|

시장보고서

상품코드

2073019

지속가능 IT 조달 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Sustainable IT Procurement Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

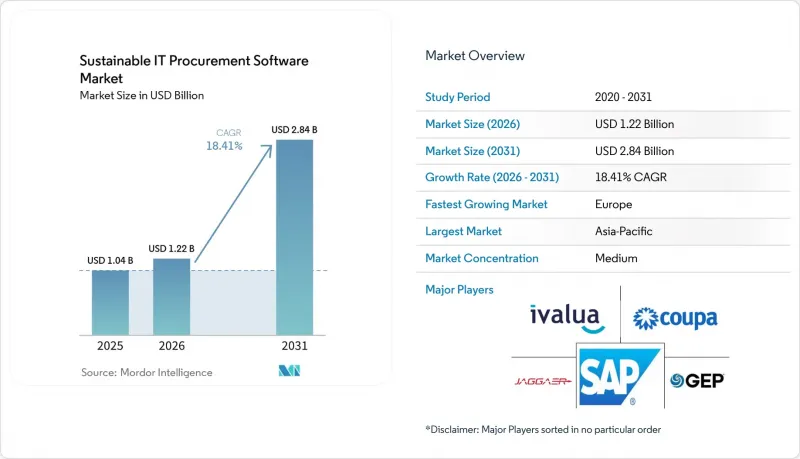

Mordor Intelligence에 의하면, 지속가능 IT 조달 소프트웨어 시장 규모는 2025년에 10억 4,000만 달러로 평가되었고 2026년 12억 2,000만 달러에서 2031년까지 28억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 18.41%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 기업 규모(대기업 및 중소기업), 용도(공급업체의 ESG 평가·점수 산정 등), IT 조달 카테고리(최종 사용자용 컴퓨팅 기기 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 지속가능 IT 조달 소프트웨어 시장 동향 및 인사이트

IT 조달 분야에서 스코프 3 데이터의 추적성에 대한 규제적 압력

지속가능 IT 조달 소프트웨어 시장은 Scope 3 보고와 관련하여 공급업체가 측정한 1차 데이터와 모델링을 통해 산출된 추정치 간의 구분을 더욱 명확히할 것을 의무화하는 공시 규정에 힘입어 성장하고 있습니다. 이는 다층적인 IT 공급망 전반에 걸쳐 수동 조달 프로세스만으로는 충족할 수 없는 요구 사항입니다. 또한, GHG 프로토콜에 따른 2026년 3월 1단계 진행 보고에서는 보고 범위의 95%를 포괄해야 하는 요건이 도입됨에 따라, 데미니스(경미) 제외 대상이 축소되는 한편, 공급업체로부터 직접 데이터를 수집해야 할 필요성이 커지고 있습니다. 세계지속가능개발기업협의회(WBCSD)는 2025년 4월에 “PACT 조사 기법 v3.0”을 발표함으로써, 거래 파트너들이 시스템 간에 제품의 탄소 발자국 데이터를 교환할 수 있는 보다 명확한 체계를 제공하여 이러한 변화를 더욱 촉진했습니다. 2025년 4월 CSRD 간소화 패키지로 인해 의무 적용 대상 기업의 수가 축소된 후에도, 대규모 구매자들은 여전히 인증된 IT 공급업체로부터 구조화된 ESG 데이터를 필요로 했기 때문에 밸류체인에 미치는 영향은 지속되었습니다. 이러한 규제, 데이터 표준, 그리고 공급업체에 대한 보고 압박이라는 요소들이 복합적으로 작용하여, 지속가능 IT 조달 소프트웨어 시장은 규정 준수를 중심으로 한 기업 지출과 밀접하게 연계된 상태를 유지하고 있습니다.

감사 가능한 공급업체 ESG 데이터에 대한 기업 수요 증가

또한, 지속가능 IT 조달 소프트웨어 시장은 감사, 제출 서류, 외부 검증을 통해 입증된 증거 없이는 공급업체의 지속가능성 관련 주장을 더 이상 받아들이지 않는 구매자들의 지지도 얻고 있습니다. EcoVadis는 2026년 5월, 자사 네트워크를 통해 확보한 지속가능성 리스크에 대한 인사이트를 바탕으로 전 세계적으로 2조 5,000억 달러 이상의 지출이 관리되고 있다고 보고했습니다. 이는 도입이 얼마나 깊이 뿌리내리고 있는지, 또한 가장 네트워크가 잘 구축된 벤더 그룹을 제외하면 여전히 공급업체의 커버리지가 얼마나 부족한지를 보여줍니다. 현재 기업들은 설문조사 응답을 감사 기록이나 실시간 위험 지표와 대조하여 검증할 수 있는 플랫폼을 요구하고 있으며, 이에 따라 공급업체 평가는 정기적인 조사 활동에서 보다 지속적인 조달 관리 단계로 전환되고 있습니다. 2025년 6월로 연장된 EcoVadis와 Ivalua의 파트너십을 통해, 조달 팀은 공급업체와의 협력을 시작하기 전에 Ivalua의 “Risk Center”에 반영함으로써, 이러한 요구를 반영한 것입니다. 그 결과, 지속가능 IT 조달 소프트웨어 시장은 공급업체 온보딩에 그치지 않고, 카테고리 계획, 리스크 심사, 그리고 공급업체 육성 프로그램으로 그 범위를 더욱 확대해 나가고 있습니다.

Tier 2 및 Tier 3 네트워크에 걸쳐 분산된 공급업체의 배출량 데이터

지속가능 IT 조달 소프트웨어 시장은 여전히 근본적인 데이터 문제에 직면해 있습니다. 이는 감사 가능한 제품 및 배출량 기록이, 특히 부품 및 원자재 공급망에서 1차 IT 공급업체를 넘어설 경우 급격히 감소하기 때문입니다. PACT에 기반한 데이터 교환 규격은 대규모 거래 파트너에게는 유용하지만, 아시아태평양이나 남미의 많은 소규모 공급업체들은 조달 플랫폼에 대규모로 입력할 수 있는 기록을 아직 갖추지 못하고 있습니다. EcoVadis는 2026년 초, 13개 언어를 지원하며 전자 및 금속을 포함한 12개 산업 분야를 대상으로 하는 '제품 탄소 발자국 계산 도구'를 제공해 대응했으나, 분산된 하위 계층 공급업체들 간의 도입 현황은 여전히 고르지 않습니다. 1차 데이터가 부족한 경우, 플랫폼은 지출 기반 모델에 의존할 수밖에 없으며, 이로 인해 보고 결과에 대한 구매자의 신뢰가 훼손되어 보다 견고한 감사 증빙이 필요하게 됩니다. 2026년 3월 EcoVadis와 Watershed가 제휴를 맺음으로써 이 문제의 일부는 해결되었지만, 이러한 제약이 실질적으로 완화되기 위해서는 지속가능 IT 조달 소프트웨어 시장에서 공급업체의 각 계층에 걸친 보다 광범위한 디지털화 노력이 여전히 필수적입니다.

부문별 분석

2025년, 소프트웨어는 68.74%의 점유율을 차지하며, 부문 수준에서 지속가능 IT 조달 소프트웨어 시장의 최대 구성 요소가 되었습니다. 기업들은 ESG 평가, 공급업체 온보딩, 보고서 대시보드, 조달 관리를 통합된 소스-투-페이 환경 내에 통합할 수 있다는 점 때문에 플랫폼 기반 도구를 선호하여 도입했습니다. 이러한 경향은 통합의 폭이 점점 더 중요시되고 있음을 반영한 것으로, 구매 담당자들은 핵심 인프라를 변경하지 않고도 기존 조달 프로세스에 지속가능성 데이터를 통합할 것을 강력히 요구했습니다. EcoVadis는 SAP Ariba, Coupa, GEP, Jaggaer, Ivalua 등 다양한 조달 플랫폼 전반에 걸쳐 인증된 통합 기능을 통해 이 모델을 지원함으로써, 완전히 맞춤형 시스템을 구축해야 할 필요성을 줄였습니다.

또한, 여러 구매자가 동일한 생태계를 이용할 경우, 공유 평가 플랫폼을 통해 설문조사 응답 부담이 줄어들기 때문에 이 부문은 공급자 측의 네트워크 효과로 인한 혜택도 누렸습니다. 그 결과, 규모, 고객 유지율, 워크플로우의 심도가 동시에 향상됨에 따라, 지속가능 IT 조달 소프트웨어 시장에서 해당 소프트웨어가 가장 뚜렷한 우위를 유지했습니다. 서로 다른 통화나 ERP 스택을 사용하는 여러 법인의 조달 환경에서는 시스템 도입, 데이터 보강, 컨설팅 및 관리형 평가 업무가 필요하기 때문에 서비스 역시 여전히 중요한 위치를 차지하고 있습니다. 또한, 많은 기업들이 단순히 라이선스를 취득하는 데 그치지 않고 플랫폼 기능을 운영상의 규정 준수 프로세스로 전환하기 위한 지원을 여전히 필요로 하고 있기 때문에 서비스 분야는 2031년까지 연평균 성장률(CAGR) 18.65%로 확대될 것으로 전망됩니다. 시장이 성숙해짐에 따라, 서비스의 구성은 광범위한 도입 지원에서 데이터 품질, 감사 대응, 그리고 조달 특유의 스코프 3 대응으로 전환될 가능성이 높다고 생각됩니다.

2025년에는 클라우드가 시장의 65.12%를 차지하며, 지속가능 IT 조달 소프트웨어 시장에서 가장 큰 도입 모델이 되었습니다. 구매자가 SaaS 방식을 선호한 이유는 도입 주기가 짧고, 규제 관련 컨텐츠의 업데이트가 용이하며, 대규모 On-Premise 인프라 없이도 공급업체와의 연동을 확장할 수 있다는 점에 있습니다. 또한, 클라우드는 공급업체 네트워크와의 실시간 데이터 공유를 가능하게 하여, 기업이 1차 IT 공급업체로부터 더 많은 1차 배출량 데이터를 수집하는 데 중요한 역할을 했습니다. 또한, 구독 방식은 완전한 On-Premise형 시스템에 비해 초기 도입 부담을 줄여주기 때문에 보다 광범위한 소프트웨어 조달 구매 행태에도 부합했습니다.

On-Premise 시스템은 공급업체의 상업 데이터나 계약 기록이 보다 엄격하게 관리되는 경우가 많은 국방, 금융 서비스, 공공 조달 분야에서 여전히 중요한 역할을 수행하고 있습니다. 많은 기업들이 기밀성이 높은 거래 데이터를 On-Premise 환경에 보관하는 한편, 지속가능성 분석 및 공급업체 참여 관련 업무를 클라우드로 이전하고 있기 때문에 하이브리드 모델은 2031년까지 연평균 성장률(CAGR) 18.52%로 확대될 것으로 예측됩니다. SAP의 ‘지속가능성 관제탑’에 관한 2026년 로드맵은 대규모 조직에서 클라우드 분석이 On-Premise S/4HANA 거래 데이터와 어떻게 연동될 수 있는지를 보여줌으로써, 이러한 수요를 직접 반영한 것입니다. 이 접근 방식은 완전한 퍼블릭 클라우드로의 전환이 반드시 현실적이지 않은 경우, 선택적인 현대화가 이미 진행되고 있는 지속가능 IT 조달 소프트웨어 시장의 현황과 일치합니다. 따라서 하이브리드화의 추세는 클라우드를 거부하기 때문이라기보다는 새로운 지속가능성 도구를 기존의 조달 인프라와 연계하려는 실용적인 필요성에서 비롯된 것이라고 할 수 있습니다.

지역별 분석

2025년, 유럽은 34.56%의 점유율을 차지하며, 지역별로는 지속가능 IT 조달 소프트웨어 시장에서 최대의 입지를 확립했습니다. 이러한 추세는 견고한 기업 조달 인프라, 복잡하고 다층적인 IT 공급망, 그리고 독일, 영국, 프랑스, 이탈리아, 스페인에 걸쳐 있는 대규모 산업·금융·기술 기업의 높은 집중도를 반영한 것입니다. 독일은 공공 IT 조달 체계에 이미 지속가능성이 공식적인 평가 요소로 포함되어 있으며, 체계화된 공급업체의 ESG 도구에 대한 민관 양측 수요를 뒷받침하고 있어, 계속해서 가장 성숙한 국내 시장으로서의 위상을 유지했습니다. 유럽연합 집행위원회도 독일의 광범위한 정보 공개 기반을 지적하고 있으며, 독일에서는 지속가능성 보고 의무화가 기업 소프트웨어 수요를 뒷받침하고 있습니다. 영국은 “IT Reuse for Good 헌장”을 통해, EU 규제 범위 밖에서도 "재사용 우선"의 관행을 지원하고, 해당 지역의 순환형 조달 방향을 강화했습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 19.12%를 나타낼 것으로 예측되며, 지속가능 IT 조달 소프트웨어 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이러한 성장은 일본, 한국, 호주, 중국, 인도에서의 정보 공개 압력, 수출 주도형 공급업체 수요, 그리고 현지 플랫폼의 개발에 힘입어 이루어지고 있습니다. 특히 일본이 두드러지는 점은 NEC가 2025년 12월에 "공급업체 포털"의 시범 검증을 시작했으며, 공급망 전반에 걸친 지속가능성 자가 평가 설문조사의 디지털화를 추진하고 있기 때문입니다. 또한, 해당 지역은 전자 및 IT 제조 분야에서 차지하는 역할 덕분에 혜택을 누리고 있으며, 다수의 소규모 하청 업체와 현지화된 워크플로우를 지원할 수 있는 공급업체 연계 도구가 요구되고 있습니다. 중국과 인도는 양국의 수출 지향형 제조업체들이 유럽의 기업 고객들로부터 ESG 데이터 제공 요청을 점점 더 많이 받고 있기 때문에 국내 공시 규제가 아직 성숙되지 않은 지역에서도 소프트웨어 도입을 촉진하고 있어 여전히 고성장 시장으로 남아 있습니다.

북미는 2025년 시점에서 중요한 위치를 차지하고 있었습니다. 이는 대형 기술 기업, 금융 기관, 연방 정부의 계약업체들이 이미 조달 방침에 공급업체의 지속가능성 요건을 반영해 놓았기 때문입니다. 남미는 여전히 신흥 지역이며, 브라질의 주요 수출 기업들은 유럽 측의 고객 보고 요건을 통해 지속가능 IT 조달 프로그램에 참여하고 있습니다. 아르헨티나를 비롯한 기타 남미은 여전히 초기 단계 시장이며, 도입은 주로 다국적 기업이나 대규모 수출 기업에 집중되어 있었습니다. 중동 및 아프리카는 도입 초기 단계에 머물러 있었으나, 아랍에미리트(UAE)와 사우디아라비아는 각국의 탄소중립 및 경제 변혁 정책과 연계된 지역적 확산을 주도하고 있었습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

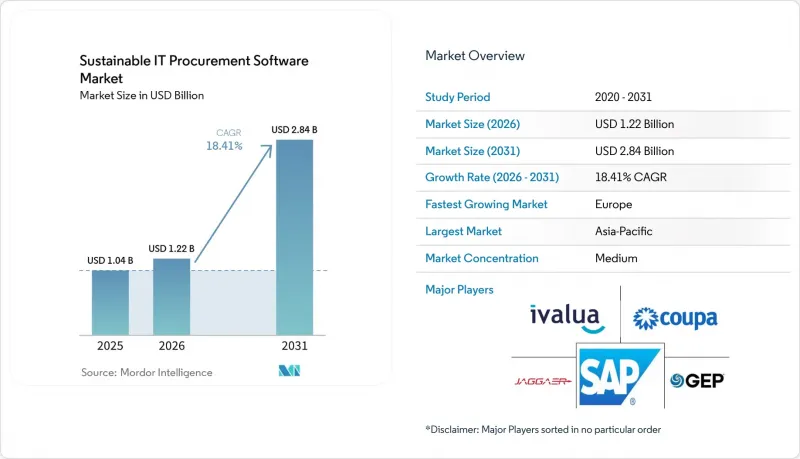

JHSAccording to Mordor Intelligence, the sustainable IT procurement software market size was valued at USD 1.04 billion in 2025 and estimated to grow from USD 1.22 billion in 2026 to reach USD 2.84 billion by 2031, at a CAGR of 18.41% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment (Cloud, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Supplier ESG Assessment and Scoring, and More), IT Procurement Category (End-User Computing Devices, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Sustainable IT Procurement Software Market Trends and Insights

Regulatory Pressure on Scope 3 Data Traceability in IT Procurement

The Sustainable IT Procurement Software Market is being pushed forward by disclosure rules that now require clearer separation between supplier-measured primary data and modeled estimates in Scope 3 reporting, which manual procurement processes cannot handle across layered IT supply chains. The March 2026 Phase 1 progress update from the GHG Protocol also introduced a 95% reporting boundary requirement, reducing the room for de minimis exclusions and increasing the need for direct supplier data collection. The World Business Council for Sustainable Development strengthened this shift when it published the PACT Methodology v3.0 in April 2025, providing trading partners with a clearer framework for exchanging product carbon footprint data across systems. Even after the April 2025 CSRD simplification package narrowed the number of companies in mandatory scope, the value-chain effect continued because large buyers still needed structured ESG data from approved IT suppliers. This combination of regulatory rules, data standards, and supplier reporting pressure is keeping the Sustainable IT Procurement Software Market firmly tied to compliance-led enterprise spending.

Rising Enterprise Demand for Auditable Supplier ESG Data

The Sustainable IT Procurement Software Market is also gaining support from buyers that no longer accept supplier sustainability claims without supporting evidence tied to audits, filings, and outside validation. EcoVadis reported in May 2026 that more than USD 2.5 trillion in global spend was governed through sustainability risk insights on its network, demonstrating both how deeply adoption has become and how much supplier coverage is still missing outside the most connected vendor groups. Enterprises now want platforms that can validate questionnaire responses against audit records and live risk indicators, which moves supplier scoring from a periodic survey exercise into a more permanent procurement control layer. The June 2025 extension of the EcoVadis and Ivalua partnership reflected that need by bringing predictive ESG risk analytics into Ivalua's Risk Center before sourcing teams launch supplier engagement. As a result, the Sustainable IT Procurement Software Market is moving beyond supplier onboarding and deeper into category planning, risk screening, and supplier development programs.

Fragmented Supplier Emissions Data Across Tier 2 and Tier 3 Networks

The Sustainable IT Procurement Software Market still faces a fundamental data problem because auditable product and emissions records decline sharply beyond first-tier IT suppliers, especially in component and raw-material networks. PACT-based exchange standards help larger trading partners, but many smaller suppliers in Asia-Pacific and South America do not yet maintain records that can be pulled into procurement platforms at scale. EcoVadis responded in early 2026 with a Product Carbon Footprint Calculator available in 13 languages and across 12 industrial sectors, including electronics and metals, yet adoption across fragmented lower-tier suppliers remains uneven. When primary data is missing, platforms fall back on spend-based models, which weakens buyers' confidence in reported results and leaves them in need of stronger audit trails. The March 2026 EcoVadis and Watershed partnership addressed part of this issue, but the Sustainable IT Procurement Software Market still depends on a much wider digitalization effort across supplier tiers before this restraint meaningfully eases.

Other drivers and restraints analyzed in the detailed report include:

- Shift From Manual Procurement Workflows to Embedded Sustainability Scoring

- Procurement-Led Cost Avoidance Through Energy and Carbon Attribute Filtering

- Limited Interoperability With Legacy ERP and E-Procurement Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 68.74% share in 2025, making it the largest component in the Sustainable IT Procurement Software Market at the segment level. Enterprises favored platform-based tools because they could place ESG scoring, supplier onboarding, reporting dashboards, and sourcing controls inside a connected source-to-pay environment. That preference also reflected the growing value of integration breadth, as buyers increasingly wanted sustainability data to be incorporated into existing procurement events without changing core infrastructure. EcoVadis supported this model with certified integrations across procurement platforms such as SAP Ariba, Coupa, GEP, Jaggaer, and Ivalua, which reduced the need for fully custom builds.

The same segment benefited from supplier-side network effects because shared assessment platforms reduced questionnaire fatigue when multiple buyers relied on the same ecosystem. As a result, software retained the clearest advantage in the Sustainable IT Procurement Software Market because scale, retention, and workflow depth improved together. Services remain important because implementation, data enrichment, consulting, and managed assessment work are necessary in multi-entity procurement environments with different currencies and ERP stacks. Services are also projected to expand at a 18.65% CAGR through 2031, as many enterprises still need help turning platform capabilities into operational compliance processes rather than simply buying licenses. Over time, that services mix is likely to shift away from broad rollout support and toward data quality, audit readiness, and procurement-specific Scope 3 support as the market matures.

Cloud accounted for 65.12% of the market in 2025, making it the largest deployment model in the Sustainable IT Procurement Software Market. Buyers favored SaaS delivery because deployment cycles were faster, regulatory content could be updated more easily, and supplier engagement could scale without the need for heavy local infrastructure. Cloud also supported live data sharing with supplier networks, which was important as enterprises sought to gather more primary emissions data from first-tier IT vendors. The model fit broader procurement software buying behavior as well, since subscription delivery reduced the upfront deployment burden compared with fully on-premises systems.

On-premise systems remained relevant in defense, financial services, and public procurement, where supplier commercial data and contract records were often under stricter control. Hybrid is projected to expand at a 18.52% CAGR through 2031, as many enterprises move sustainability analytics and supplier engagement layers to the cloud while keeping sensitive transaction data in on-premises environments. SAP's 2026 roadmap for Sustainability Control Tower directly reflected this demand by showing how cloud analytics could work with on-premise S/4HANA transaction data in large organizations. That approach fits the current stage of the Sustainable IT Procurement Software Market, where full public cloud migration is not always realistic but selective modernization is already underway. Hybrid momentum is therefore tied less to a rejection of cloud and more to the practical need to connect new sustainability tools with existing procurement infrastructure.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment

- Cloud

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Supplier ESG Assessment and Scoring

- Sustainable Sourcing and Procurement Management

- Supplier Risk Monitoring

- Carbon Footprint and Lifecycle Assessment

- Reporting, Compliance and Audit Management

- Circular Procurement and Asset Reuse Planning

- By IT Procurement Category

- End-User Computing Devices

- Servers and Data Center Equipment

- Network Infrastructure

- Cloud and Digital Services

- Software and SaaS Procurement

- IT Peripherals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe held 34.56% share in 2025, giving the region the largest position in the Sustainable IT Procurement Software Market by geography. Its lead reflected strong enterprise procurement infrastructure, complex multi-tier IT supply chains, and a high concentration of large industrial, financial, and technology companies across Germany, the United Kingdom, France, Italy, and Spain. Germany remained the deepest national market because public IT procurement frameworks already incorporate sustainability as a formal evaluation factor, supporting both public and private demand for structured supplier ESG tools. The European Commission also pointed to a large disclosure base in Germany, where mandatory sustainability reporting requirements sustain enterprise software demand. The United Kingdom reinforced the region's circular procurement direction through its IT Reuse for Good Charter, which supported reuse-first practices even outside the EU regulatory perimeter.

Asia-Pacific is projected to expand at a 19.12% CAGR through 2031, making it the fastest-growing regional block in the Sustainable IT Procurement Software Market. Growth is supported by disclosure pressure, export-led supplier demands, and local platform development across Japan, South Korea, Australia, China, and India. Japan stands out because NEC began pilot validation of its Supplier Portal in December 2025 to digitalize sustainability self-assessment questionnaires across supply chains. The region also benefits from its role in electronics and IT manufacturing, requiring supplier engagement tools that can work across many smaller sub-tier vendors and localized workflows. China and India remain high-growth markets because export-oriented manufacturers in both countries are receiving more ESG data requests from European enterprise customers, pulling software adoption forward even where domestic disclosure rules are less mature.

North America held a substantial position in 2025 as large technology companies, financial institutions, and federal contractors were already embedding supplier sustainability requirements into procurement policies. South America remained an emerging region, with large Brazilian exporters being drawn into sustainable IT procurement programs through customer reporting requirements from Europe. Argentina and the rest of South America were still early-stage markets, with adoption concentrated mainly among multinationals and larger exporters. The Middle East and Africa stayed at an earlier adoption stage, though the United Arab Emirates and Saudi Arabia led regional deployments tied to national net-zero and economic transformation agendas.

- Ivalua Inc.

- Coupa Software Incorporated

- SAP SE

- Jaggaer, LLC

- GEP Worldwide

- Zycus Infotech Pvt. Ltd.

- Oracle Corporation

- EcoVadis SAS

- IntegrityNext GmbH

- Sphera Solutions, Inc.

- Supplier.io, Inc.

- OneTrust, LLC

- Verdikt

- Sedex Information Exchange Limited

- Assent Inc.

- Asuene Inc.

- HICX Solutions Limited

- IPoint-systems gmbh

- Achilles Information Limited

- Greenly

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Pressure on Scope 3 Data Traceability in IT Procurement

- 4.2.2 Rising Enterprise Demand for Auditable Supplier ESG Data

- 4.2.3 Shift From Manual Procurement Workflows to Embedded Sustainability Scoring

- 4.2.4 Procurement-Led Cost Avoidance Through Energy and Carbon Attribute Filtering

- 4.2.5 Supplier Digitalization Enabling Automated Sustainability Questionnaires

- 4.2.6 ESG-Linked Sourcing in Hardware Refresh and Device Lifecycle Programs

- 4.3 Market Restraints

- 4.3.1 Fragmented Supplier Emissions Data Across Tier 2 and Tier 3 Networks

- 4.3.2 Limited Interoperability With Legacy ERP and e-Procurement Stacks

- 4.3.3 Internal Data Ownership Conflicts Between Procurement, Sustainability, and IT Teams

- 4.3.4 High Supplier Response Fatigue in Multi-Framework ESG Assessments

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity Of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Supplier ESG Assessment and Scoring

- 5.4.2 Sustainable Sourcing and Procurement Management

- 5.4.3 Supplier Risk Monitoring

- 5.4.4 Carbon Footprint and Lifecycle Assessment

- 5.4.5 Reporting, Compliance and Audit Management

- 5.4.6 Circular Procurement and Asset Reuse Planning

- 5.5 By IT Procurement Category

- 5.5.1 End-User Computing Devices

- 5.5.2 Servers and Data Center Equipment

- 5.5.3 Network Infrastructure

- 5.5.4 Cloud and Digital Services

- 5.5.5 Software and SaaS Procurement

- 5.5.6 IT Peripherals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ivalua Inc.

- 6.4.2 Coupa Software Incorporated

- 6.4.3 SAP SE

- 6.4.4 Jaggaer, LLC

- 6.4.5 GEP Worldwide

- 6.4.6 Zycus Infotech Pvt. Ltd.

- 6.4.7 Oracle Corporation

- 6.4.8 EcoVadis SAS

- 6.4.9 IntegrityNext GmbH

- 6.4.10 Sphera Solutions, Inc.

- 6.4.11 Supplier.io, Inc.

- 6.4.12 OneTrust, LLC

- 6.4.13 Verdikt

- 6.4.14 Sedex Information Exchange Limited

- 6.4.15 Assent Inc.

- 6.4.16 Asuene Inc.

- 6.4.17 HICX Solutions Limited

- 6.4.18 IPoint-systems gmbh

- 6.4.19 Achilles Information Limited

- 6.4.20 Greenly

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment