|

시장보고서

상품코드

2072720

GHG 프로토콜 소프트웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)GHG Protocol Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

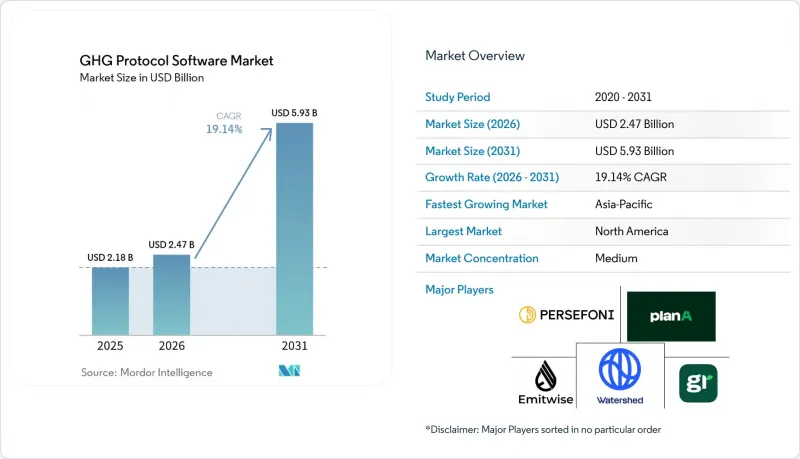

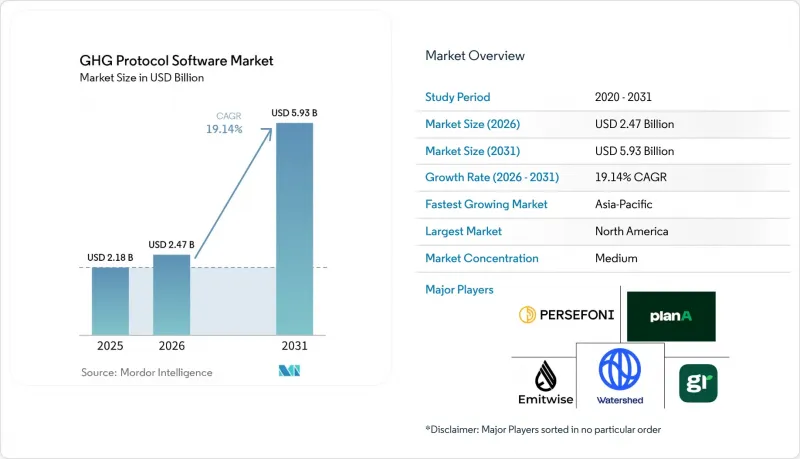

Mordor Intelligence에 의하면, GHG 프로토콜 소프트웨어 시장 규모는 2025년 21억 8,000만 달러로 평가되었고, 2026년에는 24억 7,000만 달러로 추정되고, 2031년까지 59억 3,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 19.14%로 성장할 전망입니다.

본 보고서는 도입 형태별(클라우드 기반, 온프레미스형, 하이브리드형), 기업 규모별(대기업, 중소기업), 솔루션 분야별(탄소 회계 및 인벤토리 관리, ESG 보고 및 공시 관리 등), 최종 사용자 산업별(공업 제조 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 온실가스 프로토콜 소프트웨어 시장 동향 및 인사이트

스코프 1, 스코프 2 및 스코프 3에 대한 공시 의무화를 위한 규제 동향

공시 의무화 규제로 인해 GHG 프로토콜 소프트웨어 시장의 구매자층에 변화가 생겼습니다. EU의 CSRD(기업 지속가능성 보고 지침)는 2024년 1월 1일에 발효되며, EU 역내에서 대규모 사업을 전개하는 비EU 기업 그룹을 포함해 약 5만 개의 기업이 적용 대상이 됩니다. ESRS E1에서는 GHG 프로토콜 스코프 3 기준을 직접 참조한 스코프 1, 스코프 2 및 중요한 스코프 3에 대한 공시가 요구됩니다. 캘리포니아주의 SB 253 법안 또한 또 하나의 중요한 계기가 되었습니다. 캘리포니아주 대기자원국(CARB)은 2026년 2월 26일 초기 시행 지침을 채택하고, 대상 사업체에 대한 스코프 1 및 스코프 2 공개 제출 기한을 2026년 8월 10일로 확정했습니다. 이러한 규정은 최대 규모의 보고 기업에 그치지 않고, 대형 구매 기업이 스코프 3 카테고리 1 의무를 이행하는 과정에서 공급업체에 배출량 데이터 제공을 요구하게 됨에 따라 더 광범위한 영향을 미치고 있습니다. 이러한 파급 효과로 인해, GHG 프로토콜 대응 소프트웨어 시장의 확산 속도는 단순한 규제만 고려했을 때 예상되는 것보다 더 빠르게 진행되고 있으며, 특히 기업의 조달 프로그램 참여 자격을 유지해야 하는 공급업체에서 이러한 현상이 두드러지게 나타납니다.

CSRD, IFRS S2 및 캘리포니아주 규정 준수 워크플로우에서 GHG 프로토콜과의 일관성

GHG 프로토콜 소프트웨어 시장은 여러 보고 시스템에 동일한 산정 체계가 통합되어 있다는 사실로부터도 혜택을 받고 있습니다. ISSB가 발간하고 2024년 1월 1일부터 시행되는 IFRS S2는 관할 당국이 별도로 지시하지 않는 한 GHG 프로토콜 기업 표준의 사용을 명시적으로 의무화하고 있으며, 2025년 개정안에서도 이러한 핵심적인 의존 관계에는 변경이 없었습니다. GHG 프로토콜은 2025년 1월, 이러한 의존 관계가 이미 다양한 국가의 규정 및 도입 계획에 반영되어 있다고 밝혔으며, 이는 공급업체에게 제품 설계 및 고객 유지를 위한 견고한 기반을 제공합니다. 또한, 2025년 12월에 공포된 개정 ESRS 규정은 IFRS S1 및 S2와의 일관성을 한층 더 높이고, 재무 관리형 통합의 필요성을 강화함으로써 상호 운용성도 높아졌습니다. 이로 인해 독자적인 방식보다는 표준화된 플랫폼이 우선시되게 됩니다. 이러한 추세에 따라 GHG 프로토콜 소프트웨어 시장에서 단일 감사 대응형 배출량 인벤토리의 가치가 높아지고 있습니다. 왜냐하면 단일 핵심 데이터셋으로 여러 보고 의무를 동시에 충족할 수 있기 때문입니다.

다층적 공급망 내 스코프 3 데이터의 격차

스코프 3 데이터 수집은 여전히 GHG 프로토콜 소프트웨어 시장에서 가장 큰 구조적 제약 요인으로 남아 있습니다. Sphera가 2026년 2월에 실시한 조사에 따르면, 경영진의 45%는 스코프 3 데이터의 정확성에 대해 제한적인 신뢰만을 가지고 있는 반면, 89%는 보다 광범위한 보고를 계획하고 있는 것으로 나타났습니다. 이는 보고에 대한 의욕이 여전히 데이터 품질을 앞지르고 있음을 보여줍니다. EcoVadis는 2026년 4월, 공급업체의 투명성을 높이기 위해 '카본 데이터 네트워크'을 확대하겠다고 발표했습니다. 이는 여전히 파편화된 공급망 전반에 걸쳐 일관된 업스트림 정보를 수집하는 것이 어렵다는 점을 반영하고 있습니다. 2026년 3월 31일자 GHG 프로토콜 1단계 진행 보고서에 따르면, 개정된 스코프 3 기준에서 데이터 품질 수준별 보다 명확한 공시가 제안되고 있으며, 이에 따라 많은 기존 소프트웨어 워크플로우를 재조정해야 할 필요가 있습니다. 단기적으로는 이러한 전환에 따른 부담이 GHG 프로토콜 소프트웨어 시장의 플랫폼 확장 결정을 지연시킬 가능성이 있지만, 장기적으로는 더 우수한 공급업체 데이터 도구에 대한 수요를 높일 것으로 보입니다.

부문별 분석

2025년, 온실가스(GHG) 프로토콜 소프트웨어 시장에서 클라우드 기반 솔루션의 도입이 65.23%의 점유율을 차지했습니다. 이러한 우위는 막대한 인프라 투자 없이도 사업체나 관할 구역을 넘나들며 확장 가능한 소프트웨어의 매력이 반영된 결과입니다. 클라우드 시스템은 자회사의 신속한 도입, 표준화된 보고 템플릿, 그리고 지속가능성, 재무, 조달 팀 간의 원활한 협력을 필요로 하는 다국적 기업의 운영 모델에 부합합니다. 또한, GHG 프로토콜 소프트웨어 시장은 멀티테넌트형 플랫폼이 사내에서 대규모 업그레이드를 거치지 않고도 빈번한 규제 변경에 대응할 수 있다는 점에서도 혜택을 보았습니다. 이러한 장점은 기업들이 CSRD, 캘리포니아주 규정 및 ISSB와 관련된 광범위한 도입에 대응해 나가는 데 있어 중요했습니다. 많은 구매자들은 초기 자본 부담을 줄이면서도 기능 확장을 신속하게 지원할 수 있다는 점 때문에 구독형 도입을 선호했습니다.

하이브리드형 도입은 2031년까지 연평균 성장률(CAGR) 20.12%를 나타낼 것으로 예측되며, 온실가스(GHG) 프로토콜 소프트웨어 시장에서 가장 빠르게 성장하는 도입 모델로 자리매김하고 있습니다. 이러한 경향은 특히, 탄소 데이터 등록을 재무 등급의 환경에서 관리하면서도 공급업체와의 연계 및 분석 기능을 클라우드 상에서 유지하고자 하는 기업들에게 있어, 제어성과 유연성 간의 실용적인 균형을 반영한 것입니다. SAP는 2026년 5월, Green Ledger가 SAP S/4HANA에 탄소 데이터를 등록하고, 보고서 작성 및 협업에는 SAP Business Technology Platform을 활용하고 있다고 발표했습니다. 이는 하이브리드 설계가 지지를 얻고 있는 이유를 여실히 보여줍니다. 에너지, 유틸리티, 정부 기관 등 규제가 엄격한 분야에서는 내부 통제 및 데이터 주권과 관련된 요건이 여전히 까다로워, 온프레미스형 시스템이 여전히 일정한 입지를 차지하고 있습니다. 그렇긴 하지만, GHG 프로토콜 소프트웨어 업계 동향은 현재 완전히 격리된 환경이 아닌, 보호된 핵심 기록과 유연한 디지털 인터페이스를 결합한 아키텍처로 나아가고 있습니다.

2025년에는 대기업이 매출의 67.12%를 차지하며, GHG 프로토콜 소프트웨어 시장에서 주도적인 위치를 확립했습니다. 그 규모, 법적 위험, 그리고 여러 사업체에 걸친 보고 요구 사항으로 인해, 현재 필요한 배출량 데이터의 양을 수작업으로 처리하는 데에는 한계가 있었습니다. 또한, 이러한 구매 기업들은 강력한 보증 관리, 감사 문서 및 ERP 통합을 중시하는 체계적인 공급업체 선정 프로그램을 시행하는 경향이 있었습니다. 실제로 대기업들은 정보 공개뿐만 아니라 내부 통제, 연결 재무제표, 공급업체와의 협력에도 이 소프트웨어를 활용하고 있습니다. 이러한 복합적인 용도 덕분에, GHG 프로토콜 소프트웨어 시장에서 현재 지출의 핵심 축으로 자리매김하고 있습니다.

중소기업(SME) 시장 규모는 2031년까지 연평균 성장률(CAGR) 21.34%로 확대될 것으로 예상되며, 이러한 변화는 직접적인 규제와 마찬가지로 고객의 압력에 의해서도 크게 촉진되고 있습니다. 'GHG 프로토콜 기업 기준' 그리고 '스코프 3 프레임워크'로 인해 대기업은 공급업체에 데이터 제공을 요청하도록 압박받고 있으며, 이로 인해 현지 규제가 직접 적용되지 않는 경우라 하더라도 사실상 중소기업이 보고 체인에 임베디드되게 됩니다. 2026년 3월에 발표된 중소기업용 온실가스 인벤토리 작성 관련 프레임워크에서는 디지털 도구를 활용함으로써 ISO 14064에 부합하는 기록을 작성하는 데 필요한 노력을 대폭 줄일 수 있다고 지적하고 있으며, 이는 저사양 플랫폼 도입을 뒷받침하는 근거가 되고 있습니다. 이에 대해 각 벤더사는 소프트웨어에 단계별 도입 지원 및 자문 지원을 결합하여 대응하고 있으며, 이를 통해 중소기업은 대기업 규모의 사내 팀을 갖추지 않아도 조사 방법론의 요건을 충족할 수 있게 됩니다. 이는 GHG 프로토콜 소프트웨어 시장이 대기업을 대상으로 한 틈새 시장에서 보다 광범위한 공급업체 네트워크 플랫폼 부문으로 전환되고 있음을 보여주는 가장 명확한 징후 중 하나입니다.

지역별 분석

2025년, 북미는 온실가스(GHG) 프로토콜 소프트웨어 시장의 36.12%를 차지했으며, 최대 지역 시장이 되었습니다. 이 지역은 캘리포니아주가 GHG 프로토콜을 명확히 준수한 주 차원의 제도를 확립한 한편, 상장기업들이 보다 광범위한 기후 변화 정보 공시 의무에 대비하고 있었기 때문에 보고와 관련된 여러 가지 압력이 중첩되는 이점을 누렸습니다. 캘리포니아주 대기자원국(CARB)은 2026년 2월, SB 253의 시행이 다음 단계로 접어들었음을 확인하고, 자발적 보고에서 공식적인 준수 계획으로의 전환을 촉진했습니다. 또한, 북미에는 벤더들이 밀집해 있으며, 몇몇 주요 소프트웨어 공급업체들이 미국에 본사를 두고 있습니다. 이러한 집중을 통해 구현 주기의 단축, 통합 생태계의 강화, 그리고 더욱 경쟁력 있는 기업 대상 영업 활동이 뒷받침되었습니다.

유럽은 제공된 데이터상 지역별 점유율에서는 1위를 차지하지는 못했지만, GHG 프로토콜 소프트웨어 시장에서 여전히 가장 잘 정비된 규제 환경을 유지하고 있었습니다. CSRD의 단계적 도입에 따라 2024년부터 2028년에 걸쳐 수요 곡선이 완만하게 상승하는 경향이 나타나고 있으며, 이는 신규 구매자들이 한꺼번에가 아니라 순차적으로 시장에 계속 진입하고 있음을 의미합니다. 독일이 두드러지는 이유는 해당국의 산업 분야 수출 기업들이 사업체 차원의 보고 의무에 더해, 국경을 넘는 무역과 관련된 제품에 대한 탄소 보고 요구 사항에도 직면하고 있기 때문입니다. Carbmee가 2026년 6월에 발표한 온실가스 배출량 관리 소프트웨어에 대한 포지셔닝은 DACH 시장공급업체들이 규정 준수 보고와 업무 보고의 이러한 중복 부분을 활용하여 제품을 개발하고 있는 현실을 반영하고 있습니다. 또한 영국, 프랑스, 이탈리아, 스페인, 네덜란드에서도 제도적 및 규제적 압력으로 인해 소프트웨어 도입이 지속적으로 촉진되고 있어, 유럽 전체의 비즈니스 기회는 여전히 견조한 양상을 보이고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 26.41%를 기록하며 성장할 것으로 예상되며, 온실가스(GHG) 프로토콜 소프트웨어 시장에서 가장 빠르게 성장하는 지역 부문이 될 것입니다. 이러한 성장 가속화는 싱가포르, 일본, 호주, 홍콩, 말레이시아에서 ISSB 관련 보고 요건이 단계적으로 도입됨에 따라 주도되고 있으며, 이를 통해 2024년 이전에는 거의 확립되지 않았던 의무적인 수요 기반이 형성되었습니다. 중국은 기업의 보고가 산업 활동과 연동된 공장 차원의 배출량 모니터링에 주로 의존하기 때문에 추가적인 수요원이 되고 있습니다. 또한, 상장 기업에 대해 공시 요건의 확대와 온실가스(GHG) 보고 방식과의 일관성이 요구되는 가운데, 한국과 인도의 중요성도 커지고 있습니다. 중동 및 아프리카는 여전히 초기 단계 시장이지만, 2026년 2월 SINAI가 사우디아라비아의 Regional Voluntary Carbon Market Company와 제휴한 것은 정부 지원 기업 탈탄소화 플랫폼이 현지에서 수요를 창출하기 시작하고 있음을 보여줍니다. 남미는 제공된 부문별 데이터상에서는 그다지 두드러진 존재감을 보이지 않았지만, 세계 프레임워크의 도입과 국경을 초월한 공급망 보고를 통해 향후 플랫폼 확장과 지속적으로 연계될 가능성이 높다고 볼 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the GHG protocol software market size is expected to increase from USD 2.18 billion in 2025 to USD 2.47 billion in 2026 and reach USD 5.93 billion by 2031, growing at a CAGR of 19.14% over 2026-2031.

This report is Segmented by Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Area (Carbon Accounting and Inventory Management, ESG Reporting and Disclosure Management, and More), End-User Industry (Industrial Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global GHG Protocol Software Market Trends and Insights

Regulatory Push for Mandatory Scope 1, Scope 2, and Scope 3 Disclosures

Mandatory disclosure rules have changed the buyer base for the GHG Protocol Software Market. The EU CSRD took effect from January 1, 2024, and it covers an estimated 50,000 companies, including non-EU groups with substantial EU operations, with ESRS E1 requiring Scope 1, Scope 2, and significant Scope 3 disclosures that directly reference the GHG Protocol Scope 3 Standard. California SB 253 added another major trigger: the California Air Resources Board adopted initial implementation language on February 26, 2026, and confirmed filing deadlines for Scope 1 and Scope 2 disclosures for covered entities on August 10, 2026. These rules matter beyond the largest reporters, as large buyers now push emissions data requests down to their suppliers as they work through Scope 3 Category 1 obligations. That spillover is widening adoption in the GHG Protocol Software Market faster than direct regulation alone would suggest, especially for suppliers that need to remain eligible for enterprise procurement programs.

GHG Protocol Alignment in CSRD, IFRS S2, and California Compliance Workflows

The GHG Protocol Software Market is also benefiting from the fact that the same accounting framework is embedded across multiple reporting systems. IFRS S2, issued by the ISSB and effective from January 1, 2024, explicitly requires the use of the GHG Protocol Corporate Standard unless a jurisdiction directs otherwise, and the 2025 amendments did not change that core dependency. The GHG Protocol stated in January 2025 that this dependency is already embedded in rules or adoption plans across a wide range of countries, providing vendors with a durable foundation for product design and customer retention. Interoperability is also tightening, as amended ESRS rules issued in December 2025 moved further toward alignment with IFRS S1 and S2 and reinforced the need for financial-control-style consolidation, which favors standardized platforms over custom methods. That convergence increases the value of a single audit-ready emissions inventory in the GHG Protocol Software Market because a single core dataset can support multiple reporting obligations simultaneously.

Scope 3 Data Gaps Across Multi-Tier Supply Chains

Scope 3 data collection remains the biggest structural constraint on the GHG Protocol Software Market. Sphera found in February 2026 that 45% of business leaders had only limited confidence in the accuracy of Scope 3 data, even though 89% planned broader reporting, indicating that reporting ambition is still ahead of data quality. EcoVadis stated in April 2026 that it was expanding its Carbon Data Network to improve supplier transparency, reflecting the ongoing difficulty of collecting consistent upstream information across fragmented supply chains. The GHG Protocol Phase 1 Progress Update from March 31, 2026, proposed more explicit disclosure by data quality tier in the revised Scope 3 Standard, and that would require many existing software workflows to be recalibrated. In the near term, that transition burden can slow platform expansion decisions in the GHG Protocol Software Market even though it should increase long-run demand for better supplier data tools.

Other drivers and restraints analyzed in the detailed report include:

- Audit-Ready Carbon Data Demand Across Finance and Sustainability Teams

- AI-Assisted Emissions Factor Mapping and Data Reconciliation

- Fragmented Reporting Rules Across Jurisdictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment held 65.23% of the GHG Protocol Software Market share in 2025, and that lead reflected the appeal of software that can scale across entities and jurisdictions without heavy infrastructure investment. Cloud systems align with the operating model of multinational companies that need faster onboarding for subsidiaries, standardized reporting templates, and easier collaboration among sustainability, finance, and procurement teams. The GHG Protocol Software Market also benefited from multi-tenant platforms' ability to support frequent regulatory updates without requiring lengthy in-house upgrades. That advantage mattered as companies adjusted to the CSRD, California rules, and broader adoption linked to the ISSB. Many buyers also preferred subscription-based deployments because they reduced upfront capital commitments while supporting faster feature expansion.

Hybrid deployment is projected to grow at a 20.12% CAGR through 2031, which makes it the fastest-growing deployment model in the GHG Protocol Software Market. This pattern reflects a practical balance between control and flexibility, especially for companies that want carbon entries governed within finance-grade environments while keeping supplier collaboration and analytics in the cloud. SAP stated in May 2026 that Green Ledger posts carbon data in SAP S/4HANA, using SAP Business Technology Platform for reporting and collaboration, which illustrates why hybrid design is gaining traction. On-premises systems still retain a place in regulated sectors such as energy, utilities, and government, where internal control and data sovereignty requirements remain strict. Even so, the direction of the GHG Protocol Software industry now points toward architectures that combine protected core records with flexible digital interfaces rather than fully isolated environments.

Large enterprises accounted for 67.12% of revenue in 2025, giving them the leading position in the GHG Protocol Software Market. Their scale, legal exposure, and multi-entity reporting needs made manual processes too limited for the volume of emissions data now required. These buyers also tended to run structured vendor selection programs that favored strong assurance controls, audit documentation, and ERP integration. In practice, large companies use the software not just for disclosure, but also for internal control, consolidation, and supplier engagement. That combination kept them at the center of current spending across the GHG Protocol Software Market.

SMEs are projected to expand at a 21.34% CAGR through 2031, and this shift is being driven as much by customer pressure as by direct regulation. The GHG Protocol Corporate Standard and Scope 3 framework push large enterprises to request supplier data, which effectively brings smaller firms into the reporting chain even when local rules do not directly cover them. A March 2026 framework on SME GHG inventory development noted that digital tools can sharply reduce the effort required to build ISO 14064-aligned records, which supports the case for lower-configuration platforms. Vendors are responding by pairing software with guided onboarding and advisory support, so smaller firms can meet methodology requirements without enterprise-scale internal teams. This is one of the clearest signs that the GHG Protocol Software Market is moving from a large-enterprise niche into a broader supplier-network platform category.

Complete Report Scope:

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Area

- Carbon Accounting and Inventory Management

- ESG Reporting and Disclosure Management

- Scope 3 and Supply Chain Emissions Management

- Decarbonization Planning and Climate Analytics

- Assurance, Audit and Governance

- By End-user Industry

- Industrial Manufacturing

- Energy, Utilities and Resources

- BFSI

- Retail and Consumer Goods

- IT and Telecom

- Healthcare and Life Sciences

- Government and Public Sector

- Transportation and Logistics

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 36.12% of the GHG Protocol Software Market share in 2025, making it the largest regional market. The region benefited from overlapping reporting pressures, as California established a state-level regime explicitly aligned with the GHG Protocol while public companies prepared for broader climate disclosure obligations. The California Air Resources Board confirmed in February 2026 that SB 253 implementation had entered its next phase, reinforcing the shift from voluntary reporting to formal compliance planning. North America also had strong vendor density, with several major software providers headquartered in the United States. That concentration supported faster implementation cycles, stronger integration ecosystems, and more competitive enterprise sales activity.

Europe remained the most developed regulatory environment for the GHG Protocol Software Market, even though it did not lead in regional share in the data provided. The CSRD phase-in created a rolling demand curve from 2024 through 2028, meaning new buyer cohorts continue to enter the market in sequence rather than all at once. Germany stood out because industrial exporters there face both entity-level reporting duties and product carbon reporting needs tied to cross-border trade. Carbmee's June 2026 positioning on GHG emissions management software reflects how vendors in the DACH market are building products that leverage this overlap between compliance and operational reporting. The broader European opportunity also remains strong in the United Kingdom, France, Italy, Spain, and the Netherlands, where institutional and regulatory pressure continues to reinforce software adoption.

Asia-Pacific is projected to grow at a 26.41% CAGR through 2031, which makes it the fastest-growing regional segment in the GHG Protocol Software Market. This acceleration is being driven by phased adoption of ISSB-linked reporting across Singapore, Japan, Australia, Hong Kong, and Malaysia, which has created a mandatory demand base that was far less established before 2024. China adds another source of demand because enterprise reporting often depends on plant-level emissions monitoring tied to industrial operations. South Korea and India are also becoming more important as listed companies face widening disclosure expectations and alignment with GHG reporting methods. The Middle East and Africa remained earlier-stage markets, but SINAI's February 2026 partnership with Saudi Arabia's Regional Voluntary Carbon Market Company showed that government-backed enterprise decarbonization platforms are beginning to build local demand. South America was less prominent in the provided segment data, but global framework adoption and cross-border supply chain reporting are likely to keep it connected to future platform expansion.

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Plan A ESG GmbH

- Greenly SAS

- Green Project Technologies

- Sweep SAS

- Normative AB

- CarbonChain Ltd.

- SINAI Technologies, Inc.

- Sphera Solutions, Inc.

- Cority Software Inc.

- Benchmark Gensuite, LLC

- FigBytes Inc.

- Carbmee GmbH

- Terrascope Pte. Ltd.

- Greenstone+ Ltd

- ClimatePartner GmbH

- Novisto Inc.

- EcoRealities GmbH

- Workiva Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Push for Mandatory Scope 1, Scope 2, and Scope 3 Disclosures

- 4.2.2 Shift From Spend-Based Estimates to Primary Supplier Data

- 4.2.3 GHG Protocol Alignment in CSRD, IFRS S2, and California Compliance Workflows

- 4.2.4 Audit-Ready Carbon Data Demand Across Finance and Sustainability Teams

- 4.2.5 Carbon Ledger Integration With ERP and Financial Controls

- 4.2.6 AI-Assisted Emissions Factor Mapping and Data Reconciliation

- 4.3 Market Restraints

- 4.3.1 Fragmented Reporting Rules Across Jurisdictions

- 4.3.2 Scope 3 Data Gaps Across Multi-Tier Supply Chains

- 4.3.3 High Implementation and Change-Management Burden for Mid-Market Buyers

- 4.3.4 Assurance, Traceability, and Methodology Switching Complexity

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Solution Area

- 5.3.1 Carbon Accounting and Inventory Management

- 5.3.2 ESG Reporting and Disclosure Management

- 5.3.3 Scope 3 and Supply Chain Emissions Management

- 5.3.4 Decarbonization Planning and Climate Analytics

- 5.3.5 Assurance, Audit and Governance

- 5.4 By End-user Industry

- 5.4.1 Industrial Manufacturing

- 5.4.2 Energy, Utilities and Resources

- 5.4.3 BFSI

- 5.4.4 Retail and Consumer Goods

- 5.4.5 IT and Telecom

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Government and Public Sector

- 5.4.8 Transportation and Logistics

- 5.4.9 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Persefoni AI, Inc.

- 6.4.2 Watershed Technology, Inc.

- 6.4.3 Plan A ESG GmbH

- 6.4.4 Greenly SAS

- 6.4.5 Green Project Technologies

- 6.4.6 Sweep SAS

- 6.4.7 Normative AB

- 6.4.8 CarbonChain Ltd.

- 6.4.9 SINAI Technologies, Inc.

- 6.4.10 Sphera Solutions, Inc.

- 6.4.11 Cority Software Inc.

- 6.4.12 Benchmark Gensuite, LLC

- 6.4.13 FigBytes Inc.

- 6.4.14 Carbmee GmbH

- 6.4.15 Terrascope Pte. Ltd.

- 6.4.16 Greenstone+ Ltd

- 6.4.17 ClimatePartner GmbH

- 6.4.18 Novisto Inc.

- 6.4.19 EcoRealities GmbH

- 6.4.20 Workiva Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment