|

시장보고서

상품코드

2072831

교정용 헤드기어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Orthodontic Headgear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

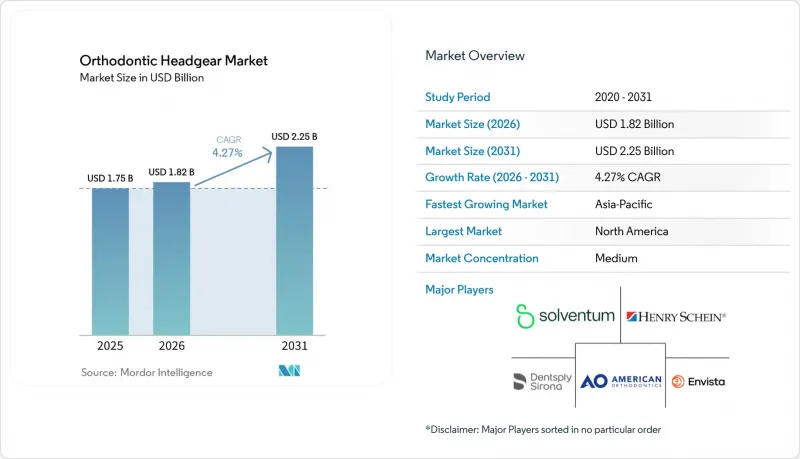

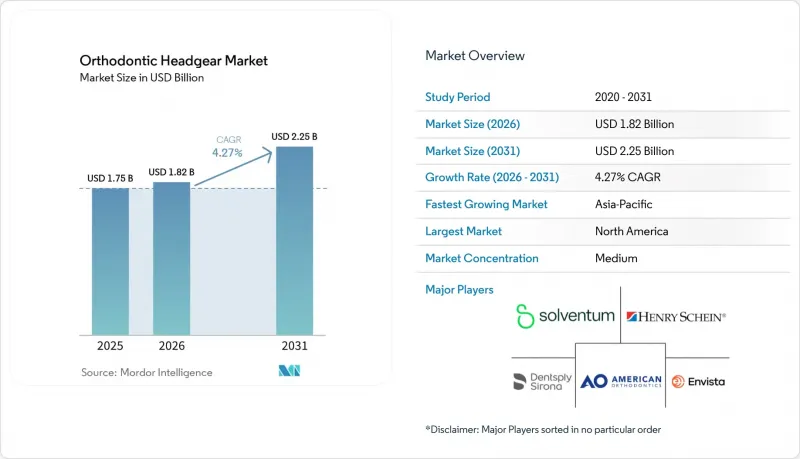

Mordor Intelligence에 의하면, 교정용 헤드기어 시장 규모는 2025년 17억 5,000만 달러에서 2026년에는 18억 2,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 4.27%로 성장을 지속하여, 2031년까지 22억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(서비컬 풀, 하이 풀, 리버스 풀, 페이스 마스크), 재질(스테인리스 스틸, 플라스틱 등), 용도(부정교합 교정, 과개교합 등), 연령대(소아, 10대, 성인), 최종 사용자(치과, 병원 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 교정용 헤드기어 시장 동향 및 인사이트

증가하는 부정교합의 부담과 조기 교정 치료

교정용 헤드기어 시장은 골격 교정이 여전히 교정력에 잘 반응하는 혼합치열기 단계로의 치료 전환에 힘입어 성장하고 있습니다. 부정교합은 여전히 광범위한 임상적 부담을 초래하고 있으며, 세계보건기구(WHO)는 이를 유병률 기준 세계 3위를 차지하는 구강 질환으로 계속해서 규정하고 있습니다. 또한, 2025년에 발표된 기업 데이터에서도 클래스 II 사례가 전 세계 부정교합의 대부분을 차지하고 있다는 점이 여전히 지적되고 있는 만큼, 교정용 헤드기어 시장은 클래스 II 치료 대상자의 규모가 여전히 크다는 점에서도 혜택을 보고 있습니다. 2025년에 실시된 학령기 아동을 대상으로 한 조사에서 표본의 28.4%에서 골격적 불균형과 관련된 구강 습관이 확인되었으며, 심교합 및 II급 교합 패턴도 상당한 비율로 확인되었습니다. 이는 사춘기 후반까지 기다리지 말고 조기에 선별 검사를 실시하는 것이 중요함을 뒷받침하는 것입니다. 주요 성장기를 지나 치료가 늦어지면, 임상의는 교정적 영향력을 어느 정도 상실하게 되므로, 조기 진단은 헤드기어를 이용한 치료의 안정적인 환자 수를 유지하는 데 도움이 됩니다. 많은 소아 환자의 경우, 장치의 선호도와 마찬가지로 시기도 여전히 중요하기 때문에 이로 인해 새로운 유형의 장치가 보급되더라도 수요는 지속적으로 유지될 것입니다.

소아 및 청소년기의 교정 치료 보급 확대

교정용 헤드기어 시장은 소아 및 청소년의 교정 치료에 대한 수용도가 높아지는 것도 호재로 작용하고 있습니다. 특히, 부모들이 조기 교정을 일상적인 치과 관리의 일환으로 인식하게 된 지역에서 이러한 현상이 두드러집니다. 이러한 수요의 조짐은 단기적인 유행이 아니라 성장의 생물학적 과정에 기인한 것이므로, 지속될 것으로 보입니다. 가장 큰 이점이 두드러지는 분야는 표준화된 프로토콜을 통해 성장기 환자를 관리하는 치료 환경입니다. 왜냐하면 비용과 골격 조절이 모두 중요한 경우, 헤드기어는 여전히 실용적인 첫 번째 선택인 교정 치료법이기 때문입니다. 또한, 대도시권 이외의 도시에서도 치료 과정이 더욱 체계화되고 비용 면에서도 부담이 줄어들고 있어, 더 많은 사춘기 환자들이 조직화된 진료 시스템을 이용하게 됨에 따라 교정용 헤드기어 시장은 더욱 성장할 것으로 전망됩니다. 이러한 효과는 교정 치료에 비용을 지출할 의사는 있으나 가격에 민감한 가구에서 특히 두드러집니다. 왜냐하면 헤드기어는 교정상의 요구를 충족시키면서도, 대부분의 경우 프리미엄 얼라이너보다 가격이 저렴하기 때문입니다. 그 결과, 소아 및 사춘기 환자의 진료 대상이 확대됨에 따라, 얼라이너 사용이 동시에 증가하고 있는 지역에서도 헤드기어를 사용하는 환자층은 더욱 넓어지고 있습니다.

경증에서 중등도의 II급 교정 사례에서 클리어 얼라이너로의 대체

교정용 헤드기어 시장은 경증의 II급 증례에서 특히 심미성이 선택에 큰 영향을 미치는 고가의 비급여 진료 현장에서 실질적인 대체 압력을 받고 있습니다. 가장 직접적인 예로는 2025년 7월 얼라인 테크놀로지(Align Technology)가 아시아태평양(APAC)에서 증가 추세를 보이고 있는 클래스 II 환자들을 대상으로, 하악 전돌 교정 기능과 견고한 교합 블록을 갖춘 인비절라인 시스템을 출시한 것을 들 수 있습니다. 2025년 체계적 문헌고찰에 따르면, 하악 전돌 교정용 얼라이너 시스템은 여러 치료 지표에서 기존의 교정 기구와 동등한 교정 효과를 달성했을 뿐만 아니라, 환자들로부터도 높은 지지를 받고 있는 것으로 보고되었습니다. 그렇긴 하지만, 수직적 과잉, 혼합 치열기의 제약, 예산이 제한된 증례의 경우, 클리어 얼라이너만으로는 임상적·경제적 과제를 모두 해결할 수 없기 때문에 교정용 헤드기어 시장은 여전히 확고한 입지를 유지하고 있습니다. 따라서 대체 효과는 보편적이라기보다는 불균일하며, 경증에서 중등도의 사례가 가장 먼저 영향을 받기 쉽다고 할 수 있습니다. 이로 인해 ‘헤드기어’라는 분류 자체가 완전히 사라지기보다는 그 증례 구성에 변화가 생기게 될 것입니다.

부문별 분석

2025년, 경부 견인 헤드기어는 38.31%의 시장 점유율을 차지하며 교정용 헤드기어 시장에서 주요 제품 유형으로서의 입지를 유지했습니다. 이러한 우위는 임상적 및 경제적 적합성이 높다는 점을 반영하며, 많은 소아 사례에서 제2급 교합에 대한 어금니 원심 이동 치료의 기본 선택지로 계속 자리 잡고 있기 때문입니다. 임상의들은 처방 방법이 간단하고, 조절이 용이하며, 맞춤형 대체 제품보다 저렴하고, 사용에 익숙한 장치가 필요할 때 계속해서 이 제품을 선호하고 있습니다. 이러한 가격 면에서의 합리성은 중요한 요소입니다. 왜냐하면 교정용 헤드기어 시장은 여전히 치료 효과와 합리적인 가격의 균형을 중시하는 많은 가정과 클리닉에 서비스를 제공하고 있기 때문입니다. 또한, 경부 견인형 디자인은 클래스 II 치료 대상 환자층의 규모가 크다는 점에서도 이점을 얻고 있어, 고급 얼라이너의 선택지가 확대되더라도 기본적인 수요는 안정적입니다.

하이풀 헤드기어는 2026년부터 2031년까지 연평균 성장률(CAGR) 6.38%를 기록하며 가장 빠르게 성장하고 있는 제품 부문입니다. 이는 복잡한 증례에서 수직 방향의 제어가 치료상 우선순위로 더욱 중요시되고 있기 때문입니다. 이러한 성장은 개방교합 경향이 있는 증례나 골격적 불균형과 과도한 수직 성장 양상을 모두 보이는 환자에서 해당 제품의 유용성을 반영하고 있습니다. 리버스 풀 헤드기어, 즉 페이스 마스크형 디자인은 규모는 작지만 임상적으로 명확한 하위 부문으로, 젊은 환자의 상악 전돌에 수반되는 III급 교정에 사용되고 있습니다. 교정용 헤드기어 업계는 여전히 이 유형에 의존하고 있습니다. 이는 성장기 소아의 골성 III급 부정교합 교정이 경도의 II급 부정교합 치료에 비해 대체하기 훨씬 어렵기 때문입니다. 또한, 디지털 제조를 통한 J-훅 콘셉트를 통해 이 카테고리에도 제품 혁신이 도입되고 있으며, 성숙한 제품군조차도 디지털과 기존 생산 모델을 융합한 하이브리드형으로 전환되고 있음을 시사하고 있습니다.

2025년에는 스테인리스 스틸이 67.24%의 점유율을 차지하며, 교정용 헤드기어 시장 전체에서 주요 소재로 자리매김했습니다. 고부하 구강외 장치에는 여전히 구조적 완전성, 내피로성 및 장기간에 걸친 안정적인 힘 전달이 요구되기 때문에 그 위상은 여전히 확고하게 유지되고 있습니다. 기기가 외부 보우와 내부 보우의 구조를 통해 지속적인 교정력을 발생시켜야 하는 경우, 이러한 특성을 대체하기는 어렵습니다. 따라서 외부 구성 요소가 경량화되는 추세임에도 불구하고, 금속은 교정용 헤드기어 시장에서 여전히 중심적인 위치를 차지하고 있습니다. 또한, 스테인리스 스틸은 이미 확립된 임상 워크플로우에도 적합하기 때문에 기존 헤드기어 치료 사례를 다수 다루고 있는 치과에서는 소재를 변경할 동기가 줄어들고 있습니다.

플라스틱은 디지털 제조 기술을 통해 더 가볍고 환자에게 친화적인 비금속 부품의 생산이 용이해짐에 따라, 2031년까지 연평균 성장률(CAGR)이 6.52%에 달하며 가장 빠르게 성장하고 있는 소재 부문입니다. 이러한 추세는 헤드캡, 턱받침, 조절 장치 등 눈에 보이는 부품과 관련이 있으며, 이러한 부위에서는 최대 하중 내구성보다 착용감과 미적 요소가 더 중요하게 여겨집니다. 실리콘, 나일론, 고무는 패드, 스트랩, 탄성 부품 분야에서 특히 환자의 편안함이 일상적인 착용에 영향을 미치는 상황에서 계속해서 보조적인 역할을 수행하고 있습니다. 앞으로 교정용 헤드기어 시장은 핵심적인 힘 전달을 담당하는 금속과, 착용감, 편안함, 맞춤 제작 가능성을 담당하는 폴리머 사이에서 더욱 명확하게 양분될 가능성이 있습니다. 이러한 변화는 소규모 제조업체들이 특정 틈새 시장에 진출하는 데 도움이 되는 한편, 데스크톱 프린터의 보급이 확대됨에 따라 범용 부품의 가격 프리미엄이 축소되는 결과로 이어집니다.

지역별 분석

2025년, 북미는 38.22%의 점유율을 차지하며 교정용 헤드기어 시장에서 가장 규모가 큰 지역 시장이 되었습니다. 이 지역은 성숙한 자비 교정 시스템, 일반 치과의사와 전문의 간의 견고한 의뢰 네트워크, 그리고 조기 교정적 개입에 대한 임상의들의 이해가 깊어지고 있다는 장점이 있습니다. 미국은 소아 교정치과 진료 분야에서 구강외 장치의 원리가 충분히 이해되고 있을 뿐만 아니라, 많은 신흥 지역에 비해 가족들이 치료를 조기에 시작하는 경향이 있기 때문에 여전히 핵심적인 수요 거점으로 자리 잡고 있습니다. 캐나다와 멕시코는 수요량은 적지만, 도시 지역의 치료 수요와 전문의에 의한 진료 서비스 확충에 힘입어 지역 기반을 확대되고 있습니다. 이로 인해 다른 지역에서 더 빠른 성장세가 나타나고 있음에도 불구하고, 북미는 교정용 헤드기어 시장에 있어 안정적인 수익의 주축이 되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.65%로 확대될 것으로 예상되며, 교정용 헤드기어 시장에서 가장 두드러진 성장을 보이는 지역입니다. 성장을 주도하고 있는 국가는 중국, 인도, 한국, 호주이지만, 이러한 추세는 지역 전체에서 일관되지는 않습니다. 한국과 호주는 디지털화 수준이 높은 반면, 인도, 동남아시아 및 중국의 내륙 도시에서는 진료소 네트워크 확대와 전문의에 대한 접근성 향상에 의존하는 경향이 강해지고 있습니다. 또한, 이 지역에서는 소아 치과 심미 치료에 대한 중산층의 소비 확대와 대도시권 이외 지역에서의 교정 치과 상담 접근성 확대도 긍정적인 요인으로 작용하고 있습니다. Align Technology가 2025년에 아시아태평양에서 하악 전돌 교정 기능을 갖춘 인비절라인 시스템을 출시한 사실 또한, 주요 기업들이 해당 지역에서 클래스 II 치료에 대한 수요가 확대되고 있음을 인식하고 있음을 뒷받침합니다. 다만, 이 제품은 대상 시장의 일부에서 헤드기어와 경쟁하게 될 것입니다.

유럽은 교정용 헤드기어 시장에서 성숙기에 접어들었음에도 여전히 활기를 띠고 있는 지역이며, 독일, 영국, 프랑스가 제품의 품질과 전문 진료 기준 면에서 계속해서 주도적인 역할을 수행하고 있습니다. 이 지역에서는 조달 요건이 더 엄격하고, 임상의들이 자재의 신뢰성과 규제 준수 여부를 중시하기 때문에 규모가 크고 실적이 풍부한 공급업체가 선호되는 경향이 있습니다. 남미, 중동 및 아프리카는 여전히 발전 가능성이 높은 유망 지역이며, 도시 지역의 치과 의료 수요와 의료 인프라 확충에 힘입어 성장 지향적인 교정 치료의 환자 기반이 점차 확대되고 있습니다. 이에 따라 교정용 헤드기어 시장은 균형 잡힌 지역 구성을 보이고 있으며, 북미는 시장 규모, 아시아태평양은 성장 속도, 그리고 유럽 및 신흥 지역은 선택적인 교체 및 확장 수요를 이끌고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the orthodontic headgear market size is expected to grow from USD 1.75 billion in 2025 to USD 1.82 billion in 2026 and is forecast to reach USD 2.25 billion by 2031 at 4.27% CAGR over 2026-2031.

This report is Segmented by Product Type (Cervical Pull, High-Pull, Reverse-Pull, Facemask), Material Type (Stainless Steel, Plastic, and More), Application (Malocclusion Correction, Overbite, and More), Age Group (Children, Teens, Adults), End User (Dental Clinics, Hospitals, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Orthodontic Headgear Market Trends and Insights

Rising Malocclusion Burden and Earlier Orthodontic Intervention

The orthodontic headgear market is supported by a treatment shift toward the mixed dentition stage, where skeletal correction still responds well to orthopedic force. Malocclusion remains a broad clinical burden, and the World Health Organization continues to rank it as the third most prevalent oral condition worldwide. The orthodontic headgear market also benefits from the continued size of the Class II treatment pool, because company data released in 2025 still described Class II cases as a large portion of global malocclusions. A 2025 schoolchild study found oral habits tied to skeletal discrepancy in 28.4% of the sample, alongside notable rates of deep bite and Class II patterns, which reinforces the value of screening early rather than waiting for later adolescence. When treatment is delayed past the main growth window, clinicians lose some orthopedic leverage, so earlier diagnosis helps maintain a stable case flow for headgear-based treatment. This keeps demand durable even as newer appliance types expand, because timing still matters as much as appliance preference in many pediatric cases.

Expanding Pediatric and Adolescent Orthodontic Treatment Adoption

The orthodontic headgear market is also gaining from broader acceptance of orthodontic treatment in children and teens, especially where parents now treat early correction as part of routine dental care. This demand signal appears durable because the need is tied to growth biology rather than short-term discretionary fashion. The largest benefit is visible in treatment settings that manage growing patients through standardized protocols, since headgear remains a practical first-line orthopedic option when cost and skeletal control both matter. The orthodontic headgear market also stands to gain as more adolescent patients enter organized clinic systems in cities beyond major urban centers, where treatment pathways are becoming more structured and more affordable. This effect is stronger in households that are willing to fund correction but remain price sensitive, because headgear often sits below premium aligner pricing while still addressing orthopedic needs. As a result, pediatric and adolescent uptake widens the patient funnel for headgear even where aligners are growing in parallel.

Clear Aligner Substitution in Mild to Moderate Class II Cases

The orthodontic headgear market is under real substitution pressure in milder Class II cases, especially in premium private-pay settings where aesthetics have a strong influence on choice. The most direct example came in July 2025, when Align Technology launched an Invisalign system with mandibular advancement and solid occlusal blocks for growing Class II patients in APAC. A 2025 systematic review reported that mandibular advancement aligner systems achieved comparable correction to conventional orthopedic appliances on several treatment measures, while also showing strong patient preference. That said, the orthodontic headgear market still holds firmer ground in cases with vertical excess, mixed dentition limitations, and tighter budgets, where clear aligners do not solve every clinical or economic issue. The substitution effect is therefore uneven rather than universal, with the mild-to-moderate end most exposed first. This shifts the case mix of headgear more than it removes the category altogether.

Other drivers and restraints analyzed in the detailed report include:

- Improved Customization Through Digital Scanning and 3D Printing

- Smart Compliance Tracking and Wear-Time Monitoring

- Wear-Time Compliance and Social Visibility Friction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cervical Pull Headgear held 38.31% share in 2025, which kept it as the leading product type in the orthodontic headgear market. Its lead reflects a simple clinical and economic fit, because it remains the default choice for Class II molar distalization in many pediatric cases. Clinicians continue to favor it when they need a familiar appliance that is straightforward to prescribe, easy to adjust, and less expensive than more customized alternatives. That cost accessibility matters because the orthodontic headgear market still serves many families and clinics that balance treatment effectiveness with affordability. Cervical pull designs also benefit from the scale of the Class II treatment pool, which keeps baseline demand stable even when premium aligner options expand.

High-Pull Headgear is the fastest-growing product segment, with a CAGR of 6.38% over 2026 to 2031, because vertical control is becoming a more visible treatment priority in complex cases. That growth reflects its usefulness in open-bite tendencies and in patients who present with both skeletal discrepancy and vertical growth excess. Reverse-Pull Headgear, or facemask designs, remains a narrower but clinically distinct sub-segment that serves Class III correction during maxillary protraction in younger patients. The orthodontic headgear industry still depends on this type because skeletal Class III correction in growing children remains far less substitutable than mild Class II treatment. Product innovation is also entering this category through digitally fabricated J-hook concepts, which suggests that even mature product groups are moving toward hybrid digital and traditional production models.

Stainless Steel held 67.24% share in 2025, which made it the dominant material base across the orthodontic headgear market. Its position remains strong because high-load extraoral mechanics still require structural integrity, fatigue resistance, and stable force delivery over time. These properties are difficult to replace when appliances need to generate sustained orthopedic forces through outer bow and inner bow configurations. For that reason, metal remains central in the orthodontic headgear market even as external components evolve toward lighter designs. Stainless steel also fits established clinical workflows, which reduces the switching incentive for practices that already manage a large volume of traditional headgear cases.

Plastic is the fastest-growing material segment, with a CAGR of 6.52% through 2031, as digital fabrication makes lighter and more patient-friendly non-metal components easier to produce. Its momentum is tied to visible parts such as head caps, chin cups, and adjustment elements, where comfort and aesthetics matter more than peak load-bearing performance. Silicone, nylon, and rubber continue to play supporting roles in pads, straps, and elastic elements, especially where patient comfort influences daily wear. Over time, the orthodontic headgear market is likely to split more clearly between metal for core force delivery and polymers for fit, comfort, and customization. This shift helps smaller fabricators enter selected niches, but it also compresses price premiums in commoditized components as desktop printing becomes more accessible.

Complete Report Scope:

- By Product Type

- Cervical Pull Headgear

- High-Pull Headgear

- Reverse-Pull Headgear

- Facemask Headgear

- By Material Type

- Stainless Steel

- Plastic

- Rubber

- Silicone

- Nylon

- By Application

- Malocclusion Correction

- Overbite Treatment

- Underbite Treatment

- Crossbite Treatment

- By Age Group

- Children

- Teens

- Adults

- By End User

- Dental Clinics

- Hospitals

- Orthodontic Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 38.22% share in 2025, which made it the largest regional base in the orthodontic headgear market size. The region benefits from a mature private-pay orthodontic structure, strong referral links between general dentists and specialists, and clinician familiarity with early orthopedic intervention. The United States remains the core demand center because extraoral mechanics are well understood in pediatric orthodontic practice and because families often enter treatment earlier than in many emerging regions. Canada and Mexico add smaller volumes, but they also widen the regional base through urban treatment demand and specialist care availability. This makes North America a stable revenue anchor for the orthodontic headgear market even as faster growth shifts elsewhere.

Asia-Pacific is projected to expand at a CAGR of 6.65% through 2031, which makes it the fastest-growing geography in the orthodontic headgear market. Growth is being led by China, India, South Korea, and Australia, though the pattern is not uniform across the region. South Korea and Australia show stronger digital maturity, while India, Southeast Asia, and inland Chinese cities depend more on clinic network expansion and better specialist reach. The region also benefits from rising middle-class spending on pediatric dental aesthetics and from broader access to orthodontic consultation outside the largest metro areas. Align Technology's 2025 APAC launch of an Invisalign system with mandibular advancement also confirms that major companies see growing Class II treatment demand in the region, even though that product competes with headgear in part of the addressable pool.

Europe remains a mature but active region for the orthodontic headgear market, with Germany, the United Kingdom, and France continuing to set the tone for product quality and specialist practice standards. Larger, better-documented suppliers tend to be favored in this region because procurement expectations are more demanding and clinicians place greater weight on material reliability and regulatory readiness. South America and the Middle East and Africa are earlier-stage opportunity areas, where urban dental demand and expanding care infrastructure are gradually broadening the patient base for growth-oriented orthodontic treatment. This leaves the orthodontic headgear market with a balanced geographic profile, where North America provides scale, Asia-Pacific provides speed, and Europe and emerging regions provide selective replacement and expansion demand.

- Adenta GmbH

- American Orthodontics

- DB Orthodontics

- Dentaurum GmbH and Co. KG

- Dentsply Sirona

- G and H Orthodontics

- GAC International

- Great Lakes Dental Technologies

- Henry Schein

- Ormco Corporation (Envista Holdings Corporation)

- Ortho Kinetics Corporation

- Ortho Technology, Inc.

- Orthodynamic Supplies Ltd.

- Plaza Orthodontics

- Rocky Mountain Orthodontics

- Solventum Corporation

- TP Orthodontics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Malocclusion Burden and Earlier Orthodontic Intervention

- 4.2.2 Expanding Pediatric and Adolescent Orthodontic Treatment Adoption

- 4.2.3 Improved Customization Through Digital Scanning and 3D Printing

- 4.2.4 Smart Compliance Tracking and Wear-Time Monitoring

- 4.2.5 Dental Infrastructure Expansion in Secondary Cities

- 4.2.6 Rising Demand for Lower-Cost Functional Alternatives to Complex Surgery

- 4.3 Market Restraints

- 4.3.1 Clear Aligner Substitution in Mild to Moderate Class II Cases

- 4.3.2 Wear-Time Compliance and Social Visibility Friction

- 4.3.3 Regulatory and Biocompatibility Burden for Small Manufacturers

- 4.3.4 Limited Clinical Preference in Adult Aesthetic-Oriented Cases

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Cervical Pull Headgear

- 5.1.2 High-Pull Headgear

- 5.1.3 Reverse-Pull Headgear

- 5.1.4 Facemask Headgear

- 5.2 By Material Type

- 5.2.1 Stainless Steel

- 5.2.2 Plastic

- 5.2.3 Rubber

- 5.2.4 Silicone

- 5.2.5 Nylon

- 5.3 By Application

- 5.3.1 Malocclusion Correction

- 5.3.2 Overbite Treatment

- 5.3.3 Underbite Treatment

- 5.3.4 Crossbite Treatment

- 5.4 By Age Group

- 5.4.1 Children

- 5.4.2 Teens

- 5.4.3 Adults

- 5.5 By End User

- 5.5.1 Dental Clinics

- 5.5.2 Hospitals

- 5.5.3 Orthodontic Centers

- 5.5.4 Other End Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Adenta GmbH

- 6.3.2 American Orthodontics

- 6.3.3 DB Orthodontics

- 6.3.4 Dentaurum GmbH and Co. KG

- 6.3.5 Dentsply Sirona

- 6.3.6 G and H Orthodontics

- 6.3.7 GAC International

- 6.3.8 Great Lakes Dental Technologies

- 6.3.9 Henry Schein, Inc.

- 6.3.10 Ormco Corporation (Envista Holdings Corporation)

- 6.3.11 Ortho Kinetics Corporation

- 6.3.12 Ortho Technology, Inc.

- 6.3.13 Orthodynamic Supplies Ltd.

- 6.3.14 Plaza Orthodontics

- 6.3.15 Rocky Mountain Orthodontics

- 6.3.16 Solventum Corporation

- 6.3.17 TP Orthodontics, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment