|

시장보고서

상품코드

2072855

미국의 의료보험자용 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Healthcare Payer Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

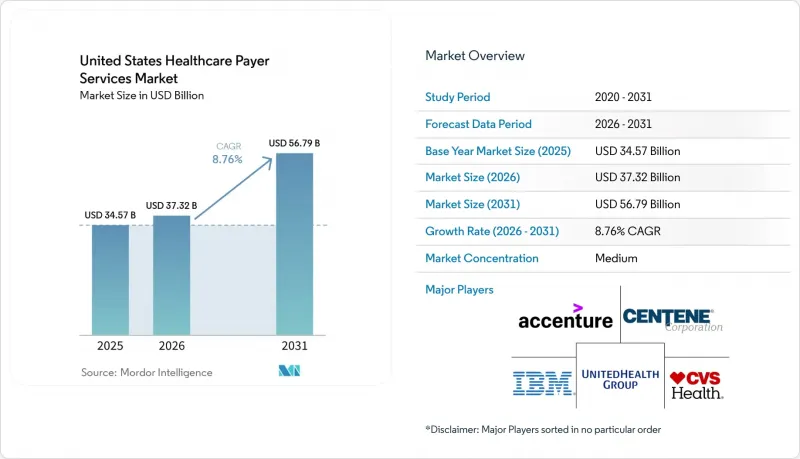

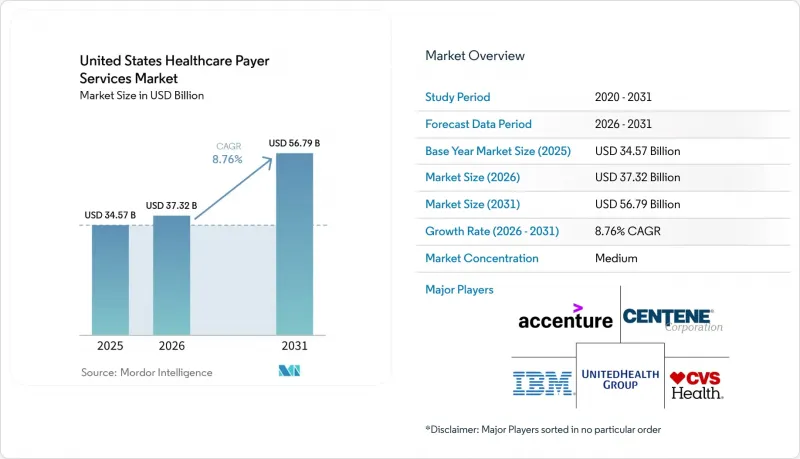

Mordor Intelligence에 의하면, 미국 의료보험자용 서비스 시장 규모는 2025년 345억 7,000만 달러, 2026년 373억 2,000만 달러에서 2031년까지 567억 9,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.76%를 나타낼 전망입니다.

본 보고서는 서비스 유형(청구 관리, 청구·지급, 부정 감지·지급 적정성 확보, 분석, KPO, ITO, BPO), 용도(건강보험, 생명보험, 매니지드 케어, 공공 프로그램), 최종 사용자(민간 보험사, 공공 보험사, 고용주 제공형 보험 플랜), 지역(미국)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국 의료보험자용 서비스 시장 동향 및 인사이트

보험금 청구 자동화 수요의 가속화: 수작업에 따른 심사 비용이 시스템적 수준에 도달했습니다.

미국의 의료보험자용 서비스 시장은 관리 업무 비용이 여전히 지나치게 높기 때문에 분산되어 있고 일부는 수작업에 의존하는 지급자 시스템 내에서 업무를 계속 처리할 수 없는 상황 덕분에 혜택을 보고 있습니다. CAQH의 보고서에 따르면, 전자 거래 처리를 통해 2024년 미국 의료 시스템은 2,580억 달러의 관리 비용을 절감할 수 있었으며, 한편 수작업 및 부분적으로 수작업이 이루어지는 업무 흐름의 추가 자동화를 통해 연간 210억 달러의 추가 절감 여지가 남아 있습니다. 이러한 격차가 중요한 이유는 기각된 청구, 보류 중인 청구, 그리고 예외 사항이 많은 청구가 여전히 재처리, 처리 기간 연장, 그리고 피할 수 있는 인건비를 발생시키고 있으며, 보험사들은 이러한 업무를 전문 운영 파트너에게 이관하는 것을 점점 더 선호하고 있기 때문입니다. 이러한 재처리 과정이 건강보험 플랜 외부로 이전되면, 공급업체는 워크플로우에 대한 투자를 많은 고객에게 분산시킬 수 있으며, 단일 보험사 내부에서 수행할 때보다 자동화의 경제성을 입증하기가 더 쉬워집니다. Aetna사는 2026년 5월, 자사의 '청구 처리 자동화 모델' 덕분에 복잡한 청구 처리 시간을 20% 이상 단축했다고 발표했습니다. 이는 실제 운영 중인 보험사 환경에서 실용적인 AI가 처리 시간을 얼마나 단축할 수 있는지를 시장에 보여주는 구체적인 사례입니다. 이와 유사한 성과를 추구하는 보험 상품이 늘어남에 따라, 미국의 의료보험자용 서비스 시장에서는 청구 업무, 워크플로우 규칙, 예외 처리, AI 기반 솔루션을 단일 제공 모델로 통합할 수 있는 공급업체에 대한 수요가 높아지고 있습니다.

가치 기반 의료 계약의 복잡화: 분석 업무의 외부 위탁이 필수적

미국의 의료보험자용 서비스 시장은 가치 기반 의료(Value-Based Care)에 의해서도 주도되고 있습니다. 이는 이러한 계약이 종량제(Fee-for-Service) 계약에 비해 정산이 훨씬 어렵기 때문입니다. AJMC는 청구 심사 및 청구 시스템을 포함한 기존의 지급 인프라가, 자체 보험에 가입한 고용주나 관련 계약에서 적용되는 가치 기반 상환 체계와 구조적으로 조화를 이루지 못하고 있다고 지적했습니다. NASCO는 또한 소속, 참여, 청구 및 보고 데이터가 단일한 신뢰할 수 있는 정보 출처 없이 여러 시스템에 분산되어 있는 파편화된 지급자 환경에 대해서도 언급했습니다. 이로 인해 계약의 측정 및 결제에 관한 관리상의 부담이 증가하고 있습니다. 이러한 상황에서 사내 팀이 조율에 어려움을 겪는 성과 측정, 보험 수리 업무, 계약 단위 보고를 일원화할 수 있기 때문에 외부 분석 및 KPO 파트너는 단순한 선택적 부가 기능이라기보다는 업무상 필수 불가결한 존재가 되었습니다. 이것이 바로 미국의 의료보험자용 서비스 시장이 공급업체와의 관계를 보다 장기적이고 심도 있게 발전시키는 방향으로 전환되고 있는 이유 중 하나입니다. 보험사는 일회성 프로젝트 기간에 그치지 않고, 정기적인 보고 주기 전반에 걸쳐 지속적으로 긴밀하게 관여해 줄 외부 파트너를 점점 더 필요로 하고 있기 때문입니다. 이와 같은 추세는 부가가치가 더 높은 아웃소싱을 촉진하고 있습니다. 왜냐하면 보험 플랜은 단순히 저렴한 처리 능력뿐만 아니라, 분석적 판단력, 보고의 지속성, 그리고 데이터 처리의 체계성을 구매하는 것이기 때문입니다.

사이버 보안과 정보 유출 위험: 제3자 공급업체의 집중이 초래하는 체계적 위험

사이버 보안은 미국의 의료보험자용 서비스 시장에 있어 진정한 걸림돌이 되고 있습니다. 아웃소싱 규모가 확대됨에 따라, 운영상의 리스크가 소수의 주요 공급업체에 집중될 가능성이 있기 때문입니다. 특정 서비스 제공업체가 다수의 보험사 고객의 청구 처리, 가입자 데이터 또는 관리 인터페이스에 걸쳐 관여하고 있는 경우, 단일 장애가 동시에 여러 계약에 영향을 미치게 되어 보험사가 벤더 집중 위험을 재평가해야 할 상황에 처하게 됩니다. 이 위험은 현재 조달 설계에 영향을 미치고 있습니다. 보험사 측은 더 강력한 감사 권한, 더 명확한 설명 책임에 관한 조항, 그리고 외부 파트너가 복잡한 운영 환경에서 PHI를 보호할 수 있다는 확실한 증거를 요구하고 있기 때문입니다. 그 결과, 구매자와 공급업체 양측의 보안 관련 지출이 증가하고 있으며, 성숙한 관리 환경을 갖춘 공급자에 대한 수요가 높아지는 한편, 계약 결정이 지연될 가능성도 있습니다. 그 결과, 유력한 공급업체 후보의 범위가 좁아지고 있습니다. 왜냐하면 모든 아웃소싱 제공업체가 보험사 수준의 운영에 필요한 보안 아키텍처, 모니터링, 테스트, 거버넌스 비용을 감당할 수 있는 것은 아니기 때문입니다. 이로 인해 미국의 의료보험자용 서비스 시장은 성장을 이어가고 있지만, 한편으로는 공급업체에 대한 자격 심사가 일반적인 비용 주도형 아웃소싱 주기에 비해 더 오랜 시간이 걸리고 더 엄격해지고 있습니다.

부문별 분석

2025년, 정보기술 아웃소싱(ITO) 서비스는 미국 의료보험자용 서비스 시장 점유율의 31.48%를 차지하며, 여전히 압도적인 차이로 최대 서비스 부문으로서의 위상을 유지했습니다. 이러한 추세는 클라우드 전환, 플랫폼 현대화, 사이버 보안 대책, API 활용 및 통합 작업과 같이 사내 팀만으로는 종종 필요한 속도로 완료하기 어려운 업무에 대한 외부 지원에, 보험사의 운영 안정성이 얼마나 의존하고 있는지를 반영하고 있습니다. 미국의 의료보험자용 서비스 업계에서 ITO는 청구 워크플로우 재설계, 가입자용 서비스 도구, 보고서 아키텍처, 사전 승인 시스템 등 다른 많은 아웃소싱 기능의 기반이 되기 때문에 전략적인 역할도 수행하고 있습니다. 보험 지급 기관은 컴플라이언스 프로그램을 정책 해석 단계에서 운영 시스템으로 전환할 수 있도록 지원하는 기술적 파트너가 필요하기 때문에 이 서비스 분야는 계속해서 규제 이행과 밀접하게 연결되어 있습니다. 향후 몇 년 동안 인접 분야의 성장이 가속화되더라도, 보험 지급 기관의 변혁 프로그램 대부분은 단순한 인건비 계약이 아닌 시스템, 인터페이스, 보안, 워크플로우와 같은 인프라에서 시작되기 때문에 ITO는 계속해서 수익의 기반이 될 것입니다.

지식 프로세스 아웃소싱(KPO) 서비스는 2026년부터 2031년까지 연평균 성장률(CAGR) 9.36%로 확대될 것으로 예상되며, 미국 의료보험자용 서비스 시장에서 가장 빠르게 성장하는 서비스 유형이 될 전망입니다. 이러한 성장은 보험사 측의 보험수리 지원, 위험 조정 업무, 예측, 계약 평가 및 가치 기반 의료(VBC) 보고에 대한 수요와 관련이 있습니다. 이러한 작업들은 일반적인 BPO 모델이 통상적으로 제공하는 것 이상의 전문적인 분석 기술과, 보다 고도의 데이터 처리 능력을 필요로 합니다. NASCO가 지적한 바와 같이, 의료 보험 플랜은 여전히 파편화된 데이터 환경에서 운영되고 있기 때문에 KPO 공급업체가 단순한 백오피스 분석 지원에 그치지 않고 지불자의 의사결정 주기에 밀접하게 관여하고 있는 이유를 설명할 수 있습니다. 청구 관리 서비스는 여전히 대량의 워크플로우 이전을 지원하는 데 핵심적인 역할을 하고 있지만, 지불자가 청구 라이프사이클의 더 초기 단계에서 개입하기를 요구함에 따라 지불의 적정성과 부정 관련 업무에 대한 관심이 높아지고 있습니다. 비즈니스 프로세스 아웃소싱(BPO) 서비스와 분석 서비스 역시, 처리 시간 단축, 재작업 감소, 사무 처리 정확성과 관련된 측정 가능한 기대치가 계약에 포함되게 됨에 따라 그 혜택을 누리고 있습니다. 즉, 미국의 의료보험자용 서비스 시장에서는 업무 수행과 심층 분석을 결합할 수 있는 공급업체가 점차 높이 평가받고 있으며, 이러한 기능을 서로 다른 공급업체의 사일로에 가두어 두는 방식은 더 이상 통용되지 않고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the united states healthcare payer services market size is projected to expand from USD 34.57 billion in 2025 and USD 37.32 billion in 2026 to USD 56.79 billion by 2031, registering a CAGR of 8.76% between 2026 to 2031.

This report is Segmented by Service Type (Claims Management, Billing and Payment, Fraud Detection and Payment Integrity, Analytics, KPO, ITO, BPO), Application (Health Insurance, Life Insurance, Managed Care, Public Programs), End Use (Private Payers, Public Payers, Employer-Sponsored Plans), and Geography (United States). The Market Forecasts are Provided in Terms of Value (USD).

United States Healthcare Payer Services Market Trends and Insights

Accelerating Claims Automation Demand: Manual Adjudication Costs Reach Systemic Levels

The United States healthcare payer services market is benefiting from the fact that administrative work is still too expensive to leave inside fragmented and partly manual payer systems. CAQH reported that electronic transaction processing helped the U.S. healthcare system avoid USD 258 billion in administrative costs in 2024, while another USD 21 billion in annual savings remains available through deeper automation of manual and partially manual workflows. That gap matters because denied, pended, and exception-heavy claims still create repeat touches, longer cycle times, and avoidable labor costs that payers increasingly prefer to shift to specialist operating partners. Once those rework loops are moved outside the health plan, vendors can spread workflow investments across many clients, which makes automation economics easier to justify than they are inside a single payer. Aetna stated in May 2026 that its Claims Automation Model reduced processing time for complex claims by more than 20%, which gives the market a visible example of how production AI can lower turnaround time in a live payer setting. As more plans look for the same result, the United States healthcare payer services market is seeing stronger demand for vendors that can combine claims operations, workflow rules, exception handling, and AI-based resolution inside one delivery model.

Value-Based Care Contracting Complexity: Outsourced Analytics Becoming Non-Negotiable

The United States healthcare payer services market is also being pulled forward by value-based care because those contracts are much harder to reconcile than fee-for-service arrangements. AJMC noted that traditional payment infrastructure, including claims adjudication and billing systems, remains structurally misaligned with value-based reimbursement mechanics for self-insured employers and related arrangements. NASCO also pointed to fragmented payer environments where attribution, engagement, claims, and reporting data sit across multiple systems without a single source of truth, which raises the administrative burden around contract measurement and settlement. In that setting, external analytics and KPO partners become less of an optional add-on and more of an operating necessity because they can centralize performance measurement, actuarial work, and contract-level reporting that internal teams struggle to coordinate. This is one reason the United States healthcare payer services market is shifting toward longer and deeper vendor relationships, since payers increasingly need outside partners that stay embedded across recurring reporting cycles and not just isolated project windows. The same dynamic also supports higher-value outsourcing because plans are buying analytical judgment, reporting continuity, and data handling discipline, not just low-cost processing capacity.

Cybersecurity and Breach Exposure: Third-Party Vendor Concentration Creates Systemic Risk

Cybersecurity is a real brake on the United States healthcare payer services market because the scale of outsourcing can also concentrate operational exposure within a smaller number of critical vendors. When one service provider sits across claims, member data, or administrative interfaces for many payer clients, a single failure can affect multiple contracts at the same time and force payers to reassess vendor concentration risk. That risk is now influencing procurement design, since plans want stronger audit rights, clearer accountability language, and better evidence that outside partners can protect PHI in complex production settings. Security spending therefore rises for both buyers and vendors, which can slow contract decisions even while it raises demand for providers with mature control environments. The result is a narrower effective vendor pool, because not every outsourcing provider can absorb the cost of security architecture, monitoring, testing, and governance required for payer-grade operations. This keeps the United States healthcare payer services market growing, but it also makes vendor qualification slower and more demanding than a standard cost-led outsourcing cycle.

Other drivers and restraints analyzed in the detailed report include:

- Interoperability-Driven Administrative Workload: Compliance Spending Converted to Services Revenue

- AI-Based Payment Integrity Expansion: Shift From Recovery to Prevention Reorders the Market

- Legacy Core System Integration Friction: A Drag Measured in Decades, Not Quarters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Information Technology Outsourcing Services held 31.48% of the United States healthcare payer services market share in 2025, which kept it as the largest service category by a clear margin. That lead reflects how much payer operating stability now depends on outside support for cloud migration, platform modernization, cybersecurity controls, API enablement, and integration work that internal teams often cannot complete at the required pace. In the United States healthcare payer services industry, ITO also carries a strategic role because it sits underneath many other outsourced functions, including claims workflow redesign, member servicing tools, reporting architecture, and prior authorization systems. The service line remains closely tied to regulatory execution, since payers need technical delivery partners that can move compliance programs from policy interpretation into operational systems. Even if adjacent categories grow faster over the next few years, ITO should continue to anchor revenue because most payer transformation programs still begin with systems, interfaces, security, and workflow infrastructure rather than with stand-alone labor contracts.

Knowledge Process Outsourcing Services is projected to expand at a 9.36% CAGR from 2026 to 2031, making it the fastest-growing service type in the United States healthcare payer services market. Its growth is linked to payer demand for actuarial support, risk adjustment work, forecasting, contract measurement, and value-based care reporting that require specialized analytical skills and stronger data handling than general BPO models usually provide. NASCO's observation that health plans still operate across fragmented data environments helps explain why KPO vendors are moving closer to payer decision cycles and not just supporting back-office analysis. Claims Management Services remains central because it supports high-volume workflow transfer, while payment integrity and fraud-related work are gaining more attention as payers look for earlier intervention inside the claims life cycle. Business Process Outsourcing Services and Analytics Services are also benefiting from contracts that now include measurable expectations around turnaround time, rework reduction, and administrative accuracy. That means the United States healthcare payer services market is gradually rewarding providers that can connect operational delivery with analytical depth, rather than keeping those functions in separate vendor silos.

Complete Report Scope:

- By Service Type

- Claims Management Services

- Billing and Payment Services

- Fraud Detection and Payment Integrity Services

- Analytics Services

- Knowledge Process Outsourcing Services

- Information Technology Outsourcing Services

- Business Process Outsourcing Services

- By Application

- Health Insurance

- Life Insurance

- Managed Care

- Public Programs

- By End Use

- Private Payers

- Public Payers

- Employer-Sponsored Plans

List of Companies Covered in this Report:

- Accenture

- Blue Cross Blue Shield Association

- Centene Corporation

- Cigna Corporation

- Cognizant

- Conduent Incorporated

- CVS Health

- Elevance Health

- EXL Service Holdings, Inc.

- Genpact

- HCL Technologies Limited

- Humana Inc.

- IBM

- Kaiser Permanente

- Molina Healthcare, Inc.

- Optum

- Sutherland Global Services, Inc.

- United Health Group

- Wipro

- Xerox Holdings Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Claims Automation Demand

- 4.2.2 Value-Based Care Contracting Complexity

- 4.2.3 Interoperability-Driven Administrative Workload

- 4.2.4 AI-Based Payment Integrity Expansion

- 4.2.5 Payer Margin Compression From Low-Mix Administrative Leakage

- 4.2.6 Rapid Rise in Prior Authorization Exception Volumes

- 4.3 Market Restraints

- 4.3.1 HIPAA and CMS Compliance Burden

- 4.3.2 Cybersecurity and Breach Exposure

- 4.3.3 Legacy Core System Integration Friction

- 4.3.4 Contract Governance and Transition Leakage in Outsourced Operations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Claims Management Services

- 5.1.2 Billing and Payment Services

- 5.1.3 Fraud Detection and Payment Integrity Services

- 5.1.4 Analytics Services

- 5.1.5 Knowledge Process Outsourcing Services

- 5.1.6 Information Technology Outsourcing Services

- 5.1.7 Business Process Outsourcing Services

- 5.2 By Application

- 5.2.1 Health Insurance

- 5.2.2 Life Insurance

- 5.2.3 Managed Care

- 5.2.4 Public Programs

- 5.3 By End Use

- 5.3.1 Private Payers

- 5.3.2 Public Payers

- 5.3.3 Employer-Sponsored Plans

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Accenture plc

- 6.3.2 Blue Cross Blue Shield Association

- 6.3.3 Centene Corporation

- 6.3.4 Cigna Corporation

- 6.3.5 Cognizant Technology Solutions Corporation

- 6.3.6 Conduent Incorporated

- 6.3.7 CVS Health

- 6.3.8 Elevance Health

- 6.3.9 EXL Service Holdings, Inc.

- 6.3.10 Genpact Limited

- 6.3.11 HCL Technologies Limited

- 6.3.12 Humana Inc.

- 6.3.13 IBM Corporation

- 6.3.14 Kaiser Permanente

- 6.3.15 Molina Healthcare, Inc.

- 6.3.16 Optum, Inc.

- 6.3.17 Sutherland Global Services, Inc.

- 6.3.18 UnitedHealth Group

- 6.3.19 Wipro Limited

- 6.3.20 Xerox Holdings Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment