|

시장보고서

상품코드

2072937

아미노산 어세이 키트 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Amino Acid Assay Kit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

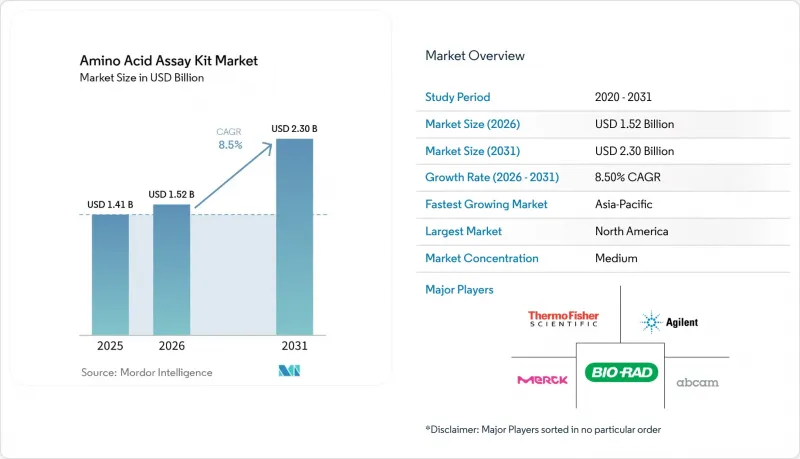

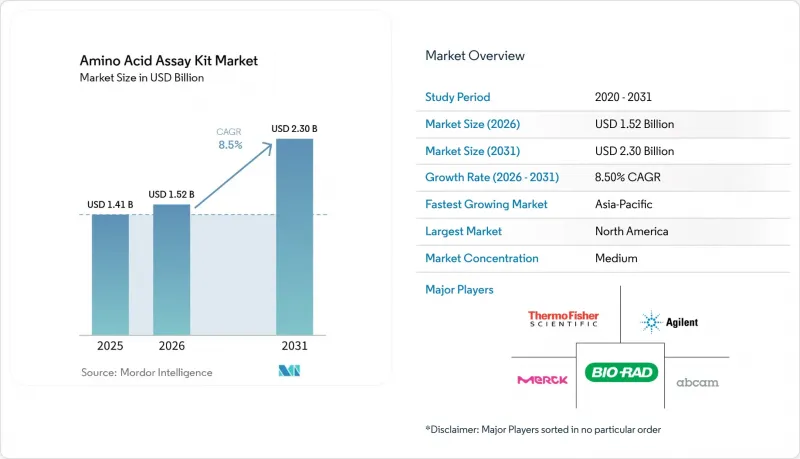

Mordor Intelligence에 의하면, 아미노산 어세이 키트 시장 규모는 2025년에 14억 1,000만 달러, 2026년에 15억 2,000만 달러되어, 2031년까지 23억 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 8.5%로 성장할 전망입니다.

본 보고서는 키트 유형(비색법 어세이 키트, 형광법 어세이 키트 등), 용도(단백질 어세이, 아미노산 프로파일링 등), 최종 사용자(제약, 생명공학 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 아미노산 어세이 키트 시장 동향 및 인사이트

생명과학 분야 전반에 걸친 정량적 아미노산 분석에 대한 수요 증가

메타보로믹스는 탐색적 도구에서 제약 연구, 중개 의학, 질병 선별 검사 분야의 핵심 요소로 자리매김하고 있으며, 이에 따라 아미노산 어세이 키트 시장은 일상적인 용도로 그 영역을 넓혀가고 있습니다. 검증이 완료된 아미노산 패널은 재현성과 확장성이 요구되는 분석 워크플로우에서 이제 필수적인 요소가 되었습니다. 2025년 연구에 따르면, 혈장 아미노산 농도의 특이적 패턴을 통해 4가지 주요 암 유형을 78%의 민감도와 0%의 위양성률로 검출할 수 있었으며, 97건의 검체로 구성된 검증 코호트에서 AUROC 0.95를 달성한 것으로 나타났습니다. 본 조사에서는 일반적인 검체 전처리 공정이 불필요해짐에 따라 1차 선별 검사에서 아미노산 검사의 실현 가능성이 높아지고, 종양학 검사 프로그램에서 새로운 기회가 창출될 뿐만 아니라, 조사 및 진단 과정에서 임상 등급의 일관성이 요구된다는 점이 강조되고 있습니다.

단백질체학 및 바이오마커 발굴 프로그램의 확대

단백질체학 프로그램에서는 신약 개발 워크플로우에 아미노산 어세이 분석을 도입하는 추세가 점점 더 확산되고 있으며, 이는 아미노산 어세이 키트 시장 수요를 끌어올리고 있습니다. 써모피셔 사이언티피크가 2024년에 Olink를 인수함에 따라, 아미노산 프로파일링이 “UK Biobank 제약 단백질체학 프로젝트”와 협력하게 되었습니다. 이 프로젝트에서는 바이오마커 발견을 목적으로 60만 건의 샘플에서 5,400종 이상의 단백질을 분석했습니다. 이러한 확대로 인해 교정 등급 어세이 키트의 필요성이 높아지면서, 효소법 및 크로마토그래피법을 활용한 분석 방식의 성장이 가속화되고 있습니다. 이는 정교한 분석을 수행하기 전에 일관성 있는 단백질 어세이가 여전히 필수적이기 때문입니다. 이 시장은 업스트림 공정의 표준화와 다운스트림 공정의 검증이라는 두 가지 측면에서 혜택을 받고 있으며, 전체 워크플로우의 처리량 증가를 뒷받침하고 있습니다.

장치에 따른 성능 및 통합과 관련된 과제

많은 키트가 특정 형광 측정 장치, 이온 교환 분석 장치 또는 LC-MS 구성에 최적화되어 있기 때문에 장비와의 호환성은 여전히 아미노산 어세이 키트 시장에서 큰 제약 요인으로 남아 있습니다. 다양한 장비를 보유한 연구소에서는 기존 하드웨어에서 새로운 키트의 검증 과정을 진행할 때 어려움에 직면하여, 기술적 성능이 뛰어나더라도 도입이 지연되는 경우가 있습니다. 이 과정에는 측정 방법의 전환, 문서화 및 직원 교육을 위해 막대한 시간과 자원이 필요합니다. 자원이 제한된 중규모 기관은 특히 이러한 영향에 취약하며, 우수한 대체품이 있더라도 익숙하고 검증된 키트를 우선적으로 선택하는 경우가 많습니다. 장비와 시약을 아우르는 통합 워크플로우를 제공하는 공급업체는 도입에 따른 불확실성을 줄임으로써 경쟁 우위를 확보하고 있습니다.

부문별 분석

2025년, 비색 어세이 키트는 아미노산 어세이 키트 시장의 35.13%를 차지하며, 키트 유형별 시장에서 1위를 유지했습니다. 이러한 인기는 표준 마이크로플레이트 리더와의 호환성, 간결한 워크플로우, 그리고 식품, 음료, 제약 업계의 품질 관리 실험실에서 사용하기 편리하다는 점에 기인합니다. 이 키트들은 효소 촉매를 이용한 산화법을 채택하고 있으며, 혈청, 소변, 조직 균질액 등의 시료에 대해 3.3µM에서 500µM에 이르는 선형 검출 범위를 제공합니다. 효소 어세이 키트는 기질 특이적 선택성에 대한 요구를 충족시키는 한편, 크로마토그래피 키트는 비용은 높지만 견고한 분석적 타당성 검증이 요구되는 규제 환경에서 지지를 넓혀가고 있습니다.

시장 세분화에서는 일상적인 대량 처리에 적합한 포맷과 고성능 특수 용도에 적합한 포맷 사이에서 세분화가 점점 더 진행되고 있습니다. 2031년까지 연평균 성장률(CAGR) 10.25%를 나타낼 것으로 예측되는 형광 측정 어세이 키트는 가장 빠르게 성장하고 있는 부문입니다. 대부분의 비색법에 비해 10-25배 더 뛰어난 검출 한계를 가지고 있어, 건조 혈액 스팟이나 마이크로바이오리액터 배지 등 저농도 시료에 가장 적합합니다. 또한, 이러한 키트는 다중 측정 및 자동화 워크플로우와도 잘 어울려, 제약 업계의 자동화 사이클에서 그 역할을 강화하고 있습니다.

지역별 분석

2025년, 북미는 아미노산 어세이 키트 시장에서 39.56%의 점유율을 차지하며 1위를 차지했습니다. 이는 미국의 강력한 제약 연구개발 역량, 대규모 바이오의약품 생산 거점, 그리고 엄격한 단백질 표시 규제가 주도한 결과입니다. 지역별 수요 측면에서 미국이 주도적인 위치를 차지한 반면, 캐나다는 학술 및 정부 연구를 통해 기여했으며, 멕시코는 제약 제조 분야의 니어쇼어링을 통해 입지를 강화했습니다. 유럽은 2위 시장이 되었으며, 독일, 프랑스, 영국이 이를 뒷받침했습니다. 이 국가들에서는 대학과 연계된 단백질체학 연구센터와 확립된 식품 안전 검사 시스템이 수요를 지탱해 주었습니다. 머크 KGaA는 브래니 비즈니스 파크에 1억 5,000만 유로(1억 6,500만 달러) 규모의 시설을 건설하고, 4억 4,000만 유로(4억 8,400만 달러)를 투자하는 등, 아일랜드에서의 사업 확장을 통해 유럽의 중요성을 강조했습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 10.12%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 지역이 될 전망입니다. 이러한 성장은 의료비 증가, 제약 생산 확대, 그리고 정부가 지원하는 신생아 선별 검사 사업에 힘입어 이루어지고 있습니다. 중국은 생명공학 정책 지원과 비용 대비 효과가 높은 MS/MS 기반의 신생아 선별 검사를 통해 중심적인 역할을 수행하고 있습니다. 선진적인 하위 시장인 일본과 한국에서는 확립된 분석 장비와 자동화 시스템이 활용되고 있는 반면, 인도의 수탁 연구 기반과 호주의 활발한 대학 연구 네트워크가 수요를 더욱 끌어올리고 있습니다.

중동 및 아프리카(MEA) 및 남미는 아미노산 어세이 키트의 신흥 시장이며, 정식 검사 인프라 구축이 진행되고 있습니다. MEA 지역에서는 사우디아라비아와 아랍에미리트(UAE)가 병원 기반의 신생아 선별 검사에 투자하고 있으며, 남아프리카공화국에서는 대학 부속 의료센터를 통해 수요가 유지되고 있습니다. 남미에서는 브라질과 아르헨티나가 수요의 주축을 이루고 있으며, 브라질의 제약 및 식품 검사 부문이 구매를 주도하고 있습니다. 이러한 지역에서는 가격에 대한 민감성과 콜드체인 체계의 미비로 인해 비색법이나 효소법을 이용한 키트가 선호되고 있어, 북미, 유럽 및 아시아태평양의 선진 지역과는 다른 제품 구성을 보이고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the amino acid assay kit market size is projected to be USD 1.41 billion in 2025, USD 1.52 billion in 2026, and reach USD 2.30 billion by 2031, growing at a CAGR of 8.5% from 2026 to 2031.

This report is Segmented by Kit Type (Colorimetric Assay Kits, Fluorometric Assay Kits, and More), Application (Protein Quantification, Amino Acid Profiling, and More), End User (Pharmaceuticals, Biotechnology, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Amino Acid Assay Kit Market Trends and Insights

Rising Need for Quantitative Amino Acid Research Across Life Sciences

Metabolomics has transitioned from an exploratory tool to a critical component in pharmaceutical research, translational medicine, and disease screening, driving the amino acid assay kit market toward routine applications. Validated amino acid panels are now integral to workflows requiring repeatable and scalable testing. A 2025 study demonstrated that plasma amino acid concentration signatures detected four major cancer types with 78% sensitivity and a 0% false positive rate, achieving an AUROC of 0.95 in a validation cohort of 97 samples. The study's elimination of common sample pre-treatment steps enhances the feasibility of amino acid testing in frontline screening, creating opportunities in oncology testing programs and emphasizing the need for clinical-grade consistency in research and diagnostics.

Expanding Proteomics and Biomarker Discovery Programmes

Proteomics programs are increasingly incorporating amino acid quantification into drug discovery workflows, boosting demand in the amino acid assay kit market. Thermo Fisher Scientific's acquisition of Olink in 2024 linked amino acid profiling to the UK Biobank Pharma Proteomics Project, which analyzes over 5,400 proteins from 600,000 samples for biomarker discovery. This expansion drives the need for calibration-grade quantification kits and supports growth in enzymatic and chromatographic formats, as consistent protein quantification remains essential before advanced analyses. The market benefits from both upstream standardization and downstream validation, supporting volume growth across workflows.

Instrument-Dependent Performance and Integration Challenges

Instrument compatibility remains a significant limitation in the amino acid assay kit market, as many kits are optimized for specific fluorometric readers, ion-exchange analyzers, or LC-MS configurations. Laboratories with diverse instrument fleets face challenges in validating new kits on existing hardware, delaying adoption despite strong technical performance. The process requires substantial time and resources for method transfer, documentation, and staff training. Mid-tier institutions, with limited resources, are particularly affected, often favoring familiar, validated kits over superior alternatives. Suppliers offering integrated workflows across instruments and reagents hold a competitive edge by reducing implementation uncertainties.

Other drivers and restraints analyzed in the detailed report include:

- Food Authentication and Protein Label Verification Requirements

- Higher Adoption of Multiplex and High-Throughput Screening Platforms

- Short Shelf Life and Cold-Chain Dependence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, colorimetric assay kits accounted for 35.13% of the amino acid assay kit market, maintaining their leading position among kit types. Their popularity stems from compatibility with standard microplate readers, simple workflows, and ease of use in quality control labs across food, beverage, and pharmaceutical industries. These kits utilize enzyme-catalyzed oxidation methods, offering linear detection ranges from 3.3 µM to 500 µM for samples like serum, urine, and tissue homogenates. Enzymatic assay kits cater to substrate-specific selectivity needs, while chromatographic kits, though costlier, are gaining traction in regulated environments requiring robust analytical validation.

The market is increasingly segmented between routine volume formats and high-performance specialty formats. Fluorometric assay kits, projected to grow at a 10.25% CAGR through 2031, are the fastest-growing segment. Their superior detection limits, 10 to 25 times better than many colorimetric alternatives, make them ideal for low-abundance samples like dried blood spots and microbioreactor media. These kits also align well with multiplexing and automated workflows, strengthening their role in pharmaceutical automation cycles.

Complete Report Scope:

- By Assay Kit Type

- Colorimetric Assay Kits

- Fluorometric Assay Kits

- Chromatographic Assay Kits

- Enzymatic Assay Kits

- By Application

- Protein Quantification

- Amino Acid Profiling

- Nutritional Analysis

- Medical Diagnostics

- Research Purposes

- By End User

- Pharmaceuticals

- Biotechnology

- Food and Beverage

- Diagnostic Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America led the amino acid assay kit market with a 39.56% share, driven by strong pharmaceutical R&D, a large biopharmaceutical manufacturing base, and stringent protein labeling regulations in the U.S. The U.S. dominated regional demand, while Canada contributed through academic and government research, and Mexico gained prominence with near-shoring in pharmaceutical manufacturing. Europe ranked as the second-largest market, supported by Germany, France, and the U.K., where university-linked proteomics centers and established food safety testing systems sustained demand. Merck KGaA emphasized Europe's importance with its Irish expansion, including a EUR 150 million (USD 165 million) facility at Blarney Business Park and a EUR 440 million (USD 484 million) investment.

Asia-Pacific is projected to grow at a 10.12% CAGR through 2031, making it the fastest-growing region. Growth is driven by rising healthcare spending, expanding pharmaceutical manufacturing, and government-backed newborn screening initiatives. China plays a central role due to biotechnology policy support and cost-effective MS/MS-based newborn screening. Japan and South Korea, as advanced sub-markets, utilize established analyzers and automated systems, while India's contract research base and Australia's active university research network further boost demand.

MEA and South America are emerging markets for amino acid assay kits, progressing toward formal testing infrastructure. In MEA, Saudi Arabia and the UAE are investing in hospital-based newborn screening, while South Africa maintains demand through academic medical centers. In South America, Brazil and Argentina anchor demand, with Brazil's pharmaceutical and food testing sectors leading purchases. Price sensitivity and inconsistent cold-chain systems in these regions favor colorimetric and enzymatic kits, resulting in a distinct product mix compared to North America, Europe, and advanced parts of Asia-Pacific.

- Abcam

- Agilent Technologies

- BioAssay Systems

- Bio-Rad Laboratories

- Biovision

- Cell Biolabs

- Creative Enzymes

- CUSABIO Technology LLC

- Danaher

- Elabscience Biotechnology

- Roche

- Genscript

- Merck

- Promega

- Randox Laboratories

- RayBiotech, Inc.

- Revvity, Inc.

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Need for Quantitative Amino Acid Readouts in Clinical Metabolic Workflows

- 4.2.2 Expanding Proteomics and Biomarker Discovery Pipelines in Biopharma

- 4.2.3 Food Authentication and Protein Label Verification Requirements

- 4.2.4 Point-of-Care And Low-Volume Workflow Preference for Rapid Colorimetric and Fluorometric Kits

- 4.2.5 Higher Adoption of Multiplex and High-Throughput Assays in Research Labs

- 4.2.6 Regulatory and Quality-Control Push for Standardized Amino Acid Quantification in Diagnostics and Nutrition

- 4.3 Market Restraints

- 4.3.1 Instrument-Dependent Performance and Interference Sensitivity Across Sample Matrices

- 4.3.2 Limited Differentiation in Commodity Assay Formats Pressuring Pricing

- 4.3.3 Fragmented Validation Standards Across End Uses Slowing Routine Clinical Uptake

- 4.3.4 Short Shelf Life and Cold-Chain Dependence for Certain Reagents and Enzymatic Kits

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Assay Kit Type

- 5.1.1 Colorimetric Assay Kits

- 5.1.2 Fluorometric Assay Kits

- 5.1.3 Chromatographic Assay Kits

- 5.1.4 Enzymatic Assay Kits

- 5.2 By Application

- 5.2.1 Protein Quantification

- 5.2.2 Amino Acid Profiling

- 5.2.3 Nutritional Analysis

- 5.2.4 Medical Diagnostics

- 5.2.5 Research Purposes

- 5.3 By End User

- 5.3.1 Pharmaceuticals

- 5.3.2 Biotechnology

- 5.3.3 Food and Beverage

- 5.3.4 Diagnostic Centers

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abcam plc

- 6.3.2 Agilent Technologies, Inc.

- 6.3.3 BioAssay Systems

- 6.3.4 Bio-Rad Laboratories, Inc.

- 6.3.5 BioVision, Inc.

- 6.3.6 Cell Biolabs, Inc.

- 6.3.7 Creative Enzymes

- 6.3.8 CUSABIO Technology LLC

- 6.3.9 Danaher Corporation

- 6.3.10 Elabscience Biotechnology Inc.

- 6.3.11 F. Hoffmann-La Roche AG

- 6.3.12 GenScript Biotech Corporation

- 6.3.13 Merck KGaA

- 6.3.14 Promega Corporation

- 6.3.15 Randox Laboratories Ltd.

- 6.3.16 RayBiotech, Inc.

- 6.3.17 Revvity, Inc.

- 6.3.18 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment