|

시장보고서

상품코드

2073008

기침 시럽 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cough Syrup - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

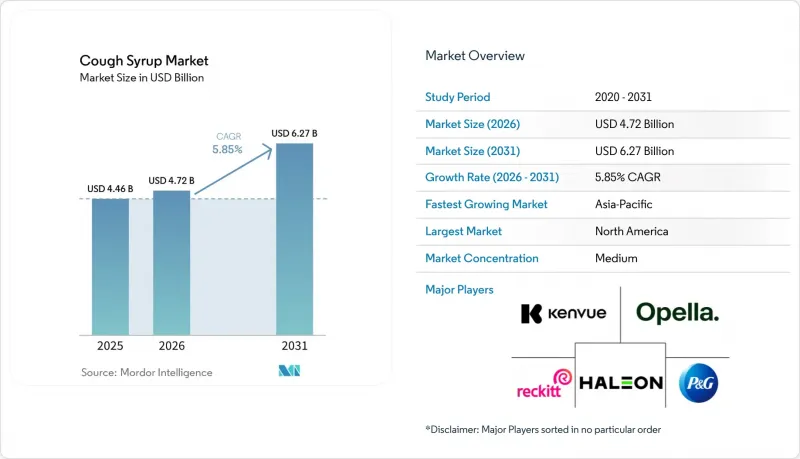

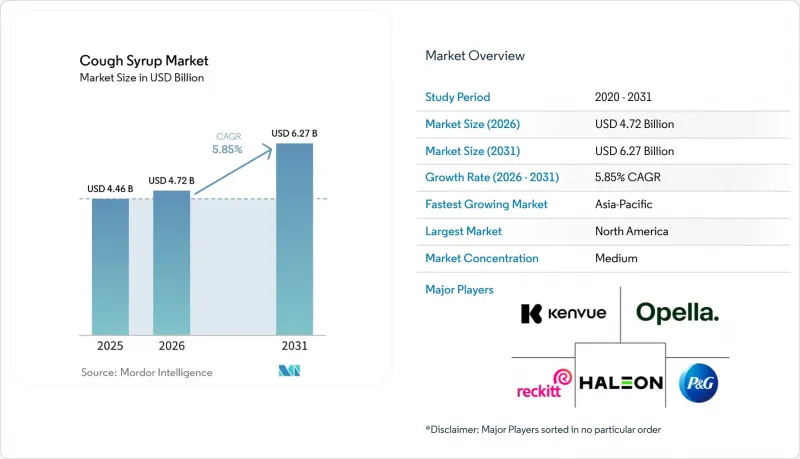

Mordor Intelligence에 의하면, 기침 시럽 시장 규모는 2025년에 44억 6,000만 달러로 평가되었고 2026년 47억 2,000만 달러에서 2031년까지 62억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.85%를 나타낼 전망입니다.

본 보고서는 제품 유형(거담제, 진해제, 복합제), 연령대(소아, 성인, 고령자), 처방 형태(처방약, 일반의약품), 기침 유형(건성 기침, 습성 기침), 판매 채널(소매, 병원, 온라인 약국), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계 기침 시럽 시장 동향 및 분석

상기도 감염의 유병률 증가

상기도 감염증은 다양한 연령대와 소득 수준에서 단기적인 증상 완화 수요가 반복적으로 발생하기 때문에 기침 시럽 시장에 있어 여전히 가장 광범위한 수요의 주축 중 하나입니다. 장기적인 연령 조정 발병률은 일부 지역에서 감소하고 있을 가능성이 있지만, 인구 증가에 따라 발병 건수의 절대 수는 계속 증가하고 있으며, 이로 인해 기침 시럽 시장 전체의 치료량은 높은 수준을 유지하고 있습니다. 미국의 2025년부터 2026년까지의 독감 시즌에는 2026년 4월 기준으로 이미 최소 4,700만 명의 감염자와 61만 명의 입원자가 발생했으며, 이러한 계절성 질환의 규모가 기침·감기약의 높은 판매 실적을 지속적으로 뒷받침하고 있습니다. 이러한 경향이 중요한 이유는 기침 시럽 시장이 단순히 프리미엄화나 판로 확대에만 의존하는 것이 아니라, 대체하기 어려운 대규모의 반복적인 질병 부담에 의해서도 지탱되고 있기 때문입니다. 또 다른 변화로, 일부 지역에서는 바이러스의 계절적 양상을 예측하기 어려워지고 있어, 이로 인해 연간 수요가 평준화될 가능성은 있지만, 제조업체 입장에서는 재고 관리 시기, 판촉 활동, 미디어 광고비 배분이 복잡해질 우려도 있습니다. 따라서 기침 시럽 시장은 단순히 연간 전체 카테고리의 성장뿐만 아니라, 공급의 유연성과 소매 현장의 실행력에 대한 의존도가 높아지고 있습니다.

일반의약품 기침약에 대한 선호도 증가

기침 시럽 시장은 특히 의사의 진찰이 반드시 필요하지 않은 경미한 호흡기 질환의 경우, 소비자들이 자가 관리를 통한 치료를 분명히 선호하는 경향 덕분에 계속해서 혜택을 보고 있습니다. 2025년에는 일반의약품이 이미 60.52%의 시장 점유율을 차지하고 있으며, 처방약 유형 중에서도 가장 높은 성장률을 보일 것으로 전망됩니다. 이는 기침 시럽 시장의 이 부문이 규모와 성장세 양면에서 모두 확대되고 있음을 보여줍니다. 이러한 변화는 단순한 편의성 이상의 의미를 담고 있으며, 소비자들이 일상적인 질병에 대해 현재 취하고 있는 대응 방식에 부합하고, 접근성이 높으며, 신속하고, 친숙한 증상 완화 방안을 추구하는 실용적인 움직임을 보여주고 있습니다. 신흥 시장에서는 약국이 종종 첫 번째 의료 접근처가 되기 때문에 이러한 경향이 더욱 두드러지며, 일반의약품 기침 시럽은 치료 과정에서 최전선 역할을 담당하고 있습니다. 성숙한 시장에서는 이러한 소비 성향으로 인해 제품의 다양성이 높아지고, 진열대의 상품 구색이 풍부해지며, 재구매가 가속화되는 한편, 브랜드 제품이 명확한 차별화를 유지하지 못할 경우, 자체 브랜드(PB)의 성장 여지도 확대됩니다. 그 결과, 기침 시럽 시장에서는 신제품 출시나 감기·독감의 단기적인 유행뿐만 아니라, 소비자의 행동 그 자체에 의해 판매량이 더욱 강력하게 뒷받침되고 있는 상황이 나타나고 있습니다.

유효 성분에 대한 엄격한 안전성 및 표시 규정의 준수

기침 시럽 시장은 현재 몇몇 주요 시장에서 동시에 유효 성분에 대한 면밀한 검토가 진행되고 있어, 규제 준수 환경이 더욱 엄격해지고 있습니다. FDA는 2024년 11월, OTC 모노그래프 M012에서 경구용 페닐에프린을 공인된 코막힘 완화제 목록에서 제외할 것을 제안했습니다. 이로 인해 제약사들은 다음 시즌을 앞두고 관련 감기·기침 복합제의 재평가를 실시해야만 했습니다. FDA의 예측에 따르면, 소아용 기침·감기약의 투여량에 대한 지속적인 재검토가 시사되고 있으며, 이에 따라 저연령아용 제품에 대해 추가적인 표시 및 위험 관리 요건이 부과될 가능성이 높아졌습니다. 호주에서는 치료용 의약품청(TGA)이 2024년에 덱스트로메토르판의 분류를 재검토하여, 오용에 대한 우려를 여전히 강조하면서도 약국 전용 판매를 유지했습니다. 이는 규제 당국의 신중한 태도가 특정 지역에 국한되지 않음을 보여줍니다. 이러한 조치는 이미 시장에 정착된 기존 제품에 대해 처방 변경, 재검증, 라벨 변경, 재출시와 같은 작업이 종종 필요하게 되므로 비용 증가로 이어집니다. 이러한 영향은 기침 시럽 시장에서 특히 두드러집니다. 왜냐하면 중소 제조업체는 대형 브랜드 기업만큼 반복되는 규정 준수 대응 주기를 감당할 수 있는 기술적·재정적 여유가 없을 가능성이 있기 때문입니다.

부문별 분석

2025년, 진해제는 매출의 45.31%를 차지하며, 기침 시럽 시장에서 가장 큰 제품 유형으로서의 입지를 확고히 했습니다. 이러한 우위는 기침 억제 작용을 통한 증상 완화에 대한 소비자들의 오랜 친숙함, 특히 덱스트로메토르판을 주성분으로 하는 제품이 오랫동안 확고한 인지도를 쌓아온 데 힘입은 것이었습니다. 이러한 친근함은 매장 현장에서도 여전히 중요한 요소로 남아 있습니다. 왜냐하면 기침 시럽 시장의 구매자들은 상세한 비교를 하기보다는 이미 알고 있는 유효 성분이나 익숙한 라벨을 바탕으로 신속하게 결정을 내리는 경우가 많기 때문입니다. 또한, 거담제도 여전히 중요한 위치를 차지하고 있습니다. 이는 습성 기침 치료 분야에서 구아이페네신이 여전히 임상적으로나 소비자들 사이에서 높은 인지도를 유지하고 있기 때문입니다. 이러한 균형은 새로운 제형이 주변에서 확산되고 있음에도 불구하고, 기침 시럽 시장의 제품 구조가 여전히 확립된 증상 범주에 뿌리를 두고 있음을 보여줍니다.

복합 제제는 2031년까지 연평균 성장률(CAGR) 7.38%를 나타낼 것으로 예측되며, 이는 기침 시럽 시장에서 가장 성장세가 두드러진 제품군임을 보여줍니다. 이러한 부상은 하나의 제품으로 여러 증상을 해결할 수 있다는 뚜렷한 추세를 반영하고 있으며, 이를 통해 소매점 진열대의 복잡성이 줄어들고 소비자의 선택도 단순화됩니다. 이러한 변화는 건성 기침 시럽이나 습성 기침 시럽에 대한 수요를 보다 광범위한 다중 증상 대응 제품 구매 기회로 전환하고, 기침 시럽 시장에서 복합 제품의 실질적인 역할을 확대한다는 점에서 중요합니다. 동시에, 특정 유효 성분에 대한 규제 당국의 심사로 인해 제조업체들은 배합 변경의 수단으로 복합 제품 라인을 활용해야 하는 상황에 놓여 있으며, 이러한 제품들은 상업적 목표와 규정 준수 목표를 모두 점점 더 충족시키고 있습니다. 기침 시럽 업계에서 이를 통해 복합 제품은 프리미엄 효능을 내세울 수 있고, 더 광범위한 유통망을 구축할 수 있으며, 단일 성분 제품이 압박을 받을 때에도 유연하게 대응할 수 있기 때문에 전략적 입지를 강화하고 있습니다.

2025년에는 성인이 48.24%의 점유율을 차지하며, 기침 시럽 시장에서 가장 큰 비중을 차지하는 연령층이 되었습니다. 이러한 위상은 높은 자가치료율, 직장 내 편의성을 중시한 빈번한 구매, 그리고 근로 연령층 소비자들 사이에서 높은 브랜드 인지도에 힘입어 유지되어 왔습니다. 또한, 성인 구매자는 "졸리지 않은", '무설탕', “무알코올”프리미엄 제품의 주요 타겟층이기도 하며, 기침 시럽 시장의 가치 중 상당 부분이 이 계층의 기능성을 중시한 구매를 통해 창출되고 있습니다. 이 점은 중요합니다. 왜냐하면 성인층 수요는 폭이 넓을 뿐만 아니라 재구매율이 높고, 편의성을 중시하는 이점에 대해 기꺼이 비용을 지불할 의향이 있기 때문에 상업적으로도 매력적이기 때문입니다. 고령층 시장 규모는 여전히 작지만, 유럽과 일본의 고령화 추세에 따라 보다 체계적이고 지속적인 관리와 브랜드 충성도를 바탕으로 한 호흡기 증상 관리에 대한 수요가 증가함에 따라 그 중요성이 커지고 있습니다.

소아 시장은 2031년까지 연평균 성장률(CAGR) 6.52%로 확대될 것으로 예상되며, 위험 환경이 악화되고 있음에도 불구하고 기침 시럽 시장에서 가장 빠르게 성장하는 연령층으로 꼽히고 있습니다. 이러한 성장은 소비자 선호도의 향상, 보다 명확한 투여 형태, 그리고 위험성이 높은 유효 성분에 대한 의존도를 낮추기 위한 장기적인 투자를 바탕으로 이루어지고 있습니다. 이로 인해, 비록 고르지 않기는 하지만 중요한 기회가 생겨나고 있습니다. 왜냐하면 제품이 안전성, 사용 편의성, 맛에 관한 더욱 엄격한 기대에 부응할 수 있다면, 소아용 기침 시럽 시장은 여전히 성장 여지가 있기 때문입니다. 따라서 소아용 혁신 의약품은 단순히 성인용 시럽의 용량을 줄인 형태가 아니라, 제형에 특화된 제품이나 복약 순응도를 중시하는 제품으로 변화하고 있습니다. 기침 시럽 업계에서 안전성 측면에서 더욱 확고한 입지를 갖춘 소아용 제제에 대한 투자를 지속하는 기업은 규제 당국의 감시가 점점 더 엄격해지는 상황에서도 시장 접근성을 유지할 가능성이 높아집니다.

지역별 분석

2025년, 북미는 기침 시럽 시장 점유율의 36.52%를 차지하며, 본 보고서에서 지역별 1위를 기록하고 있습니다. 이 지역은 OTC(일반의약품)에 대한 소비자들의 확고한 습관, 광범위하게 구축된 약국 네트워크, 그리고 호흡기 증상 완화 제품으로 정평이 나 있는 브랜드의 높은 인지도 등의 혜택을 누리고 있습니다. 미국에서는 2025년부터 2026년에 걸친 독감 시즌 동안 2026년 4월까지 최소 4,700만 명의 감염자와 61만 명의 입원자가 확인되었으며, 이로 인해 기침·감기약에 대한 계절적 수요가 급증했습니다. 캐나다와 멕시코는 여전히 시장 기여도가 낮은 편이지만, 두 나라 모두 광범위한 약국 네트워크와 확고한 자가치료 습관 덕분에 계속해서 혜택을 누리고 있습니다. 이러한 조합 덕분에 북미는 판매량의 안정성과 브랜드 제품의 뛰어난 수익성을 모두 갖추고 있어, 기침 시럽 시장에서 계속해서 중심적인 위치를 차지하고 있습니다.

유럽은 여전히 기침 시럽 시장의 주요 지역이며, 특히 건성 기침 시럽 및 습성 기침 시럽 부문에서 허브 제품의 보급과 OTC(일반의약품)에 대한 수용도가 모두 충분히 정착되어 있습니다. 독일은 성숙한 소비자 헬스케어 기반과 확립된 허브 의약품 인프라에 힘입어 유럽 내에서 가장 큰 국내 시장 점유율을 차지하고 있습니다. EU의 약초 관련 약전은 유럽을 식물 유래 기침 치료제 분야에서 상업적으로 가장 활발한 지역으로 만드는 데 일조하고 있으며, 레킷사는 자사의 "Strepsils Cough Dual Action" 시리즈가 EU 15개 시장에서 시장 선두 주자 지위를 확보했다고 보고하고 있습니다. 프랑스, 영국, 이탈리아, 스페인도 상당한 매출을 올리고 있지만, 소비자의 선호도는 제형의 형태나 천연 성분의 매력에 따라 달라집니다. 이 지역은 허브 제품 혁신에 대한 규제상의 지원과 차별화된 제형을 시도해 보고자 하는 소비자들의 강한 의지가 결합되어 있어, 기침 시럽 시장에서 여전히 중요한 위치를 차지하고 있습니다.

아시아태평양은 기침 시럽 시장 규모 측면에서 가장 빠르게 성장하고 있는 지역이며, 2031년까지의 연평균 성장률(CAGR)은 7.45%로 전망됩니다. 인도와 중국은 방대한 인구, 약국 접근성 개선, 디지털 헬스 이용 확대에 힘입어 수요가 지속적으로 증가하고 있어 판매량의 주요 견인 역할을 하고 있습니다. 중국에서는 2024년에 덱스트로메토르판(DXM)의 분류가 변경되면서 일반의약품(OTC) 기침약 시장의 구도가 변화했으며, 현재는 DXM을 함유하지 않은 대체 제품을 갖춘 제품 포트폴리오가 유리한 입지를 차지하고 있습니다. 인도에서는 자가치료 증가와 고령 인구 확대에 힘입어 성장이 예상되지만, 2025년에 발생한 오염된 기침 시럽 사건을 계기로 품질 관리가 대폭 강화되고 있습니다. 한국, 일본, 호주는 판매량 면에서는 여전히 소규모이지만, 프리미엄 가격 책정과 참신한 제형에서 강점을 보이고 있습니다. 중동 및 아프리카 및 남미에서도 소매 약국에 대한 접근성이 확대되고, 브랜드 일반의약품이 기존의 가정 요법 일부를 대체함에 따라 그 중요성이 커지고 있습니다. 이러한 시장들이 결합되어 기침 시럽 시장의 지리적 범위는 광범위하지만, 현재 아시아태평양이 가장 뚜렷한 성장세를 보이고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the cough syrup market size was valued at USD 4.46 billion in 2025 and is estimated to grow from USD 4.72 billion in 2026 to reach USD 6.27 billion by 2031, at a CAGR of 5.85% during the forecast period (2026-2031).

This report is Segmented by Product Type (Expectorants, Cough Suppressants, Combination Medications), Age Group (Pediatric, Adult, Geriatric), Prescription Type (Prescription, OTC), Cough Type (Dry Cough, Wet Cough), Distribution Channel (Retail, Hospital, Online Pharmacy), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are in Value (USD).

Global Cough Syrup Market Trends and Insights

Increasing Prevalence of Upper Respiratory Tract Infections

Upper respiratory tract infections remain one of the broadest demand anchors for the cough syrup market because they create a recurring need for short-cycle symptom relief across many age groups and income levels. Long-run age-standardized rates may have eased in some settings, but the absolute number of episodes has continued to rise with population growth, which keeps total treatment volumes elevated across the cough syrup market. The 2025 to 2026 flu season in the United States had already produced at least 47 million illnesses and 610,000 hospitalizations through April 2026, and that scale of seasonal illness continued to support high sell-through for cough and cold remedies. This pattern matters because the cough syrup market does not rely only on premiumization or channel gains, it also rests on a large and repeating disease burden that is difficult to displace. A further shift is that viral seasonality is becoming less predictable in some places, which may smooth annual demand but can also complicate inventory timing, promotions, and media spending for manufacturers. That makes the cough syrup market more dependent on supply responsiveness and retail execution rather than only on broad annual category growth.

Growing Preference for Over-the-Counter Cough Remedies

The cough syrup market continues to benefit from a clear consumer preference for self-managed care, especially for minor respiratory conditions that do not always require a physician visit. OTC products already held 60.52% share in 2025 and also carried the fastest forecast growth within prescription type, which shows that this part of the cough syrup market is expanding on both a scale and momentum basis. This shift reflects more than convenience because it also points to a practical move toward accessible, fast, and familiar symptom relief that fits how consumers now respond to everyday illness. In emerging markets, the same pattern is even more visible because pharmacy access often serves as the first point of care, which gives OTC cough syrups a frontline role in treatment behavior. In mature markets, the preference supports higher product variety, wider shelf depth, and faster repeat purchases, but it also gives private labels more room to grow if branded products do not maintain clear differentiation. The result is that the cough syrup market is seeing stronger volume support from consumer behavior itself, not only from new product launches or short-term cold and flu spikes.

Stringent Safety and Labeling Compliance for Active Ingredients

The cough syrup market is facing a tighter compliance environment because active ingredient scrutiny is now taking place across several large markets at the same time. The FDA proposed removing oral phenylephrine as a recognized nasal decongestant under OTC Monograph M012 in November 2024, and this pushed manufacturers to reassess relevant cold and cough combinations before the following season. The same FDA forecast also signaled continued review of pediatric cough and cold dosing, which raised the likelihood of further labeling and risk management requirements in products for younger children. In Australia, the Therapeutic Goods Administration reviewed dextromethorphan scheduling in 2024 and kept it pharmacy-only while still highlighting misuse concerns, which shows that regulatory caution is not limited to one region. These actions raise costs because reformulation, revalidation, relabeling, and relaunch work must often happen on existing products that were already commercially established. The effect is especially meaningful in the cough syrup market because smaller manufacturers may not have the technical and financial capacity to absorb repeated compliance cycles as easily as large branded players.

Other drivers and restraints analyzed in the detailed report include:

- Rising Popularity of Natural and Herbal Ingredients

- Expansion of E-Commerce and Online Pharmacy Access

- Misuse and Overuse Concerns, Especially in Pediatric Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cough suppressants or antitussives held 45.31% of revenue in 2025, giving them the largest product type position in the cough syrup market. Their lead rested on long-standing consumer familiarity with suppressant-led relief, especially where dextromethorphan-based products had built strong recognition over many years. That familiarity still matters at shelf level because buyers in the cough syrup market often make fast decisions based on known actives and familiar labels rather than extended comparison. Expectorants also retained an important place because guaifenesin continues to hold strong clinical and consumer recognition in wet cough treatment. This balance shows that the product structure of the cough syrup market is still anchored in established symptom categories even as newer formats expand around them.

Combination medications are projected to grow at 7.38% CAGR through 2031, which makes them the strongest advancing product group in the cough syrup market. Their rise reflects a clear move toward one product covering several symptoms, which reduces shelf complexity for retailers and simplifies choice for consumers. That shift is important because it turns dry cough syrup and wet cough syrup needs into a broader multi-symptom purchase occasion, which expands the practical role of combination products inside the cough syrup market. At the same time, regulatory reviews of certain actives are pushing manufacturers to use combination lines as reformulation vehicles, so these products increasingly serve both commercial and compliance goals. In the cough syrup industry, this gives combination formats a stronger strategic position because they can carry premium claims, support broader distribution, and respond more flexibly when single-ingredient products face pressure.

Adults accounted for 48.24% share in 2025, which made them the largest age cohort in the cough syrup market. This position was supported by high self-medication rates, frequent workplace-driven convenience purchases, and strong brand recall among working-age consumers. Adult buyers also form the core audience for premium non-drowsy, sugar-free, and alcohol-free products, which means the cough syrup market draws a significant share of its value from feature-led purchases in this group. That matters because adult demand is not only broad, it is also commercially attractive due to higher repeat purchases and willingness to pay for convenience-oriented benefits. The geriatric segment remains smaller, but it is gaining relevance as aging populations in Europe and Japan increase demand for respiratory symptom management that is more guided, repeatable, and brand loyal.

Pediatrics is forecast to expand at 6.52% CAGR through 2031, which places it as the fastest-growing age group in the cough syrup market despite the stricter risk environment. Growth is being supported by long-term investment in palatability, clearer dosing formats, and reduced reliance on higher-risk active ingredient profiles. That creates an uneven but important opening because the cough syrup market can still grow in children when products meet tighter expectations around safety, usability, and taste. This is why child-focused innovation is becoming more format-specific and compliance-led rather than simply extending adult syrups into smaller doses. In the cough syrup industry, companies that stay invested in pediatric formulations with stronger safety positioning are more likely to keep access as regulatory scrutiny continues to rise.

Complete Report Scope:

- By Product Type

- Expectorants

- Cough Suppressants/Antitussives

- Combination Medications

- By Age Group

- Pediatric

- Adult

- Geriatric

- By Prescription Type

- Prescription

- Over-the-Counter

- By Cough Type

- Dry Cough

- Wet Cough

- By Distribution Channel

- Retail Pharmacy

- Hospital Pharmacy

- Online Pharmacy

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 36.52% of the cough syrup market share in 2025, which gave it the leading regional position in the report. The region benefits from strong OTC consumer habits, deep pharmacy coverage, and high brand recognition for established respiratory relief products. In the United States, the 2025 to 2026 flu season had reached at least 47 million illnesses and 610,000 hospitalizations through April 2026, which supported heavy seasonal demand for cough and cold products. Canada and Mexico remain smaller contributors, but both continue to benefit from pharmacy network reach and steady self-medication behavior. This combination keeps North America central to the cough syrup market because it offers both volume stability and strong branded product economics.

Europe remains a major region for the cough syrup market, especially across dry cough syrup and wet cough syrup categories where herbal adoption and OTC familiarity are both well developed. Germany holds the largest national share within Europe, supported by a mature consumer healthcare base and a well-established herbal medicines infrastructure. EU herbal monographs have helped make Europe the most commercially active region for botanical cough formulations, and Reckitt reported that its Strepsils Cough Dual Action range reached market leadership across 15 EU markets. France, the United Kingdom, Italy, and Spain also contribute meaningful revenue, though consumer preferences differ by formulation style and natural ingredient appeal. The region remains important to the cough syrup market because it combines regulatory support for herbal innovation with strong consumer willingness to try differentiated formulations.

Asia-Pacific represents the fastest-growing regional component of cough syrup market size, with a 7.45% CAGR projected through 2031. India and China are the main volume engines because large populations, better pharmacy access, and broader digital health use continue to lift demand. China's 2024 reclassification of dextromethorphan changed the balance of OTC suppressant products and now favors portfolios with non-DXM alternatives. India adds growth through rising self-medication and a larger elderly population, but quality oversight has tightened sharply after the 2025 contaminated cough syrup events. South Korea, Japan, and Australia remain smaller in volume but stronger in premium pricing and novel delivery formats. The Middle East and Africa, along with South America, are also gaining relevance as retail pharmacy access expands and branded OTC products displace some traditional home remedies. Together, these markets keep the cough syrup market geographically broad, but Asia-Pacific now carries the clearest growth momentum.

- Abbott Laboratories

- Aurobindo Pharma

- Bayer

- Cipla

- Dr. Reddy's Laboratories

- Haleon plc

- Hikma Pharmaceuticals

- Kenvue Inc.

- Lupin

- Opella Healthcare Group

- Prestige Consumer Healthcare

- Procter and Gamble Company

- Reckitt Benckiser Group

- Sun Pharmaceuticals Industries

- Torrent Pharmaceuticals Limited

- Wockhardt Limited

- Zydus Lifesciences Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Upper Respiratory Tract Infections

- 4.2.2 Growing Preference for Over-the-Counter Cough Remedies

- 4.2.3 Rising Popularity of Natural and Herbal Ingredients

- 4.2.4 Expansion of E-Commerce and Online Pharmacy Access

- 4.2.5 Pediatric-First Formulation Innovation and Palatability Engineering

- 4.2.6 Non-Drowsy, Sugar-Free, and Alcohol-Free Product Differentiation

- 4.3 Market Restraints

- 4.3.1 Stringent Safety and Labeling Compliance for Active Ingredients

- 4.3.2 Misuse and Overuse Concerns, Especially in Pediatric Use

- 4.3.3 Price Pressure From Generic and Private-Label Competition

- 4.3.4 API and Packaging Supply Volatility in Oral Liquid Formulations

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Expectorants

- 5.1.2 Cough Suppressants/Antitussives

- 5.1.3 Combination Medications

- 5.2 By Age Group

- 5.2.1 Pediatric

- 5.2.2 Adult

- 5.2.3 Geriatric

- 5.3 By Prescription Type

- 5.3.1 Prescription

- 5.3.2 Over-the-Counter

- 5.4 By Cough Type

- 5.4.1 Dry Cough

- 5.4.2 Wet Cough

- 5.5 By Distribution Channel

- 5.5.1 Retail Pharmacy

- 5.5.2 Hospital Pharmacy

- 5.5.3 Online Pharmacy

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Aurobindo Pharma Limited

- 6.3.3 Bayer AG

- 6.3.4 Cipla Limited

- 6.3.5 Dr. Reddy's Laboratories Ltd.

- 6.3.6 Haleon plc

- 6.3.7 Hikma Pharmaceuticals PLC

- 6.3.8 Kenvue Inc.

- 6.3.9 Lupin Limited

- 6.3.10 Opella Healthcare Group

- 6.3.11 Prestige Consumer Healthcare Inc.

- 6.3.12 Procter and Gamble Company

- 6.3.13 Reckitt Benckiser Group plc

- 6.3.14 Sun Pharmaceutical Industries Limited

- 6.3.15 Torrent Pharmaceuticals Limited

- 6.3.16 Wockhardt Limited

- 6.3.17 Zydus Lifesciences Limited

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment