|

시장보고서

상품코드

2072832

수의용 정형외과 임플란트 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Veterinary Orthopedic Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

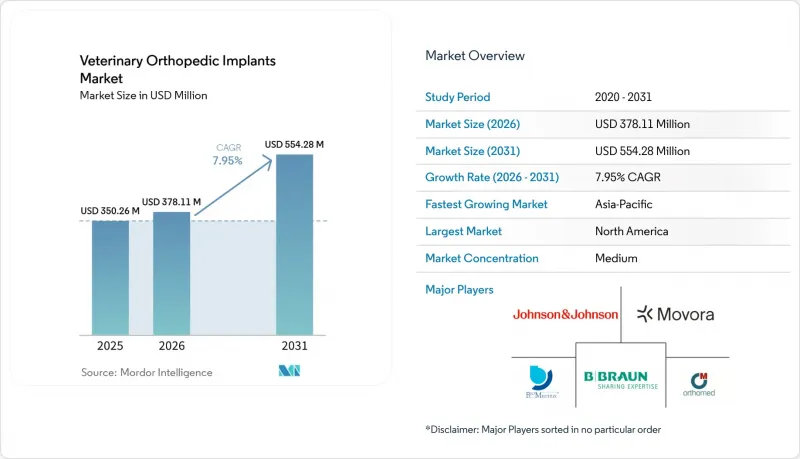

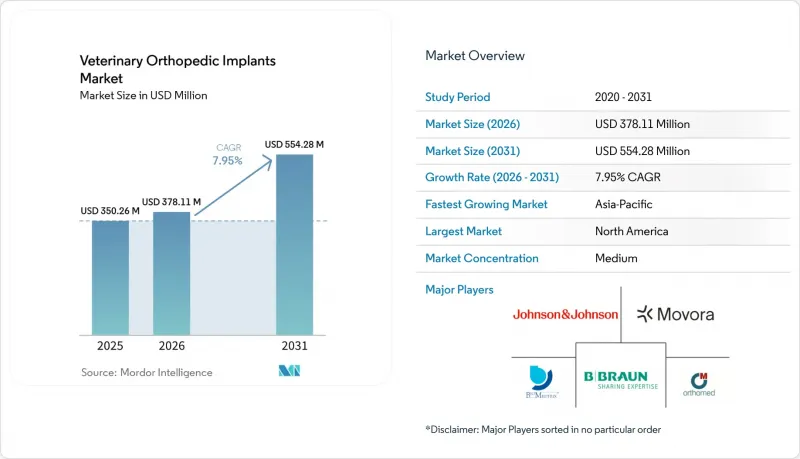

Mordor Intelligence에 의하면, 수의용 정형외과 임플란트 시장 규모는 2025년에 3억 5,026만 달러로 평가되었고 2026년 3억 7,811만 달러에서 2031년까지 5억 5,428만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.95%를 나타낼 전망입니다.

본 보고서는 제품 유형(플레이트(잠금 압축 플레이트 등), 나사, 핀·와이어 등), 동물 종(개, 고양이 등), 재질(티타늄, 스테인리스 스틸 등), 적용 분야(외상 고정, 관절 치환 등), 최종 사용자(동물병원 등), 지역(북미 등)별로 분류되어 있습니다. 예측치는 금액(달러)으로 표시되어 있습니다.

전 세계 수의용 정형외과 임플란트 시장 동향 및 인사이트

반려동물의 정형외과 진료 건수 증가

수의용 정형외과 임플란트 시장은 반려동물 수 증가와 반려동물의 수명 연장으로 인해 퇴행성 근골격계 질환의 발생률이 높아지고 있는 점에 힘입어 성장을 이어가고 있습니다. 미국수의사협회(AVMA)의 보고서에 따르면, 2025년에는 미국 가구의 58.6%가 반려동물을 키우고 있으며, 이는 10년 전의 56.8%에서 증가한 수치입니다. 또한, 반려견을 키우는 가구 수는 1년 동안 400만 가구 순 증가를 기록하며, 2025년에는 7,100만 가구에 달했습니다. 이러한 구조적 확대는 임상적으로도 중요한 의미를 지닙니다. 왜냐하면 반려동물 가구 증가가 단순히 반려동물의 수가 늘어난다는 것을 의미할 뿐만 아니라, 십자인대 질환, 기형, 노화에 따른 골절 위험이 높아지는 나이에 도달하는 동물이 늘어난다는 것을 의미하기 때문입니다.

수의용 정형외과 임플란트 시장은 일상적인 수의 의료 서비스의 향상으로 인해 개와 고양이의 수명이 늘어나고 있다는 사실로부터도 혜택을 보고 있습니다. 이로 인해 개별 동물의 생애에서 노년기에 고정술이나 재건술을 받을 가능성이 높아지고 있습니다. 이러한 수요는 특히 중형-대형견에 집중되어 있으며, 전십자인대 질환과 고관절 이형성증이 선택적 정형외과 의뢰의 상당 부분을 계속 차지하고 있습니다. 일부 지역에서는 환자 수가 전문의의 대응 능력을 초과하는 속도로 증가하고 있기 때문에 수의용 정형외과 임플란트 시장에서는 의사 결정 시간을 단축하고, 보다 예측 가능한 수술법 선택을 통해 외과의사가 더 많은 환자를 치료할 수 있도록 지원하는 표준화된 시스템이 선호되고 있습니다.

기본 수준의 수술 능력 확대

수의용 정형외과 임플란트 시장이 확대되고 있는 배경에는 그동안 많은 정형외과 사례가 치료되지 않은 채로 남아 있거나 보존적 치료만으로 관리되던 지방 도시나 교외 진료권에서 의뢰 수준의 진료 능력이 점차 보급되고 있는 점도 한 요인으로 꼽힙니다. Vimian Group은 2024년 연차 보고서에서 십자인대 수술이 필요한 개 중 3마리 중 1마리만이 현재 해당 수술을 받고 있다고 밝혔으며, 이는 접근성 확대를 통해 충족되지 않은 수요를 적극적인 수술 수요로 전환할 여지가 여전히 있음을 보여줍니다. 해당 보고서에서는 Movora사가 2024년에 현장 수술 워크숍을 통해 5,150명의 수의학 전문가를 교육하고, 4,000명에 가까운 온라인 학습자를 지원한 사실도 언급하고 있습니다. 이는 연수가 임상적 지원 수단일 뿐만 아니라, 상업적 성장 도구로도 활용되고 있음을 보여줍니다. 이 교육 모델이 중요한 이유는 소개 의료기관에서 표준화된 기법을 배운 외과의사가 그 기법을 일반 진료나 복합 진료 현장에 적용함으로써, 치료 대상이 되는 환자층을 점차 확대해 나가기 때문입니다.

수의용 정형외과 임플란트 시장은 이러한 보급의 혜택을 누리고 있습니다. 이는 고품질의 플레이트와 스크류, 그리고 수술별 전용 시스템에 능숙한 외과의사의 기반이 확대되기 때문입니다. 또한, 임플란트 설계, 기구 및 교육은 개별 구매 결정이 아닌 세트 형태로 채택되는 경향이 있기 때문에 공급업체에 대한 지속적인 선호도도 형성됩니다.

고액의 수술 비용과 동물의 경제적 가치

수술 비용 부담 가능성은 수의용 정형외과 임플란트 시장에서 여전히 가장 뚜렷한 제약 요인 중 하나입니다. 일반적인 정형외과 수술 비용은 보험 보상이 없는 경우, 많은 반려인이 지불할 각오를 하고 있는 금액을 훨씬 초과하는 경우가 많기 때문입니다. NAPHIA의 벤치마크 범위에 따르면, TPLO 수술 비용은 4,000-8,000달러, 전방십자인대(ACL) 및 고관절 질환에 대한 정형외과 수술 비용은 3,000-7,000달러로 알려져 있으며, 이로 인해 수요의 상당 부분이 본인 부담에 대한 부담으로 인해 계속해서 위축되고 있습니다. 이러한 비용 측면의 압박은 저소득층의 상황, 반려인이 치료비와 반려동물의 경제적 가치를 비교 검토하는 경우, 특히 부유한 도시 지역의 반려동물 시장을 제외한 곳에서는 더욱 두드러지게 나타납니다. Vimian Group의 2024년 연차 보고서에 따르면, 십자인대 수술이 필요한 개 중 현재 치료를 받고 있는 개는 3마리 중 1마리에 불과한 것으로 추정되며, 이는 실제 수술 건수가 생물학적 필요에 비해 여전히 얼마나 낮은 수준에 머물러 있는지를 보여줍니다.

따라서 수의용 정형외과 임플란트 시장에서 수술 건수가 정체되어 있는 것은 임상적인 해결책이 없기 때문이 아니라, 반려인이 "이익", "비용" ,'정서적 가치'를 종합적으로 비교·검토한 결과, 치료에 대한 동의를 얻지 못했기 때문입니다. 단계적인 치료 계획을 제공하거나 보험사와 더욱 긴밀히 협력하는 공급업체나 동물병원은 가격대를 전반적으로 낮추도록 강요하지 않으면서도, 이러한 미뤄져 온 수요를 발굴하는 데 유리한 입장에 있습니다.

부문별 분석

2025년에는 플레이트가 매출의 38.31%를 차지하며, 수의용 정형외과 임플란트 시장 내 제품 유형 중 1위를 차지하고 있습니다. 이러한 장점은 골절 고정, 교정 절골술, 경골 재정렬 등 외과의사가 다양한 유형의 증례에서 예측 가능한 고정이 필요한 분야에서 폭넓게 활용될 수 있음을 반영합니다. 로킹 압축 플레이트 및 TPLO 전용 플레이트의 설계는 수술의 표준화에 부합하며, 수술 건수가 많은 개에서 안정적인 고정을 뒷받침하기 때문에 계속해서 이 매출의 상당 부분을 차지하고 있습니다. 수의용 정형외과 임플란트 업계에서 플레이트는 일상적인 외상 치료부터 보다 고도의 재건 수술에 이르기까지 폭넓게 활용될 수 있기 때문에 병원이나 의뢰 외과 의사들에게 여전히 핵심 재고 품목으로 자리 잡고 있습니다. 이러한 도입 실적이 갖는 장점은 매우 중요하며, 플레이트 시리즈와 관련 기구의 사용법에 대해 한 번 교육을 받은 팀은 구매 행태가 정착되기 쉬운 경향이 있기 때문입니다.

스크류는 2031년까지 연평균 성장률(CAGR) 10.38%를 기록하며 성장할 것으로 예상되며, 수의용 정형외과 임플란트 시장에서 가장 빠르게 성장하는 제품 유형이 될 전망입니다. 수요를 주도하고 있는 것은 저침습적인 TPLO 및 TTA 수술 절차에 적합하며, 점점 더 표준화되고 있는 수술에서 저프로파일 고정을 가능하게 하는 잠금형 및 캐뉼레이트형 나사입니다. 또한, 외과의사들은 폐쇄 정복술과의 호환성을 높이 평가했습니다. 이를 통해 특정 증례에서 골막 손상을 줄이고, 뼈의 조기 유합을 촉진할 수 있기 때문입니다. 『Veterinary and Comparative Orthopaedics and Traumatology』지에 게재된 2026년 연구에 따르면, 체중 45-70 kg의 개에게 3.5 mm TPLO용 잠금 압축 플레이트를 사용한 경우, 경골 고원각의 유지 및 골유합 결과에 유의미한 편차가 관찰되었습니다. 이는 대형견의 해부학적 구조에 표준 임플란트를 적용하는 데 따르는 기술적 과제를 여실히 드러내고 있습니다. 주요 치료법 외에도, 핀과 와이어는 여전히 소동물의 골절 치료에서 중요한 역할을 하고 있는 반면, 관절 치환용 임플란트는 전문의의 기술이 성숙해짐에 따라 성장하고 있는 고가이며 판매량이 적은 분야로 분류됩니다.

2025년 동물 유형별 매출에서 개가 차지하는 비중은 67.24%이며, 개는 수의용 정형외과 임플란트 시장 수요를 주도하는 주요 요인으로 작용하고 있습니다. 이러한 우위는 개 환자의 수가 많다는 점 외에도, 십자인대 질환, 고관절 이형성증, 외상성 골절에 걸리기 쉬운 중형-대형 견종에서 나타나는 높은 정형외과적 부담과 밀접한 관련이 있습니다. 또한, 개의 경우 순수한 보존적 치료만 시행되는 것이 아니라 고액의 안정화 조치나 재건 수술이 이루어지는 경우가 많기 때문에 치료를 받은 개 한 마리당 수익도 높은 임베디드니다. 미국수의사협회(AVMA)의 보고서에 따르면, 미국의 반려견 수는 8,730만 마리에 달하며, 이는 개가 수의용 정형외과 임플란트 시장의 상업적 중심지로 계속 자리매김하고 있는 이유를 뒷받침합니다. 수의용 정형외과 임플란트 업계에서 개의 수술 건수는 거의 모든 주요 공급업체에서 제품 개발, 교육 우선순위, 재고 계획을 계속해서 좌우하고 있습니다.

고양이 시장은 2031년까지 9.52%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측되며, 이에 따라 고양이 정형외과 분야는 동물 종 중에서 가장 강력한 성장 궤도를 그리고 있습니다. 미국 반려동물 제품 협회(APPA)의 보고서에 따르면, 2024년 고양이 사육 마릿수는 23% 증가했으며, 이러한 가구 동향의 변화로 인해 고양이의 골절 치료, 무릎 관절 안정화 및 슬개골 탈구 치료 분야의 환자 기반이 확대되고 있습니다. 미국수의사협회(AVMA)의 데이터에 따르면, 고양이 사육 마릿수가 5,830만 마리에서 7,630만 마리로 증가한 것으로 나타났으며, 이는 향후 정형외과 치료가 필요한 고양이 집단이 더욱 대규모로 확대되고 연령대가 낮아지고 있음을 시사합니다. 또한, 고양이의 선택적 정형외과 수술에 대한 반려인의 수용도가 높아지고 있는 점도 이러한 성장을 뒷받침하고 있습니다. 이 분야는 그동안 인지도와 치료율 두 가지 측면에서 모두 개에 비해 뒤처져 있었습니다. 현재 사용되고 있는 고양이용 임플란트의 대부분은 고양이 전용으로 설계된 것이 아니라, 개용 시스템을 개조하여 사용하는 것입니다. 따라서 생체역학적 안정성을 해치지 않으면서 소형화를 실현할 수 있는 기업에게는 분명한 제품 공백이 존재합니다.

지역별 분석

2025년, 북미는 매출의 41.22%를 차지하며, 수의용 정형외과 임플란트 시장에서 지역별 1위를 기록하고 있습니다. 이 지역은 높은 수준의 반려동물 의료비, 전문의에 의한 긴밀한 의뢰 네트워크, 그리고 고액 수술을 감당할 수 있도록 보험에 가입된 반려동물이 많다는 점 등의 혜택을 누리고 있습니다. NAPHIA의 보고서에 따르면, 2024년 미국의 반려동물 보험 총 인수 보험료는 47억 달러이며, 2026년 말까지 60억 달러를 넘어설 것으로 전망됩니다. 이로 인해 북미에서는 정형외과 수술에 대한 보험 급여가 강력한 호재로 작용하고 있습니다. 또한 APPA의 보고서에 따르면, 미국의 반려동물 산업 지출은 2025년에 1,580억 달러, 2026년에는 1,650억 달러에 달할 것으로 예상되며, 그중에서도 수의학 서비스의 비중이 가장 빠르게 확대되고 있어 해당 지역의 지출 규모를 뒷받침하고 있습니다. 유럽은 여전히 2위 지역 블록이지만, 남미는 규모가 작고 도시 지역의 반려동물 사육률이 상승하고 있음에도 불구하고, 경제적 부담이나 전문의 확보와 같은 제약에 여전히 직면해 있습니다.

유럽의 수의용 정형외과 임플란트 시장에서의 입지는 성숙한 의뢰 체계와 확립된 품질 관리 시스템을 점점 더 중시하는 엄격한 규제 환경에 힘입어 공고해지고 있습니다. EU 의료기기 규정에 따라, 회원국 간에 거래되는 임플란트의 생체적합성에 관한 문서화 및 시판 후 조사에 대한 기대가 높아지고 있으며, 이로 인해 소규모 제조업체의 규정 준수 부담이 증가하는 반면, 충분한 자원을 보유한 공급업체에게는 더욱 견고한 경쟁 우위가 생겨나고 있습니다. 또한, 이 지역은 독일, 영국, 프랑스, 스위스의 강력한 수의외과 생태계의 혜택을 누리고 있습니다. 이 국가들에서는 외과 의사가 주도하는 제품 개발과 체계화된 도입 경로가 고품질의 고정 및 재건 수술에 대한 수요를 뒷받침하고 있습니다. 따라서 유럽 시장에서는 수술 기술의 고도화와 규제의 강화가 서로 별개의 궤도가 아니라 상호 연동하며 진행되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.65%로 확대될 것으로 예측되며, 수의용 정형외과 임플란트 시장에서 가장 높은 성장률을 보일 것으로 전망됩니다. 중국, 일본, 인도, 호주, 한국은 반려동물에 대한 지출 증가와 동물병원 및 전문 교육에 대한 지속적인 투자가 맞물리면서 계속해서 주요 수요 거점으로 자리 잡고 있습니다. 도시화와 중산층의 확대에 따라, 고도의 정형외과 의료에 대한 수용이 확대되고 있습니다. 특히 반려동물 분야에서는 반려인들이 운동 기능 회복을 위한 수술 비용을 지불하려는 의지가 높아지고 있습니다. 중동 및 아프리카는 소규모 기반에서 발전하는 단계에 있지만, GCC 국가들에서는 말의 의료 서비스와 고급 반려동물 사육을 중심으로 고급 병원의 수용 능력을 확충하고 있습니다. 또한 인도는 합리적인 가격의 고정 시스템에 대한 국내 수요 증가와 인근 지역으로의 수출 지향적 공급을 뒷받침하는 제조 거점을 모두 갖추고 있어, 두 가지 측면에서 두드러진 기회를 제공합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the veterinary orthopedic implants market size was valued at USD 350.26 million in 2025 and is estimated to grow from USD 378.11 million in 2026 to reach USD 554.28 million by 2031, at a CAGR of 7.95% during the forecast period (2026-2031).

This report is Segmented by Product Type (Plates [Locking Compression Plates, and More], Screws, Pins & Wires, and More), Animal Type (Dog, Cat, and More), Material Type (Titanium, Stainless Steel, and More), Application (Trauma Fixation, Joint Replacement, and More), End User (Veterinary Hospitals, and More), and Geography (North America, and More). Forecasts are Provided in Value (USD).

Global Veterinary Orthopedic Implants Market Trends and Insights

Rising Companion Animal Orthopedic Caseload

The Veterinary orthopedic implants market is being lifted by a larger companion animal population and by longer pet lifespans that increase the incidence of degenerative musculoskeletal disease. The American Veterinary Medical Association reported that 58.6% of U.S. households owned a pet in 2025, up from 56.8% a decade earlier, and the dog-owning base reached 71 million U.S. households in 2025 after a net addition of 4 million households in 1 year. The same structural expansion matters clinically because a larger household base does not just mean more pets, it also means more animals reaching ages where cruciate disease, dysplasia, and age-related fracture risk become more common.

The Veterinary orthopedic implants market also benefits from the fact that improved routine veterinary care is keeping dogs and cats alive longer, which raises the probability of later-life fixation and reconstruction procedures over each animal's lifetime. This demand is especially concentrated in medium-to-large breed dogs, where cranial cruciate ligament disease and hip dysplasia continue to generate a high share of elective orthopedic referrals. As the case load expands faster than specialist capacity in several regions, the Veterinary orthopedic implants market is favoring standardized systems that shorten decision time and help surgeons move through a larger caseload with more predictable technique selection.

Expansion Of Referral-Grade Surgical Capability

The Veterinary orthopedic implants market is also advancing because more referral-grade capability is reaching secondary cities and suburban catchments that previously sent many orthopedic cases untreated or managed conservatively. Vimian Group stated in its 2024 Annual Report that only 1 in 3 dogs requiring cruciate ligament surgery currently receives the procedure, which shows that access expansion still has room to convert unmet need into active procedural demand. The same report noted that Movora trained 5,150 veterinary professionals through on-site surgery workshops and supported nearly 4,000 online learners in 2024, which shows how training is being used as a commercial growth tool as well as a clinical enabler. This education model matters because surgeons who learn standardized methods at referral centers often carry those methods into general or mixed specialty settings, which gradually widens the treated population.

The Veterinary orthopedic implants market gains from that diffusion because it expands the installed base of surgeons comfortable with premium plate, screw, and procedure-specific systems. It also creates lasting vendor preference, since implant design, instrumentation, and training tend to be adopted together rather than as separate buying decisions.

High Procedure Cost Versus Animal Economic Value

Procedure affordability remains one of the clearest limits on the Veterinary orthopedic implants market because common orthopedic surgeries often cost far more than many owners are prepared to spend without reimbursement support. NAPHIA's benchmark ranges place TPLO surgery at USD 4,000 to USD 8,000 and orthopedic surgery for ACL and hip conditions at USD 3,000 to USD 7,000, which keeps a large part of demand exposed to out-of-pocket resistance. This cost pressure is sharper in lower-income settings and in cases where owners compare treatment expense with the perceived economic value of the animal, especially outside affluent urban companion animal markets. Vimian Group's 2024 Annual Report estimated that only 1 in 3 dogs requiring cruciate surgery currently receives treatment, which shows how far realized procedure volume still sits below biological need.

The Veterinary orthopedic implants market therefore loses volume not because clinical solutions are absent, but because owner approval breaks down at the point where benefit, cost, and emotional value are weighed together. Suppliers and hospitals that offer tiered treatment pathways or work more closely with insurers are better placed to unlock that deferred demand without forcing a broad move down the pricing curve.

Other drivers and restraints analyzed in the detailed report include:

- 3D Printed Patient-Specific Implants And Guides

- Growth In Pet Insurance Reimbursement For Orthopedic Care

- Limited Specialist Surgeon Availability Outside Major Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plates accounted for 38.31% of revenue in 2025, giving them the leading position across product categories in the Veterinary orthopedic implants market. Their lead reflects broad utility across fracture fixation, corrective osteotomy, and tibial realignment, where surgeons need predictable fixation across many case types. Locking compression plates and TPLO-specific plate designs continue to anchor a large share of this revenue because they align with procedure standardization and support stable fixation in high-volume canine cases. Within the Veterinary orthopedic implants industry, plates remain the foundational inventory line for hospitals and referral surgeons because they support both routine trauma and more advanced reconstructive work. That installed-base advantage matters because once a team is trained around a plate family and its instrumentation, purchasing behavior tends to remain sticky.

Screws are projected to grow at a 10.38% CAGR through 2031, making them the fastest-growing product type in the Veterinary orthopedic implants market. Demand is being lifted by locking and cannulated variants that fit minimally invasive TPLO and TTA workflows and support lower-profile fixation in increasingly standardized procedures. Surgeons also value screws for their compatibility with closed-reduction methods, which can reduce periosteal disruption and support faster bone consolidation in selected cases. A 2026 study in Veterinary and Comparative Orthopaedics and Traumatology found meaningful variability in tibial plateau angle maintenance and bone healing outcomes when a 3.5 mm TPLO locking compression plate was used in dogs weighing 45 to 70 kg, which underlines the engineering challenge of adapting standard hardware across large-breed anatomy. Beyond the leading lines, pins and wires still hold an important role in small-animal fracture management, while joint replacement implants sit in a premium, lower-volume tier that grows as specialist capability matures.

Dogs contributed 67.24% of revenue by animal type in 2025, which makes them the core demand driver in the Veterinary orthopedic implants market. That dominance is tied to the size of the canine patient pool and to the high orthopedic burden seen in medium-to-large breeds prone to cruciate ligament disease, hip dysplasia, and trauma-related fractures. Dog cases also tend to produce more revenue per treated animal because they more often involve high-value stabilization or reconstruction procedures rather than purely conservative management. The American Veterinary Medical Association reported a U.S. dog population of 87.3 million, which reinforces why the canine base remains the commercial center of the Veterinary orthopedic implants market. Within the Veterinary orthopedic implants industry, canine procedure volume continues to shape product development, training priorities, and inventory planning across almost every major supplier.

Cats are expected to record the fastest CAGR at 9.52% through 2031, which gives feline orthopedics the strongest growth profile among animal types. The American Pet Products Association reported a 23% increase in cat ownership in 2024, and that household shift is widening the patient base for feline fracture repair, stifle stabilization, and patellar luxation treatment. The American Veterinary Medical Association also showed owned cat numbers rising from 58.3 million to 76.3 million, which points to a larger and younger pool of future orthopedic candidates. Growth is also being helped by stronger owner willingness to authorize elective orthopedic work for cats, a category that historically lagged dogs in both recognition and treatment rates. Most current feline implants still adapt canine systems rather than fully purpose-built feline designs, which leaves a clear product gap for companies able to miniaturize without compromising biomechanical stability.

Complete Report Scope:

- By Product Type

- Plates

- Locking Compression Plates

- Locking Distal Plates

- Dynamic Compression Plates

- Reconstruction Plates

- TPLO Plates

- TTA Plates

- Screws

- Bone Screws

- Cortical Screws

- Cancellous Screws

- Locking Screws

- Cannulated Screws

- Pins and Wires

- Intramedullary Pins

- Kirschner Wires

- Total Elbow Replacement Implants

- Total Hip Replacement Implants

- Total Knee Replacement Implants

- Fixation Systems

- Other Product Types

- Plates

- By Animal Type

- Dog

- Cat

- Horses

- Other Animals

- By Material Type

- Titanium

- Stainless Steel

- Bioabsorbable Polymers

- Other Materials

- By Application

- Trauma Fixation

- Joint Replacement

- Ligament Reconstruction

- Osteoarthritis Management

- Other Applications

- By End User

- Veterinary Hospitals

- Veterinary Clinics

- Veterinary Surgical Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 41.22% of revenue in 2025, which gave it the leading regional position in the Veterinary orthopedic implants market share. The region benefits from high pet healthcare spending, dense specialist referral networks, and a large insured companion animal base that supports acceptance of high-value surgery. NAPHIA reported USD 4.7 billion in U.S. pet insurance gross written premium in 2024 and projected more than USD 6 billion by the end of 2026, which gives North America a strong reimbursement tailwind for orthopedic procedures. APPA also reported U.S. pet industry expenditures of USD 158 billion in 2025 and USD 165 billion in 2026, with veterinary services capturing the fastest-growing share, which reinforces the region's spending depth. Europe remains the second-largest regional block, while South America is smaller and still constrained by affordability and specialist availability even as urban pet ownership rises.

Europe's position in the Veterinary orthopedic implants market rests on mature referral pathways and a tighter regulatory environment that increasingly rewards established quality systems. The EU Medical Device Regulation is raising expectations around biocompatibility documentation and post-market surveillance for implants traded across member states, which creates a higher compliance burden for smaller producers and a stronger moat for better-resourced suppliers. The region also benefits from strong veterinary surgery ecosystems in Germany, the United Kingdom, France, and Switzerland, where surgeon-led product development and structured referral channels support premium fixation and reconstruction demand. This makes Europe a market where procedural sophistication and regulatory discipline move together rather than in separate tracks.

Asia-Pacific is projected to expand at a 9.65% CAGR through 2031, giving it the fastest growth profile in the Veterinary orthopedic implants market size. China, Japan, India, Australia, and South Korea remain the core demand centers because they combine rising companion animal spending with ongoing investment in veterinary hospitals and specialist education. Urbanization and middle-class expansion are widening acceptance of advanced orthopedic care, especially in companion animal segments where owners are increasingly willing to pay for mobility-restoring procedures. The Middle East and Africa are developing from a smaller base, but GCC countries are building higher-end hospital capacity around equine medicine and premium pet ownership. India also stands out as a dual opportunity because it offers both expanding domestic demand for affordable fixation systems and a manufacturing base that can support export-oriented supply into neighboring regions.

- Arthrex Vet Systems

- Auxein Medical

- B. Braun

- BioMedtrix LLC

- BlueSAO Co., Ltd.

- Johnson & Johnson

- Fusion Implants

- GerVetUSA Inc.

- IMEX Veterinary, Inc.

- Innoplant Medizintechnik GmbH

- Integra LifeSciences

- Intrauma S.p.A.

- KYON AG

- Movora

- Narang Medical

- New Generation Devices, Inc.

- Orthomed (UK) Ltd.

- Rita Leibinger GmbH and Co. KG

- Securos Surgical

- Veterinary Instrumentation

- Veterinary Orthopedic Implants

- Vimian Group AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Companion Animal Orthopedic Caseload

- 4.2.2 Expansion of Referral-Grade Surgical Capability

- 4.2.3 3D Printed Patient-Specific Implants and Guides

- 4.2.4 Growth in Pet Insurance Reimbursement for Orthopedic Care

- 4.2.5 Standardization of Minimally Invasive TPLO and TTA Protocols

- 4.2.6 Cross-Border Sourcing of Veterinary-Grade Implant Systems

- 4.3 Market Restraints

- 4.3.1 High Procedure Cost Versus Animal Economic Value

- 4.3.2 Limited Specialist Surgeon Availability Outside Major Cities

- 4.3.3 Fragmented Reimbursement for Veterinary Orthopedic Procedures

- 4.3.4 Import Tariffs and Metal Input Volatility

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Plates

- 5.1.1.1 Locking Compression Plates

- 5.1.1.2 Locking Distal Plates

- 5.1.1.3 Dynamic Compression Plates

- 5.1.1.4 Reconstruction Plates

- 5.1.1.5 TPLO Plates

- 5.1.1.6 TTA Plates

- 5.1.2 Screws

- 5.1.2.1 Bone Screws

- 5.1.2.2 Cortical Screws

- 5.1.2.3 Cancellous Screws

- 5.1.2.4 Locking Screws

- 5.1.2.5 Cannulated Screws

- 5.1.3 Pins and Wires

- 5.1.3.1 Intramedullary Pins

- 5.1.3.2 Kirschner Wires

- 5.1.4 Total Elbow Replacement Implants

- 5.1.5 Total Hip Replacement Implants

- 5.1.6 Total Knee Replacement Implants

- 5.1.7 Fixation Systems

- 5.1.8 Other Product Types

- 5.1.1 Plates

- 5.2 By Animal Type

- 5.2.1 Dog

- 5.2.2 Cat

- 5.2.3 Horses

- 5.2.4 Other Animals

- 5.3 By Material Type

- 5.3.1 Titanium

- 5.3.2 Stainless Steel

- 5.3.3 Bioabsorbable Polymers

- 5.3.4 Other Materials

- 5.4 By Application

- 5.4.1 Trauma Fixation

- 5.4.2 Joint Replacement

- 5.4.3 Ligament Reconstruction

- 5.4.4 Osteoarthritis Management

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Veterinary Hospitals

- 5.5.2 Veterinary Clinics

- 5.5.3 Veterinary Surgical Centers

- 5.5.4 Other End Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Arthrex Vet Systems

- 6.3.2 Auxein Medical

- 6.3.3 B. Braun Vet Care GmbH

- 6.3.4 BioMedtrix LLC

- 6.3.5 BlueSAO Co., Ltd.

- 6.3.6 DePuy Synthes (Johnson & Johnson)

- 6.3.7 Fusion Implants

- 6.3.8 GerVetUSA Inc.

- 6.3.9 IMEX Veterinary, Inc.

- 6.3.10 Innoplant Medizintechnik GmbH

- 6.3.11 Integra LifeSciences Corporation

- 6.3.12 Intrauma S.p.A.

- 6.3.13 KYON AG

- 6.3.14 Movora

- 6.3.15 Narang Medical Limited

- 6.3.16 New Generation Devices, Inc.

- 6.3.17 Orthomed (UK) Ltd.

- 6.3.18 Rita Leibinger GmbH and Co. KG

- 6.3.19 Securos Surgical

- 6.3.20 Veterinary Instrumentation

- 6.3.21 Veterinary Orthopedic Implants

- 6.3.22 Vimian Group AB

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment