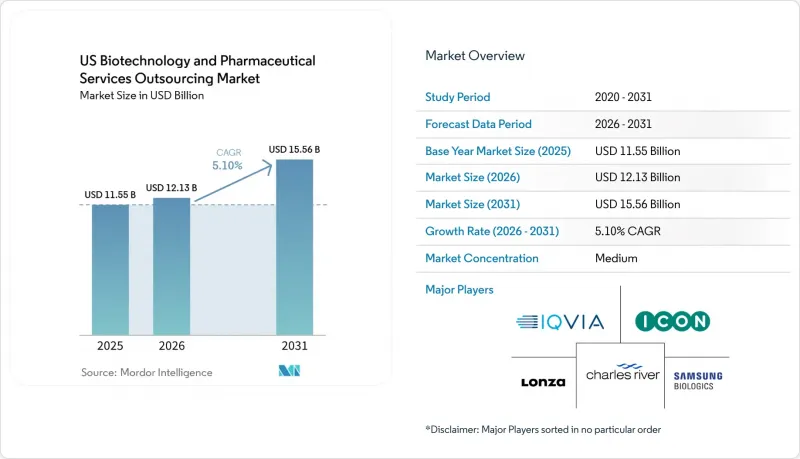

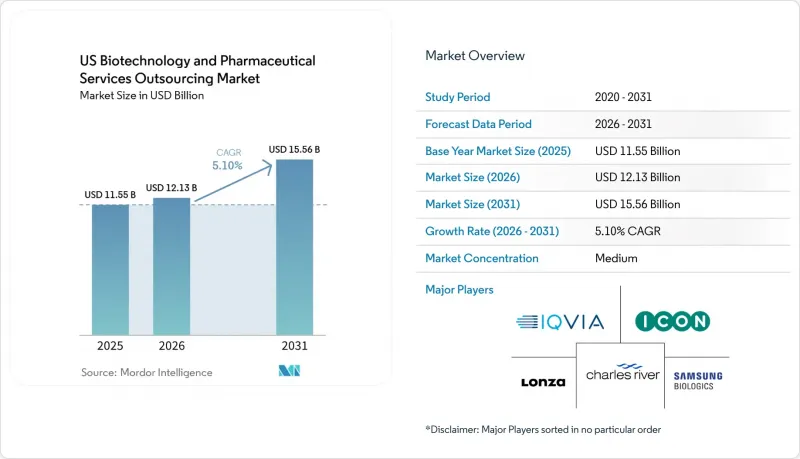

Mordor Intelligence에 의하면, 미국의 바이오테크놀러지 및 의약품 서비스 아웃소싱 시장 규모는 2025년 115억 5,000만 달러로 평가되었고, 2026년에는 121억 3,000만 달러로 추정되고, 2031년까지 155억 6,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 5.10%로 성장할 전망입니다.

본 보고서는 서비스 유형별(CRO, CDMO, 분석, 약사 규제, 의약품 안전성 모니터링, 포장), 제제 유형별(저분자 의약품, 고분자 의약품, 세포 및 유전자 치료, 백신), 개발 단계별, 최종 사용자 및 치료 분야별(종양학, 신경학, 면역학, 순환기, 희귀질환, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 바이오테크놀러지 및 의약품 서비스 아웃소싱 시장 동향과 인사이트

바이오의약품, 세포 및 유전자 치료 파이프라인의 복잡화

바이오의약품, 세포 치료, 유전자 치료로의 전환이 미국 바이오기술 및 제약 서비스 아웃소싱 시장의 주요 수요 견인 요인으로 작용하고 있습니다. 이러한 프로그램에는 전문적인 GMP 시설, 치료법별로 특화된 분석 기법, 복잡한 콜드체인 프로세스, 그리고 단기간에 구축하기 어려운 규제 관련 전문 지식이 필요합니다. 2024년에는 총 5,318건의 임상시험이 시작된 가운데, 종양학, 면역학, 신경학 및 순환기 계통 프로그램이 71%를 차지하여 복잡한 분야에 대한 집중이 반영되었습니다. 세포 및 유전자 치료, 항체-약물 복합체(ADC), 다중 특이성 항체 등의 새로운 종양학 치료법은 종양학 임상시험의 35%를 차지하며, 고도의 역량을 갖춘 CDMO에 대한 수요를 높이고 있습니다. 자체 개발 CAR-T 프로그램에는 여러 가지 전문적인 업무가 포함되어 있으며, 작업이 다양한 공급업체에 분산됨에 따라 아웃소싱 규모와 프로그램 비용 증가, 그리고 공급업체와의 협력 기간 장기화로 이어지고 있습니다.

엔드투엔드 통합 개발 및 제조 파트너에 대한 수요

미국의 바이오테크놀러지 및 의약품 서비스 아웃소싱 시장에서 각 스폰서사는 프로그램당 아웃소싱 파트너 수를 줄이고 있으며, 개발부터 규제 당국에 대한 신청에 이르기까지의 전 과정을 일원화하여 관리하는 서비스 제공업체를 우선적으로 선택하고 있습니다. 통합형 CDMO 및 CRO 모델은 개발 일정을 단축하는 효과가 입증되었으며, 350건 이상의 프로토콜에서 120개 이상의 생명공학 기업에 채택되고 있습니다. 이러한 추세로 인해 폭넓은 역량을 갖춘 제공업체에 수익이 집중되는 한편, 소규모 전문 기업들은 파트너십을 맺어 서비스 제공 범위를 확대되고 있습니다. 조달 팀은 속도와 인수인계 횟수 감소를 최우선으로 하고 있으며, 이를 통해 통합 플랫폼은 가격 협상력을 강화하고 스폰서와의 관계를 더욱 공고히 하고 있습니다.

스폰서의 집중 위험과 공급업체 통합

미국의 바이오테크놀러지 및 의약품 서비스 아웃소싱 시장에서는 주요 발주사들 간공급업체 통합이 성장 기회를 제한하고 있습니다. 현재 많은 대형 제약사들은 서비스 분야를 불문하고, 엄선된 소수의 우선 협력 CRO 및 CDMO와 제휴하고 있습니다. 이러한 접근 방식은 감독 및 비용 관리를 효율화하지만, 우선순위 지위를 상실할 경우 공급업체는 막대한 수익 위험에 노출될 수 있습니다. 중견 기업들은 계약을 따내기 전에 품질 관리 시스템, 인력, 시설에 대한 투자를 하는 경우가 많기 때문에 더 큰 압박에 직면하고 있습니다. 소규모 생명공학 기업으로부터의 수주가 어느 정도 균형을 유지하고 있지만, 이러한 수요는 자금 조달 상황이나 포트폴리오 변경에 따라 변동하기 때문에 수익의 질은 고객 집중도나 계약 갱신 주기에 쉽게 좌우됩니다.

부문별 분석

2025년, 계약연구기관(CRO) 서비스는 미국의 바이오테크놀러지 및 의약품 서비스 아웃소싱 시장을 주도하며 매출의 39.88%를 차지했습니다. 이러한 우위는 주로 종양학 및 신경학 분야에서 제2상부터 제4상에 이르는 지속적인 활동에 기인합니다. 이러한 분야에서는 임상시험의 수행이 데이터 집약적일 뿐만 아니라, 운영 면에서도 매우 복잡합니다. 각 CRO 기업은 기존의 모니터링 및 임상시험 기관 관리에 그치지 않고, 프로토콜 설계 지원, 피험자 모집 분석, 의약품 안전성 감시, 통합적인 품질 감독 등을 포함하도록 업무 범위를 확대되고 있습니다. 스폰서들이 개별 서비스보다 종합적인 실행 패키지를 선택하는 경향이 있기 때문에 이러한 변화로 인해 평균 계약 금액이 상승하고 있습니다. 시장에서는 임상 업무와 엄격한 규제 및 기술적 지원을 원활하게 결합하는 서비스 제공업체에 대한 지지가 점점 더 높아지고 있습니다.

다기관 공동 프로그램 전반에 걸친 감시 기준의 강화로 인해, 약사 및 품질 보증 관련 서비스가 호황을 누리고 있습니다. 스폰서들은 공급업체 간의 품질 관리 시스템 운영을 지원하는 것을 점점 더 요구하고 있습니다. 임상시험 설계에 바이오마커가 점점 더 많이 도입됨에 따라, 특히 종양학 분야에서 분석 및 바이오분석 서비스에 대한 수요가 급증하고 있습니다. 의약품 안전성 감시 및 의약품 안전성 서비스는 자동화 모델로 전환되고 있으며, 각 서비스 제공업체들은 신속한 신호 감지 및 대규모 사례 처리 도구에 대한 투자를 확대되고 있습니다. 포장, 표시, 일련번호 부여 서비스는 여전히 틈새 분야이지만, 보관 관리의 연속성(체인 오브 카스투디)을 유지하는 것이 극히 중요한 첨단 치료 프로그램에서는 그 중요성이 매우 큽니다.

2025년에는 저분자 화합물이 매출의 42.35%를 차지했으며, 미국의 바이오테크놀러지 및 의약품 서비스 아웃소싱 시장에서 주요 의약품 유형 부문으로서의 입지를 확고히 다졌습니다. 이러한 확고한 입지는 신규 화학 물질과 고활성 화합물이 풍부하게 포함된 파이프라인에 의해 뒷받침되고 있습니다. API 합성 및 경구용 고형 제제 제조 분야에서는 특히 규제 물질이나 엄격한 격리 요건이 수반되는 프로그램의 경우, 아웃소싱이 이미 널리 보급되어 있습니다. 그 결과, 이 부문의 향후 성장은 아웃소싱 비율의 큰 변화보다는 오히려 구성 비율의 개선에 기인할 것으로 예측됩니다. 고효능 화합물이나 복잡한 합성 경로에 힘입어 계약액이 증가했다는 사실은 프로그램 수가 비례적으로 증가하지 않았더라도 분명합니다.

세포 및 유전자 치료는 가장 빠르게 성장하는 의약품 유형으로 부상하고 있으며, 미국의 바이오테크놀러지 및 의약품 서비스 아웃소싱 시장에서 2031년까지 연평균 성장률(CAGR)이 8.88%를 나타낼 것으로 전망됩니다. 이러한 부상은 IND(신약 임상시험 신청) 활동 증가와 벡터, 플라스미드, 세포 처리 및 출하 검사와 관련된 사내 역량을 갖춘 의뢰사가 부족하기 때문인 것으로 보입니다. 세포 및 유전자 치료, 항체-약물 복합체(ADC), 다중 특이성 항체 등을 포함한 새로운 종양학 치료법은 현재 종양학 임상시험의 35%를 차지하고 있으며, 전문적인 제조 및 분석 지원에 대한 수요 증가를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the US biotechnology and pharmaceutical services outsourcing market size is expected to increase from USD 11.55 billion in 2025 to USD 12.13 billion in 2026 and reach USD 15.56 billion by 2031, growing at a CAGR of 5.10% over 2026-2031.

This report is Segmented by Service Type (CRO, CDMO, Analytical, Regulatory Affairs, Pharmacovigilance, Packaging), Drug Type (Small Molecules, Large Molecules, Cell and Gene Therapies, Vaccines), Development Stage, End User, and Therapeutic Area (Oncology, Neurology, Immunology, Cardiovascular, Rare Diseases, Others). The Market Forecasts are Provided in Terms of Value (USD).

US Biotechnology And Pharmaceutical Services Outsourcing Market Trends and Insights

Rising Complexity of Biologics, Cell and Gene Therapy Pipelines

The shift towards biologics, cell therapies, and gene therapies is the primary demand driver in the United States biotechnology and pharmaceutical services outsourcing market. These programs require specialized GMP suites, modality-specific analytical methods, complex cold-chain processes, and regulatory expertise that are challenging to develop quickly. In 2024, oncology, immunology, neurology, and cardiovascular programs accounted for 71% of the 5,318 clinical trial starts, reflecting the focus on complex areas. Novel oncology modalities, including cell and gene therapies, antibody-drug conjugates, and multispecific antibodies, represented 35% of oncology trials, increasing demand for CDMOs with advanced capabilities. Autologous CAR-T programs involve multiple specialized tasks, spreading work across various vendors, which drives higher outsourcing volumes, program costs, and longer provider relationships.

Demand for Integrated End-to-End Development and Manufacturing Partners

Sponsors in the United States biotechnology and pharmaceutical services outsourcing market are reducing the number of outsourcing partners per program, favoring providers that manage end-to-end processes from development to regulatory submission. Integrated CDMO and CRO models have been shown to accelerate timelines, with adoption by over 120 biotechs across 350-plus protocols. This trend is concentrating revenue among providers with broader capabilities, while smaller specialists form partnerships to expand service offerings. Procurement teams prioritize speed and fewer handoffs, giving integrated platforms pricing leverage and stronger sponsor relationships.

Sponsor Concentration Risk and Vendor Consolidation

In the United States biotechnology and pharmaceutical services outsourcing market, vendor consolidation among major sponsors is limiting growth opportunities. Many leading pharmaceutical firms now work with a select few preferred CROs and CDMOs across service categories. While this approach streamlines oversight and cost management, it exposes providers to significant revenue risks if they lose a preferred status. Mid-tier companies face added pressure as they often invest in quality systems, staffing, and facilities before securing contracts. Smaller biotech clients provide some balance, but their demand fluctuates with financing and portfolio changes, making revenue quality sensitive to client concentration and renewal cycles.

Other drivers and restraints analyzed in the detailed report include:

- Reshoring and North American Supply Chain Risk Diversification

- Data-Heavy Clinical Operations Favor Scalable US-Based Technology Platforms

- Capacity Bottlenecks in Specialized Modalities and GMP Suites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Contract Research Organization (CRO) services dominated the US biotechnology and pharmaceutical services outsourcing market, accounting for 39.88% of the revenue. This dominance is largely attributed to ongoing Phase II to Phase IV activities in oncology and neurology, fields where trial execution is both data-intensive and operationally intricate. CROs are broadening their scope, moving beyond traditional monitoring and site management to include protocol design support, patient recruitment analytics, pharmacovigilance, and integrated quality oversight. This evolution is driving up average contract values, as sponsors opt for comprehensive execution packages over standalone services. The market is increasingly favoring providers that seamlessly blend clinical operations with robust regulatory and technological backing.

Services in Regulatory Affairs and Quality Assurance are thriving, thanks to heightened oversight standards across multi-site programs. Sponsors are increasingly seeking assistance in managing quality systems across vendors. As trial designs become richer in biomarkers, the demand for Analytical and Bioanalytical services is surging, especially in oncology. Pharmacovigilance and Drug Safety services are transitioning to automated models, with providers channeling investments into rapid signal detection and expansive case-processing tools. While Packaging, Labeling, and Serialization services remain niche, their significance is paramount in advanced therapy programs, where maintaining chain-of-custody control is critical.

In 2025, small molecules constituted 42.35% of the revenue, solidifying their position as the leading drug-type segment in the US biotechnology and pharmaceutical services outsourcing market. Their stronghold is bolstered by a pipeline teeming with new chemical entities and high-potency compounds. Outsourcing is already prevalent in API synthesis and oral solid dose manufacturing, particularly for programs involving controlled substances or stringent containment needs. Consequently, future growth in this segment is anticipated to stem more from an improved mix rather than a significant shift in outsourcing rates. The rising contract values, driven by higher-potency compounds and intricate synthesis routes, are evident even without a proportional increase in program counts.

Cell and gene therapies are emerging as the fastest-growing drug type, with an anticipated 8.88% CAGR through 2031 in the US biotechnology and pharmaceutical services outsourcing market. Their ascent is fueled by increasing IND activity and the scarcity of sponsors possessing in-house capabilities for vector, plasmid, cell-processing, and release-testing. Novel oncology modalities, encompassing cell and gene therapies, antibody-drug conjugates, and multispecific antibodies, now represent 35% of oncology trials, sustaining a heightened demand for specialized manufacturing and analytical support.

Complete Report Scope:

- By Service Type

- Contract Research Organization Services

- Contract Development and Manufacturing Organization Services

- Analytical and Bioanalytical Services

- Regulatory Affairs and Quality Assurance Services

- Pharmacovigilance and Drug Safety Services

- Market Access and Medical Affairs Services

- Packaging, Labeling and Serialization Services

- By Drug Type

- Small Molecules

- Large Molecules

- Cell and Gene Therapies

- Vaccines

- Other Drug Types

- By Development Stage

- Discovery and Preclinical

- Phase I

- Phase II

- Phase III

- Phase IV and Post-Marketing

- By End User

- Pharmaceutical Companies

- Biotechnology Companies

- Medical Device Companies

- Academic and Research Institutions

- Government and Public Health Organizations

- By Therapeutic Area

- Oncology

- Neurology

- Immunology

- Infectious Diseases

- Cardiovascular Diseases

- Rare Diseases

- Metabolic Disorders

- Other Therapeutic Areas

List of Companies Covered in this Report:

- Abbvie

- Aenova Group GmbH

- Alcami

- Boehringer Ingelheim

- Cambrex

- Catalent

- Charles River

- Eurofins

- Fortrea Holdings Inc.

- ICON

- IQVIA

- Labcorp Holdings Inc.

- Lonza Group Ltd.

- Medpace Holdings, Inc.

- Parexel International

- PCI Pharma Services

- Pfizer

- Samsung Biologics Co., Ltd.

- Syneos Health

- Thermo Fisher Scientific Inc. (PPD, Inc.)

- WuXi AppTec Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Complexity of Biologics, Cell and Gene Therapy Pipelines

- 4.2.2 Sponsor Push for Fixed-Cost, Variable-Capacity Operating Models

- 4.2.3 Demand for Integrated End-to-End Development and Manufacturing Partners

- 4.2.4 Reshoring and North American Supply Chain Risk Diversification

- 4.2.5 Data-Heavy Clinical Operations Favor Scalable US-Based Technology Platforms

- 4.2.6 Faster Protocol Design and Enrollment Support for Complex Trials

- 4.3 Market Restraints

- 4.3.1 Sponsor Concentration Risk and Vendor Consolidation

- 4.3.2 Regulatory and Quality Compliance Burden Across Multi-Site Programs

- 4.3.3 Capacity Bottlenecks in Specialized Modalities and GMP Suites

- 4.3.4 Margin Pressure From Bid Competition and Pricing Compression

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Service Type

- 5.1.1 Contract Research Organization Services

- 5.1.2 Contract Development and Manufacturing Organization Services

- 5.1.3 Analytical and Bioanalytical Services

- 5.1.4 Regulatory Affairs and Quality Assurance Services

- 5.1.5 Pharmacovigilance and Drug Safety Services

- 5.1.6 Market Access and Medical Affairs Services

- 5.1.7 Packaging, Labeling and Serialization Services

- 5.2 By Drug Type

- 5.2.1 Small Molecules

- 5.2.2 Large Molecules

- 5.2.3 Cell and Gene Therapies

- 5.2.4 Vaccines

- 5.2.5 Other Drug Types

- 5.3 By Development Stage

- 5.3.1 Discovery and Preclinical

- 5.3.2 Phase I

- 5.3.3 Phase II

- 5.3.4 Phase III

- 5.3.5 Phase IV and Post-Marketing

- 5.4 By End User

- 5.4.1 Pharmaceutical Companies

- 5.4.2 Biotechnology Companies

- 5.4.3 Medical Device Companies

- 5.4.4 Academic and Research Institutions

- 5.4.5 Government and Public Health Organizations

- 5.5 By Therapeutic Area

- 5.5.1 Oncology

- 5.5.2 Neurology

- 5.5.3 Immunology

- 5.5.4 Infectious Diseases

- 5.5.5 Cardiovascular Diseases

- 5.5.6 Rare Diseases

- 5.5.7 Metabolic Disorders

- 5.5.8 Other Therapeutic Areas

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 AbbVie

- 6.3.2 Aenova Group GmbH

- 6.3.3 Alcami Corporation

- 6.3.4 Boehringer Ingelheim GmbH

- 6.3.5 Cambrex Corporation

- 6.3.6 Catalent, Inc.

- 6.3.7 Charles River Laboratories International, Inc.

- 6.3.8 Eurofins Scientific SE

- 6.3.9 Fortrea Holdings Inc.

- 6.3.10 ICON plc

- 6.3.11 IQVIA Holdings Inc.

- 6.3.12 Labcorp Holdings Inc.

- 6.3.13 Lonza Group Ltd.

- 6.3.14 Medpace Holdings, Inc.

- 6.3.15 Parexel International Corporation

- 6.3.16 PCI Pharma Services

- 6.3.17 Pfizer

- 6.3.18 Samsung Biologics Co., Ltd.

- 6.3.19 Syneos Health, Inc.

- 6.3.20 Thermo Fisher Scientific Inc. (PPD, Inc.)

- 6.3.21 WuXi AppTec Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment