|

시장보고서

상품코드

2072719

독일의 보청기 판매점 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Germany Hearing Aid Retailers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

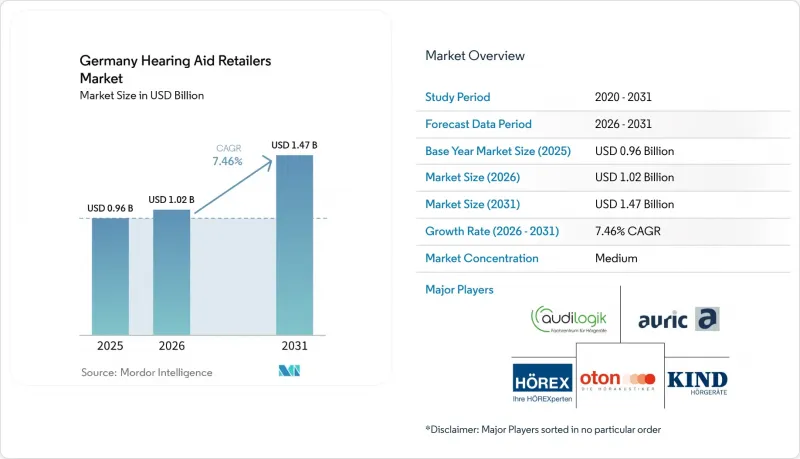

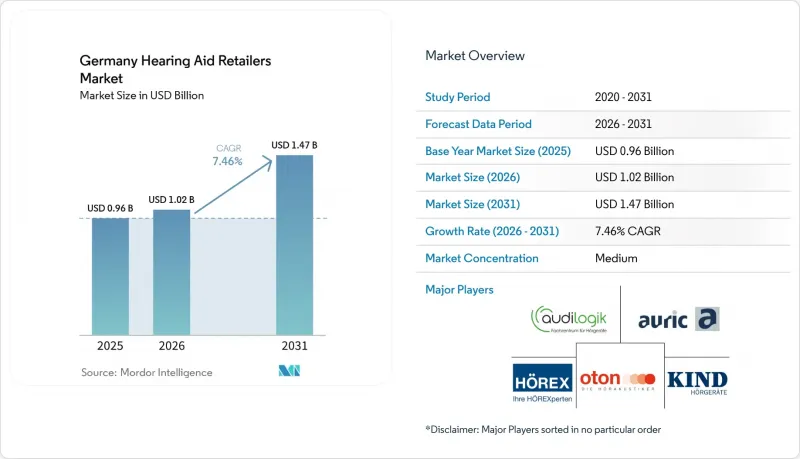

Mordor Intelligence에 의하면, 독일의 보청기 판매점 시장 규모는 2025년 9억 6,000만 달러로 평가되었고, 2026년에는 10억 2,000만 달러로 추정되고, 2026-2031년 CAGR 7.46%로 성장을 지속할 전망이며, 2031년까지 14억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형별(귀내형, 수화기 귀내형, 귀걸이형, 외이도형 보청기), 기술별(디지털, 아날로그), 환자층별(18-64세 성인, 65세 이상 고령자, 0-17세 소아) 및 지역별(독일)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일의 보청기 판매점 시장 동향 및 인사이트

독일의 고령화로 인해 보청기 수요가 있는 계층이 확대되고 있습니다.

독일의 보청기 판매점 시장은 보청기 수요의 핵심을 이루는 고령층의 꾸준한 증가에 힘입어 성장하고 있습니다. Destatis는 2025년 12월, 67세 이상 고령자가 2035년까지 전국 인구의 25%를 차지하게 될 것이라고 발표했습니다. 이는 2024년의 20%에서 증가할 것으로 전망됩니다. 또한, 'EuroTrak Germany 2025' 보고서에 따르면, 독일에서는 911만 명이 스스로를 청각장애인으로 인식하고 있으며, 이는 다음 고령화 물결이 본격화되기 전부터 이미 잠재 고객 기반이 충분히 크다는 것을 의미합니다. 보급률은 여전히 완전한 보급과는 거리가 먼 수준에 머물러 있어, 독일 보청기 판매점 시장에는 첫 구매자와 교체 수요자 양쪽 모두에서 성장 여지가 있습니다. 이러한 조합으로 인해 고령화는 단순한 완만한 배경 요인에 그치지 않고, 예측 기간 동안 소매 판매량을 직접 견인하는 요인이 됩니다.

법정 의료비 환급 제도가 첫 구매를 촉진하는 데 기여합니다.

독일의 보청기 판매점 시장은 많은 사용자에게 첫 구매의 장벽을 낮춰주는 의료 지원 제도의 혜택을 받고 있습니다. 독일 사회법전 제5편(SGB V) 제33조에 근거한 법정 제도에서는 보청기가 여전히 의료 급여 대상으로 분류되고 있으나, 개정된 '보조기구 지침(Hilfsmittel-Richtlinie)' 또한 2025년 6월의 인증 권고안에 따라, 계약 제공업체에 대한 품질 및 서류 제출 요건이 강화되었습니다. 『EuroTrak Germany 2025』 조사에 따르면, 청각 장애가 있음에도 보청기를 사용하지 않는 사람들의 64%가 자신의 급여 수급 자격에 대해 알지 못했습니다. 이는 구매 장벽이 단순한 경제적 문제가 아니라, 여전히 인지도가 낮기 때문임을 보여줍니다. 따라서, 지급 자격을 명확하게 설명할 수 있는 소매업체는 가계 지출 패턴에 큰 변화가 생길 때까지 기다릴 필요 없이 판매량을 늘릴 수 있습니다. 또한, 새로운 규정 준수 부담으로 인해 임상 및 관리 측면의 체제가 취약한 사업자보다, 체계적으로 조직된 체인점이나 문서 관리가 잘 갖춰진 독립 소매업체가 유리한 입장에 있습니다.

가격 투명화로 인해 소매업체의 이익률이 압박받고 있습니다.

독일의 보청기 판매점 시장은 수요가 견조함에도 불구하고 뚜렷한 이익률 문제에 직면해 있습니다. 연방사회법원(Bundessozialgericht)은 2025년 6월, 정액 상한액(Festbetrag)을 초과하는 보청기가 보조금 지원 대상이 되는 조건에 대해 판결을 내렸으며, 이러한 결정으로 인해 판매 현장에서 정보에 정통한 구매자의 협상력이 강화되고 있습니다. 이러한 압박은 오프라인 매장을 운영하는 소매업체들에게 더욱 가혹하게 다가오고 있습니다. 왜냐하면 그들의 비즈니스 모델에는 피팅룸, 임상 장비, 청력 검사 업무, 지역 임대료 등의 비용이 포함되어 있는데, 이러한 비용은 디지털 전용 모델에서는 같은 형태로 발생하지 않기 때문입니다. 대형 체인점은 규모의 경제, 조달 능력, 그리고 표준화된 업무 프로세스를 통해 이러한 비용의 일부를 상쇄할 수 있습니다. 따라서 독일 보청기 판매점 시장에서 소규모 독립 매장들은 고객 수요 자체보다 중저가 가격 책정 측면에서 더 큰 압박에 직면해 있습니다.

부문별 분석

2025년 시점에서 독일 보청기 판매점 시장에서 '귀 안쪽형(RITE)'이 시장 점유율은 72.23%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 9.58%로 성장할 것으로 전망됩니다. 이러한 장점은 폭넓은 착용 범위를 지원할 수 있는 형태라는 점 외에도, 충전 기능, 블루투스 연결, 그리고 수신기를 장기간에 걸쳐 쉽게 교체할 수 있다는 점과도 잘 부합하고 있음을 반영하고 있습니다. 독일 보청기 판매점 시장에서 이러한 점 때문에 RITE는 혁신에 대한 투자와 소매업체의 추천 패턴이라는 두 가지 측면에서 주요 대상으로 주목받고 있습니다. 귀걸이형(BTE) 보청기는 중증에서 극중증의 난청, 내구성과 적응성이 요구되는 소아용 피팅 과정에서 여전히 중요한 역할을 하고 있습니다.

귀 안쪽형(ITE) 보청기는 성능 면에서의 격차가 좁혀짐에 따라 다시 프리미엄 제품으로서의 위상을 되찾아가고 있습니다. 2026년 1월 독일에서 출시된 오티콘사의 'Zeal'은 거의 눈에 띄지 않는 ITE 디자인이면서도 LE Audio, Auracast, 충전 기능, 당일 피팅 기능을 모두 갖출 수 있음을 보여주며, 이를 통해 눈에 띄지 않는 디자인과 기능성 사이의 기존의 상충 관계가 완화되었습니다. 이도형 보청기는 여전히 틈새 전문 분야이지만, 일상 생활에서 눈에 덜 띄는 맞춤형 보청기를 중요하게 여기는 성인들에게는 여전히 중요한 선택지입니다. 독일의 보청기 소매 업계 전반에서는 단순히 기기의 크기를 줄이는 데 그치지 않고, 착용 편의성, 연결성, 장기적인 서비스 호환성을 모두 갖춘 제품 구성으로 전환해 가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the germany hearing aid retailers market size is expected to grow from USD 0.96 billion in 2025 to USD 1.02 billion in 2026 and is forecast to reach USD 1.47 billion by 2031 at 7.46% CAGR over 2026-2031.

This report is Segmented by Product Type (In-The-Ear, Receiver-In-The-Ear, Behind-The-Ear, Canal Hearing Aids), Technology (Digital, Analog), Patient Type (Adults 18-64, Geriatric 65+, Pediatric 0-17 Years), and Geography (Germany). The Market Forecasts are Provided in Terms of Value (USD).

Germany Hearing Aid Retailers Market Trends and Insights

Germany's Aging Population is Expanding the Addressable Hearing-Loss Pool

The Germany hearing aid retailers market is being lifted by a steady increase in older age groups, which are the core population for hearing care demand. Destatis stated in December 2025 that people aged 67 and older will account for 25% of the national population by 2035, compared with 20% in 2024. EuroTrak Germany 2025 also reported that 9.11 million people in Germany describe themselves as hearing impaired, which means the addressable base is already large before the next wave of aging fully arrives. Adoption still sits well below full penetration, so the Germany hearing aid retailers market has room to grow from both first-time users and replacement buyers. That combination keeps aging from being a slow background factor and turns it into a direct retail volume driver through the forecast period.

Statutory Reimbursement Sustains First-Purchase Conversion

The Germany hearing aid retailers market benefits from a medical reimbursement structure that reduces the first-purchase barrier for a large share of users. Germany's statutory system under §33 SGB V continues to frame hearing aids as a covered medical benefit, while the updated Hilfsmittel-Richtlinie and the June 2025 qualification recommendations tightened quality and documentation expectations for contracted providers. EuroTrak Germany 2025 found that 64% of hearing-impaired non-users did not know about their reimbursement eligibility, which shows that awareness remains a conversion issue rather than pure affordability alone. Retailers that explain eligibility clearly can therefore add volume without waiting for a major shift in household spending patterns. The new compliance burden also favors organized chains and better-documented independents over weaker operators with limited clinical and administrative depth.

Price Transparency is Compressing Retailer Margins

The Germany hearing aid retailers market faces a clear margin issue even while demand remains healthy. The Bundessozialgericht issued rulings in June 2025 on the conditions under which above-Festbetrag devices qualify for co-funding, and those decisions strengthen the negotiating position of better-informed buyers at the point of sale. That pressure is harder on store-based retailers because their model includes fitting rooms, clinical equipment, audiological labor, and local lease costs that digital-only models do not carry in the same way. Large chains can absorb some of this through scale, procurement leverage, and standardized workflows. Smaller independents in the Germany hearing aid retailers market, therefore, face more pressure on mid-tier pricing than on customer demand itself.

Other drivers and restraints analyzed in the detailed report include:

- Bluetooth, App-Based Fitting, and Rechargeable Devices Are Widening Upgrade Demand

- Omnichannel Retail Is Improving Conversion from Awareness to Trial

- Skilled Hearing-Care Talent Scarcity Limits Branch Productivity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Receiver-in-the-ear accounted for 72.23% of the Germany hearing aid retailers market share in 2025 and is projected to grow at a 9.58% CAGR through 2031. That lead reflects a format that works across a wide fitting range and aligns well with rechargeability, Bluetooth connectivity, and easy receiver replacement over time. In the Germany hearing aid retailers market, this makes RITE the main destination for both innovation spending and retailer recommendation patterns. Behind-The-Ear devices still hold an important role for severe-to-profound hearing loss and for pediatric fitting pathways that need durability and adaptability.

In-The-Ear devices are moving back into the premium conversation as their performance gap narrows. Oticon's Zeal launch in Germany in January 2026 showed that an almost invisible ITE design can now include LE Audio, Auracast, rechargeability, and same-day fitting, which weakens the older tradeoff between discretion and capability. Canal devices remain a narrower specialist format, but they keep relevance for adults who value a more discreet custom fit in daily use. Across the Germany hearing aid retailers industry, the product mix is moving toward formats that combine comfort, connectivity, and long-term service compatibility rather than simply smaller device size.

Complete Report Scope:

- By Product Type

- In-The-Ear Hearing Aids

- Receiver-In-The-Ear Hearing Aids

- Behind-The-Ear Hearing Aids

- Canal Hearing Aids

- By Technology

- Digital

- Analog

- By Patient Type

- Adults (18-64 Years)

- Geriatric Population (65+ Years)

- Pediatric Population (0-17 Years)

List of Companies Covered in this Report:

- Amplifon

- AUDILOGIK

- auric Management GmbH

- Fielmann

- GEERS

- Gerland & Mellentin

- Hansaton

- Hearly.de

- HOREX Hor-Akustik eG

- HORGERATE SEIFERT

- Horakustik Brasgalla

- Horluchs Horgerate

- HorPartner GmbH

- Horsysteme Heinen & Ricking

- Horzentrum Finowfurt

- KIND GmbH & Co. KG

- Meister Beuchert

- Neuroth

- Oberlin Horpunkt

- OTON Die Horakustiker

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Germany's Aging Population is Expanding the Addressable Hearing-Loss Pool

- 4.2.2 Statutory Reimbursement Sustains First-Purchase Conversion

- 4.2.3 Bluetooth, App-Based Fitting, and Rechargeable Devices Are Widening Upgrade Demand

- 4.2.4 Omnichannel Retail Is Improving Conversion from Awareness to Trial

- 4.2.5 Tele-Audiology Is Reducing Friction in Follow-Up Care and Servicing

- 4.2.6 Private-Pay Premiumization is Increasing Average Selling Prices

- 4.3 Market Restraints

- 4.3.1 Price Transparency is Compressing Retailer Margins

- 4.3.2 Skilled Hearing-Care Talent Scarcity Limits Branch Productivity

- 4.3.3 Digital Comparison Platforms Are Raising Customer Acquisition Costs

- 4.3.4 MDR And Reimbursement Documentation Add Operating Complexity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 In-The-Ear Hearing Aids

- 5.1.2 Receiver-In-The-Ear Hearing Aids

- 5.1.3 Behind-The-Ear Hearing Aids

- 5.1.4 Canal Hearing Aids

- 5.2 By Technology

- 5.2.1 Digital

- 5.2.2 Analog

- 5.3 By Patient Type

- 5.3.1 Adults (18-64 Years)

- 5.3.2 Geriatric Population (65+ Years)

- 5.3.3 Pediatric Population (0-17 Years)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Amplifon

- 6.3.2 AUDILOGIK

- 6.3.3 auric Management GmbH

- 6.3.4 Fielmann

- 6.3.5 GEERS

- 6.3.6 Gerland & Mellentin

- 6.3.7 Hansaton

- 6.3.8 Hearly.de

- 6.3.9 HOREX Hor-Akustik eG

- 6.3.10 HORGERATE SEIFERT

- 6.3.11 Horakustik Brasgalla

- 6.3.12 Horluchs Horgerate

- 6.3.13 HorPartner GmbH

- 6.3.14 Horsysteme Heinen & Ricking

- 6.3.15 Horzentrum Finowfurt

- 6.3.16 KIND GmbH & Co. KG

- 6.3.17 Meister Beuchert

- 6.3.18 Neuroth

- 6.3.19 Oberlin Horpunkt

- 6.3.20 OTON Die Horakustiker

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment