|

시장보고서

상품코드

2072929

미국의 봉합 와이어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Suture Wire - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

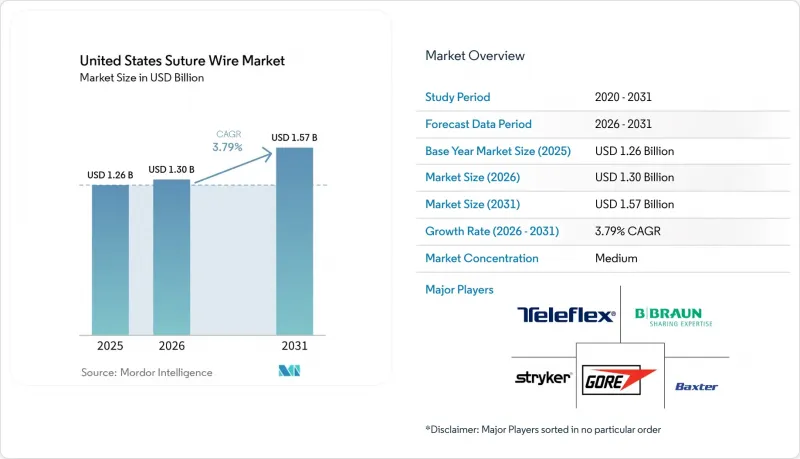

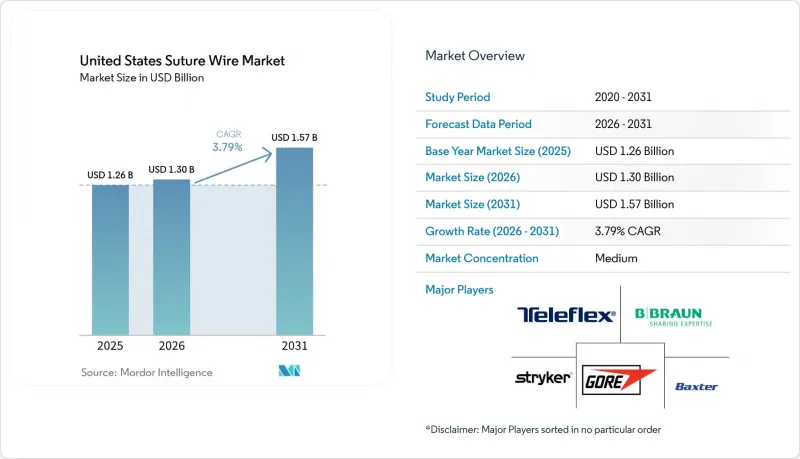

Mordor Intelligence에 의하면, 미국 봉합 와이어 시장 규모는 2025년 12억 6,000만 달러, 2026년 13억 달러에서 2031년까지 15억 7,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 3.79%를 나타낼 전망입니다.

본 보고서는 유형(스테인리스 봉합 와이어, 기타 유형), 재질(스테인리스 스틸, 기타 금속 및 합금), 최종 사용자(병원, ASC, 전문 클리닉), 용도(심혈관 외과, 정형외과, 일반외과, 안과 수술, 기타 외과 용도)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국 봉합 와이어 시장 동향 및 분석

미국 내 수술 건수 및 수술 빈도 증가

미국의 봉합 와이어 시장은 연간 5,200만 건이 넘는 전국적인 수술 건수에 힘입어, 공급업체들에게 모든 의료 현장에 걸친 광범위하고 지속적인 수요 기반을 제공합니다. 수술 건수만이 유일한 요인은 아닙니다. 증례 구성도 폐쇄의 확실성이 더욱 중요시되는 복잡한 수술로 전환되고 있으며, 금속 와이어는 임상 현장에서 여전히 친숙한 소재이기 때문입니다. 개흉 수술은 여전히 가장 확실한 소비처 중 하나이며, 연간 30만 건 이상의 수술이 시행되고 있으며, 일반 위험군 환자의 표준 흉골 절개 봉합에는 여전히 스테인리스 와이어가 사용되고 있습니다. 미국 흉부외과학회(Society of Thoracic Surgeons)의 데이터베이스는 1,000개 이상의 의료기관에서 수행된 누적 830만 건 이상의 수술과 미국 심장외과 프로그램의 97% 이상을 포괄하고 있어, 이러한 기반을 뒷받침하고 있습니다. 중증도가 높은 사례가 증가하는 것도 병원이 신뢰할 수 있는 와이어 공급에 계속 주력하는 요인이 되고 있습니다. 왜냐하면 폐쇄 부위의 불완전, 재입원, 재시술은 임상적 및 재정적으로 심각한 결과를 초래하기 때문입니다. 동시에, 미국의 봉합 와이어 시장에서는 고위험 환자군에서 강성 고정 시스템으로의 선택적 전환을 주의 깊게 지켜볼 필요가 있습니다. 이로 인해 향후 복잡한 심장 질환 사례 중 극히 일부에서 와이어 사용이 줄어들 가능성이 있습니다.

정형외과 및 심혈관외과에서 와이어를 많이 사용하는 수술 증가

미국의 봉합 와이어 시장은 여전히 정형외과 및 심혈관 외과 분야에 의해 지탱되고 있습니다. 이 두 전문 분야가 스테인리스 스틸 와이어 소비량의 대부분을 차지하고 있기 때문입니다. 심장 치료 분야에서는 정중 흉골 절개술 후 금속 와이어에 대한 의존도가 여전히 높으며, 병원 측이 가격 면에서 압박을 가하더라도 안정적인 수요 기반이 유지되고 있습니다. 정형외과 분야 수요도 폭넓어, 인공관절 주위 골절의 고정, 슬개골 복원, 인공관절 재치환술, 그리고 여전히 견고한 비흡수성 고정이 필요한 서클라주를 주된 내용으로 하는 재건 수술 등을 포괄하고 있습니다. 국내 인공관절 치환술 건수는 이미 연간 150만 건을 넘어섰으며, 고령화에 따라 재치환술 및 외상 사례 수가 증가함에 따라 고정 관련 수요는 높은 수준을 유지하고 있습니다. 세계 심혈관·흉부외과학회(World Society of Cardiovascular and Thoracic Surgeons)에서 발표된 2024년 분석에 따르면, 비교 대상 코호트에서 발생한 37건의 흉골 관련 재입원 사례는 모두 와이어 서클라주 군에서 발생했으며, 1회 입원당 평균 비용은 4만 2,326달러에 달했습니다. 이러한 상황으로 인해 의료 제공업체들은 환자의 위험도 분류를 더욱 엄격하게 선별해야 하는 상황에 놓여 있습니다. 이로 인해 봉합 와이어가 임상 현장에서 완전히 사라지는 것은 아니지만, 미국의 봉합 와이어 시장은 표준적인 강철 제품이 계속 사용되는 일상적인 증례와, 대체 고정 시스템의 도입이 정당화될 가능성이 있는 고위험 증례로 더욱 세분화되고 있음을 의미합니다.

스테이플러, 접착제 및 흡수성 고분자 봉합 와이어와의 경쟁

미국 봉합 와이어 시장이 가장 뚜렷한 대체 위험에 직면해 있는 분야는 심장외과 및 정형외과 이외의 분야이며, 이러한 분야에서는 이미 대체 폐쇄법이 임상적으로 널리 받아들여지고 있습니다. 스테이플러는 연조직 봉합 분야에서 지속적으로 개선되고 있으며, 존슨앤드존슨은 2025년 6월 미국에서 "ETHICON 4000 스테이플러"를 출시했으며, 2026년 4월에는 해당 플랫폼에 대한 CE 마크 인증을 획득했습니다. 조직용 접착제 및 고성능 흡수성 봉합 와이어 역시 표재 수술, 복강경 수술 및 최소 침습 수술에서 와이어 사용을 줄이고 있습니다. 흉골 절개 부위의 봉합과 관련하여, 2025년 『Journal of Clinical Medicine』지에 게재된 연구에 따르면, UHMWPE 봉합 테이프가 표준 강선보다 높은 생체역학적 하중 내성을 보이는 것으로 보고되었으며, 이는 특정 심장 수술에서 대체 방식의 신뢰성이 점차 높아지고 있음을 시사합니다. 강선은 사용에 익숙하고 비용 대비 효과가 높으며 표준 프로토콜에 깊이 정착되어 있음에도 불구하고, 일상 진료에서 채택되는 경우는 여전히 제한적입니다. 그렇긴 하지만, 이러한 사실은 확립된 수술법 분야에서 미국의 봉합 와이어 시장을 가장 견고하게 유지해 주는 한편, 강선이 기본 봉합 수단이 아닌 용도에서의 성장 가능성을 제한하고 있습니다.

부문별 분석

2025년, 스테인리스 봉합 와이어는 미국 봉합 와이어 시장 점유율의 61.42%를 차지하며, 동 카테고리 내의 특수한 형태의 제품들을 확실히 앞질렀습니다. 이러한 선도적인 위상은 흉골 봉합, 정형외과용 서클라주, 탈장 보강 및 복부 상처 봉합 분야에서 폭넓게 사용되고 있기 때문이며, 이러한 분야에서 외과의사들은 여전히 신뢰할 수 있는 인장 성능과 익숙한 취급 방식을 중요하게 여깁니다. 이러한 기존 수요 기반을 바탕으로, 미국의 봉합 와이어 시장은 수술법 선호도에 따른 단기적인 변화의 영향을 덜 받는 안정적인 수요 기반을 갖추고 있습니다. 티타늄 케이블 시스템, 니치놀 계열 제품, 초고분자량 폴리에틸렌(UHMWPE) 섬유 와이어, 코팅된 특수 제품 등 기타 봉합 와이어 유형은 2026년부터 2031년까지 연평균 성장률(CAGR) 4.89%를 나타낼 것으로 예측되며, 향후 확장의 다음 단계가 어디에서 형성되고 있는지를 보여주고 있습니다.

이 부문에서 나타나는 프리미엄 성장은 원자재 그 자체보다는 오히려 기술적 품질에 의해 형성되고 있습니다. 2025년 4월 『Archives of Orthopaedic and Trauma Surgery』지에 게재된 연구에 따르면, 더블 루프 방식의 서클라주 구조는 싱글 루프 방식의 대체품보다 더 강력하고 일관된 압축력을 발휘하는 것으로 나타났습니다. 이는 와이어 구성에 있어 부가가치가 높은 설계 개선을 뒷받침하는 것입니다. 이러한 증거는 공급업체가 표준 처리 방식에서 스테인리스 스틸을 완전히 대체할 수 있다고 주장하지 않으면서도, 성능 중심의 포지셔닝을 정당화하는 데 도움이 됩니다. 규제상의 요건 또한 기존 공급업체에 유리하게 작용하고 있습니다. 왜냐하면 새로운 합금이나 표면 처리는 대기업들이 이미 관리 체계를 갖추고 있는 것과 동일한 생체적합성, 멸균 및 의료기기 관리 검사에 합격해야 하기 때문입니다. 그 결과, 이 부문에서는 기존의 철강 제품이 판매량의 기반을 유지하는 한편, 특수한 형태의 제품은 해당 카테고리의 표준을 대체하기보다는 신중하게 선별된 임상 분야의 틈새 시장에서 우선적으로 시장 점유율을 확대해 나가는 상황이 나타나고 있습니다.

2025년, 스테인리스 스틸은 미국 봉합 와이어 시장 규모의 73.88%를 계속 차지했습니다. 이는 심장외과 및 정형외과 수술 프로토콜에서 오랫동안 사용되어 왔으며, 많은 의료 기관에서 여전히 기본 재료로서의 위상을 유지하고 있음을 반영합니다. 인장 강도와 비용의 균형, 멸균 방법에 대한 익숙함, 그리고 표준화된 수술 트레이로의 광범위한 채택 덕분에 스테인리스 스틸은 일상적인 조달 결정에서 여전히 핵심적인 위치를 차지하고 있습니다. 이러한 안정성은 중요한 의미를 지닙니다. 왜냐하면 병원의 구매 담당자들은 여전히 기존의 업무 흐름, 교육, 승인 시스템에 이미 부합하는 자재를 중시하고 있기 때문입니다. 그 밖의 금속 및 합금은 2026년부터 2031년까지 연평균 성장률(CAGR) 5.89%를 나타낼 것으로 예측되며, 미국 봉합 와이어 시장에서 가장 빠르게 성장하는 소재 부문이 될 전망입니다.

이러한 성장은 외과의사들이 MRI 호환성, 절단 위험 감소, 또는 취약한 뼈나 고위험 흉골 폐쇄 사례에서 서로 다른 성능 특성을 요구하는 경우에 집중되고 있습니다. 티타늄은 비만, 골다공증 또는 임플란트 고정 안정성을 저해하는 기타 요인을 가진 환자에게 실용적인 선택지로 간주되기 때문에 이러한 변화의 중심에 자리 잡고 있습니다. 등탄성 흉골 폐쇄 시스템을 둘러싼 임상시험 동향을 보면, 이 시스템이 광범위하게 도입되기까지는 시간이 걸리겠지만, 대체 소재 시스템이 단순한 논의 단계에서 공식적인 평가 단계로 넘어가고 있음이 드러나고 있습니다. 조달 동향 또한 2025년 관세와 관련된 투입 비용 압박의 영향을 받고 있으며, 이로 인해 특수 제품에 대한 이중 조달 및 지역별 제조 전략에 대한 관심이 높아지고 있습니다. 그 결과, 미국의 봉합 와이어 시장에서는 비용 중시에 따른 스테인리스 스틸의 표준화와, 성능 차이가 가격 부담을 정당화한다고 판단되는 증례에서 첨단 소재를 선별적으로 사용하는 경향 사이에서 양극화가 진행되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the united states suture wire market size is projected to expand from USD 1.26 billion in 2025 and USD 1.30 billion in 2026 to USD 1.57 billion by 2031, registering a CAGR of 3.79% between 2026 to 2031.

This report is Segmented by Type (Stainless Steel Suture Wire, Other Types), Material (Stainless Steel, Other Metals and Alloys), End User (Hospitals, Ascs, Specialty Clinics), Application (Cardiovascular Surgery, Orthopedic Surgery, General Surgery, Ophthalmic Surgery, Other Surgical Applications). The Market Forecasts are Provided in Terms of Value (USD).

United States Suture Wire Market Trends and Insights

Rising US Surgical Volumes and Procedure Intensity

The United States suture wire market draws support from a national surgical base that exceeds 52 million procedures each year, giving suppliers a broad and recurring demand foundation across care settings. Volume alone is not the only factor, because case mix is also shifting toward more complex interventions where closure security matters more and metal wire remains clinically familiar. Open-heart surgery still creates one of the most dependable consumption pools, with more than 300,000 annual procedures and continued reliance on stainless steel wire for standard sternotomy closure in routine-risk patients. The Society of Thoracic Surgeons database reinforces that base, covering more than 8.3 million cumulative procedures across over 1,000 institutions and more than 97% of U.S. cardiac surgery programs. Higher-acuity case flow also keeps hospitals focused on dependable wire supply, because closure failure, readmission, and reintervention carry material clinical and financial consequences. At the same time, the United States suture wire market must monitor a selective shift in high-risk patients toward rigid fixation systems, which may narrow wire use in a small subset of complex cardiac cases over time.

Orthopedic and Cardiovascular Wire-Intensive Procedure Growth

The United States suture wire market remains anchored in orthopedic and cardiovascular surgery because these two specialties account for most stainless steel wire consumption. Cardiac care continues to rely on metal wire after median sternotomy, which preserves a stable volume base even when hospitals push harder on pricing. Orthopedic demand is also broad, covering periprosthetic fracture fixation, patellar repair, revision arthroplasty, and other cerclage-driven reconstruction procedures that still require strong non-absorbable fixation. Joint replacement volumes already exceed 1.5 million procedures per year in the country, which keeps fixation-related demand elevated as revision and trauma workloads expand with age. A 2024 analysis presented to the World Society of Cardiovascular and Thoracic Surgeons found that all 37 sternal readmissions in the compared cohorts occurred in the wire cerclage group and averaged USD 42,326 per admission, which is pushing providers toward more selective patient risk stratification. This does not remove wire from practice, but it does mean the United States suture wire market is becoming more segmented between routine cases that stay with standard steel formats and higher-risk cases that may justify alternative fixation systems.

Competition From Staplers, Adhesives, and Absorbable Polymer Sutures

The United States suture wire market faces its clearest substitution risk outside cardiac and orthopedic surgery, where alternative closure methods already have stronger clinical acceptance. Staplers continue to improve in soft-tissue closure, and Johnson & Johnson launched the ETHICON 4000 Stapler in the United States in June 2025 before securing CE Mark approval for the platform in April 2026. Tissue adhesives and high-performance absorbable sutures have also reduced wire use in superficial, laparoscopic, and minimally invasive procedures. Even in sternotomy closure, a 2025 Journal of Clinical Medicine study reported greater biomechanical load tolerance for UHMWPE suture tapes than standard steel wires, showing that alternative formats are becoming more credible in selected cardiac cases. Adoption remains limited in routine practice because steel wire is familiar, cost-effective, and well embedded in standard protocols. Even so, this keeps the United States suture wire market the strongest in entrenched procedures while capping upside in applications where wire is not the default closure option.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Ambulatory and Outpatient Surgery Settings

- Demand for Lower-Infection-Profile Closure Materials

- Pricing Pressure From Group Purchasing Organizations and IDNs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stainless steel suture wire held 61.42% of United States suture wire market share in 2025, which kept it clearly ahead of specialty formats across the category. Its leadership came from broad use in sternal closure, orthopedic cerclage, hernia reinforcement, and abdominal wound closure, where surgeons continue to value dependable tensile performance and familiar handling. That installed base gives the United States suture wire market a stable demand core that is less exposed to short-term changes in procedural preference. Other suture wire types, including titanium cable systems, nitinol-based configurations, UHMWPE fiber wire, and coated specialty formats, are projected to grow at 4.89% CAGR from 2026 to 2031, showing where the next layer of expansion is forming.

Premium growth within this segment is being shaped more by engineering quality than by raw material identity alone. Research published in Archives of Orthopaedic and Trauma Surgery in April 2025 showed that double-looped cerclage constructs produced stronger and more consistent compression than single-looped alternatives, which supports higher-value design improvements in wire configuration. That kind of evidence helps suppliers justify performance-led positioning without claiming a full replacement of stainless steel in standard care. Regulatory demands also favor established suppliers, because novel alloys and surface modifications must pass the same biocompatibility, sterilization, and device control checks that larger players are already equipped to manage. The result is a segment where incumbent steel products retain the volume base, while specialty formats expand first in carefully selected clinical niches rather than replacing the category standard.

Stainless steel retained 73.88% of the United States suture wire market size in 2025, reflecting its long use across cardiac and orthopedic protocols and its continued position as the default material in many facilities. Its tensile-to-cost balance, sterilization familiarity, and broad inclusion in standardized surgical trays keep it central to routine procurement decisions. This stability matters because hospital buyers still place heavy weight on materials that already fit existing workflow, training, and approval systems. Other metals and alloys are projected to grow at 5.89% CAGR from 2026 to 2031, making this the fastest-growing material tier in the United States suture wire market.

That growth is concentrated in cases where surgeons want MRI compatibility, lower cutting risk, or a different performance profile in fragile bone and high-risk sternal closure. Titanium sits at the center of this shift because it is seen as a practical option for patients with obesity, osteoporosis, or other factors that complicate closure stability. The clinical trial activity around iso-elastic sternal closure systems shows that alternative material systems are moving from discussion into formal evaluation, even if broad adoption will take time. Procurement behavior is also being affected by 2025 tariff-related input cost pressure, which has increased attention on dual sourcing and regional manufacturing strategies for specialty products. The practical outcome is a split inside the United States suture wire market between cost-led stainless steel standardization and targeted use of advanced materials in cases where performance differences are considered worth the premium.

Complete Report Scope:

- By Type

- Stainless Steel Suture Wire

- Other Suture Wire Types

- By Material

- Stainless Steel

- Other Metals and Alloys

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Application

- Cardiovascular Surgery

- Orthopedic Surgery

- General Surgery

- Ophthalmic Surgery

- Other Surgical Applications

List of Companies Covered in this Report:

- AEMEDICAL Corporation

- Advanced Medical Solutions Group

- B. Braun

- Beckton Dickinson

- Boston Scientific

- Conmed

- Corza Medical

- CP Medical, Inc.

- DemeTECH

- Dynarex

- Ethicon US, LLC.

- Integra LifeSciences

- Johnson & Johnson

- Medtronic

- Molnlycke Health Care

- Smiths Group

- Stryker

- Surgical Specialties

- Teleflex

- W. L. Gore and Associates, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising U.S. Surgical Volumes and Procedure Intensity

- 4.2.2 Shift Toward Ambulatory and Outpatient Surgery Settings

- 4.2.3 Demand for Lower-Infection-Profile Closure Materials

- 4.2.4 Sterile Packaging and Kit Integration for High-Throughput Operating Rooms

- 4.2.5 Dual-Source Procurement Requirements From Health Systems

- 4.2.6 Orthopedic and Cardiovascular Wire-Intensive Procedure Growth

- 4.3 Market Restraints

- 4.3.1 Competition From Staplers, Adhesives, and Absorbable Polymer Sutures

- 4.3.2 Pricing Pressure From Group Purchasing Organizations and IDNs

- 4.3.3 Regulatory Validation Burden for Material, Process, and Sterilization Changes

- 4.3.4 Limited Clinical Differentiation in Commodity Wire Formats

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Stainless Steel Suture Wire

- 5.1.2 Other Suture Wire Types

- 5.2 By Material

- 5.2.1 Stainless Steel

- 5.2.2 Other Metals and Alloys

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics

- 5.4 By Application

- 5.4.1 Cardiovascular Surgery

- 5.4.2 Orthopedic Surgery

- 5.4.3 General Surgery

- 5.4.4 Ophthalmic Surgery

- 5.4.5 Other Surgical Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AEMEDICAL Corporation

- 6.3.2 Advanced Medical Solutions Group plc

- 6.3.3 B. Braun SE

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Boston Scientific Corporation

- 6.3.6 CONMED Corporation

- 6.3.7 Corza Medical

- 6.3.8 CP Medical, Inc.

- 6.3.9 DemeTECH Corporation

- 6.3.10 Dynarex Corporation

- 6.3.11 Ethicon US, LLC.

- 6.3.12 Integra LifeSciences Holdings Corporation

- 6.3.13 Johnson and Johnson

- 6.3.14 Medtronic

- 6.3.15 Molnlycke Health Care AB

- 6.3.16 Smith and Nephew plc

- 6.3.17 Stryker Corporation

- 6.3.18 Surgical Specialties Corporation

- 6.3.19 Teleflex Incorporated

- 6.3.20 W. L. Gore and Associates, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment