|

시장보고서

상품코드

2072809

케타민 클리닉 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Ketamine Clinic - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

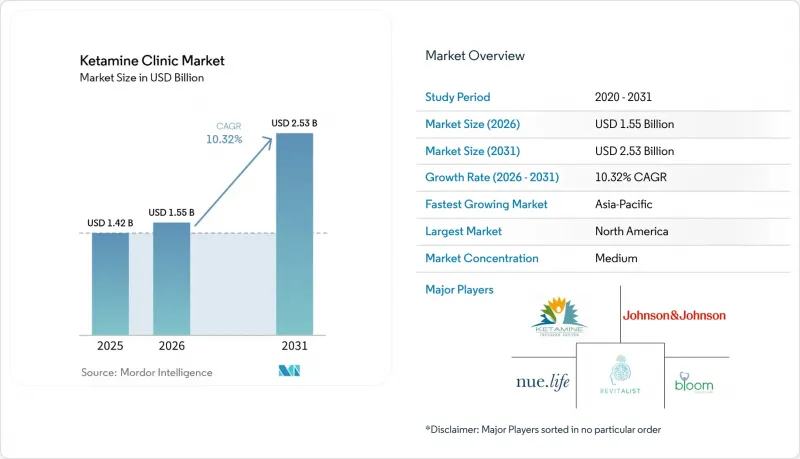

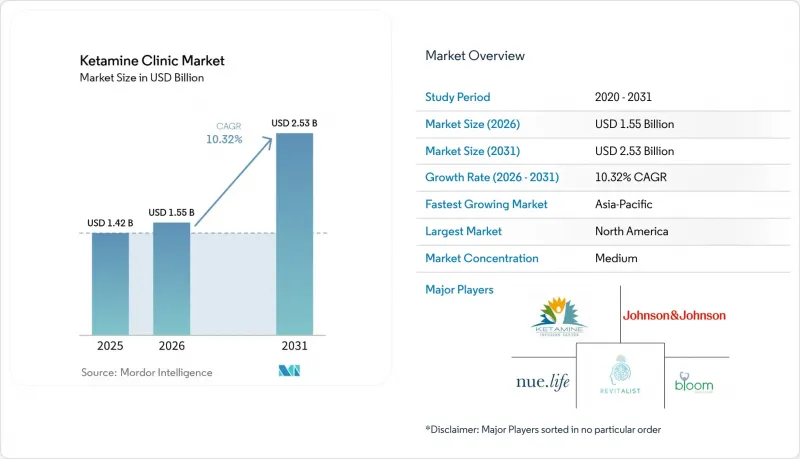

Mordor Intelligence에 의하면, 케타민 클리닉 시장 규모는 2025년에 14억 2,000만 달러로 평가되었고 2026년 15억 5,000만 달러에서 2031년까지 25억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 10.32%를 나타낼 전망입니다.

본 보고서는 치료 형태(대면, 온라인, 하이브리드), 임상 적응증(우울증, 불안 장애, PTSD, 강박 장애, 약물 사용 장애, 만성 통증, 기타), 투여 경로(정맥 내, 근육 내, 비강 내, 설하, 피하), 케어 유형, 소개 채널, 비즈니스 모델, 환자 연령대 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 케타민 클리닉 시장 동향 및 인사이트

치료 저항성 우울증으로 인한 부담이 커지면서, 대상 환자층이 확대되고 있습니다.

치료 저항성 우울증은 더 광범위한 항우울제 범주보다 케타민 클리닉 시장을 더 직접적으로 뒷받침하고 있습니다. 이는 이러한 환자들이 대개 약물 치료를 반복적으로 시도했다가 실패한 끝에 병원을 찾기 때문입니다. 『The British Journal of Psychiatry』지에 게재된 2025년의 혼합 방법론에 의한 연구에서는 주요 우울 장애 환자 2,461명을 대상으로 조사가 실시되었으며, 48%가 치료 저항성 우울증의 기준을 충족했고, 36.9%가 4유형 이상의 항우울제를 시도한 적이 있는 것으로 밝혀졌습니다. 또한, 치료 저항성이 높을수록 경제적 비활동 및 소득 감소와 관련이 있는 것으로 나타났습니다. 또한, 2025년 『Frontiers in Psychiatry』에 게재된 논설에 따르면, 항우울제 치료를 받고 있는 환자 중 치료 저항성 우울증의 유병률은 30%에서 40%로 추정되며, 이는 경구 약물 요법만으로는 극복할 수 없는 지속적인 한계가 존재함을 시사합니다. 이로 인해 많은 환자가 문서화된 치료 이력과 치료 강도를 단계적으로 높이기 위한 명확한 임상적 근거를 갖추고 내원하기 때문에 의뢰되는 환자층은 유례없이 적격한 것으로 나타납니다. 2025년 9월에 발표된 WHO의 지역별 보고서에 따르면, 전 세계적으로 10억 명 이상이 정신 질환을 앓으며 생활하고 있으며, 이는 케타민 클리닉이 여러 적응증에 걸쳐 환자를 유치할 수 있는 광범위한 수요 기반을 뒷받침하고 있습니다.

기존 항우울제에 대한 "즉각적인 증상 완화"가 소개 건수를 견인

케타민 클리닉 시장은 케타민의 즉각적인 효과와 일반적인 항우울제의 반응이 느리다는 특징과의 뚜렷한 대비 덕분에 혜택을 보고 있습니다. 존슨앤드존슨은 2025년 1월, 세 번째 경구용 항우울제 치료가 실패한 후 환자의 86%가 관해에 이르지 못했다고 발표했습니다. 이는 정신과 의사에게 적합한 환자를 더 신속한 치료법으로 전환해야 할 강력한 이유가 됩니다. 4상 TRD4005 임상시험에서 미국 내 51개 외래 진료 센터를 대상으로 한 결과, 첫 투여 후 24시간 이내에 개선이 확인되었으며, 4주 차의 관해율은 22.5%였던 반면, 위약군에서는 7.6%에 그쳤습니다. 이러한 신속한 효과는 급성기에 자살 충동을 보이는 상황에서 가장 중요합니다. 왜냐하면, 효과가 나타나기까지 걸리는 시간이 환자가 더 긴급한 상황에 머물게 될지, 아니면 감독 하에 외래 치료로 전환될지를 좌우하기 때문입니다. 또한, 반응 속도가 빠르기 때문에 투여 중 모니터링의 필요성을 저해하지 않으면서도 치료 주기를 단축할 수 있어, 진료소의 환자 처리 능력 향상에도 기여합니다.

적응증 외 케타민의 보험 적용 범위가 좁아 시장 확대에 제약이 되고 있습니다.

보험 적용 범위는 케타민 클리닉 시장에서 여전히 가장 뿌리 깊은 제약 요소 중 하나입니다. 이는 SPRAVATO에 대한 보험 급여가 정맥 내 투여나 조제된 정신과용 케타민에 비해 훨씬 더 후하기 때문입니다. 하버드 로스쿨의 페트리 프롬 센터에 따르면, 메디케어 파트 B가 연간 본인부담 한도를 초과하는 금액에 대해 SPRAVATO 비용의 80%를 보장하고 있는 반면, 적응증 외 사용되는 환각제나 케타민의 경우, 일반적인 공적 보험 제도를 통해 환급을 받는 것이 여전히 훨씬 더 어렵다고 지적하고 있습니다. 이로 인해 시장은 양극화되어 있으며, REMS 인증을 받고 병원과 제휴를 맺은 의료 제공업체는 보험 적용이 가능한 경로를 통해 치료를 진행하는 데 유리한 입장에 있는 반면, 많은 독립형 정맥주사 치료 사업자는 여전히 환자 본인 부담에 의한 수요에 의존하고 있습니다. 그 결과, 가격에 민감한 환자의 경우, 도입 치료는 완료되었더라도 유지 요법을 지속하지 못해 치료의 지속성이 떨어지고 있습니다. 또한, 임상적 필요성이 분명하더라도 저소득층에 대한 보급이 제한되고 있습니다.

부문별 분석

2025년 기준으로, 시설 내 치료는 치료법 부문의 82.12%를 차지하며 케타민 클리닉 시장 규모에서 가장 큰 점유율을 기록했습니다. REMS 요건에 따라 SPRAVATO의 투여는 직접 감독을 받는 인증 시설 내에서만 이루어져야 하므로, 이에 따라 승인된 비강 내 치료의 경우 시설 기반의 제공이 여전히 유리합니다. 진정, 해리, 혈압 모니터링의 관점에서도 시설 내 치료는 중증도가 높은 정신과 치료에서 가장 안전하며, 정당화하기 쉬운 모델로 자리 잡고 있습니다. 하이브리드 요법은 클리닉에서 도입 단계를 대면으로 시작하고, 유지 요법 및 사후 관리의 일부를 원격 의료 워크플로로 전환할 수 있기 때문에 여전히 중간적인 선택지로 남아 있습니다. 이러한 구조를 통해 사업자는 급성기 관리에 소홀하지 않으면서도 환자 1인당 비용을 절감할 수 있습니다.

온라인 치료는 2031년까지 연평균 성장률(CAGR) 12.62%를 나타낼 것으로 예측되며, 케타민 클리닉 시장에서 가장 빠르게 성장하는 치료 형태가 될 것입니다. 이러한 성장을 주도하고 있는 것은 규제가 허용하는 범위 내에서 경구 및 설하 투여용 조제 케타민을 제공하고, 디지털 문진, 원격 처방, 비동기 모니터링 기능을 갖춘 플랫폼입니다. 케타민 클리닉 업계는 임상 선별 검사를 소홀히 하지 않으면서도, 규정을 준수하는 대면 투여와 디지털을 통한 환자 유치 모두를 관리할 수 있는 사업자로 점차 전환되고 있습니다. 이러한 이중 체제를 통해 클리닉은 더 조기에 환자를 유치하고, 도입 후에도 지속적인 관계를 유지하며, 전체 치료 과정에 걸친 전환율을 높일 수 있습니다. 또한, 미국 내 인증 시설의 수가 증가하고 있는 점도, ‘디지털 퍼스트’ 플랫폼이 필요에 따라 원격 문진과 감독 하의 대면 투약을 연계하는 것을 용이하게 하고 있습니다.

2025년, 우울증은 임상 적응증 부문의 44.17%를 차지하며 케타민 클리닉 시장에서 가장 큰 수익 기반이 되었습니다. 이러한 선도적 지위는 치료 저항성 우울증 환자 의뢰 건수가 많다는 점과, 적절한 환자에게 SPRAVATO를 통해 이용 가능한 보다 명확한 보험 급여 절차가 확립되어 있다는 점을 반영하고 있습니다. 불안 장애, PTSD, 강박 장애(OCD), 약물 사용 장애는 모두 상당한 환자 수를 차지하고 있지만, 여전히 본인 부담으로 진료를 받는 것이 주를 이루고 있습니다. 이러한 구성으로 인해 우울증이 여전히 중심적인 위치를 차지하고 있습니다. 이는 우울증이 승인된 제품과의 일치도가 가장 높고, 소개 패턴이 명확하며, 임상적 인지도도 높은 부문이기 때문입니다. 또한, 이는 정신과 평가 및 문서화 시스템이 더 잘 갖춰진 클리닉일수록 이용률을 높게 유지하기 쉽다는 것을 의미합니다.

만성 통증 시장은 2031년까지 연평균 성장률(CAGR) 12.17%로 확대될 것으로 예상되며, 케타민 클리닉 시장에서 가장 빠르게 성장하는 적응증이 될 전망입니다. 클리블랜드 클리닉의 보고에 따르면, 환자의 86.1%가 해당 클리닉의 저용량 정맥주사 치료 과정을 완료했으며, 80%가 재주사를 받기 위해 내원했습니다. 또한, 3개월 및 6개월 시점에서 20%에서 46%에 이르는 환자가 임상적으로 유의미한 개선을 보였으며, 이는 일회성 치료에 비해 높은 환자 유지율로 인한 경제성을 뒷받침하는 것입니다. 2024년 『Frontiers in Psychiatry』지에 게재된 재향군인을 대상으로 한 메타분석에 따르면, 통증, 우울증, PTSD 각 분야에서 케타민의 효과 크기가 1.8인 것으로 나타났으며, 이는 이미 모니터링 체계를 갖추고 있는 클리닉이 다양한 적응증으로의 확대를 추진하는 데 힘을 실어줄 것입니다. 섭식 장애나 정체성에 기인한 트라우마 등 기타 적응증은 여전히 초기 단계의 틈새 분야에 머물러 있지만, 심리치료와 연계된 치료를 통해 보다 체계적인 프로토콜 개발이 진행되기 시작하고 있습니다. 따라서 케타민 클리닉 시장은 여전히 우울증이 주를 이루고 있지만, 만성 통증이 수요의 폭을 넓히며 유지 요법의 가능성을 확대되고 있습니다.

2025년 기준으로, 정맥 내 투여는 투여 경로 부문의 46.59%를 차지하며 케타민 클리닉 시장에서 주요 투여 경로가 되었습니다. 정맥 내 케타민은 용량 조절이 정확하고 작용 발현이 빠르기 때문에 많은 치료 저항성 우울증 및 통증 치료 프로토콜에서 여전히 표준 투여 경로로 사용되고 있습니다. 근육 내 및 피하 투여의 비중은 작지만, 혈관 접근이 어려운 경우나 시술 부담을 줄여야 하는 경우에는 여전히 임상적으로 중요한 역할을 하고 있습니다. 이를 통해 제품 구성이 변경되더라도, 수액 요법을 중심으로 한 치료의 확고한 입지가 유지됩니다. 또한, 보다 정교한 모니터링을 관리할 수 있는 병원 부속 클리닉이나 전문 클리닉의 프리미엄 위상도 뒷받침되고 있습니다.

비강 투여용 에스케타민 시장은 2031년까지 연평균 성장률(CAGR) 13.57%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 투여 경로가 될 전망입니다. 2025년 1월 FDA의 단일 요법 승인으로 인해 비강 투여 대상 환자군이 확대되었으며, 치료 저항성 우울증의 모든 적격 사례에 대해 항우울제의 경구 병용 처방을 의무화했던 요건이 폐지되었습니다. 또한, 비강 내 투여를 통한 치료는 정맥 주사를 많이 사용하는 모델에 비해 간호 부담과 진료실 설비의 복잡성을 줄여주므로, 이미 승인된 외래 진료 환경에서 사업을 확대하기가 용이해집니다. 설하 투여 및 경구 투여는 원격의료 분야에서 성장하고 있지만, 조제 제제 및 투여량의 편차에 대한 우려로 인해 규제 당국의 엄격한 심사 하에서는 이러한 하위 부문이 어느 정도까지 확대될 수 있을지에 여전히 한계가 있습니다. 따라서 케타민 클리닉 시장은 더욱 다양한 투여 경로로 전환되고 있으며, 정맥 내 투여를 통한 치료는 여전히 주요한 역할을 유지하고 있는 반면, 비강 내 요법은 감독 하에 이루어지는 외래 치료의 적용 범위를 확대되고 있습니다.

지역별 분석

2025년, 북미는 케타민 클리닉 시장의 53.86%를 차지하며 지역별로는 가장 큰 기여도를 보였습니다. 이 지역은 가장 잘 갖춰진 클리닉 인프라, 승인된 제품에 대한 가장 강력한 입지, 그리고 가장 폭넓은 정신과 의사 및 중재 의료 제공업체 기반을 모두 갖추고 있습니다. 2026년에는 미국에서 7,000곳 이상의 REMS 인증을 받은 SPRAVATO 투여 시설이 운영되고 있어, 단기간에 감독 하의 투여 체계가 얼마나 확대되었는지 알 수 있습니다. 캐나다에서는 민간 케타민 클리닉의 수용 능력이 증가하고 있지만, 에스케타민의 승인 범위가 광범위하지 않기 때문에 치료의 상당 부분은 본인 부담 방식으로 이루어지고 있습니다. 2025년 1월에 발표된 미국의 원격의료 관련 규제는 케타민 클리닉 시장에서 ‘디지털 퍼스트’ 방식의 의료 제공업체들이 규제 약물에 대한 규정 준수 위험을 초래하지 않으면서 사업을 확장해 나갈 수 있는 방식을 앞으로도 계속해서 형성해 나갈 것입니다.

유럽은 케타민 클리닉 시장에서 2위를 차지하는 지역 부문이며, 독일, 영국, 프랑스가 도입을 주도하고 있습니다. 해당 지역에서는 본인 부담과 국가 보험 환급 제도에 연동된 보다 공식적인 평가 경로가 결합되면서 시장이 확대되고 있습니다. 이탈리아와 스페인 등의 학술 기관에서 실시한 시판 후 조사 결과는 SPRAVATO의 초기 임상시험에서 확인된 안전성 및 유효성 프로파일을 지속적으로 뒷받침하고 있습니다. 의료기술평가(HTA) 지원이 확대되면 의사의 의뢰 건수가 대폭 증가할 것으로 예상되지만, 한편 민간 클리닉은 보다 종합적인 보험 적용 결정에 앞서 계속해서 수요를 창출하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 11.64%를 나타낼 것으로 예측되며, 케타민 클리닉 시장 규모 전망에서 가장 빠르게 성장하는 지역 부문이 될 것으로 보입니다. 호주가 이 지역의 발전을 주도하고 있으며, Avive Health사는 2026년 중반에 멜버른에 클리닉을 개설하고, 빅토리아주의 두 병원에 케타민 및 환각제 보조 치료용 입원 병상 120개를 증설할 예정입니다. 일본과 한국에서는 마취과 관련 의료 현장에서 적응증 외 사용으로 정맥 내 케타민 투여가 증가하고 있습니다. 한편, 중국의 민간 병원 부문에서는 정신과 및 마취 용도를 위한 정맥 주입 인프라가 점차 갖춰지고 있습니다. 인도 및 아시아태평양 주변국 중 상당수는 규제상의 차이 및 정신과 의사 밀도가 여전히 단기적인 보급을 제한하고 있어 초기 단계에 머물러 있습니다. 중동 및 아프리카 및 남미는 케타민 클리닉 시장에서 여전히 소규모 비중을 차지하고 있지만, GCC 국가들과 브라질에서는 민간 의료 서비스의 수용 능력과 고소득층 환자층이 새로운 치료법의 도입을 뒷받침하고 있어, 다른 지역보다 조기에 시장이 확대될 가능성이 높은 것으로 보입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the ketamine clinic market size was valued at USD 1.42 billion in 2025 and is estimated to grow from USD 1.55 billion in 2026 to reach USD 2.53 billion by 2031, at a CAGR of 10.32% during the forecast period (2026-2031).

This report is Segmented by Therapy Modality (On-Site, Online, Hybrid), Clinical Indication (Depression, Anxiety, PTSD, OCD, SUD, Chronic Pain, Others), Route of Administration (IV, IM, Intranasal, Sublingual, SC), Care Type, Referral Channel, Business Model, Patient Age Group, and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Ketamine Clinic Market Trends and Insights

Rising Treatment-Resistant Depression Burden Expands the Addressable Patient Pool

Treatment-resistant depression supports the ketamine clinic market more directly than the wider antidepressant category because these patients typically reach clinics after repeated medication failure. A 2025 mixed-methods study in The British Journal of Psychiatry covering 2,461 patients with major depressive disorder found that 48% met treatment-resistant depression criteria and 36.9% had tried 4 or more antidepressants, with greater resistance linked to economic inactivity and income loss. A 2025 editorial in Frontiers in Psychiatry also placed treatment-resistant depression prevalence at 30% to 40% among antidepressant-treated patients, which points to a durable ceiling that oral pharmacotherapy alone does not close. This keeps the referral pool unusually qualified because many patients arrive with documented treatment history and a clearer clinical basis for escalation. WHO regional reporting released in September 2025 stated that more than 1 billion people live with mental health conditions globally, which underlines the broad demand base from which ketamine clinics can draw patients across several indications.

Rapid-Acting Symptom Relief Versus Conventional Antidepressants Drives Referral Volume

The ketamine clinic market benefits from the clear contrast between ketamine's rapid action and the delayed response pattern of standard antidepressants. Johnson & Johnson stated in January 2025 that after a third failed oral antidepressant, 86% of patients do not achieve remission, which gives psychiatrists a strong reason to move suitable patients toward faster-acting options. The Phase 4 TRD4005 trial showed improvement within 24 hours of the first dose and a 22.5% remission rate at week 4 compared with 7.6% for placebo across 51 U.S. outpatient centers. This speed matters most in acute suicidal ideation settings because time to effect influences whether the patient stays in a higher-acuity setting or moves into supervised outpatient care. Faster response also helps clinics improve throughput because care cycles can be shortened without removing the need for monitoring during administration.

Limited Insurance Coverage for Off-Label Ketamine Constrains Market Expansion

Coverage remains one of the most persistent limits on the ketamine clinic market because reimbursement is much stronger for SPRAVATO than for intravenous or compounded psychiatric ketamine. Harvard Law School's Petrie-Flom Center noted that Medicare Part B covers SPRAVATO at 80% after the annual deductible, while off-label psychedelic and ketamine pathways remain much harder to reimburse through standard public insurance structures. This creates a split market where REMS-certified and hospital-linked providers are better placed to work within reimbursable channels, while many independent infusion operators continue to rely on self-pay demand. The result is lower treatment continuity for price-sensitive patients who may complete induction but not remain on maintenance schedules. This also limits penetration into lower-income populations even when the clinical need is clear.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Interventional Psychiatry Acceptance Widens the Prescriber Base

- SPRAVATO Label and Evidence Base Supporting Clinic Adoption

- Protocol Heterogeneity and Limited Long-Term Outcomes Data Temper Clinical Confidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-site therapy held 82.12% of the therapy modality segment in 2025, giving it the largest share of the ketamine clinic market size. REMS requirements keep SPRAVATO administration inside certified settings with direct supervision, which continues to favor facility-based delivery for approved intranasal treatment. Sedation, dissociation, and blood pressure monitoring also make on-site care the safest and most defensible model for higher-acuity psychiatric treatment. Hybrid therapy remains the middle ground because it allows clinics to start induction in person and shift parts of maintenance and follow-up into telehealth workflows. That structure helps operators lower per-patient cost without removing acute-phase oversight.

Online therapy is projected to grow at 12.62% CAGR through 2031, making it the fastest-growing modality in the ketamine clinic market. Growth is being driven by platforms offering oral and sublingual compounded ketamine with digital intake, remote prescribing, and asynchronous monitoring where regulation permits. The ketamine clinic industry is moving toward operators that can manage both compliant in-person administration and digital patient acquisition without weakening clinical screening. That dual positioning helps clinics capture patients earlier, extend engagement after induction, and improve conversion across the care pathway. The larger certified-site footprint in the United States also makes it easier for digital-first platforms to connect remote intake with supervised in-person administration when required.

Depression held 44.17% of the clinical indication segment in 2025, making it the largest revenue base in the ketamine clinic market. This leadership reflects the strength of treatment-resistant depression referrals and the clearer reimbursement path available through SPRAVATO for suitable patients. Anxiety disorders, PTSD, OCD, and substance use disorders all add meaningful volume, but they continue to sit more heavily in self-pay channels. That mix keeps depression central because it is the segment most aligned with an approved product, clearer referral patterns, and stronger clinical familiarity. It also means clinics with better psychiatric evaluation and documentation systems are better placed to keep utilization high.

Chronic pain is forecast to expand at 12.17% CAGR through 2031, making it the fastest-growing indication in the ketamine clinic market. Cleveland Clinic reported that 86.1% of patients completed its low-dose infusion protocol and 80% returned for repeat infusions, while 20% to 46% achieved clinically meaningful improvement at 3 and 6 months, which supports stronger retention economics than one-time episodic care. A 2024 Frontiers in Psychiatry meta-analysis across veteran samples found an effect size of 1.8 for ketamine across pain, depression, and PTSD, which supports multi-indication positioning for clinics that already have monitoring capability. Other indications, such as eating disorders and identity-based trauma, remain early-stage niches, but they are beginning to attract more structured protocol development through psychotherapy-linked care. The ketamine clinic market, therefore, remains anchored by depression, while chronic pain is broadening the demand profile and extending maintenance potential.

Intravenous administration held 46.59% of the route-of-administration segment in 2025, which made it the leading route in the ketamine clinic market. Intravenous ketamine remains the reference pathway for many treatment-resistant depression and pain protocols because dose titration is precise and onset is fast. Intramuscular and subcutaneous routes hold smaller shares, but they remain clinically relevant where vascular access is difficult or procedural burden must be reduced. This preserves a strong place for infusion-centered care even as product mix changes. It also supports the premium position of hospital-affiliated and specialist clinics that can manage higher monitoring intensity.

Intranasal esketamine is expected to grow at 13.57% CAGR through 2031, making it the fastest-growing route. The January 2025 FDA monotherapy approval widened the patient pool for intranasal use and removed the need for mandatory oral antidepressant co-prescribing in every eligible treatment-resistant depression case. Intranasal treatment also reduces nursing intensity and clinic setup complexity compared with infusion-heavy models, which makes expansion easier for approved outpatient settings. Sublingual and oral routes are growing in telehealth channels, but concerns around compounded formulations and inconsistent dosing continue to limit how far those sub-segments can scale under closer regulatory review. The ketamine clinic market is therefore moving toward a more mixed route profile, with intravenous care retaining its premium role while intranasal therapy expands the reach of supervised outpatient treatment.

Complete Report Scope:

- By Therapy Modality

- On-Site Therapy

- Online Therapy

- Hybrid Therapy

- By Clinical Indication

- Depression

- Anxiety Disorders

- Post-Traumatic Stress Disorder

- Obsessive-Compulsive Disorder

- Substance Use Disorders

- Chronic Pain

- Other Clinical Indications

- By Route Of Administration

- Intravenous

- Intramuscular

- Intranasal Esketamine

- Sublingual And Oral

- Subcutaneous

- By Care Type

- Medication-Only

- Ketamine-Assisted Psychotherapy

- By Referral Channel

- Direct-To-Consumer And Self-Referred

- Physician-Referred

- Payer And Case-Management Referred

- By Business Model

- Independently Owned Private Clinics

- Franchise-Owned Clinics

- Hospital-Affiliated Clinics

- Research And Clinical Trial Centers

- Anesthesiology And Psychology Practice Extensions

- By Patient Age Group

- Adolescents

- Adults

- Geriatric

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 53.86% of the ketamine clinic market share in 2025, which made it the largest regional contributor. The region combines the deepest clinic infrastructure, the strongest approved product presence, and the broadest base of psychiatrists and interventional providers. More than 7,000 REMS-certified SPRAVATO administration sites were operating in the United States in 2026, which shows how far supervised delivery capacity has expanded in a short period. Canada is adding private ketamine clinic capacity, but the absence of broad approved esketamine coverage keeps much of care in self-pay channels. U.S. telemedicine rules announced in January 2025 will continue to shape how digital-first providers in the ketamine clinic market expand without creating controlled-substance compliance risk.

Europe is the second-largest regional segment in the ketamine clinic market, with Germany, the UK, and France leading adoption. The region is advancing through a mix of private pay and more formal evaluation pathways tied to national reimbursement systems. Post-marketing experience from academic centers in countries such as Italy and Spain has continued to support the safety and efficacy profile seen in earlier SPRAVATO studies. Wider health technology assessment support would materially lift physician-referred volume, while private clinics continue building demand ahead of fuller coverage decisions.

Asia-Pacific is projected to expand at 11.64% CAGR through 2031, making it the fastest-growing regional component of the ketamine clinic market size forecast. Australia leads regional development, with Avive Health opening a Melbourne clinic in mid-2026 and adding 120 inpatient beds across 2 Victorian hospitals for ketamine and psychedelic-assisted therapies. Japan and South Korea are seeing greater off-label intravenous ketamine use in anesthesiology-adjacent settings, while China's private hospital sector is building infusion infrastructure for psychiatric and anesthetic applications. India and much of the wider Asia-Pacific periphery remain early stage because regulatory heterogeneity and psychiatrist density still limit near-term penetration. The Middle East and Africa and South America remain smaller parts of the ketamine clinic market, with GCC countries and Brazil appearing most likely to move earlier because private healthcare capacity and higher-income patient pools are more supportive of novel therapy adoption.

- Actify Neurotherapies

- ATAI Life Sciences N.V.

- Awakn Life Sciences Corp.

- Bloom Mental Health

- Ember Health, Inc.

- Field Trip Health Ltd.

- HealingMaps Ketamine Network

- Johnson & Johnson

- Joyous

- Klarisana

- Klarity Clinic

- Luye Pharma Group Ltd.

- Mindbloom, Inc.

- Mindful Health Solutions, Inc.

- MindPeace Clinics

- Nue Life Health

- Nushama Psychedelic Wellness Center

- NY Ketamine Infusions

- Pasithea Therapeutics Corp.

- Revitalist Lifestyle and Wellness Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Treatment-Resistant Depression Burden

- 4.2.2 Rapid-Acting Symptom Relief Versus Conventional Antidepressants

- 4.2.3 Expansion Of Interventional Psychiatry Acceptance

- 4.2.4 SPRAVATO Label And Evidence Base Supporting Clinic Adoption

- 4.2.5 Digital Intake, Monitoring, And Hybrid Care Improving Conversion

- 4.2.6 Veteran, Pain, And Comorbidity Patient Pools Broadening Demand

- 4.3 Market Restraints

- 4.3.1 Limited Insurance Coverage For Off-Label Ketamine Care

- 4.3.2 Protocol Heterogeneity And Limited Long-Term Outcomes Data

- 4.3.3 FDA And State-Level Scrutiny Of Compounded Ketamine And Telehealth Use

- 4.3.4 High Total Course Cost And Maintenance Dependence

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Therapy Modality

- 5.1.1 On-Site Therapy

- 5.1.2 Online Therapy

- 5.1.3 Hybrid Therapy

- 5.2 By Clinical Indication

- 5.2.1 Depression

- 5.2.2 Anxiety Disorders

- 5.2.3 Post-Traumatic Stress Disorder

- 5.2.4 Obsessive-Compulsive Disorder

- 5.2.5 Substance Use Disorders

- 5.2.6 Chronic Pain

- 5.2.7 Other Clinical Indications

- 5.3 By Route Of Administration

- 5.3.1 Intravenous

- 5.3.2 Intramuscular

- 5.3.3 Intranasal Esketamine

- 5.3.4 Sublingual And Oral

- 5.3.5 Subcutaneous

- 5.4 By Care Type

- 5.4.1 Medication-Only

- 5.4.2 Ketamine-Assisted Psychotherapy

- 5.5 By Referral Channel

- 5.5.1 Direct-To-Consumer And Self-Referred

- 5.5.2 Physician-Referred

- 5.5.3 Payer And Case-Management Referred

- 5.6 By Business Model

- 5.6.1 Independently Owned Private Clinics

- 5.6.2 Franchise-Owned Clinics

- 5.6.3 Hospital-Affiliated Clinics

- 5.6.4 Research And Clinical Trial Centers

- 5.6.5 Anesthesiology And Psychology Practice Extensions

- 5.7 By Patient Age Group

- 5.7.1 Adolescents

- 5.7.2 Adults

- 5.7.3 Geriatric

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Spain

- 5.8.2.6 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 India

- 5.8.3.4 Australia

- 5.8.3.5 South Korea

- 5.8.3.6 Rest of Asia-Pacific

- 5.8.4 Middle East & Africa

- 5.8.4.1 GCC

- 5.8.4.2 South Africa

- 5.8.4.3 Rest of Middle East & Africa

- 5.8.5 South America

- 5.8.5.1 Brazil

- 5.8.5.2 Argentina

- 5.8.5.3 Rest of South America

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Actify Neurotherapies

- 6.3.2 ATAI Life Sciences N.V.

- 6.3.3 Awakn Life Sciences Corp.

- 6.3.4 Bloom Mental Health

- 6.3.5 Ember Health, Inc.

- 6.3.6 Field Trip Health Ltd.

- 6.3.7 HealingMaps Ketamine Network

- 6.3.8 Johnson and Johnson Services, Inc.

- 6.3.9 Joyous

- 6.3.10 Klarisana

- 6.3.11 Klarity Clinic

- 6.3.12 Luye Pharma Group Ltd.

- 6.3.13 Mindbloom, Inc.

- 6.3.14 Mindful Health Solutions, Inc.

- 6.3.15 MindPeace Clinics

- 6.3.16 Nue Life Health

- 6.3.17 Nushama Psychedelic Wellness Center

- 6.3.18 NY Ketamine Infusions

- 6.3.19 Pasithea Therapeutics Corp.

- 6.3.20 Revitalist Lifestyle and Wellness Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment