|

시장보고서

상품코드

2072705

헤지호그 경로 억제제 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Hedgehog Pathway Inhibitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

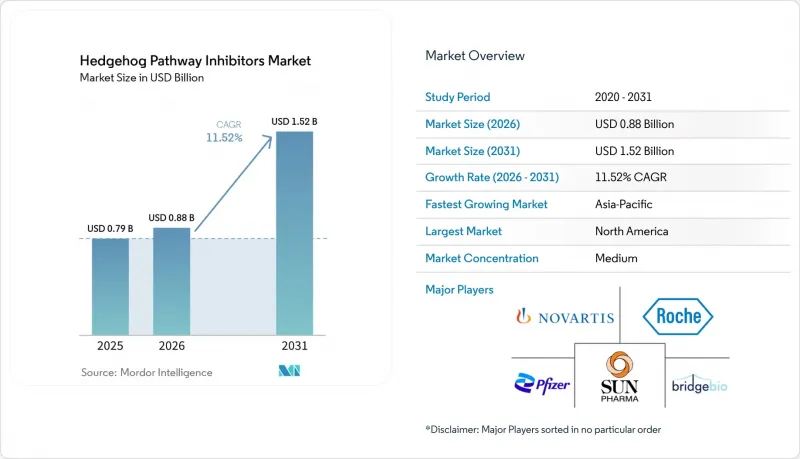

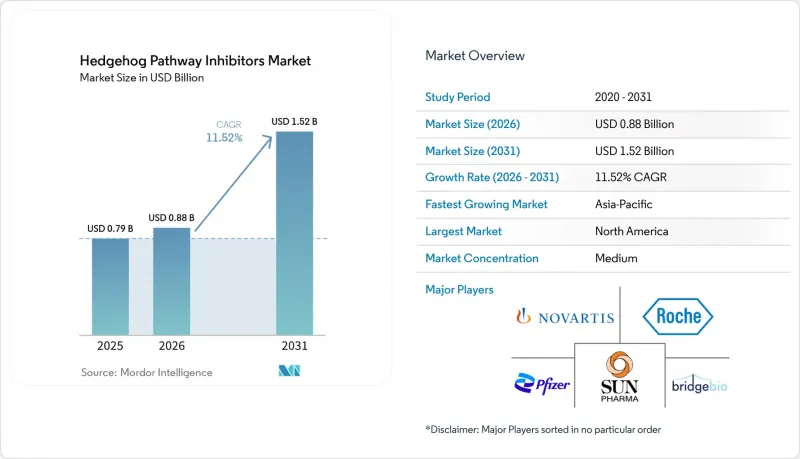

Mordor Intelligence에 의하면, 헤지호그 경로 억제제 시장 규모는 2025년 7억 9,000만 달러로 평가되었고, 2026년에는 8억 8,000만 달러로 추정되고, 2026-2031년 CAGR 11.52%로 성장을 지속할 전망이며, 2031년에는 15억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 약제 유형별(비스모데기브, 소니데기브, 글라스데기브, 기타), 적응증별(기저세포암, 급성 골수성 백혈병, 골수모세포종, 고린 증후군), 투여 경로별(경구, 외용, 주사), 유통 채널별(병원, 소매, 온라인 약국), 최종 사용자별(병원, 진료소, 연구 기관, 재택치료), 지역별(북미, 유럽, 남미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 헤지호그 경로 억제제 시장 동향 및 인사이트

고령화 및 자외선에 노출된 인구에서 기저세포암(BCC) 및 급성 골수성 백혈병(AML)의 부담 증가

헤지호그 경로 억제제 시장의 기본적인 수요 동인은 인구 통계에 있습니다. 이는 치료 대상이 되는 환자층이 고령층에 집중되어 있으며, 이 연령대에서는 피부암으로 인한 부담과 치료의 복잡성이 모두 증가하고 있기 때문입니다. 55세 이상 성인을 대상으로 한 전 세계 기저세포암(BCC)의 신규 환자 수는 증가하고 있으며, 예측에 따르면 최고령층에서는 향후 더욱 급격한 증가가 예상됩니다. 절대적인 환자 수가 가장 많은 나라는 미국, 브라질, 중국입니다. 헤지호그 경로 억제제 시장은 눈에 띄지는 않지만 중요한 요인인 면역 억제 상태의 환자 증가로 인해 혜택을 보고 있습니다. 이식 수혜자나 생물학적 제제를 장기간 투여받고 있는 환자는 면역 기능이 정상인 집단에 비해 기저세포암 발병률이 현저히 높기 때문에 약물 요법의 대상이 될 수 있는 국소 진행 사례의 수가 증가하고 있기 때문입니다.

백혈병 분야에서 글라스데기브는 75세 이상의 성인 또는 집중 화학요법을 받을 수 없는 동반 질환이 있는 성인을 대상으로 하고 있으며, 이에 따라 이 제품은 가장 고령이면서 가장 빠르게 확대되고 있는 급성 골수성 백혈병(AML) 치료 환자 집단과 부합합니다. 실제 임상 데이터도 이 논리를 뒷받침하고 있으며, 글라스데기브를 기반으로 한 치료를 지역 암 진료에서 1차 선택으로 적용했을 때 50%의 종합 관해율이 보고되었습니다. 이는 허약한 AML 환자군에서 헤지호그 경로 억제제 시장이 임상적 및 상업적으로 지속적인 역할을 수행할 것임을 뒷받침합니다. 이처럼 고령이며 의학적으로 복잡한 환자층이 확대됨에 따라, 헤지호그 경로 억제제 시장은 단순히 환자 수를 늘리는 데 그치지 않고, 현재의 적응증 및 진료 환경 요건을 충족하는 환자를 더 많이 확보하게 될 것입니다.

바이오마커를 기반으로 한 환자군 선별을 통해 대상 환자군이 확대됨

환자 선별이 더욱 정교해지고 있으며, 이러한 정교함 덕분에 헤지호그 경로 억제제 시장에서 진단에서 치료로의 전환율이 실질적으로 향상될 가능성이 있습니다. PTCH1 변이를 가진 종양에서 비스모데기브는 고린 증후군 환자에서 100%의 반응률을 보였으나, 이에 반해 선별 기준이 없는 진행성 기저세포암(BCC) 코호트에서는 반응률이 43%에 그쳤습니다. 이는 분자 수준의 배경이 치료의 가치를 얼마나 크게 변화시키는지를 보여줍니다. 이 차이는 중요합니다. 왜냐하면 피부과나 종양학 임상 현장에서 보다 광범위한 유전체 스크리닝이 이루어짐으로써, 헤지호그 억제제를 최후의 수단인 난치성 사례에만 국한하지 않고, 높은 반응률을 기대할 수 있는 환자를 조기에 치료에 포함시킬 수 있기 때문입니다.

헤지호그 경로 억제제 시장은 경로 수준의 검사가 점차 표준화됨에 따라 혜택을 볼 것으로 전망됩니다. 왜냐하면, 표적의 활성화나 예상되는 치료 효과를 특정 돌연변이 패턴과 연관 지을 수 있다면, 임상의의 확신이 높아지기 때문입니다. 순환 혈액 내 PTCH1 및 SMO 돌연변이체를 검출하는 체액 생검 플랫폼은 조직 검사와의 일치율이 87.5%에 달하며, 이를 통해 검체 채취의 부담이 줄어들고, 피부암 및 백혈병 프로그램 모두에서 선별 검사율이 향상될 가능성이 있습니다. 비침습적 검사가 개선되고 대규모 활용이 용이해짐에 따라, 헤지호그 경로 억제제 시장은 적응증 확대뿐만 아니라 보다 적절한 환자 선정을 통해 환자 수를 늘릴 수 있을 것입니다.

근골격계 및 미각 관련 독성이 치료 중단의 요인으로 작용

독성은 적격 환자 수가 계속 증가하고 있음에도 불구하고 치료 기간을 단축시키기 때문에 헤지호그 경로 억제제 시장에서 여전히 가장 큰 제약 요인 중 하나로 남아 있습니다. 다기관 공동 실세계 연구에 따르면, 이상반응으로 인한 치료 중단은 비스모데기브 투여군에서 47.4%, 소니데기브 투여군에서 13.2% 발생했으며, 이는 동일한 치료제 계열 내에서도 치료 지속률에 매우 큰 격차가 있음을 여실히 보여주고 있습니다. 이러한 차이는 상업적으로도 중요한 의미를 지닙니다. 소니데기브는 반감기가 길어 간헐적인 투여를 통해 보다 유연한 치료가 가능한 반면, 비스모데기브의 경우 지속적인 질환 관리와 내약성 사이에서 더 까다로운 절충을 요구받는 경우가 많기 때문입니다. 부작용의 발생은 대조군 연구에만 국한된 것이 아니며, 실제 임상 현장에서의 약물 안전성 모니터링 활동에서는 경구용 헤지호그 억제제 투여 시 근육 경련 및 미각 이상에 대한 뚜렷한 징후가 계속해서 나타나고 있습니다.

헤지호그 경로 억제제 시장은 환자가 완전한 치료 효과를 얻기 전에 치료를 중단할 때마다 그 가치를 잃게 됩니다. 이는 치료 대상이 되는 환자 수가 수요를 창출하기에 충분한 규모인 반면, 각 환자가 가져오는 치료 개월 수가 예상보다 적기 때문입니다. 독성이 낮은 제형이나 더 우수한 관리 프로토콜이 표준화될 때까지는 헤지호그 경로 억제제 시장은 단순한 인지도 문제가 아니라 구조적인 치료 지속률 문제에 계속 직면하게 될 것입니다.

부문별 분석

비스모데기브는 2025년에도 헤지호그 경로 억제제 시장에서 42.31%의 점유율을 유지했습니다. 이는 해당 약제가 선구적인 위치를 차지하고 있으며, 의사의 인지도가 여전히 높은 국소 진행성 기저세포암(BCC) 분야에서 오랫동안 사용되어 온 사실을 반영한 것입니다. 헤지호그 경로 억제제 시장에서 이 약물의 위상은 BCC 분야에서 폭넓은 임상적 인지도와, 신약이 사례별로 대체해 나가야 할 정도로 오랫동안 확립된 처방 기반에 의해 여전히 뒷받침되고 있습니다. 실제 임상 데이터 역시 비스모데기브가 진행성 기저세포암에서 임상적 유효성을 유지하고 있음을 계속해서 뒷받침하고 있으며, 이는 해당 약물군 전체에서 나타나는 독성 프로파일에도 불구하고 시장 점유율이 유지되고 있는 이유를 설명해 줍니다. 소니데기브는 내약성 측면에서 보다 명확한 메시지를 내세우며 경쟁하고 있으며, 실세계 데이터 분석에 따르면 9개월간의 추적 기간 동안 소니데기브 치료를 받은 환자는 비스모데기브 치료를 받은 환자에 비해 근경련 발병 확률이 52% 낮고, 미각 장애 발병 확률이 71% 낮은 것으로 나타났습니다. 이러한 차이는 비스모데기브의 확고한 기반을 뒤엎는 것은 아니지만, 헤지호그 경로 억제제 시장에서 제품 차원의 규모와 내약성이라는 명확한 양극화를 초래하고 있습니다.

글라스데기브는 헤지호그 경로 억제제 시장에서 가장 빠르게 성장하고 있는 약물 유형으로, 2026-2031년 연평균 성장률(CAGR) 12.38%로 성장을 지속할 전망입니다. 이러한 성장은 AML(급성 골수성 백혈병) 이외의 백혈병 분야, 즉 골수섬유증, 골수이형성증후군, 만성 골수단핵구 백혈병 등에서의 임상 연구와 관련되어 있으며, 이를 통해 BCC(기저세포암)에 대한 추가적인 노출에 의존하지 않고도 이 약물 군에 대한 임상적 평가의 폭이 넓어지고 있습니다. 헤지호그 경로 억제제 업계에게도 글라스데기브는 유용한 다각화의 계기가 될 것입니다. 이는 혈액종양 분야에서의 역할을 통해 피부암에 대한 의존도를 낮추기 위함입니다. 미국의 지역 암 진료소를 대상으로 한 실제 임상 연구에 따르면, 글라스데기브를 이용한 1차 치료를 받은 급성 골수성 백혈병(AML) 환자에서 50%의 종합 관해율이 보고되었으며, 이는 학술적 임상시험 센터 이외의 환경에서 본 제품의 유용성을 입증하는 것입니다. '기타 헤지호그 경로 억제제'가 카테고리는 현재로서는 규모가 작지만, 특발성 폐섬유증에 대한 타라데기브의 희귀질환용 의약품 지정은 헤지호그 경로 억제제 시장이 인접한 질환 영역으로 확대되고 있음을 보여주며, 향후 상업적으로 중요한 시장이 될 가능성을 시사하고 있습니다.

2025년 헤지호그 경로 억제제 시장 규모 중 기저세포암이 76.24%를 차지했으며, 현재 수익이 진행성 기저세포암 치료 경로에 얼마나 의존하고 있는지를 알 수 있습니다. 이러한 집중 현상이 나타나는 이유는 약물 요법이 주로 수술이나 방사선 치료가 적용될 수 없는 경우에 도입되기 때문이며, 이에 따라 헤지호그 경로 억제제 시장은 명확하게 정의된 미충족 의료 수요가 있는 환자 집단에서 확고한 입지를 확보하고 있습니다. 적용 범위에 관한 규정이 이러한 구조를 강화하고 있으며, 사전 승인 체계를 통해 환급은 광범위한 일반 진료에서의 처방이 아닌, 적응증 범위 내에서의 사용 및 전문의의 감독과 계속해서 밀접하게 연계되어 있습니다. AML(급성 골수성 백혈병)은 헤지호그 경로 억제제 시장에서 여전히 명확한 2차 적응증으로 자리매김하고 있습니다. 이는 글라스데기브가 집중적인 화학요법의 적응증이 되지 않는 고령 또는 신체적으로 허약한 환자에게 투여되기 때문이며, 이 제품은 임상적으로 차별화되고 의료기관에 집중된 부문에 속합니다. 수모세포종은 현재 수익 규모는 작지만, PTCH1 돌연변이형 SHH 하위 그룹의 종양에서 50%에 가까운 반응률이 나타난 점을 고려할 때, 특정 증례에서는 유전자형에 기반한 사용이 여전히 중요하다는 것을 알 수 있습니다.

고린 증후군은 헤지호그 경로 억제제 시장에서 가장 빠르게 성장하고 있는 적응증으로, 2026-2031년 연평균 성장률(CAGR) 13.52%를 나타낼 것으로 전망됩니다. 이 부문이 두드러지는 이유는 새로운 병변의 형성을 무기한으로 억제해야 하기 때문에 일회성 치료 과정뿐만 아니라 반복되는 예방 조치를 통해 수익이 누적된다는 점에 있습니다. 이러한 특성으로 인해 고린 증후군은 헤지호그 경로 억제제 시장에서 시장 침투율이 가장 낮은 분야 중 하나이며, 특히 외용 예방 요법이 승인된다면 이러한 경향은 더욱 두드러질 것입니다. Sol-Gel Technologies는 SGT-610의 3상 임상시험 참가자 등록을 완료했으며, 2026년 4분기에 주요 결과가 발표될 전망입니다. 이를 통해 예방에 중점을 둔 최초의 상용화를 향한 길이 확고해졌습니다. 승인될 경우, 이 치료법은 기존의 진행성 기저세포암(BCC) 치료와는 차별화된 예방 분야를 개척하게 될 것이며, 현재 종양학 분야에서 사용을 규정하는 동일한 보험 급여 논리에 의존하지 않고도 헤지호그 경로 억제제 시장의 확대가 가능해질 것입니다.

지역별 분석

2025년, 북미는 헤지호그 경로 억제제 시장의 41.52%를 차지했으며, 지역별 순위에서 단연 1위를 차지했습니다. 이러한 순위의 대부분은 기저세포암(BCC) 발병률이 세계 최고를 기록한 미국이 주도한 결과입니다. 또한, 이 지역은 국소 진행성 기저세포암(BCC)의 전원 체계 및 브랜드 항암제의 보험 급여 제도와 긴밀히 연계된 전문적인 종양 의료 인프라의 혜택을 누리고 있습니다. 규제 측면에서의 지원도 한몫을 했으며, 2025년 신속 승인 및 시판 후 확인에 관한 지침 초안의 개정을 통해, 증거 요건을 유지하면서도 암 치료제의 조기 시장 진입을 계속해서 지원할 수 있는 체계가 강화되었습니다.

헤지호그 경로 억제제 시장에서 아시아태평양 시장 규모는 2026-2031년 연평균 성장률(CAGR) 13.55%로 확대될 것으로 예상되며, 가장 빠르게 성장하는 지역 블록이 될 전망입니다. 이러한 성장은 중국과 일본의 고령화, 야외에서 일하는 사람들의 자외선 노출 증가, 그리고 전문 항암제에 대한 접근성 향상 등에 힘입은 것입니다. 중국의 규제 개혁에 따라, 서유럽에서 이미 승인된 암 치료제의 국내 승인까지 소요되는 기간이 단축되었으며, 전 세계의 임상 증거를 바탕으로 국내 상용화에 이르는 과정이 개선되었습니다. 또한 일본에서는 지역별 특화된 지원이 더해져, 집중 화학요법 대상에서 제외되는 급성 골수성 백혈병(AML) 환자를 대상으로 한 글라스데기브의 제Ib/II상 임상시험에서 확대 코호트에서 질병 수정 반응률이 46.7%로 보고되었습니다. 중국 내 55세 이상 성인을 대상으로 한 기저세포암(BCC) 사례 수는 인구 동향의 변화가 해당 지역의 헤지호그 경로 억제제 시장에 향후 얼마나 큰 기반을 마련해 주고 있는지를 보여줍니다.

그 밖의 지역은 현재 매출 규모는 아직 작지만, 시간이 지남에 따라 헤지호그 경로 억제제 시장에서 그 중요성이 커지고 있습니다. 걸프협력회의(GCC) 회원국들은 자외선(UV) 노출량이 높은 데다 종양학 분야의 의료 체계가 점차 정비되고 있지만, 보험 환급 제도는 각 시스템 간에 여전히 차이가 있습니다. 남아프리카는 민간 의료 채널과 대학 부속 병원이 전문적인 종양 치료를 받을 수 있는 가장 확실한 경로를 제공하고 있기 때문에 사하라 이남 아프리카에서 헤지호그 경로 억제제 시장에 진출하기 위한 거점으로서 가장 발전된 지역으로 자리매김하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the hedgehog pathway inhibitors market size is expected to grow from USD 0.79 billion in 2025 to USD 0.88 billion in 2026 and is forecast to reach USD 1.52 billion by 2031 at 11.52% CAGR over 2026-2031.

This report is Segmented by Drug Type (Vismodegib, Sonidegib, Glasdegib, Others), Application (BCC, AML, Medulloblastoma, Gorlin Syndrome), Route (Oral, Topical, Injectable), Distribution (Hospital, Retail, Online Pharmacies), End User (Hospitals, Clinics, Research Institutes, Homecare), and Geography (North America, Europe, South America, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Hedgehog Pathway Inhibitors Market Trends and Insights

Rising Burden of Basal Cell Carcinoma and AML in Aging and UV-Exposed Populations

The basic demand engine for the hedgehog pathway inhibitors market is demographic, because the treated population sits heavily in older age groups where both skin cancer burden and treatment complexity are rising. Global new BCC cases among adults aged 55 and above are increasing, and projections show sharper increases ahead in the oldest age bands, with the United States, Brazil, and China carrying the largest absolute caseloads. The hedgehog pathway inhibitors market also benefits from a less visible but important expansion in immunosuppressed patients, since transplant recipients and people on long-term biologics develop BCC at materially higher rates than immunocompetent populations, which widens the locally advanced pool that can move toward drug therapy.

On the leukemia side, glasdegib is positioned for adults aged 75 years or older or for adults with comorbidities that preclude intensive chemotherapy, which aligns the product with the oldest and fastest-growing AML treatment cohort. Real-world practice has reinforced that logic, with a 50% combined remission rate reported in first-line community oncology use of glasdegib-based care, which supports a durable clinical and commercial role for the hedgehog pathway inhibitors market in frail AML patients. As these older and medically complex populations expand, the hedgehog pathway inhibitors market gains not just more patients, but more patients who fit current label and care-setting requirements.

Biomarker-Guided Patient Stratification Expands Addressable Cohorts

Patient selection is becoming more precise, and that precision can materially improve conversion from diagnosis to treatment within the hedgehog pathway inhibitors market. In PTCH1-mutated tumors, vismodegib produced a 100% response rate in Gorlin syndrome patients, compared with a 43% response rate in unselected advanced BCC cohorts, which shows how strongly molecular context can change treatment value. That gap matters because broader genomic screening in dermatology and oncology practice can bring high-response patients into therapy earlier, rather than leaving hedgehog inhibitors for the latest refractory settings.

The hedgehog pathway inhibitors market also stands to benefit from the gradual normalization of pathway-level testing, since clinicians gain more confidence when target activation and likely response can be tied to a defined mutation pattern. Liquid biopsy platforms detecting circulating PTCH1 and SMO variants reached an 87.5% concordance rate with tissue-based testing, which lowers sampling friction and could increase screening rates in both skin cancer and leukemia programs. As noninvasive testing improves and becomes easier to use at scale, the hedgehog pathway inhibitors market can add patients through better selection rather than through label expansion alone.

Musculoskeletal and Taste-Related Toxicity Drives Discontinuation

Toxicity remains one of the strongest limits on the hedgehog pathway inhibitors market because it reduces treatment duration even when eligible patient numbers continue to rise. In a multicenter real-world study, treatment interruption due to adverse events occurred in 47.4% of vismodegib recipients and in 13.2% of sonidegib recipients, which highlights a very large persistence gap within the same therapeutic class. That gap is commercially meaningful because sonidegib's longer half-life allows more flexibility through intermittent dosing, while vismodegib often forces a harder trade-off between continuous disease control and tolerability. The adverse event burden is not limited to controlled studies, and real-world pharmacovigilance work continues to show a strong signal for muscle spasms and dysgeusia in oral hedgehog inhibitor exposure.

The hedgehog pathway inhibitors market loses value whenever patients stop before complete response, because the treated population is large enough to create demand, but each patient contributes fewer therapy months than expected. Until lower-toxicity formats or better management protocols become routine, the hedgehog pathway inhibitors market will keep facing a structural persistence problem rather than a simple awareness problem.

Other drivers and restraints analyzed in the detailed report include:

- Combination Regimens Extend Clinical Utility Beyond Monotherapy

- Topical and Locally Delivered Reformulations Reduce Systemic Toxicity

- SMO Mutation-Mediated Resistance Limits Duration of Response

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vismodegib retained 42.31% of the hedgehog pathway inhibitors market share in 2025, reflecting its first-mover position and its durable use in locally advanced BCC where physician familiarity remains high. Its position in the hedgehog pathway inhibitors market is still supported by broad clinical recognition in BCC and by a long-established prescribing base that newer agents must displace case by case. Real-world data also continue to confirm that vismodegib remains clinically active in advanced BCC, which explains why share has held despite the class-wide toxicity profile. Sonidegib competes with a clearer tolerability message, and real-world analysis showed sonidegib-treated patients were 52% less likely to experience muscle spasms and 71% less likely to develop taste-related conditions than vismodegib-treated patients over nine months of follow-up. That difference does not overturn vismodegib's entrenched base, but it does give the hedgehog pathway inhibitors market a visible product-level split between scale and tolerability.

Glasdegib is the fastest-growing drug type in the hedgehog pathway inhibitors market at a 12.38% CAGR from 2026 to 2031. Its growth is linked to investigation across leukemia settings beyond AML, including myelofibrosis, myelodysplastic syndromes, and chronic myelomonocytic leukemia, which broadens the clinical narrative around the class without relying on additional BCC exposure. The hedgehog pathway inhibitors industry also gains a useful diversification point from glasdegib because its hematology role reduces dependence on skin cancer alone. A real-world study across U.S. community oncology practices reported a 50% combined remission rate in first-line glasdegib-treated AML patients, which supports the product's utility beyond academic trial centers. The "other hedgehog pathway inhibitors" bucket remains small today, but taladegib's orphan designation in idiopathic pulmonary fibrosis shows how the hedgehog pathway inhibitors market is extending into adjacent disease areas that could become commercially meaningful over time.

Basal cell carcinoma accounted for 76.24% of the hedgehog pathway inhibitors market size in 2025, which shows how heavily current revenue still depends on advanced BCC treatment pathways. This concentration exists because drug therapy mainly enters when surgery or radiation cannot be used, which gives the hedgehog pathway inhibitors market a protected base in a clearly defined unmet-need population. Coverage rules reinforce that structure, and prior authorization frameworks continue to tie reimbursement closely to labeled use and specialist oversight rather than broad community prescribing. AML remains a distinct secondary application within the hedgehog pathway inhibitors market because glasdegib serves older or medically frail patients who are not candidates for intensive chemotherapy, which places the product in a clinically different and institutionally concentrated segment. Medulloblastoma is smaller in current revenue terms, but response rates near 50% in PTCH1-variant SHH-subgroup tumors show why genotype-gated use remains relevant in selected cases.

Gorlin syndrome is the fastest-growing application in the hedgehog pathway inhibitors market at a 13.52% CAGR from 2026 to 2031. The segment stands out because it requires indefinite suppression of new lesion formation, so revenue can build from repeated prevention rather than from episodic treatment lines alone. That profile makes Gorlin syndrome one of the most underpenetrated parts of the hedgehog pathway inhibitors market, especially if topical prevention therapy reaches approval. Sol-Gel Technologies completed enrollment in the Phase 3 SGT-610 study, and top-line results are expected in Q4 2026, which keeps the first prevention-focused commercial pathway firmly in view. If approved, that therapy would open a prevention pool distinct from the existing advanced BCC treatment pool, which would let the hedgehog pathway inhibitors market expand without relying on the same reimbursement logic that governs current oncology use.

Complete Report Scope:

- By Drug Type

- Vismodegib

- Sonidegib

- Glasdegib

- Other Hedgehog Pathway Inhibitors

- By Application

- Basal Cell Carcinoma

- Acute Myeloid Leukemia

- Medulloblastoma

- Gorlin Syndrome

- Other Applications

- By Route of Administration

- Oral

- Topical

- Injectable

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Other Distribution Channels

- By End User

- Hospitals

- Specialty Clinics

- Research Institutes

- Homecare Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 41.52% of the hedgehog pathway inhibitors market share in 2025, making it the clear regional leader. The United States drove most of that position because it recorded the world's highest BCC incidence burden. The region also benefits from a specialist oncology infrastructure that is well aligned with referral of locally advanced BCC and with branded oncology reimbursement. Regulatory support has helped as well, and the 2025 draft-guidance update around accelerated approval and post-marketing confirmation reinforced a framework that can still support earlier entry for oncology drugs while maintaining evidence requirements.

Asia-Pacific within the hedgehog pathway inhibitors market size is projected to expand at a 13.55% CAGR from 2026 to 2031, making it the fastest-growing regional block. Growth is being supported by aging populations in China and Japan, rising UV-linked exposure in several outdoor-working populations, and stronger access to specialty oncology medicines. China's regulatory reforms have shortened local approval timelines for oncology products with prior Western approvals, which improves the path from global evidence to local commercialization. Japan has also added region-specific support, with a Phase Ib/II glasdegib study in AML patients ineligible for intensive chemotherapy reporting a disease-modifying response rate of 46.7% in the expansion cohort. China's BCC caseload among adults aged 55 and above shows how demographic change is creating a much larger future base for the hedgehog pathway inhibitors market in the region.

The remaining geographies remain smaller in current revenue terms, but they are becoming more relevant to the hedgehog pathway inhibitors market over time. The Gulf Cooperation Council countries combine high UV exposure with improving oncology capacity, although reimbursement remains fragmented across systems. South Africa remains the most developed sub-Saharan entry point for the hedgehog pathway inhibitors market because private healthcare channels and academic medical centers provide the clearest route to specialized oncology use.

- BridgeBio Pharma Inc

- Endeavor BioMedicines

- HedgePath Pharmaceuticals Inc.

- Impact Therapeutics Inc.

- Kintor Pharmaceutical Ltd.

- Mayne Pharma Group Ltd.

- Merck

- Novartis

- Pfizer

- Roche

- Sol-Gel Technologies Ltd.

- Sun Pharmaceuticals Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Basal Cell Carcinoma and AML in Aging and UV-Exposed Populations

- 4.2.2 Biomarker-Guided Patient Stratification Expands Addressable Cohorts

- 4.2.3 Combination Regimens Extend Clinical Utility Beyond Monotherapy

- 4.2.4 Topical And Locally Delivered Reformulations Reduce Systemic Toxicity

- 4.2.5 Orphan and Accelerated Pathways Shorten Development Timelines

- 4.2.6 Real-World Evidence Strengthens Long-Tail Adoption and Persistence

- 4.3 Market Restraints

- 4.3.1 Musculoskeletal and Taste-Related Toxicity Drives Discontinuation

- 4.3.2 SMO Mutation-Mediated Resistance Limits Duration of Response

- 4.3.3 Narrow Reimbursable Label and Surgery or Radiation Substitution Caps Uptake

- 4.3.4 Limited Late-Stage Pipeline Depth and High Attrition in Niche Indications

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Type

- 5.1.1 Vismodegib

- 5.1.2 Sonidegib

- 5.1.3 Glasdegib

- 5.1.4 Other Hedgehog Pathway Inhibitors

- 5.2 By Application

- 5.2.1 Basal Cell Carcinoma

- 5.2.2 Acute Myeloid Leukemia

- 5.2.3 Medulloblastoma

- 5.2.4 Gorlin Syndrome

- 5.2.5 Other Applications

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Topical

- 5.3.3 Injectable

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.4.4 Other Distribution Channels

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Specialty Clinics

- 5.5.3 Research Institutes

- 5.5.4 Homecare Settings

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 BridgeBio Pharma Inc

- 6.3.2 Endeavor BioMedicines

- 6.3.3 HedgePath Pharmaceuticals Inc.

- 6.3.4 Impact Therapeutics Inc.

- 6.3.5 Kintor Pharmaceutical Ltd.

- 6.3.6 Mayne Pharma Group Ltd.

- 6.3.7 Merck KGaA (Sigma-Aldrich)

- 6.3.8 Novartis AG

- 6.3.9 Pfizer Inc.

- 6.3.10 Roche Holding AG

- 6.3.11 Sol-Gel Technologies Ltd.

- 6.3.12 Sun Pharmaceutical Industries Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment