|

시장보고서

상품코드

2073009

천연 바닐린 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Natural Vanillin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

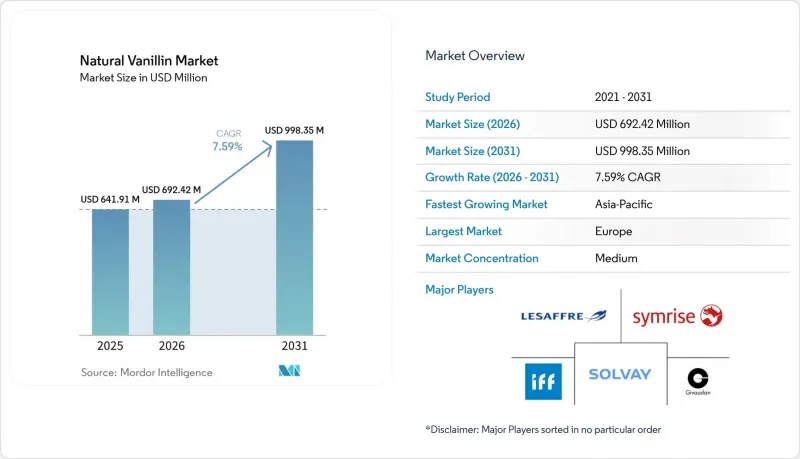

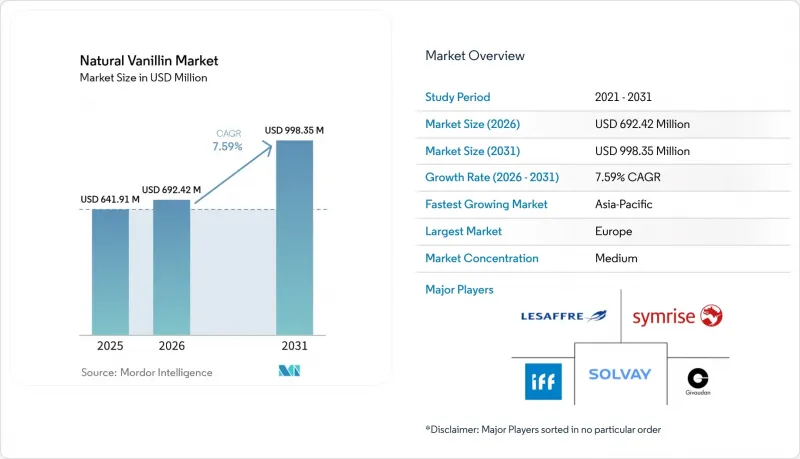

Mordor Intelligence에 의하면, 천연 바닐린 시장 규모는 2025년 6억 4,190만 달러, 2026년 6억 9,240만 달러에서 2031년까지 9억 9,840만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 7.6%를 나타낼 전망입니다.

본 보고서는 원료별(바닐라빈 추출물, 오이게놀 합성, 페룰산 합성, 기타), 용도별(식품 및 음료, 의약품, 화장품 및 퍼스널케어, 향료), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계 천연 바닐린 시장 동향 및 분석

클린 라벨 및 천연 원료에 대한 수요 증가

주요 식품 및 퍼스널케어 기업들은 현재 클린 라벨 전략을 표준 조달 요건으로 간주하고 있으며, 과거의 "프리미엄 브랜드의 차별화 요인"이라는 인식에서 점차 벗어나고 있습니다. EU 규정(EC) No 1334/2008 및 FDA 21 CFR 101.22(a)(3)에 따라, 바닐라 빈에서 유래되었는지 또는 생물학적 발효를 통해 생산되었는지 여부와 관계없이 바닐린은 "천연 향료"로 인정받고 있습니다. 이러한 분류를 통해 순수한 바닐라 추출물을 조달하는 경우에 비해, 적은 비용으로 제품 라벨의 매력을 높일 수 있습니다. 2026년 3월, 라레망드 바이오 인그리디언츠(Lalemand Bio-Ingredients)사는 2023년부터 2025년까지 바닐라를 주원료로 한 식품 및 음료 신제품이 전 세계적으로 급증하고 있다고 지적했습니다. 베이커리, 유제품, 과자, 초콜릿 등 각 분야에서 뚜렷하게 나타나는 이러한 추세는 제품 배합에 대한 대대적인 재검토가 진행되고 있음을 보여줍니다. 종종 간과되기 쉬운 비즈니스적 인사이트 중 하나는 합성 바닐린에서 천연 바닐린으로 전환하면 표시 기준을 준수할 수 있을 뿐만 아니라, 제과 및 유제품 제조업체가 더 높은 소매 가격을 책정할 수 있게 된다는 점입니다. 이러한 가격 프리미엄은 원자재 비용의 차이를 메우는 데 도움이 되며, 조달 부서에게 설득력 있는 근거가 됩니다. 또한, 천연 바닐린이 지닌 '클린 라벨'의 매력에 대한 수요는 화장품 및 퍼스널케어 분야에서도 점점 더 커지고 있습니다. 이 분야에서는 젊은 소비자들이 원재료의 투명성을 중요하게 여기며, 구매 결정 시 이를 제품의 성능과 동등한 수준으로 간주하고 있습니다.

인공 성분에 대한 규제상의 제약

바닐린 시장에서 천연 유래와 합성 유래의 구분은 상업적으로 큰 의미를 지닙니다. EU 규정(EC) 제1334/2008호에 따르면, 천연 향료 물질은 식물, 동물 또는 미생물 유래 원료로부터 물리적, 효소적 또는 미생물학적 방법만을 통해 추출되어야 합니다. 이 정의에 따라, 구아이아콜을 원료로 한 합성 바닐린이 유럽 시장에서 "천연"이라고 표시되는 것은 사실상 금지되어 있습니다. 규제가 더욱 강화되면서, 2025년 6월 12일 유럽집행위원회는 EU 생산자들에게 피해를 입힌 불공정한 가격 책정 관행을 이유로, 중국산 바닐린 수입에 대해 131.1%라는 높은 반덤핑 관세를 부과했습니다. 이 조치는 EU 식품 제조 업계에서 합성 바닐린과 "천연" 인증 바닐린의 비용 격차를 줄이는 것은 물론, 특히 기존에는 중국의 합성 바닐린 공급에 의존하던 제품의 경우, 바이오 유래 대체재의 매력을 높이는 데에도 기여할 것입니다. 또한, 유럽의 식품 가공업체에 제품을 공급하는 아시아 제조업체들은 중국산 수입품에 부과되는 관세로 인해 원가 상승에 직면해 있습니다. 이러한 인플레이션 압력은 EU의 규제 체계에 따라, "천연" 인증된 바닐린을 조달하도록 독려하고 있습니다.

합성 바닐린에 비해 훨씬 높은 비용

천연 바닐린이 시장에 보급되는 데에는 합성 대체품과의 가격 차이라는 큰 장벽이 있습니다. GDCh(독일화학자협회)의 의견서에 따르면, 바닐라 빈에서 추출되는 천연 바닐린의 가격은 화학적으로 합성된 것보다 500배에서 1,000배 더 비싸다고 합니다. 또한, 발효를 통해 생산되는 "천연" 바닐린은 구아이아콜을 원료로 한 합성 제품에 비해 가격이 약 10배 정도 비쌉니다. 이러한 현저한 가격 차이로 인해 천연 바닐린의 사용은 장인의 솜씨가 돋보이는 초콜릿, 고급 퍼스널케어 제품, 프리미엄 음료의 배합 등 프리미엄 제품군으로 한정되어 있습니다. 반면, 주요 제과점 및 음료 제조업체들은 주로 합성 등급의 바닐린을 선택하고 있습니다. 이러한 상황은 구조적인 위험을 초래하고 있습니다. 즉, 이미 다양한 비용 측면에서 인플레이션 압박에 시달리고 있는 중견 브랜드 소유주들은 생산 규모 확대에 따라 비용 격차가 줄어들지 않는 한, 클린 라벨을 위한 제품 재조성 노력을 미룰 가능성이 높습니다. 이러한 가격 차이를 해소하기 위한 주목할 만한 노력으로는 보레가드(Boregard)사의 살프스보르그(Sarpusborg)에서 진행 중인 약 8억 노르웨이 크로네 규모의 생산 능력 확대 프로젝트와, 라레만드(Lalemand)사의 상업용 발효 생산 확대 등이 있습니다. 그러나 합성 생산과의 완전한 비용 평형을 달성하는 것은 당장의 현실이라기보다는 여전히 먼 목표로 남아 있습니다.

부문별 분석

2025년, 바닐라빈 추출물은 천연 바닐린 시장에서 46.71%의 점유율을 차지하며, 풍미 품질 및 원산지 측면에서 기준이 되는 위상을 유지했습니다. 고급 과자, 하이엔드 향수, 프리미엄 유제품 분야에서 그 존재감은 여전히 강력합니다. "바닐라 맛" 혹은 "천연 바닐라 향"과 같은 용어를 콩 유래 원료로만 제한하는 EU 및 미국의 표시 규정은 발효를 통해 만든 대체품으로는 대체할 수 없는 규제상의 틈새를 만들어내고 있습니다. 그러나 이 부문은 공급원이 마다가스카르에 의존하고 있으며, 비용 구조상의 제약으로 인해 프리미엄 용도로의 사용이 제한되어 있어 여러 과제에 직면해 있습니다. 정향 오일에서 추출한 오이게놀을 미생물을 이용한 산화법으로 변환하는 "오이게놀 합성"은 중간 수준에 위치하고 있습니다. 이 제품은 일관되게 높은 순도를 얻을 수 있어 의약품 분야에서 또한 독특한 향기 프로파일을 지니고 있어 고급 향수 분야에서 선호되고 있습니다.

페룰라산 합성은 2026년부터 2031년까지 연평균 성장률(CAGR) 9.96%를 기록하며, 가장 빠르게 성장하고 있는 공급원입니다. 이러한 성장은 확장성, 농업 원료의 확보 가능성, 그리고 EU 규정(EC) No 1334/2008 및 FDA 21 CFR 101.22(a)(3)에 근거한 "천연" 표시로서의 인증에 힘입어 성장하고 있습니다. ScienceDirect의 『Biochemical Engineering Journal』에 게재된 2024년 총설에서는 곡물 작물에 풍부하게 함유되어 있으며 생물학적 전환을 통한 수율도 입증된 바와 같이, 페룰산이 천연 바닐린의 전구체로서 유망하다는 점이 강조되었습니다. 중국, 인도, 태국, 인도네시아에서 널리 구할 수 있는 쌀겨유 가공 잔여물은 비용 대비 효과가 높은 원료가 되어, 아시아태평양의 쌀 가공 경제권에서 페룰산 유래 바닐린 생산의 입지를 다지고 있습니다. 발효 기술의 선두주자인 프랑스의 Ennolys사는 바이오전환 발효를 이용하여 쌀겨유에서 천연 바닐린 "Ennallin"을 생산하고 있으며, 순도 99% 이상을 달성함과 동시에 EU 및 미국의 천연 유래 기준을 완벽하게 충족하고 있습니다. 리그닌의 해중합이나 바닐라와 유사한 식물에서 추출하는 등 다른 공급원은 규모는 작지만, 목재를 원료로 한 공동 생산이 경쟁력 있는 생산 경제성을 가져다주는 스칸디나비아의 바이오 정유 공장에서 전략적으로 중요한 위치를 차지하고 있습니다.

지역별 분석

2025년, 유럽은 천연 바닐린 시장에서 36.40%라는 압도적인 점유율을 차지하고 있으며, 이는 견조한 프리미엄 수요, 명확한 규제 체계, 그리고 강력한 현지 생산 능력에 힘입은 결과입니다. 천연 향료의 지위에 대한 명확한 상업적 가치를 인정하는 EU 규정(EC) 제1334/2008호는 생산자들이 해당 지역의 엄격한 천연 향료 물질 정의에 부합하는 데 도움이 되고 있습니다. 또한, 2025년 6월에 시행된 중국산 바닐린에 대한 반덤핑 조치로 인해 유럽 식품 제조 업계에서 합성 수입품의 가격 경쟁력이 약화되었습니다. 독일, 프랑스, 네덜란드는 고급 과자, 베이커리, 향수 시장이 확고한 기반을 다지고 있어 중요한 수요 거점으로 두각을 나타내고 있습니다. 또한, 프랑스의 Ennolys나 노르웨이의 Borregaard와 같은 대형 생산 기업들이 해당 지역의 규제 상황과 지속가능성 동향에 능숙하게 대응하고 있는 점도 유럽의 우위를 더욱 공고히 하고 있습니다.

아시아태평양은 급속히 부상하고 있으며, 이 지역의 천연 바닐린 시장은 고급 식품 제조의 급증과 원재료 투명성에 대한 인식 제고를 배경으로 2026년부터 2031년까지 연평균 성장률(CAGR) 9.98%로 확대될 것으로 전망됩니다. 중국은 합성 바닐린의 주요 생산국일 뿐만 아니라, 특히 고급 가공식품 및 음료 분야에서 천연 바닐린의 소비국으로서도 점점 더 중요한 역할을 하고 있습니다. 한편, 인도는 쌀겨공급 능력을 활용해 페룰라산 생산 및 클린 라벨 제품 개발을 추진하는 등 주요 주자로 부상하고 있습니다. 일본에서는 고급 과자에 대한 꾸준한 수요와 원재료의 투명성에 대한 높은 인식에 힘입어 천연 바닐린의 매출이 증가 추세를 보이고 있습니다. 또한 인도네시아, 태국, 한국 등의 국가들이 특히 음료 및 화장품 분야에서 2차 성장을 주도하고 있어, 천연 바닐린 시장에서 해당 지역의 입지를 더욱 공고히 하고 있습니다.

북미는 막대한 식품 생산 능력과 프리미엄 맛 및 향에 대한 꾸준한 수요가 맞물려 매우 중요한 역할을 하고 있습니다. 그러나 해당 지역에서는 특히 발효 유래 제품에서 바닐라 특유의 용어와 관련된 표시상의 복잡성에 직면해 있어, 브랜딩 전략을 수립하는 데 어려움을 겪고 있습니다. 남미에서는 브라질이 주도적인 역할을 하고 있으며, 호황을 누리고 있는 고급 식품 가공 부문 덕분에 이 지역의 천연 바닐린 시장에 있어 가장 유망한 성장 경로를 보여주고 있습니다. 한편, 중동 및 아프리카는 규모는 작지만, 광범위한 국내 제품보다는 수입된 고급 소비재나 특정 의약품 용도에 수요가 집중되어 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the natural vanillin market size is projected to expand from USD 641.9 million in 2025 and USD 692.4 million in 2026 to USD 998.4 million by 2031, registering a CAGR of 7.6% between 2026 and 2031.

This report is Segmented by Source (Vanilla Bean Extract, Eugenol Synthesis, Ferulic Acid Synthesis, and Other Sources), Application (Food and Beverages, Pharmaceuticals, Cosmetics and Personal Care, and Fragrances), and Geography (North America, Europe, Asia Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Natural Vanillin Market Trends and Insights

Rising clean-label and natural ingredient demand

Leading food and personal care companies now view clean-label positioning as a standard procurement requirement, moving away from its previous status as a premium brand differentiator. Under EU Regulation (EC) No 1334/2008 and FDA 21 CFR 101.22(a)(3), vanillin, whether sourced from vanilla beans or produced through bio-fermentation, qualifies as a "natural flavoring". This classification allows for product label enhancements at a fraction of the cost of procuring full vanilla extract. In March 2026, Lallemand Bio-Ingredients highlighted a surge in global food and beverage launches featuring vanilla from 2023 to 2025. This trend, evident in the bakery, dairy, confectionery, and chocolate sectors, points to a significant reformulation movement. The often-overlooked commercial insight is that shifting from synthetic to natural vanillin not only ensures label compliance but also empowers confectionery and dairy producers to command a higher retail price. This price premium helps bridge the gap in ingredient costs, presenting a compelling case for procurement teams. Furthermore, the demand for natural vanillin's clean-label appeal is gaining momentum in the cosmetics and personal care sectors. Here, younger consumers prioritize ingredient transparency, equating it with product performance in their purchasing decisions.

Regulatory restrictions on artificial ingredients

In the vanillin market, the distinction between natural and synthetic sources carries significant commercial weight. According to EU Regulation (EC) No 1334/2008, natural flavoring substances must be derived solely through physical, enzymatic, or microbiological methods from vegetable, animal, or microbiological sources. This definition effectively bars guaiacol-based synthetic vanillin from being labeled as "natural" in European markets. Further tightening the screws, on June 12, 2025, the European Commission slapped a hefty 131.1% anti-dumping duty on vanillin imports from China, citing unfair pricing practices that harmed EU producers. This move not only narrows the cost disparity between synthetic and naturally-certified vanillin in the EU's food manufacturing sector but also boosts the appeal of bio-based alternatives, especially for formulations that traditionally relied on Chinese synthetic supplies. Additionally, Asian manufacturers supplying to European food processors now grapple with heightened costs due to the duties on Chinese imports. This inflationary pressure nudges them towards sourcing naturally certified vanillin, aligning with the EU's regulatory framework.

Significantly higher cost compared to synthetic vanillin

Mass-market adoption of natural vanillin faces a significant hurdle: its cost compared to synthetic alternatives. According to a position paper by GDCh (Gesellschaft Deutscher Chemiker), natural vanillin sourced from vanilla beans is priced at 500 to 1,000 times more than its chemically synthesized counterparts. Furthermore, "natural" vanillin produced through fermentation commands a price that's roughly 10 times higher than the guaiacol-based synthetic versions. This pronounced cost disparity limits the use of natural vanillin to premium product tiers, such as artisanal chocolates, luxury personal care items, and high-end beverage formulations. In contrast, mainstream bakery and beverage producers predominantly opt for synthetic grades. This situation poses a structural risk: mid-market brand owners, already squeezed by inflationary pressures on various costs, are likely to postpone their clean-label reformulation efforts unless the cost gap narrows through increased production scale. Notable efforts to bridge this premium include Borregaard's ~NOK 800 million debottlenecking project in Sarpsborg and Lallemand's ramp-up in commercial fermentation. However, achieving full cost parity with synthetic production remains a distant goal rather than an immediate reality.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in fermentation-based vanillin production technologies

- Sustainability advantages of bio-based vanillin production

- Volatility in the supply of natural raw materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Vanilla Bean Extract held a 46.71% share of the natural vanillin market, maintaining its status as the benchmark for flavor quality and origin. Its presence in luxury confectionery, high-end fragrances, and premium dairy products remains strong. EU and US labeling laws, which reserve terms like "vanilla flavor" and "natural vanilla flavoring" for bean-derived ingredients, create a regulatory niche that fermentation alternatives cannot replace. However, this segment faces constraints due to reliance on Madagascar for supply and a cost structure limiting its use to premium applications. Eugenol Synthesis, which converts eugenol from clove oil through oxidative microbial methods, occupies a mid-tier position. It is preferred in pharmaceuticals for its consistent high purity and in fine fragrances for its unique aromatic profiles.

Ferulic Acid Synthesis is the fastest-growing source, with a 9.96% CAGR from 2026 to 2031. This growth is driven by its scalability, agricultural feedstock availability, and recognition as a natural label under EU Regulation (EC) No 1334/2008 and FDA 21 CFR 101.22(a)(3). A 2024 review in ScienceDirect's Biochemical Engineering Journal highlighted ferulic acid's viability as a natural vanillin precursor due to its abundance in cereal crops and proven bioconversion yields. Rice bran oil processing residues, widely available in China, India, Thailand, and Indonesia, provide a cost-effective feedstock, positioning ferulic acid vanillin production within the Asia-Pacific's rice processing economies. French fermentation leader Ennolys produces Ennallin natural vanillin from rice bran oil using bioconversion fermentation, achieving over 99% purity and full EU and US natural status. Other Sources, such as lignin depolymerization and extraction from vanilla-adjacent botanicals, remain smaller but hold strategic importance in Scandinavian biorefineries, where wood-based co-production offers competitive production economics.

Complete Report Scope:

- Source

- Vanilla Bean Extract

- Eugenol Synthesis

- Ferulic Acid Synthesis

- Other Sources

- Application

- Food and Beverages

- Bakery and Confectionery

- Beverages

- Dairy

- Other Food and Beverages

- Pharmaceuticals

- Cosmetics and Personal Care

- Fragrances

- Food and Beverages

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Peru

- Chile

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Geography Analysis

In 2025, Europe commanded a dominant 36.40% share of the natural vanillin market, bolstered by robust premium demand, clear regulatory frameworks, and strong local production capabilities. The EU's Regulation (EC) No 1334/2008, which bestows a clear commercial value to natural flavor status, aids producers in aligning with the region's stringent definitions of natural flavoring substances. Furthermore, an anti-dumping measure in June 2025 targeted Chinese vanillin, curbing the pricing edge of synthetic imports in Europe's food manufacturing sector. Germany, France, and the Netherlands stand out as pivotal demand hubs, thanks to their well-entrenched premium confectionery, bakery, and fragrance markets. Adding to Europe's advantage are production leaders like France's Ennolys and Norway's Borregaard, both adeptly navigating the region's regulatory and sustainability landscape.

Asia-Pacific is on a rapid ascent, with the region's natural vanillin market projected to expand at a 9.98% CAGR from 2026 to 2031, driven by a surge in premium food manufacturing and heightened awareness of ingredient transparency. China finds itself in a dual role: a significant producer of synthetic vanillin and an increasingly prominent consumer of natural vanillin, especially in its premium processed food and beverage sector. Meanwhile, India is emerging as a key player, leveraging its rice bran availability for ferulic acid production and clean-label product development. Japan's natural vanillin sales are on the rise, fueled by a robust demand for premium confectionery and a keen sensitivity to ingredient transparency. Additionally, countries like Indonesia, Thailand, and South Korea are driving secondary growth, particularly in beverages and cosmetics, further solidifying the region's foothold in the natural vanillin market.

North America plays a pivotal role, merging vast food manufacturing capabilities with a deep-rooted demand for premium flavors and fragrances. However, the region grapples with complexities in labeling, especially concerning vanilla-specific terminology in fermentation-derived products, complicating branding strategies. In South America, Brazil takes the lead, presenting the region's most promising growth avenue for the natural vanillin market, thanks to its thriving premium food processing sector. Meanwhile, the Middle East and Africa, though smaller in scale, see concentrated demand in imported premium consumer goods and select pharmaceutical applications, rather than widespread domestic formulations.

- Givaudan SA

- Symrise AG

- International Flavors & Fragrances Inc. (IFF)

- Solvay SA

- Lesaffre Group (Lesaffre et Compagnie SA)

- MANE SA (V. MANE FILS SA)

- Sensient Technologies Corporation

- Kerry Group plc

- Takasago International Corporation

- Robertet SA

- Borregaard ASA

- Evolva Holding SA

- Camlin Fine Sciences Limited

- Conagen, Inc.

- Treatt plc

- Axxence Aromatic GmbH

- Aurochemicals Private Limited

- Advanced Biotech, LLC

- De Monchy Aromatics B.V.

- Synergy Flavors, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Clean-Label and Natural Ingredient Demand

- 4.2.2 Regulatory Restrictions on Artificial Ingredients

- 4.2.3 Growth in Premium Food, Beverage, and Fine Fragrance Formulations

- 4.2.4 Sustainability Advantages of Bio-Based Vanillin Production

- 4.2.5 Advancements in Fermentation-Based Vanillin Production Technologies

- 4.2.6 Increasing Adoption in Premium Confectionery and Chocolate Products

- 4.3 Market Restraints

- 4.3.1 Significantly Higher Cost Compared to Synthetic Vanillin

- 4.3.2 Volatility in the supply of Natural Raw Materials

- 4.3.3 Stringent Regulatory Definitions for "Natural" Claims

- 4.3.4 Flavor Consistency Challenges Across Natural Sources

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Source

- 5.1.1 Vanilla Bean Extract

- 5.1.2 Eugenol Synthesis

- 5.1.3 Ferulic Acid Synthesis

- 5.1.4 Other Sources

- 5.2 Application

- 5.2.1 Food and Beverages

- 5.2.1.1 Bakery and Confectionery

- 5.2.1.2 Beverages

- 5.2.1.3 Dairy

- 5.2.1.4 Other Food and Beverages

- 5.2.2 Pharmaceuticals

- 5.2.3 Cosmetics and Personal Care

- 5.2.4 Fragrances

- 5.2.1 Food and Beverages

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Sweden

- 5.3.2.7 Belgium

- 5.3.2.8 Poland

- 5.3.2.9 Netherlands

- 5.3.2.10 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Thailand

- 5.3.3.5 Singapore

- 5.3.3.6 Indonesia

- 5.3.3.7 South Korea

- 5.3.3.8 Australia

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Peru

- 5.3.4.5 Chile

- 5.3.4.6 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 South Africa

- 5.3.5.3 Saudi Arabia

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 Morocco

- 5.3.5.7 Turkey

- 5.3.5.8 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles

- 6.4.1 Givaudan SA

- 6.4.2 Symrise AG

- 6.4.3 International Flavors & Fragrances Inc. (IFF)

- 6.4.4 Solvay SA

- 6.4.5 Lesaffre Group (Lesaffre et Compagnie SA)

- 6.4.6 MANE SA (V. MANE FILS SA)

- 6.4.7 Sensient Technologies Corporation

- 6.4.8 Kerry Group plc

- 6.4.9 Takasago International Corporation

- 6.4.10 Robertet SA

- 6.4.11 Borregaard ASA

- 6.4.12 Evolva Holding SA

- 6.4.13 Camlin Fine Sciences Limited

- 6.4.14 Conagen, Inc.

- 6.4.15 Treatt plc

- 6.4.16 Axxence Aromatic GmbH

- 6.4.17 Aurochemicals Private Limited

- 6.4.18 Advanced Biotech, LLC

- 6.4.19 De Monchy Aromatics B.V.

- 6.4.20 Synergy Flavors, Inc.