|

시장보고서

상품코드

2072858

혈뇨 치료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Hematuria Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

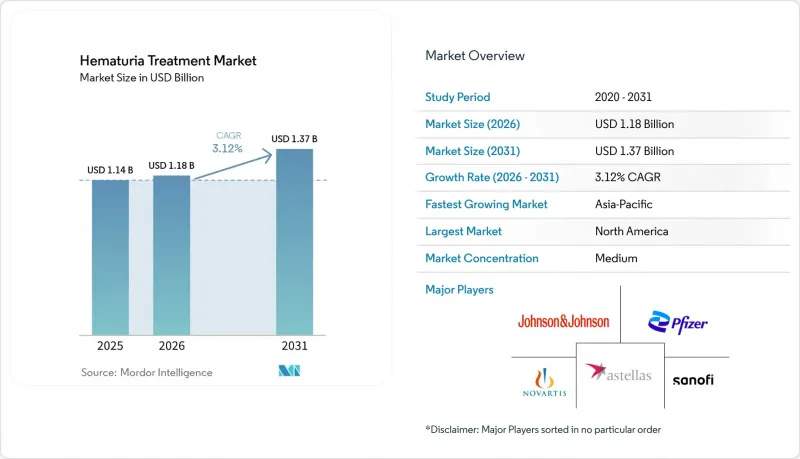

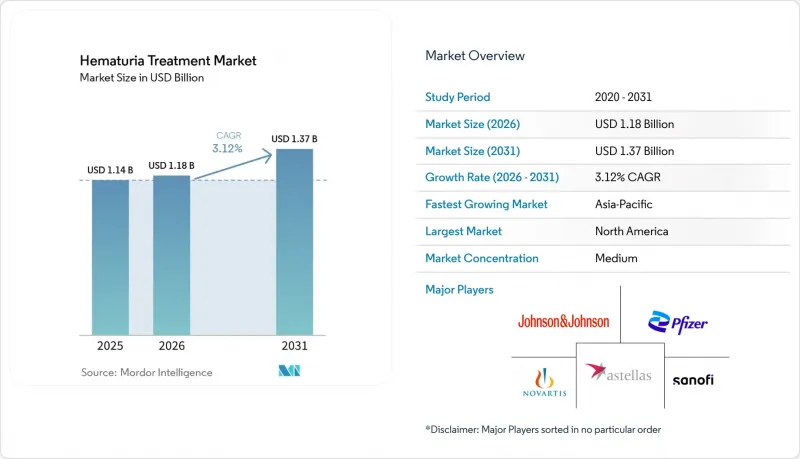

Mordor Intelligence에 의하면, 혈뇨 치료 시장 규모는 2025년 11억 4,000만 달러, 2026년 11억 8,000만 달러에서 2031년까지 13억 7,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 3.12%를 나타낼 전망입니다.

본 보고서는 혈뇨의 유형(육안적, 현미경적), 치료의 유형(약물요법, 시술·중재요법, 보조·지지요법), 원인(요로감염, 요로결석증, 방광암, 전립선비대증, 사구체 질환, 의인성), 최종 사용자(병원, 비뇨기과 클리닉, 외래수술센터(ASC), 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카(MEA), 남미)별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계 혈뇨 치료 시장 동향 및 인사이트

비뇨기 질환 및 혈뇨와 관련된 질환의 부담 증가

혈뇨 치료 시장은 소변에 혈액이 섞이는 상태와 관련된 질환의 높은 유병률에 힘입어 성장하고 있습니다. 2025년, 방광암의 연령 조정 발병률은 10만 명당 6.35였습니다. 조사 대상이 된 6가지 주요 비뇨기 질환 중, 1990년부터 2025년까지 발병률과 사망률이 모두 증가한 것은 요로 감염증뿐이었습니다. 2025년에는 전 세계적으로 1억 598만 명이 요로결석증을 앓고 있으며, 이 질환으로 인한 부담은 50세에서 65세 연령대에 집중되어 있는데, 이는 혈뇨 검사를 받는 환자층과 일치합니다. 2025년에는 흡연이 전 세계 방광암 사망의 26.48%, 방광암으로 인한 DALY의 28.15%를 차지하는 원인이 될 것으로 보이며, 향후 혈뇨 치료 수요는 동남아시아나 사하라 이남 아프리카 등 흡연율이 높은 지역과 밀접한 관련이 있습니다. 또한, 2025년에는 높은 BMI가 신장암으로 인한 사망의 20.07%를 차지하는 것으로 나타나, 혈뇨 관련 시장에서 검사와 치료의 필요성이 더욱 강조되고 있습니다.

일상 진료에서 위험도에 따라 분류된 혈뇨 진료 프로토콜의 보급

혈뇨 치료 시장은 위험 기반 평가의 도입에 따라 발전하고 있습니다. AUA/SUFU 2025년 미량 혈뇨 지침 개정판에서는 평가를 '무시할 수 있는 위험', '저위험', '중간 위험', '고위험' 4개의 그룹으로 분류했습니다. 이러한 접근 방식을 통해 저위험 환자에 대한 불필요한 방광경 검사가 줄어드는 동시에, 악성 종양 위험이 높은 환자에 대한 대응에 중점을 두게 되었습니다. 이 개정된 지침에서는 무시할 수 있는 위험군 환자에 대해 6개월 후 소변 검사를 다시 실시할 것을 권장하고 있으며, 이를 통해 외래 진료 기회가 확대되고, 즉시 침습적 검사로 넘어가는 것에 대한 의존도가 낮아지고 있습니다. 이러한 변화는 체계적인 선별 진료와 후속 검사를 중시하는 것으로, 시장 역학을 재편하고 있습니다.

지침에 따른 저위험 환자에 대한 불필요한 검사 축소

혈뇨 치료 시장의 주요 제약 요인 중 하나는 저위험 환자에 대한 침습적 검사의 전략적 축소입니다. AUA 2025년 개정판에서는 무시할 수 있는 위험군 환자에 대해 즉시 시행되는 방광경 검사 대신 6개월 이내에 소변 검사를 재실시할 것을 권장하고 있으며, 이로 인해 해당 그룹의 단기적인 검사 수요가 직접적으로 감소하게 될 것입니다. 또한, 이 지침에서는 저위험군에서 암 검출률이 추적 관찰 기간의 중앙값인 26개월 동안 0%에서 0.4% 범위에 머무른다는 점이 강조되고 있어, 초진 시 광범위한 침습적 검사를 실시하는 것의 타당성이 약화되고 있습니다. 이로 인해 수요가 완전히 사라지는 것은 아니지만, 지출이 경과 관찰, 소변 검사 재검사 및 선택적 검사 단계로의 전환으로 이동함에 따라, 저위험 집단의 시술 관련 수익 증가세는 둔화되는 반면, 고위험 집단을 대상으로 한 진료 경로는 계속해서 활발하게 기능하게 될 것입니다.

부문별 분석

2025년, 육안으로 확인되는 혈뇨는 시장 점유율의 56.6%를 차지하고 있으며, 응급실 및 비뇨기과 현장에서 즉각적인 의뢰나 평가를 유도하는 경향이 강하다는 사실이 부각되고 있습니다. 육안으로 확인되는 혈뇨가 있는 환자는 종종 방광경 검사나 상부 요로 영상 검사를 받게 되므로, 이에 대한 관심이 높아집니다. 그러나 시장에서는 육안으로 확인되는 혈뇨보다 현미경적 혈뇨가 장기적인 성장 가능성이 더 높으며, 2031년까지 연평균 성장률(CAGR) 3.66%로 확대될 것으로 예측되고 있습니다. 2024년 유병률 조사에서 조사 대상인 성인 코호트의 34.1%가 무증상 현미경적 혈뇨를 보였으며, 이 결과는 2년에 걸친 매니지드 케어 데이터에서도 뒷받침되고 있습니다.

이는 육안으로 확인되는 혈뇨와 비교했을 때, 현미경적 혈뇨 환자군이 치료 시장에 대해 정기적인 추적 관찰을 수행할 수 있는 보다 광범위한 기반을 제공한다는 점에서 중요합니다. 2025년 AUA 지침에서는 접근 방식이 변경되어, 저위험 미세 혈뇨의 경우 즉시 침습적 검사를 실시하기보다는 6개월 후 소변 검사를 다시 실시하는 것이 권장되게 되었습니다. 이러한 변경으로 인해 환자가 모니터링 대상 치료 경로에 머무르는 기간이 연장될 가능성이 있습니다. 일관된 소변 침전물 검사와 평가가 중요시된다는 점을 고려할 때, 검사실에서의 표준화된 처리 절차야말로 매우 중요합니다. 따라서 현미경적 혈뇨는 처음에는 긴급성이 낮아 보일 수 있지만, 환자가 모니터링, 재분류 및 치료 단계적 강화를 위해 자주 내원하기 때문에 의료 업계에 있어 보다 지속 가능한 중점 분야임이 입증되었습니다.

2025년에는 요로 감염증에 대한 항생제, 증상 완화제, 그리고 방광암 관련 혈뇨에 대한 방광 내 치료가 주도하면서 약물 요법이 36.75%의 점유율을 차지하며 시장을 독점했습니다. 이러한 선두에도 불구하고, 수기 요법 및 중재 요법은 더 빠른 성장세를 보이고 있으며, 2031년까지 연평균 성장률(CAGR)은 3.95%로 예측됩니다. FDA는 2025년, UroGen Pharma사의 방광 내 투여용 마이토마이신 제제 "Zusduri"를, 재발성 저악성도·중위험군의 비근층침윤성 방광암에 대해 승인했습니다. 이번 승인은 ENVISION 임상시험 결과를 바탕으로 한 것으로, 해당 임상시험에서는 3개월 시점의 완전 반응률이 78%였으며, 환자의 79%가 1년 이상 그 상태를 유지한 것으로 보고되었습니다.

2025년 하반기에는 FDA가 얀센 바이오텍사의 방광 내 투여용 젬시타빈 제제 "Inlexzo"를 BCG 요법에 반응하지 않는 상피내암을 동반한 비근층침윤성 방광암에 대해 승인했습니다. SunRISe-1 임상시험에서는 82%의 완전 반응률이 확인되었으며, 이는 당시 이 범주에서 승인된 치료법 중 가장 높은 수치였습니다. 이러한 승인으로 인해 치료 선택의 폭이 넓어졌으며, 항생제나 기본적인 치료 이상의 치료가 필요한 환자들에게 가격 협상 여지가 확대되었습니다. 방광 세척이나 항응고제 관리와 같은 지지 요법은 표준 감염 치료와 고도의 암 치료 사이의 격차를 메우는 데 있어 매우 중요한 역할을 하고 있습니다.

지역별 분석

2025년, 북미는 혈뇨 치료 시장에서 41.25%의 점유율을 차지하며 시장을 주도했습니다. 이는 비뇨기계 암에 대한 높은 인지도, 전문의에 대한 접근성이 양호한 점, 그리고 새로운 치료법의 급속한 보급이 요인으로 작용하고 있습니다. 미국에서는 방광암에 따른 혈뇨 관리에 필수적인 방광 내 요법에 대해 FDA로부터 2건의 승인을 획득함에 따라, 이 분야가 계속해서 주요 수익원으로 자리매김했습니다. 또한, 40세 이상의 전립선 비대증 환자 중 8%에서 11%가 혈뇨로 고통받고 있어, 종양학 이외의 치료에 대한 안정적인 수요가 확보되어 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 4.88%를 나타낼 것으로 예측되며, 혈뇨 치료 시장에서 가장 빠르게 성장하고 있는 지역입니다. 일본에서는 국민건강검진에서 인구의 5%에서 10%가 소변 검사 결과 혈뇨 양성으로 판정되고 있으며, 안정적인 진단 체계가 구축되어 있어 이 지역은 중요한 역할을 수행하고 있습니다. 2025년, 펠링사는 BCG 요법에 반응하지 않는 비근층 침윤성 방광암을 대상으로 한 3상 임상시험에서 ADSTILADRIN의 완전 반응률이 75%였습니다고 보고하며, 치료 전망을 밝게 했습니다. 중국도 크게 기여하고 있으며, 3상 임상시험 데이터에 따르면 Hexvix를 이용한 청색광 방광경 검사는 백색광 방광경 검사에 비해 방광암 검출률을 높이는 것으로 나타났습니다.

유럽은 주요 국가들의 보험 환급 제도가 일상 진료에서 시행되는 방광경 검사, 병리 검사 및 방광 내 치료를 지원하고 있기 때문에 여전히 주요 시장으로 남아 있습니다. 이 지역은 잘 구축된 병원 및 검사 기관 네트워크의 혜택을 받고 있어, 진단에서 치료로의 원활한 전환이 보장되고 있습니다. 성장 속도는 아시아태평양보다 완만하지만, 표준화된 임상 경로와 높은 전문의 평가율이 유럽 시장의 매력을 유지하고 있습니다. 중동 및 아프리카와 남미는 시장 규모는 작지만, 비뇨기과 인프라가 잘 갖춰져 있고, 그동안 진단에서 누락되었던 환자들이 정식 치료를 받게 됨에 따라 성장 잠재력을 지니고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the hematuria treatment market size is projected to expand from USD 1.14 billion in 2025 and USD 1.18 billion in 2026 to USD 1.37 billion by 2031, registering a CAGR of 3.12% between 2026 to 2031.

This report is Segmented by Hematuria Type (Gross, Microscopic), Treatment Type (Pharmacotherapy, Procedural and Interventional, Adjunctive and Supportive), Cause (UTI, Urolithiasis, Bladder Cancer, BPH, Glomerular Disorders, Iatrogenic), End User (Hospitals, Urology Clinics, Ascs, Others), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global Hematuria Treatment Market Trends and Insights

Rising Burden of Urological Disorders and Hematuria-Linked Conditions

The hematuria treatment market is driven by the high prevalence of conditions associated with blood in urine. In 2025, bladder cancer had an age-standardized incidence rate of 6.35 per 100,000 persons. Urinary tract infections were the only major urological disease among six studied to show both rising incidence and mortality from 1990 to 2025. Urolithiasis affected 105.98 million people globally in 2025, with the disease burden concentrated in the 50 to 65 age group, aligning with those undergoing hematuria evaluations. Smoking caused 26.48% of global bladder cancer deaths and 28.15% of bladder cancer DALYs in 2025, linking future demand for hematuria treatments to tobacco-heavy regions like Southeast Asia and Sub-Saharan Africa. Additionally, high BMI contributed to 20.07% of kidney cancer deaths in 2025, reinforcing the need for evaluations and treatments in the hematuria market.

Wider Use of Risk-Stratified Hematuria Pathways in Routine Care

The hematuria treatment market is evolving with the adoption of risk-based evaluations. The AUA/SUFU 2025 Microhematuria Guideline Amendment categorized evaluations into negligible, low, intermediate, and high-risk groups. This approach reduced unnecessary cystoscopies for lower-risk patients while focusing on those with higher malignancy risks. The updated framework supports repeat urinalysis at six months for negligible-risk patients, extending outpatient contact points and reducing reliance on immediate procedural escalation. This shift emphasizes structured triage and follow-up testing, reshaping the market dynamics.

Guideline-Driven Reduction in Unnecessary Testing for Low-Risk Patients

A key restraint in the hematuria treatment market is the strategic reduction of invasive testing for low-risk patients. The AUA 2025 amendment recommends repeat urinalysis within 6 months instead of immediate cystoscopy for negligible-risk patients, directly reducing near-term procedure demand in this group. The guideline also highlights that cancer detection rates in low-risk groups range from 0% to 0.4% over a median follow-up of 26 months, weakening the justification for broad invasive workups at initial presentation. While this does not eliminate demand, it shifts spending toward observation, repeat urinalysis, and selective escalation, slowing procedural revenue growth in lower-risk populations while higher-risk pathways remain active.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Urine-Based Biomarker Use in Intermediate-Risk Hematuria Patients

- Growth of Outpatient, Lower-Acuity Evaluation Pathways

- High Dependence on Cystoscopy and Imaging Infrastructure for Definitive Workup

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, gross hematuria accounted for a 56.6% market share, highlighting its tendency to prompt immediate referrals and evaluations in emergency and urology settings. Patients with gross hematuria often undergo cystoscopy and upper-tract imaging, leading to a more intense procedural focus. However, the market sees greater long-term growth potential in microscopic hematuria, projected to expand at a 3.66% CAGR through 2031. A 2024 prevalence study highlighted that 34.1% of a surveyed adult cohort exhibited asymptomatic microscopic hematuria, a finding echoed by managed care data over a two-year span.

This is significant as the microscopic hematuria demographic offers the treatment market a broader base for recurring follow-ups compared to its gross counterpart. The 2025 AUA guideline shifted its approach, suggesting a 6-month repeat urinalysis for low-risk microhematuria, rather than an immediate invasive evaluation. This change potentially extends the duration patients remain within monitored care pathways. Given the emphasis on consistent urine microscopy and evaluations, standardized laboratory handling becomes paramount. Thus, while microscopic hematuria may seem less urgent initially, it proves to be a more sustainable focus for the treatment industry, as patients frequently return for monitoring, reclassification, and potential escalation of care.

In 2025, pharmacotherapy dominated the market with a 36.75% share, driven by antibiotics for urinary tract infections, agents for symptom relief, and intravesical therapies for bladder-cancer-related hematuria. Despite this lead, procedural and interventional therapies are growing faster, with a projected 3.95% CAGR through 2031. The FDA approved Zusduri, an intravesical mitomycin solution from UroGen Pharma, in 2025 for recurrent low-grade, intermediate-risk, non-muscle invasive bladder cancer. This approval was supported by the ENVISION trial, which reported a 78% complete response rate at 3 months, with 79% maintaining their status for a year or more.

Later in 2025, the FDA approved Inlexzo, a gemcitabine intravesical system from Janssen Biotech, for BCG-unresponsive, non-muscle invasive bladder cancer with carcinoma in situ. The SunRISe-1 trial highlighted an 82% complete response rate, marking it as the highest for any approved therapy in this category at the time. These approvals broaden treatment options and enhance pricing leverage for patients needing more than just antibiotics or basic care. Supportive therapies like bladder irrigation and anticoagulant management play a crucial role, bridging the gap between standard infection treatments and premium cancer interventions.

Complete Report Scope:

- By Hematuria Type

- Gross Hematuria

- Microscopic Hematuria

- By Treatment Type

- Pharmacotherapy

- Procedural and Interventional Therapies

- Adjunctive and Supportive Therapies

- By Cause

- Urinary Tract Infection

- Urolithiasis

- Bladder Cancer and Upper Tract Urothelial Cancer

- Benign Prostatic Hyperplasia

- Glomerular and Renal Disorders

- Iatrogenic and Anticoagulant-Associated Hematuria

- By End User

- Hospitals

- Specialty Urology Clinics

- Ambulatory Surgical Centers

- Diagnostic Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America led the hematuria treatment market with a 41.25% share, driven by high awareness of urological cancers, better access to specialists, and rapid adoption of new therapies. The United States remained the primary revenue contributor, supported by two FDA approvals for intravesical therapies critical to managing bladder cancer-associated hematuria. Additionally, hematuria affected 8% to 11% of men over 40 with benign prostatic hyperplasia, ensuring steady demand for treatments beyond oncology.

Asia-Pacific is the fastest-growing region in the hematuria treatment market, with a projected 4.88% CAGR through 2031. Japan plays a key role, as national health checks identify 5% to 10% of the population as urine dipstick positive for hematuria, creating a consistent diagnostic funnel. In 2025, Ferring reported a 75% complete response rate for ADSTILADRIN in Phase 3 trials for BCG-unresponsive non-muscle invasive bladder cancer, enhancing the treatment outlook. China also contributes significantly, with Phase 3 data showing blue light cystoscopy with Hexvix improves bladder cancer detection compared to white light cystoscopy.

Europe remains a major market due to reimbursement systems in large countries that support cystoscopy, pathology, and intravesical therapies in routine care. The region benefits from established hospital and laboratory networks, ensuring smooth transitions from detection to treatment. Although growth is slower than in Asia-Pacific, standardized clinical pathways and high specialist evaluation rates maintain Europe's market appeal. The Middle East, Africa, and South America, while smaller in market value, offer growth potential as urology infrastructure improves and more patients transition from underdiagnosis to formal treatment.

- Abbott Laboratories

- Amneal Pharmaceuticals

- Astellas Pharma

- Boston Scientific

- Bristol-Myers Squibb

- Cipla

- Cook Group

- Dr. Reddy's Laboratories

- Roche

- Ferring Pharmaceuticals

- GlaxoSmithKline

- Johnson & Johnson

- Karl Storz SE and Co. KG

- Merck

- Novartis

- Olympus

- Pacific Edge

- Pfizer

- Photocure ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Urological Disorders and Hematuria-Linked Complications

- 4.2.2 Wider Use of Risk-Stratified Hematuria Pathways in Routine Urology Practice

- 4.2.3 Expansion of Urine-Based Biomarker Use in Intermediate-Risk Evaluation

- 4.2.4 Growth of Outpatient, Lower-Acuity Evaluation Pathways for Stable Patients

- 4.2.5 Delayed Referral and Under-Evaluation of Women and Older Adults in Primary Care

- 4.2.6 Rising Need for Cause-Specific Management Beyond Empiric Symptom Treatment

- 4.3 Market Restraints

- 4.3.1 Guideline-Driven Reduction in Unnecessary Testing for Low-Risk Patients

- 4.3.2 Limited Clinical Acceptance of Urinary Biomarkers in Initial Workups

- 4.3.3 High Dependence on Cystoscopy and Imaging Infrastructure

- 4.3.4 Treatment Heterogeneity Linked to the Underlying Cause of Hematuria

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Hematuria Type

- 5.1.1 Gross Hematuria

- 5.1.2 Microscopic Hematuria

- 5.2 By Treatment Type

- 5.2.1 Pharmacotherapy

- 5.2.2 Procedural and Interventional Therapies

- 5.2.3 Adjunctive and Supportive Therapies

- 5.3 By Cause

- 5.3.1 Urinary Tract Infection

- 5.3.2 Urolithiasis

- 5.3.3 Bladder Cancer and Upper Tract Urothelial Cancer

- 5.3.4 Benign Prostatic Hyperplasia

- 5.3.5 Glomerular and Renal Disorders

- 5.3.6 Iatrogenic and Anticoagulant-Associated Hematuria

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty Urology Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Diagnostic Laboratories

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Amneal Pharmaceuticals LLC

- 6.3.3 Astellas Pharma Inc.

- 6.3.4 Boston Scientific Corporation

- 6.3.5 Bristol-Myers Squibb Company

- 6.3.6 Cipla Limited

- 6.3.7 Cook Medical LLC

- 6.3.8 Dr. Reddy's Laboratories Limited

- 6.3.9 F. Hoffmann-La Roche Ltd

- 6.3.10 Ferring Pharmaceuticals Inc.

- 6.3.11 GSK plc

- 6.3.12 Johnson and Johnson

- 6.3.13 Karl Storz SE and Co. KG

- 6.3.14 Merck and Co., Inc.

- 6.3.15 Novartis AG

- 6.3.16 Olympus Corporation

- 6.3.17 Pacific Edge Limited

- 6.3.18 Pfizer Inc.

- 6.3.19 Photocure ASA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment