|

시장보고서

상품코드

2073074

데스크톱 워크스테이션 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Desktop Workstation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

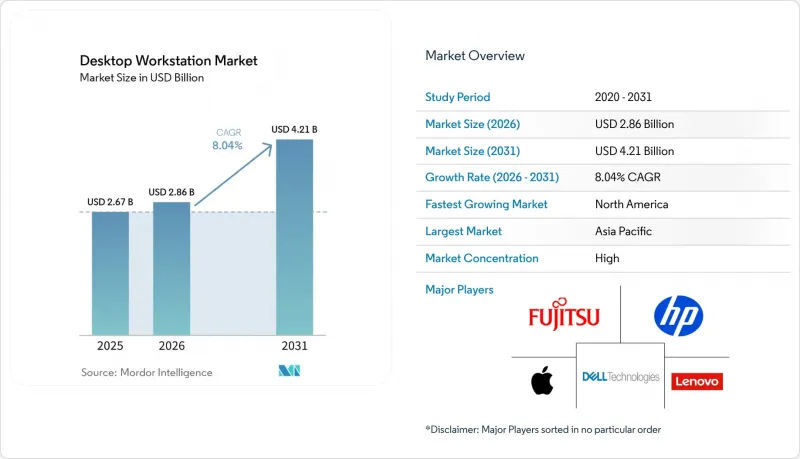

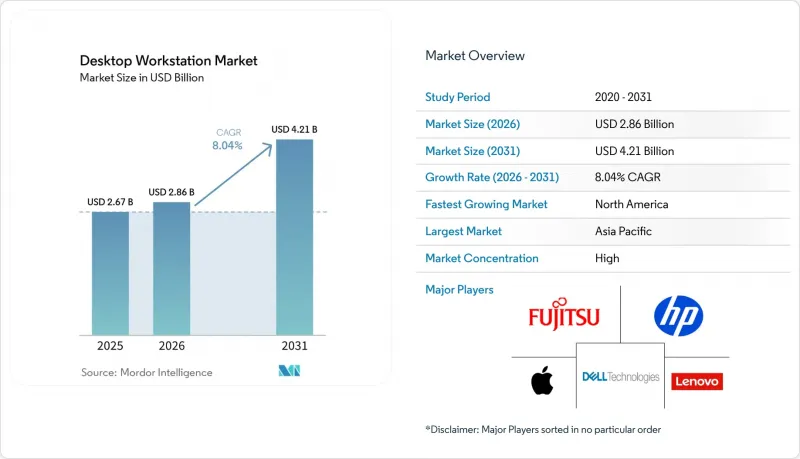

Mordor Intelligence에 의하면, 데스크톱 워크스테이션 시장 규모는 2025년 26억 7,000만 달러에서 2026년에는 28억 6,000만 달러로 확대되어 2031년까지 42억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 8.04%로 확대해 갈 전망입니다.

본 보고서는 폼 팩터(타워형, 소형 폼 팩터, 랙형, 모바일형 또는 올인원형), 프로세서 유형(x86 기반, ARM 기반 등), 최종 사용자 산업(미디어 및 엔터테인먼트, 엔지니어링·건축, 헬스케어 및 생명과학, 금융 서비스 등), 판매 채널(직접 판매, 간접 판매 또는 리셀러), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 데스크톱 워크스테이션 시장 동향 및 분석

AI 및 실시간 레이 트레이싱 워크로드의 도입 확대

기업들은 로컬 환경에서 대규모 언어 모델을 튜닝하고 영화 수준의 패스트레이싱을 처리하기 위해 워크스테이션을 교체하고 있습니다. 2026년 3월에 출시된 NVIDIA의 RTX PRO 6000 Blackwell GPU는 4세대 RT 코어와 RTX 메가 지오메트리 유닛을 탑재하여, 가상 제작을 위한 상호작용형 장면 구축을 가능하게 합니다. Dell의 Precision 9 T6 타워는 최대 5개의 300와트 GPU와 4테라바이트의 DDR5 ECC 메모리를 지원하며, 책상 위 시스템을 멀티 에이전트 AI 워크플로우용 미니 클러스터로 탈바꿈시킵니다. HP의 테스트 데이터에 따르면, Z Boost를 통한 GPU 공유로 인해 CATIA 및 Siemens NX의 렌더링 속도가 5.7배 향상된 것으로 나타났으며, 이는 긴밀하게 네트워크로 연결된 워크스테이션이 원격 렌더링 팜을 대체할 수 있음을 입증했습니다. 이러한 변화에 따라 예산은 다수의 GPU를 탑재한 구성으로 전환되고 있으며, AI 개발 및 시각화 분야에서 데스크톱 워크스테이션 시장의 전략적 역할이 더욱 강화되고 있습니다.

가상 제작 파이프라인에서 컨텐츠 제작 수요 증가

2025년 말까지 전 세계 LED 볼륨 스테이지의 수는 300개를 넘어설 전망이며, 수백만 픽셀 규모의 벽면에 10비트 HDR 영상을 초당 60프레임으로 스트리밍할 수 있는 시스템에 대한 수요가 지속적으로 증가하고 있습니다. NVIDIA의 Blackwell 제품군은 AI 기반 노이즈 제거 속도를 높여주는 5세대 Tensor Core를 탑재하고 있어, 소규모 스튜디오에서도 더 적은 수의 GPU로 영화급 결과물을 구현할 수 있습니다. Lenovo의 ThinkStation P5Gen 2는 듀얼 RTX PRO 6000 Blackwell Max-Q 카드를 랙 장착형 케이스에 탑재하여, 책상에서의 반복 작업과 스튜디오 인프라를 연결해 줍니다. 실시간 합성이 주류가 됨에 따라, 크리에이티브 에이전시들은 지연 시간이 최적화된 스토리지와 25기가비트 네트워크를 통합한 워크스테이션 번들을 점점 더 많이 지정하고 있으며, 이는 수익성이 높은 주변기기 매출을 견인하고 있습니다.

클라우드 워크스테이션의 보급으로 인해 하드웨어 교체 주기가 단축되었습니다.

Desktop-as-a-Service(DaaS) 서비스를 통해 기업은 GPU 사용 시간을 시간 단위로 대여할 수 있게 되었으며, 고가의 하드웨어를 전액 구매하는 대신 비용 대비 효율이 높은 대안을 제공받고 있습니다. 이러한 접근 방식을 통해 On-Premise 시스템의 업데이트 주기가 기존 3년에서 최대 5년으로 연장되어, 기업은 설비 투자를 최적화할 수 있게 됩니다. 이 모델은 고성능 컴퓨팅 리소스에 대한 수요가 변동하는 간헐적인 렌더링이나 디자인 작업의 피크 시간에 대응하는 데 특히 적합합니다. 그러나 이러한 이용 패턴의 변화로 인해, 특히 광섬유 회선이 구축된 지역에서 연간 출하 대수가 감소하고 있습니다. 이러한 지역에서는 네트워크 지연이 최소화되어 원활한 성능이 보장되므로, DaaS가 더욱 매력적인 선택지가 되고 있습니다. 사용자들은 AWS, Azure, NVIDIA DGX Cloud 인스턴스 등의 클라우드 플랫폼에 접속할 때 점점 더 씬 클라이언트를 선호하는 추세입니다. 이 전략을 통해 조직은 워크로드가 안정될 때까지 막대한 설비 투자를 미룰 수 있으며, IT 인프라 관리에 있어 더 높은 유연성과 확장성을 실현할 수 있습니다.

부문별 분석

랙형 워크스테이션은 2031년까지 연평균 성장률(CAGR) 8.84%를 기록한 반면, 타워형은 2025년 매출의 53.21%를 차지하고 있어, 데스크톱 워크스테이션 시장에서 한 형태가 다른 형태를 잠식하는 것이 아니라 이 두 형태가 공존하고 있음이 드러나고 있습니다. IT 팀은 제어된 냉각 환경 내에서 수 kW급 GPU 어레이를 일원화하여 관리하기 위해 랙형 워크스테이션을 점점 더 선호하고 있습니다. 이 설계 접근 방식의 좋은 예로는 HP의 "Z8 Fury G6i"입니다. 이 모델은 최대 4개의 RTX PRO 6000 Blackwell GPU를 지원하면서도 평면 배치에 미치는 영향을 최소화함으로써, 사무 공간을 효율적으로 활용할 수 있도록 합니다.

소형 폼 팩터나 모바일 워크스테이션 모델은 공간이 제한된 환경에 적합하지만, 일반적으로는 단일 GPU 구성으로만 제공됩니다. 예를 들어, 레노버의 "ThinkPad P1 Gen 9"는 55 TOPS의 NPU를 탑재하고 있어, 노트북급 칩으로도 현재 엔트리 레벨의 AI 추론 작업을 처리할 수 있음을 보여줍니다. 또한, HP의 "Max 사이드 패널"과 같은 모듈식 사이드 패널은 기업이 랙 시스템으로의 전환을 미루면서도 더 대형의 GPU를 탑재할 수 있게 함으로써, 타워형 워크스테이션의 수명을 연장합니다. 열 관리와 소음 수준 간의 균형을 효과적으로 맞추고 있는 업체는 데스크톱 워크스테이션 시장 수요 증가를 포착하는 데 유리한 입장에 있습니다. 특히, 성능과 신뢰성이 극히 중요한 크리에이티브 스튜디오나 금융 거래장 등의 업계에서 그 우위가 두드러집니다.

x86 플랫폼은 2025년 매출의 74.36%를 차지하며, 데스크톱 워크스테이션 시장에서 우위를 유지하고 있습니다. 그러나 ARM 기반 구성은 연평균 성장률(CAGR) 8.96%를 기록하며 성장할 것으로 예상되며, 2031년까지 시장 점유율을 점진적으로 확대할 것으로 전망됩니다. 이러한 성장은 에너지 효율과 성능의 확장성을 향상시킨 ARM 아키텍처의 발전에 힘입어 이루어지고 있으며, 특정 이용 사례에서 그 매력이 더욱 부각되고 있습니다. Grace-Blackwell 칩과 128기가바이트의 통합 메모리를 결합한 NVIDIA의 "DGX Spark"는 600와트 미만의 전력 소비 범위 내에서 약 1페타플롭스의 AI 연산 능력을 구현하고 있어, 이러한 추세를 상징하는 존재입니다. 이를 통해 고성능 컴퓨팅 분야에서 ARM 기반 시스템의 잠재력이 입증되었습니다.

RISC-V는 아직 초기 단계이긴 하지만, 시장에서 영향력 있는 존재로 부상하고 있습니다. 480개의 Tensix 코어와 수냉 시스템을 탑재한 Tenstorrent사의 "QuietBox 2"(9,999달러)는 더 높은 제어성과 유연성을 확보하기 위해 개방형 명령어 세트를 우선시하는 소버린 컴퓨팅 구매자를 대상으로 설계되었습니다. 또한, RISC-V International의 RVA23 프로파일 및 ACPI 6.6 지원 덕분에 펌웨어 개발이 효율화되었으며, 데스크톱 OS 도입 절차가 간소화되었습니다. 다른 프로세서 유형은 여전히 틈새 시장으로 남아 있지만, 특히 정부 산하 연구소나 전문 연구 기관을 대상으로 한 '포스트 무어의 법칙' 시대의 가속화 요인을 통해 시장에서 전략적 기회를 제시하고 있습니다. 이러한 동향은 데스크톱 워크스테이션 시장에서 프로세서 기술의 다양화가 진행되고 있음을 여실히 보여주고 있습니다.

지역별 분석

북미는 미국 기업들의 AI 하드웨어 교체에 힘입어 2025년 매출의 39.49%를 차지했으나, 신흥 지역과 비교하면 성장세가 둔화되고 있습니다. HIPAA나 주 차원의 개인정보 보호 관련 법규와 같은 규제 요인으로 인해 워크로드는 여전히 On-Premise에 집중되어 있으며, 클라우드 도입이 확대되는 상황에서도 최소한 수요는 확보되고 있습니다. 또한, 이 지역은 잘 갖춰진 IT 인프라와 주요 시장 참여자들의 강력한 입지에 힘입어 고성능 데스크톱 워크스테이션에 대한 안정적인 수요가 보장되고 있습니다. 의료, 금융, 제조 등 다양한 산업 분야에서 AI 기반 용도의 도입이 확대되고 있는 점도 시장의 안정성을 더욱 뒷받침하고 있습니다.

아시아태평양은 성장의 원동력이 되고 있으며, 2031년까지의 연평균 성장률(CAGR)은 9.04%로 예측됩니다. 중국의 반도체 자급자족을 위한 노력으로 인해 전자 설계 자동화(EDA)용 워크스테이션 예산이 증가하는 한편, 한국의 파운드리 확장 및 일본의 정부 주도 AI 이니셔티브가 판매량 증가를 가속화하고 있습니다. 인도의 엔지니어링 서비스 부문에서는 로컬 컴퓨팅을 활용하여 WAN 트래픽을 줄이고 있으며, CAD 및 시뮬레이션 업무에서 데스크톱 워크스테이션 시장 침투율이 높아지고 있습니다. 또한, 해당 지역의 급속한 산업화와 연구개발(R&D) 활동에 대한 투자 확대가 첨단 컴퓨팅 솔루션에 대한 수요를 견인하고 있습니다. 스마트 제조의 부상과 인더스트리 4.0 기술의 도입 역시 이 지역의 데스크톱 워크스테이션 시장 성장을 뒷받침하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정) 시행을 배경으로 꾸준한 성장세를 보이고 있습니다. 독일 자동차 업계에서는 디지털 트윈 시뮬레이션이 활용되고 있으며, 영국의 트레이딩 플로어에서는 1밀리초 미만의 분석 처리를 실현하기 위해 GPU를 다수 탑재한 타워형 워크스테이션이 선호되고 있습니다. 또한, 해당 지역에서 지속가능성과 에너지 효율이 높은 기술에 대한 집중은 워크스테이션 설계에도 영향을 미치고 있으며, 각 벤더들은 이러한 우선 순위에 부합하는 제품을 출시하고 있습니다. 남미, 중동 및 아프리카에서는 건설, 미디어, 에너지 분야에서 가격에 대한 민감성과 공급업체의 자금 조달 제한으로 인해 도입 규모는 작지만 증가 추세를 보이고 있습니다. 그러나 디지털 전환 노력의 확대와 기술 발전에 대한 정부의 지원 덕분에, 이들 지역 시장 환경은 서서히 개선되고 있습니다. 채널 인센티브와 현지 언어 지원을 최적화하는 공급업체는 특히 이러한 시장의 중소기업(SME)이 가진 고유한 요구 사항을 충족시킴으로써 시장 점유율을 더욱 확대할 수 있을 것으로 기대됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the desktop workstation market size expanded from USD 2.67 billion in 2025 to USD 2.86 billion in 2026 and is projected to reach USD 4.21 billion by 2031, advancing at an 8.04% CAGR over 2026-2031.

This report is Segmented by Form Factor (Tower, Small Form Factor, Rack, and Mobile or All-In-One), Processor Type (x86-Based, ARM-Based, and More), End-User Industry (Media and Entertainment, Engineering and Architecture, Healthcare and Life Sciences, Financial Services, and More), Sales Channel (Direct, and Indirect or Reseller), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Desktop Workstation Market Trends and Insights

Rising Adoption of AI and Real-Time Ray Tracing Workloads

Enterprises are refreshing fleets to accommodate local large-language-model tuning and cinematic-quality path tracing. NVIDIA's RTX PRO 6000 Blackwell GPU, launched in March 2026, adds fourth-generation RT Cores and RTX Mega Geometry units that enable interactive scene builds for virtual production. Dell's Precision 9 T6 tower supports up to five 300-watt GPUs and 4 terabytes of DDR5 ECC memory, turning desk-side systems into mini-clusters for multi-agent AI workflows. HP test data showed that Z Boost GPU sharing achieved 5.7x faster rendering in CATIA and Siemens NX, proving that tightly networked workstations can substitute for remote render farms. The shift is tilting budgets toward GPU-dense configurations and reinforcing the strategic role of the desktop workstation market in AI development and visualization.

Increasing Content Creation Demands in Virtual Production Pipelines

LED volume stages surpassed 300 worldwide by late 2025, creating a persistent need for systems that can stream 10-bit HDR imagery at 60 frames per second to multi-million-pixel walls. NVIDIA's Blackwell family integrates fifth-generation Tensor Cores that accelerate AI-based denoising, letting smaller studios achieve cinema-grade output with fewer GPUs. Lenovo's ThinkStation P5 Gen 2 wraps dual RTX PRO 6000 Blackwell Max-Q cards in a rack-ready enclosure, bridging desk-side iteration and studio infrastructure. As real-time compositing becomes mainstream, creative agencies increasingly specify workstation bundles that integrate latency-optimized storage and 25-gigabit networking, bolstering revenue for high-margin peripherals.

Proliferation of Cloud Workstations Reducing Hardware Refresh Cycles

Desktop-as-a-Service (DaaS) offerings enable firms to rent GPU time on an hourly basis, providing a cost-effective alternative to purchasing expensive hardware outright. This approach extends the replacement intervals for on-premises systems from the typical 3 years to up to 5 years, allowing businesses to optimize their capital expenditures. The model is particularly well-suited for handling episodic rendering and design peaks, where the demand for high-performance computing resources fluctuates. However, this shift in usage patterns has led to a decline in annual unit shipments, especially in regions with robust fiber connectivity. In such areas, minimal network latency ensures seamless performance, making DaaS a more attractive option. Users increasingly prefer thin clients for accessing cloud platforms such as AWS, Azure, or NVIDIA DGX Cloud instances. This strategy allows organizations to defer significant capital expenditures until their workloads stabilize, offering greater flexibility and scalability in managing their IT infrastructure.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Hybrid Work Driving Demand for Remote-Capable Rack Workstations

- Growing Use of Engineering Simulation Requiring High-Core Count CPUs

- Supply Chain Volatility for Advanced GPUs and Chipsets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rack workstations generated a 8.84% CAGR through 2031, while towers retained 53.21% of 2025 revenue, highlighting the coexistence of these two formats rather than one cannibalizing the other in the desktop workstation market. IT teams increasingly prefer rack workstations to centralize multi-kilowatt GPU arrays within controlled cooling environments. This design approach is exemplified by HP's Z8 Fury G6i, which supports up to four RTX PRO 6000 Blackwell GPUs while maintaining efficient use of office space by avoiding encroachment on floor plans.

Small-form-factor and mobile workstation models cater to space-constrained environments but are generally limited to single-GPU configurations. For instance, Lenovo's ThinkPad P1 Gen 9 features a 55 TOPS NPU, demonstrating that laptop-class silicon can now handle entry-level AI inference tasks. Additionally, modular side panels, such as HP's Max Side Panel, enhance the longevity of tower workstations by enabling enterprises to delay transitioning to rack systems while still accommodating larger GPUs. Vendors that effectively balance thermal management and noise levels are well-positioned to capture incremental demand in the desktop workstation market, particularly in industries such as creative studios and financial trading floors, where performance and reliability are critical.

x86 platforms controlled 74.36% of 2025 revenue, maintaining their dominance in the desktop workstation market. However, ARM-based configurations are projected to grow at a compound annual growth rate (CAGR) of 8.96%, gradually increasing their market share by 2031. This growth is driven by advancements in ARM architecture, which offer improved energy efficiency and performance scalability, making them increasingly attractive for specific use cases. NVIDIA's DGX Spark, which combines Grace-Blackwell chips with 128 gigabytes of unified memory, exemplifies this trend by delivering approximately 1 petaflop of AI compute power within a sub-600-watt power envelope, showcasing the potential of ARM-based systems in high-performance computing.

RISC-V, while still in its early stages, is emerging as an influential player in the market. Tenstorrent's USD 9,999 QuietBox 2, equipped with 480 Tensix cores and liquid cooling, is designed for sovereign-compute buyers who prioritize open instruction sets for greater control and flexibility. Additionally, RISC-V International's RVA23 profile and ACPI 6.6 support streamline firmware development, simplifying the deployment of desktop operating systems. Although other processor types remain niche, they represent strategic opportunities in the market, particularly for post-Moore accelerators aimed at government laboratories and specialized research institutions. These developments highlight the growing diversification in processor technologies within the desktop workstation market.

Complete Report Scope:

- By Form Factor

- Tower Workstations

- Small Form Factor Workstations

- Rack Workstations

- Mobile or All-in-One Workstations

- By Processor Type

- x86-Based Workstations

- ARM-Based Workstations

- RISC-V Workstations

- Other Processor Types

- By End-User Industry

- Media and Entertainment

- Engineering and Architecture

- Healthcare and Life Sciences

- Financial Services

- Scientific Research

- Other End-User Industries

- By Sales Channel

- Direct Sales

- Indirect or Reseller Sales

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America accounted for 39.49% of 2025 revenue as U.S. enterprises refreshed AI hardware, yet growth is moderating compared with that of emerging regions. Regulatory forces such as HIPAA and state-level privacy statutes continue to anchor workloads locally, safeguarding a baseline of demand even as cloud adoption rises. Additionally, the region benefits from a mature IT infrastructure and a strong presence of key market players, which ensures consistent demand for high-performance desktop workstations. The increasing adoption of AI-driven applications in industries such as healthcare, finance, and manufacturing further supports market stability.

Asia-Pacific is the growth engine, with a 9.04% CAGR projected through 2031. China's semiconductor self-sufficiency push elevates workstation budgets for electronic design automation, while South Korea's foundry expansions and Japan's sovereign-AI initiatives accelerate unit sales. India's engineering services sector leverages local compute to reduce WAN traffic, increasing desktop workstation market penetration for CAD and simulation tasks. Furthermore, the region's rapid industrialization and growing investments in R&D activities are driving demand for advanced computing solutions. The rise of smart manufacturing and the adoption of Industry 4.0 technologies are also driving growth in the desktop workstation market in this region.

Europe records steady gains amid GDPR enforcement. Germany's automotive sector uses digital twin simulations, and the United Kingdom's trading floors favor GPU-rich towers for sub-millisecond analytics. The region's focus on sustainability and energy-efficient technologies is also influencing workstation designs, with vendors introducing products that align with these priorities. South America plus Middle East, and Africa show smaller but rising adoption in construction, media, and energy, constrained by pricing sensitivity and limited vendor financing. However, increasing digital transformation initiatives and government support for technological advancements are gradually improving market conditions in these regions. Vendors that tailor channel incentives and local-language support stand to unlock incremental share, particularly by addressing the unique needs of small and medium-sized enterprises (SMEs) in these markets.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- Fujitsu Limited

- NEC Corporation

- BOXX Technologies, LLC

- ASUSTeK Computer Inc.

- Acer Incorporated

- Micro-Star International Co., Ltd.

- Apple Inc.

- Super Micro Computer, Inc.

- Corsair Gaming, Inc.

- Maingear, Inc.

- Velocity Micro, Inc.

- Puget Systems, LLC

- Xi Computer Corporation

- Eurocom Corporation

- System76, Inc.

- OnLogic Inc.

- Tuxedo Computers GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of AI and Real-Time Ray Tracing Workloads

- 4.2.2 Increasing Content Creation Demands in Virtual Production Pipelines

- 4.2.3 Shift to Hybrid Work Driving Demand for Remote-Capable Rack Workstations

- 4.2.4 Growing Use of Engineering Simulation Requiring High-Core Count CPUs

- 4.2.5 Regulatory Push for Secure, On-Premise Data Processing in Sensitive Industries

- 4.2.6 Emergence of ARM-Based Workstations Optimized for Energy Efficiency

- 4.3 Market Restraints

- 4.3.1 Proliferation of Cloud Workstations Reducing Hardware Refresh Cycles

- 4.3.2 Supply Chain Volatility for Advanced GPUs and Chipsets

- 4.3.3 Rising Average Selling Prices Limiting Adoption in SMEs

- 4.3.4 Rapid Obsolescence Due to Accelerated CPU and GPU Roadmaps

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form Factor

- 5.1.1 Tower Workstations

- 5.1.2 Small Form Factor Workstations

- 5.1.3 Rack Workstations

- 5.1.4 Mobile or All-in-One Workstations

- 5.2 By Processor Type

- 5.2.1 x86-Based Workstations

- 5.2.2 ARM-Based Workstations

- 5.2.3 RISC-V Workstations

- 5.2.4 Other Processor Types

- 5.3 By End-User Industry

- 5.3.1 Media and Entertainment

- 5.3.2 Engineering and Architecture

- 5.3.3 Healthcare and Life Sciences

- 5.3.4 Financial Services

- 5.3.5 Scientific Research

- 5.3.6 Other End-User Industries

- 5.4 By Sales Channel

- 5.4.1 Direct Sales

- 5.4.2 Indirect or Reseller Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Dell Technologies Inc.

- 6.4.2 HP Inc.

- 6.4.3 Lenovo Group Limited

- 6.4.4 Fujitsu Limited

- 6.4.5 NEC Corporation

- 6.4.6 BOXX Technologies, LLC

- 6.4.7 ASUSTeK Computer Inc.

- 6.4.8 Acer Incorporated

- 6.4.9 Micro-Star International Co., Ltd.

- 6.4.10 Apple Inc.

- 6.4.11 Super Micro Computer, Inc.

- 6.4.12 Corsair Gaming, Inc.

- 6.4.13 Maingear, Inc.

- 6.4.14 Velocity Micro, Inc.

- 6.4.15 Puget Systems, LLC

- 6.4.16 Xi Computer Corporation

- 6.4.17 Eurocom Corporation

- 6.4.18 System76, Inc.

- 6.4.19 OnLogic Inc.

- 6.4.20 Tuxedo Computers GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment