|

시장보고서

상품코드

2073011

혈액 투석 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Hemodialysis Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

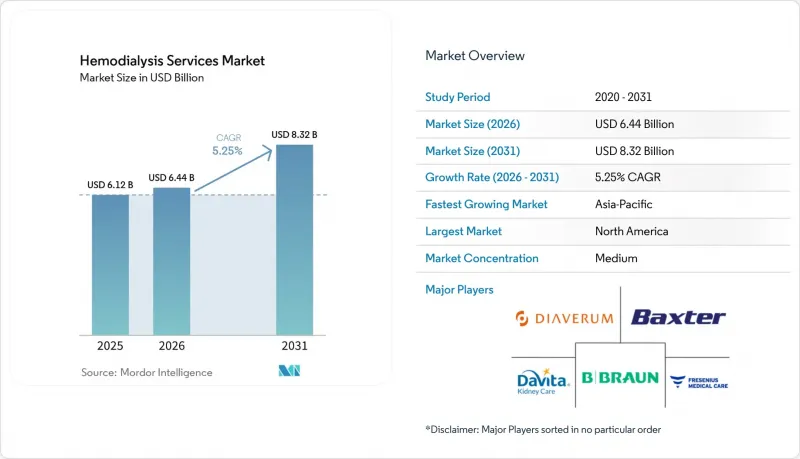

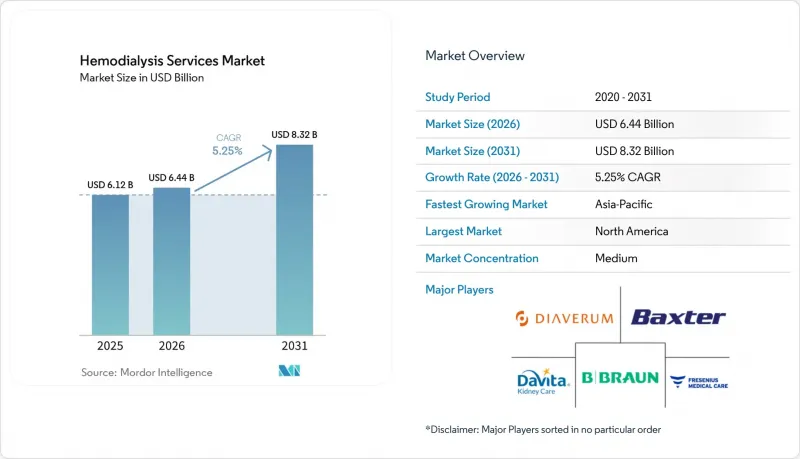

Mordor Intelligence에 의하면, 혈액 투석 서비스 시장 규모는 2025년에 61억 2,000만 달러로 평가되었고 2026년 64억 4,000만 달러에서 2031년까지 83억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.25%를 나타낼 전망입니다.

본 보고서는 서비스 유형(시설 내 혈액 투석, 재택 혈액 투석, 야간 혈액 투석, 기타), 최종 사용자(투석 센터, 병원, 재택 간호 시설, 기타), 적응증(만성 신장병, 급성 신장 감염증, 패혈증성 쇼크, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 혈액 투석 서비스 시장 동향 및 인사이트

말기 신부전(ESRD)의 부담 증가와 만성 신장 질환(CKD)의 진행

혈액 투석 서비스 시장은 결국 말기 신부전(ESRD)으로 진행되어 지속적인 신장 대체 요법이 필요한 만성 신장 질환(CKD) 환자 증가에 힘입어 성장하고 있습니다. 2024년 브라질 투석 조사에 따르면, 투석을 받고 있는 환자 수는 17만 2,585명에 달했으며, 이는 지난 10년간 55%에 가까운 증가율을 보인 것으로, 대규모 치료 시스템 전반에 걸쳐 환자 수가 지속적으로 증가하고 있는 실태가 드러났습니다. 이 조사에서 만성 신장 질환의 원인 중 당뇨병과 고혈압이 각각 29%를 차지하는 것으로 밝혀졌습니다. 이는 투석 수요가 단발적인 임상적 사례가 아니라, 여전히 일반적인 장기적인 대사성 질환에 기인하고 있음을 보여줍니다. 이 점은 중요합니다. 왜냐하면, 질환이 상당히 진행된 단계에서 치료를 시작하는 환자는 더 복잡한 치료, 더 치밀한 임상적 감독, 그리고 더 장기간에 걸친 치료 지속이 필요한 경우가 많으며, 이 모든 것이 환자 한 명 한 명을 돌보는 데 드는 서비스 부담을 증가시키기 때문입니다. 혈액 투석 서비스 시장은 말기 신부전(ESRD)이 단기적인 질환이 아니라는 사실에서도 혜택을 보고 있습니다. 따라서 신규 환자 증가는 즉시 이탈하는 것이 아니라, 지속적인 치료 환자 수로 누적되는 경향이 있습니다. 그 결과, 만성 신장 질환(CKD)의 유병률 증가는 단순히 환자 기반을 확대할 뿐만 아니라, 보다 안정적인 이용률, 예측 가능한 일정 관리, 그리고 고도의 치료를 제공할 수 있는 의료 기관의 경우 수익 전망 개선으로도 이어집니다.

메디케어 및 전국 투석 보상 범위 확대

시설 운영은 안정적인 지급 규정과 빈번한 치료비 청구에 크게 의존하고 있기 때문에 환급 지원은 여전히 혈액 투석 서비스 시장의 가장 뚜렷한 성장 요인 중 하나입니다. 2026 회계연도 ESRD 전향적 지불 시스템(PPS) 최종 규정에 따라, 메디케어의 기본 단가는 1회 치료당 281.71달러로 인상되었으며, 이는 2025년 대비 7.89달러 증가한 금액입니다. 또한 CMS는 모든 ESRD 시설에 대한 총 지급액이 2.2% 증가할 것으로 전망하고 있으며, 독립형 센터는 2.2% 증가, 병원 내 시설은 1.5% 증가할 것으로 예측됩니다. 이는 대규모 외부 네트워크를 뒷받침하는 결제 역량을 입증하는 것입니다. 또한, 본 규정에서는 재택 및 자가 투석에 대한 추가 교육비 지급 조정을 2026년까지 연장하는 한편, 급성 신장 손상(AKI)의 투석 지급률을 281.71달러로 통일했습니다. 이를 통해 클리닉 외부에서의 치료에 대한 자금 지원의 길이 넓어질 것입니다. 이러한 지원이 있음에도 불구하고, ‘말기 신부전 치료 선택지 모델’ 프로그램의 조기 종료는 인력 배치, 환자 교육, 인프라가 여전히 시행을 제한하고 있는 상황에서 지급 인센티브만으로는 돌봄 모델이 자동으로 전환되지 않는다는 점을 보여줍니다. 따라서 혈액 투석 서비스 시장은 보험 적용 범위 확대로 인한 혜택을 지속적으로 누리고 있지만, 사업자 입장에서는 해당 자금을 ESRD 품질 인센티브 프로그램에 기반한 임상 역량 및 규정 준수 실적과 연계해야 할 필요성이 여전히 요구되고 있습니다.

높은 노동 집약성과 간호사 부족으로 인한 압박

혈액 투석 서비스 시장에 있어 가장 뿌리 깊은 걸림돌은 치료 제공 과정의 노동 집약성입니다. 왜냐하면 투석 치료는 여전히 전문 간호사, 신장내과 전문의, 기술 직원, 그리고 엄격한 감독 체계에 의존하고 있기 때문입니다. 2024년 미국의 신장내과 펠로우십 정원 충족률은 66%에 그쳤으며, 이는 환자 수요가 계속 증가하는 반면 인력 공급 부족이라는 문제를 안고 있음을 보여줍니다. 미국 의료 인력 분석 센터(National Center for Health Workforce Analysis)의 예측에 따르면, 2037년까지 신장 전문의가 21% 부족하고, 2027년까지 간호사가 10% 부족할 것으로 예상되며, 지방 지역에서는 의료 서비스 공백이 발생할 위험이 더욱 높아지고 있습니다. 시설에서 교대 근무 인력 배치, 환자에 대한 지도, 또는 필요한 감독 비율을 유지하지 못할 경우, 새로운 투석 의자의 가동 능력을 충분히 활용할 수 없게 되므로, 이러한 인력 부족은 심각한 문제가 됩니다. 원격의료나 전문 의료진은 어느 정도 도움이 되지만, 메디케어의 대면 진료 요건으로 인해 이러한 해결책이 일상적인 이용에서 어느 정도까지 확대될 수 있는지는 여전히 제한을 받고 있습니다. 따라서 혈액 투석 서비스 시장은 수요가 견조함에도 불구하고, 인력 부족으로 인해 사업자가 그 수요를 실제 치료 건수로 전환하는 속도가 둔화되면서 실질적인 한계에 직면해 있습니다.

부문별 분석

2025년 기준으로, 서비스 유형별 혈액 투석 서비스 시장 점유율의 85.31%를 시설 내 혈액 투석이 차지하고 있으며, 이는 수익 기반이 여전히 클리닉에서의 치료 제공에 얼마나 크게 의존하고 있는지를 보여줍니다. 이 부문이 여전히 지배적인 위치를 유지하고 있는 이유는 투석 센터가 여러 가지 동반 질환을 앓고 있는 많은 환자들이 여전히 정기적으로 필요로 하는 투석 장비, 훈련을 받은 임상 직원, 수처리 시스템 및 응급 상황 시의 모니터링 체계를 제공하고 있기 때문입니다. 혈액 투석 서비스 시장이 여전히 시설 내 치료에 치우쳐 있는 이유는 이러한 시설들이 예측 가능한 일정, 보험사 측이 익숙한 체계, 그리고 엄격한 절차 관리를 중심으로 수십 년까지 구축되어 왔기 때문입니다. 야간 혈액 투석은 1회 세션당 클리어런스량이 많아 일상생활의 유연성을 원하는 환자에게 매력적이지만, 투석 의자 점유 시간이 길어짐에 따라 각 치료 시간대의 수익성이 달라지기 때문에 여전히 보급률은 낮은 임베디드니다. 하이브리드형 및 재택 연계형을 포함한 기타 서비스 형태는 공공 정책이 기존 시설 밖에서의 치료를 지원하고 있는 시장에서 계속해서 소규모 수익원으로 자리 잡고 있습니다.

재택 혈액 투석은 2026년부터 2031년까지 연평균 성장률(CAGR) 8.38%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 서비스 형태로, 혈액 투석 서비스 시장에서 향후 의료 서비스 재설계가 어느 분야에 집중될지를 보여주고 있습니다. 아웃셋 메디컬사는 2026년 1월에 차세대 혈액 투석 시스템 "Tablo"에 대해 FDA의 510(k) 승인을 획득했습니다. 이는 또한 FDA의 2025년 의료기기 사이버 보안 요건에 따라 승인된 최초의 투석 시스템이기도 합니다. 이 시스템은 현재 미국 내 1,000곳 이상의 의료시설에 도입되어 있으며, 이는 의료 제공업체들이 치료 환경 간 전환을 더욱 원활하게 하는 기술을 지지하는 태도를 강화하고 있음을 시사합니다. 규제 기준이 강화됨에 따라 새로운 규정 준수 기준을 충족할 수 있는 공급업체에 우위가 생길 가능성이 있으며, 이로 인해 향후 공급업체의 선택 폭은 좁아지는 반면, 혈액 투석 서비스 시장에서 확장성이 높은 재택 프로그램의 사업적 타당성은 더욱 높아질 가능성이 있습니다.

지역별 분석

2025년, 북미는 혈액 투석 서비스 시장 점유율의 38.22%를 차지하며, 같은 기간 동안 지역별 매출 기준 중 가장 큰 비중을 차지했습니다. 미국에서는 연령에 관계없이 투석 환자를 대상으로 하는 메디케어의 ESRD 급여 제도에 의해 이러한 지위가 뒷받침되고 있으며, 해당 지역에는 견고한 공적 보상 기반이 구축되어 있습니다. 2026년 한 해 동안 ESRD PPS 기본 단가는 281.71달러에 달할 것으로 예상되며, 약 7,600곳의 ESRD 시설에 대한 메디케어 지급액은 60억 달러에 육박할 것으로 전망됩니다. 이는 2025년 대비 2.2% 증가한 수치입니다. 또한, 분석에 따르면 메디케어 인증 투석 시설에서 체인 운영의 비중이 여전히 매우 높은 것으로 나타났으며, 이는 혈액 투석 서비스 시장에서 규모, 보험사와의 계약, 그리고 운영 효율성이 여전히 주요 경쟁 수단으로 남아 있는 이유를 설명해 줍니다. 남미의 상황은 다르며, 환자 수요는 계속 증가하고 있지만, 공적 보상액이 낮기 때문에 네트워크 확장을 위한 투자 환경은 어려운 실정입니다.

유럽은 지역별 시장 규모에서 2위를 차지하고 있으며, 독일과 프랑스가 혈액 투석 서비스 시장의 주요 시장으로 확인되었습니다. 독일은 법정 건강보험에 기반을 둔 성숙하고 보급률이 높은 시스템을 특징으로 하는 반면, 프랑스는 전국적으로 조직화된 의료 체계를 통해 다수의 투석 환자를 지원하고 있습니다. 프랑스의 “PLFSS 2026”법령에 따라 2027년 1월부터 투석 자금 조달 방식이 "1회당 결제"에서 "환자별로 설정된 주 단위 일괄 납부"로 전환됩니다. 이는 재택 투석 및 자립 투석 이용 확대를 촉진하는 것을 목적으로 하고 있습니다. 유럽의 혈액 투석 서비스 시장 전체에 있어, 이러한 정책 변경은 중요한 의미를 지닙니다. 왜냐하면 각국의 의료 제도는 순수한 민간 가격의 동향보다 의료 제공업체의 투자 결정에 직접적인 영향을 미치는 경우가 많기 때문입니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 7.65%로 가장 빠르게 성장하고 있는 지역 부문이며, 혈액 투석 서비스 시장에 있어 가장 강력한 지리적 확장 기반을 제공합니다. 특히 인구가 많은 국가들에서 의료 접근성이 여전히 질병 부담에 미치지 못하고 있는 서비스가 부족한 도시 및 준도시 지역의 서비스 제공 영역을 중심으로 네트워크 확장이 진행되고 있습니다. 이러한 지역적 경향은 중요합니다. 왜냐하면 수요가 높은 지역에 새로운 클리닉이 건립되고, 환급 및 공급 조건이 정기적인 서비스 제공을 뒷받침할 수 있게 되면 환자 수를 신속하게 늘릴 수 있기 때문입니다. 중동 및 아프리카는 여전히 혈액 투석 서비스 시장에서의 점유율이 낮은 편이지만, 민관 협력 투자 모델과 선별적인 국제 진출을 통해 이 지역의 의료 서비스 제공 범위가 점차 확대되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the hemodialysis services market size was valued at USD 6.12 billion in 2025 and is estimated to grow from USD 6.44 billion in 2026 to reach USD 8.32 billion by 2031, at a CAGR of 5.25% during the forecast period (2026-2031).

This report is Segmented by Service Type (In-Center Hemodialysis, Home Hemodialysis, Nocturnal Hemodialysis, Others), End User (Dialysis Centers, Hospitals, Home Care Settings, Others), Indication (CKD, Acute Kidney Infections, Septic Shock, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Hemodialysis Services Market Trends and Insights

Rising ESRD Burden and CKD Progression

The hemodialysis services market is being pushed by a larger pool of patients with chronic kidney disease who eventually progress to ESRD and require ongoing renal replacement therapy. The Brazilian Dialysis Census 2024 recorded 172,585 patients on dialysis, which represented nearly 55% growth over the prior decade and showed how patient load continues to build across large treatment systems. The same census found that diabetes and hypertension each accounted for 29% of chronic kidney disease etiology, which shows that dialysis demand is still being fed by common long-duration metabolic disorders rather than isolated clinical episodes. This matters because patients who enter treatment later in the disease course often need more complex care, more clinical oversight, and longer treatment continuity, all of which raise the service intensity attached to each patient relationship. The hemodialysis services market also benefits from the fact that ESRD is not a short-cycle condition, so new patient additions tend to accumulate into a durable treatment census instead of rolling off quickly. As a result, rising CKD prevalence does not just widen the patient base, it also supports steadier utilization, more predictable scheduling, and stronger revenue visibility for operators that can handle higher-acuity care.

Expanding Medicare and National Dialysis Reimbursement Coverage

Reimbursement support remains one of the clearest growth supports for the hemodialysis services market because facility economics depend heavily on stable payment rules and frequent treatment billing. The CY 2026 ESRD Prospective Payment System final rule raised the Medicare base rate to USD 281.71 per treatment, which was USD 7.89 higher than in 2025. CMS also projected 2.2% growth in total payments to all ESRD facilities, with freestanding centers receiving a 2.2% increase and hospital-based facilities receiving a 1.5% increase, which reinforces the payment strength behind large outpatient networks. The rule also extended the training add-on payment adjustment for home and self-dialysis through 2026 and aligned the AKI dialysis payment rate at USD 281.71, which broadens the funded pathway for care outside the clinic. Even with that support, the early end of the ESRD Treatment Choices Model showed that payment incentives alone do not automatically shift care models when staffing, patient training, and infrastructure still limit execution. The hemodialysis services market therefore continues to gain from reimbursement breadth, while operators still need to pair that funding with clinical capacity and compliance performance under the ESRD Quality Incentive Program.

High Labor Intensity and Nurse Shortage Pressure

The most persistent brake on the hemodialysis services market is the labor intensity of treatment delivery, because dialysis care still depends on specialized nurses, nephrologists, technical staff, and strict supervision routines. The U.S. nephrology fellowship fill rate stood at 66% in 2024, which points to a pipeline problem at the same time that patient need continues to rise. The National Center for Health Workforce Analysis projected a 21% shortage of nephrologists by 2037 and a 10% shortage of registered nurses by 2027, with rural areas facing greater exposure to service gaps. Those shortages matter because new chair capacity cannot be fully utilized when a facility cannot staff shifts, train patients, or keep required oversight ratios in place. Telehealth and advanced practice providers can help at the margin, but Medicare's in-person requirements still limit how far those solutions can scale in routine use. The hemodialysis services market therefore faces a practical ceiling where demand remains strong, but labor shortages slow the pace at which operators can convert that demand into active treatment volume.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Home Hemodialysis and Remote Monitoring

- Hemodiafiltration Upgrade Cycle in Installed Base Markets

- Uneven Reimbursement for Home Modalities and Training Logistics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In-center hemodialysis held 85.31% of hemodialysis services market share by service type in 2025, which shows how strongly the revenue base still depends on clinic-based treatment delivery. This segment remains dominant because dialysis centers provide the machines, trained clinical staff, water treatment systems, and emergency oversight that many patients with multiple comorbidities still need on a regular basis. The hemodialysis services market still leans toward in-center care because these facilities have been built over decades around predictable scheduling, payer familiarity, and strong procedural control. Nocturnal hemodialysis offers higher clearance volumes per session and has appeal for patients who want better daily-life flexibility, but it remains less common because longer chair occupancy changes the economics of each treatment slot. Other service types, including hybrid and home-linked modalities, continue to add smaller revenue streams in markets where public policy supports treatment outside the traditional center.

Home hemodialysis is the fastest-growing service type with an 8.38% CAGR from 2026 to 2031, which shows where future care redesign is concentrated inside the hemodialysis services market. Outset Medical received FDA 510(k) clearance in January 2026 for the next-generation Tablo hemodialysis system, which was also the first dialysis system cleared under the FDA's 2025 medical device cybersecurity requirements. The system is now deployed across more than 1,000 U.S. healthcare facilities, which suggests that providers are increasingly willing to back technology that supports simpler movement across care settings. That tighter regulatory bar may give an edge to vendors that can meet newer compliance standards, which could narrow supplier choice over time while strengthening the operating case for scalable home programs in the hemodialysis services market.

Complete Report Scope:

- By Service Type

- In-Center Hemodialysis

- Home Hemodialysis

- Nocturnal Hemodialysis

- Other Service Types

- By End User

- Dialysis Centers

- Hospitals

- Home Care Settings

- Other End Users

- By Indication

- Chronic Kidney Disease (CKD)

- Acute Kidney Infections

- Septic Shock

- Other Indications

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 38.22% of hemodialysis services market share in 2025, which made it the largest regional revenue base in the period. The United States supports this position through a Medicare ESRD entitlement that covers dialysis patients regardless of age, which gives the region a strong public reimbursement foundation. In CY 2026, the ESRD PPS base rate stands at USD 281.71 and is projected to generate nearly USD 6 billion in Medicare payments to nearly 7,600 ESRD facilities, which was a 2.2% increase from CY 2025. The analysis also showed that chain ownership remained very high among Medicare-certified dialysis facilities, which explains why scale, payer contracting, and operating efficiency remain central competitive tools in the hemodialysis services market. South America presents a different picture, where patient need continues to expand but lower public reimbursement creates a tighter investment environment for network growth.

Europe was the second-largest regional presence, with Germany and France identified as its anchor markets in the hemodialysis services market. Germany reflects a mature, high-penetration system backed by statutory health insurance, while France supports a large dialysis population through a nationally organized care structure. France's PLFSS 2026 legislation will shift dialysis financing from per-session payment to individualized weekly lump sums from January 2027, which is intended to encourage more home and autonomous dialysis use. That policy change matters across the wider hemodialysis services market in Europe because national health systems often influence provider investment decisions more directly than pure private pricing dynamics.

Asia-Pacific is the fastest-growing regional segment with a 7.65% CAGR through 2031, which gives the hemodialysis services market its strongest geographic expansion runway. The network expansion in underserved urban and semi-urban catchments, especially in large population countries, where access is still catching up with disease burden. This regional pattern is important because new clinic buildout in high-need areas can add volume quickly once reimbursement and supply conditions support regular service delivery. The Middle East and Africa still represent a smaller share of the hemodialysis services market, but public-private investment models and selective international expansion are gradually widening the regional care footprint.

- Apollo Dialysis Clinics

- B. Braun

- Baxter

- DaVita

- DCDC Health Services

- Dialysis Clinic, Inc.

- Diaverum AB

- Fresenius

- Innovative Renal Care

- Interwell Health

- Mozarc Medical

- NefroCenter Group

- NephroPlus

- Northwest Kidney Centers

- Rogosin Institute

- Satellite Healthcare, Inc.

- U.S. Renal Care, Inc.

- VitusCare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising ESRD Burden and CKD Progression

- 4.2.2 Expanding Medicare and National Dialysis Reimbursement Coverage

- 4.2.3 Shift Toward Home Hemodialysis and Remote Monitoring

- 4.2.4 Expansion of Center Networks in Urban and Tier-2 Catchments

- 4.2.5 Hemodiafiltration Upgrade Cycle in Installed Base Markets

- 4.2.6 Telehealth-Led Staffing Efficiency and Lower Chair Time Friction

- 4.3 Market Restraints

- 4.3.1 High Labor Intensity and Nurse Shortage Pressure

- 4.3.2 Vascular Access Failure and Rehospitalization Risk

- 4.3.3 Water Treatment, Infection Control, and Compliance Overheads

- 4.3.4 Uneven Reimbursement for Home Modalities and Training Logistics

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 In-Center Hemodialysis

- 5.1.2 Home Hemodialysis

- 5.1.3 Nocturnal Hemodialysis

- 5.1.4 Other Service Types

- 5.2 By End User

- 5.2.1 Dialysis Centers

- 5.2.2 Hospitals

- 5.2.3 Home Care Settings

- 5.2.4 Other End Users

- 5.3 By Indication

- 5.3.1 Chronic Kidney Disease (CKD)

- 5.3.2 Acute Kidney Infections

- 5.3.3 Septic Shock

- 5.3.4 Other Indications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Apollo Dialysis Clinics

- 6.3.2 B. Braun SE

- 6.3.3 Baxter International Inc.

- 6.3.4 DaVita Inc.

- 6.3.5 DCDC Health Services

- 6.3.6 Dialysis Clinic, Inc.

- 6.3.7 Diaverum AB

- 6.3.8 Fresenius Medical Care AG & Co. KGaA

- 6.3.9 Innovative Renal Care

- 6.3.10 Interwell Health

- 6.3.11 Mozarc Medical

- 6.3.12 NefroCenter Group

- 6.3.13 NephroPlus

- 6.3.14 Northwest Kidney Centers

- 6.3.15 Rogosin Institute

- 6.3.16 Satellite Healthcare, Inc.

- 6.3.17 U.S. Renal Care, Inc.

- 6.3.18 VitusCare

7 Market Opportunities & Future Outlook

- 7.1 White-Space and Unmet-Need Assessment