|

시장보고서

상품코드

2073083

전립선암 진단 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Prostate Cancer Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

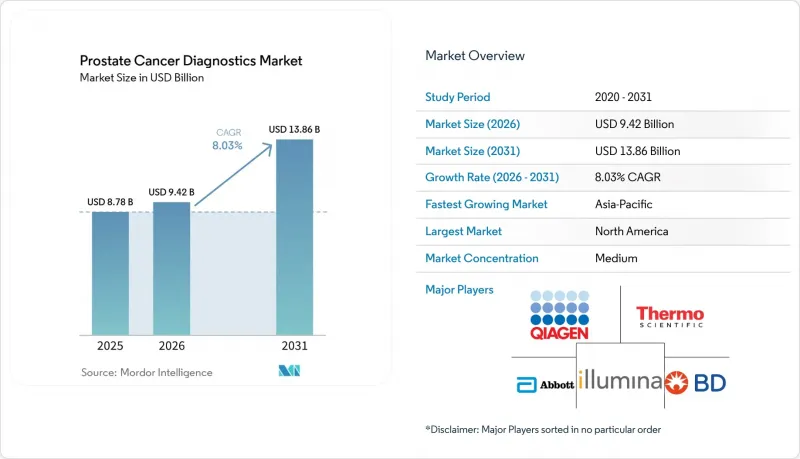

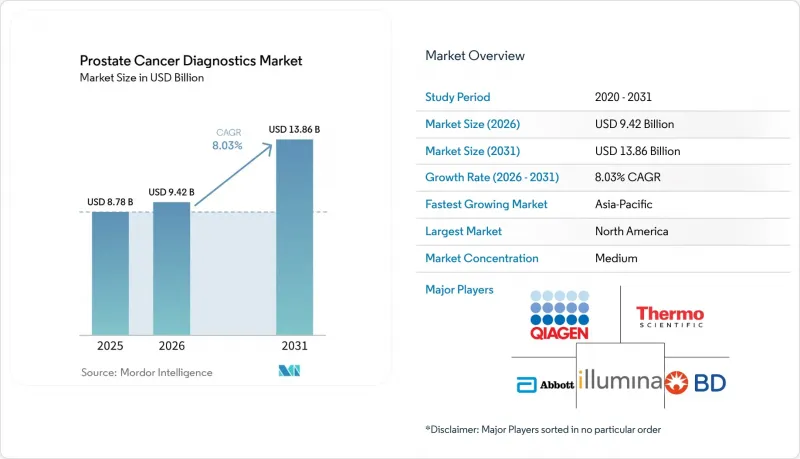

Mordor Intelligence에 의하면, 전립선암 진단 시장 규모는 2025년에 87억 8,000만 달러로 평가되었고 2026년 94억 2,000만 달러에서 2031년까지 138억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.03%를 나타낼 전망입니다.

본 보고서는 진단 기술(PSA/바이오마커 검사, MRI/MpMRI, 생검, 분자/유전체 검사, PSMA PET/CT), 검체 유형(혈액, 조직, 소변, 타액), 암의 유형, 병기, 최종 사용자(병원 비뇨기과, 종양 검사실, 영상 진단센터, 비뇨기과 클리닉, 연구 기관), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

전 세계 전립선암 진단 시장 동향 및 인사이트

전립선암 검진 건수 증가

전립선암 진단 시장은 여러 국가에서 체계적 및 비체계적인 선별 검사 활동이 광범위하게 증가하고 있는 데 힘입어 성장하고 있습니다. 현재 185개국 중 118개국에서 전립선암은 남성에게서 가장 많이 진단되는 암으로, 이는 의료 체계가 잘 발달된 국가와 선별 검사가 미흡한 국가 모두에서 보다 일상적인 검사 경로의 필요성을 뒷받침하고 있습니다. 일본의 2025년판 임상 진료 지침에서는 중년 남성을 대상으로 한 PSA 선별검사를 권장하는 최초의 "약한 권장"이 도입됨에 따라, 오랫동안 불투명했던 공식 지침에서 명확한 전환이 나타났습니다. 미국에서는 1993년부터 2022년 사이에 전립선암 사망률이 50% 감소했으며, 조기 발견의 중요성은 여전히 선별검사에 대한 결정에서 핵심적인 위치를 차지하고 있습니다. 롬바르디아주에서 실시된 다단계 선별검사의 시범 사업에서는 2025년 6월까지 8,558명의 남성이 등록되었으며, 과잉진단의 징후는 나타나지 않은 채 15.9%의 의뢰율이 기록되었습니다. 이는 전립선암 진단 시장에서 도시 지역의 선별검사를 확대하기 위한 실질적인 모델을 제시하고 있습니다. 선별 검사 건수 증가는 보다 광범위한 전립선암 진단 시장 전반에 걸쳐 PSA 시약, 추적 바이오마커 검사, 영상 진단, 생검에 대한 지속적인 수요를 뒷받침하고 있습니다.

고도의 바이오마커 검사 및 영상 진단 검사에 대한 보험 적용 범위 확대

전립선암 진단 시장은 임상의와 검사 기관의 검사 의뢰 시 발생하는 불확실성을 줄여주는 보험 적용 결정에 힘입어 성장하고 있습니다. CMS는 2025년 7월 3일부터 발효되는 “Decipher 전립선암 분류 분석법”에 관한 지역별 보험 적용 결정(LCD)을 갱신하여, NCCN 기준에 부합하는 조건 하에서 잔여 수명이 10년 이상으로 예상되는 국소성 전립선암 환자에 대한 사용을 보험 적용 대상으로 지정했습니다. 분자 검사가 보험 적용 대상이 되면, 유사한 검사 도구들도 보험사가 이미 인지하고 있는 기준에 따라 그 가치를 입증하기가 더 쉬워집니다. 이러한 경향은 첨단 영상 진단 분야에서도 마찬가지로 중요하며, 보험 적용 변경은 전립선암 진단 시장 전반의 의뢰 행태, 예산 계획 및 공급업체의 투자 결정에 영향을 미치기 때문입니다. 특히 미국이나 그 밖의 보험 적용 주도형 시장에서 보험 적용 방침이 일상적인 임상 경로에 신속하게 반영되는 시스템에서는 그 직접적인 영향이 더욱 두드러집니다. 장기적으로는 이를 통해 임상적 열의만으로는 얻을 수 없는 전립선암 진단 시장을 위한 보다 안정적인 상업적 기반이 마련될 것입니다.

고도의 진단 검사에서 발생하는 고액의 본인 부담금

전립선암 진단 시장은 첨단 검사 분야에서 여전히 뚜렷한 경제적 장벽에 직면해 있습니다. ASCO의 2025년 지침에 따르면, ctDNA 액체 생검 검사의 가격은 1회당 1,000-3,000달러이며, 유전체 분류 검사도 대개 비슷한 가격대에 속하는 것으로 알려져 있습니다. 이러한 가격 수준은 강력한 보상 체계가 마련되지 않은 환경에서는 의사의 검사 의뢰와 환자의 진료 의욕을 모두 저해할 가능성이 있습니다. 접근성 격차는 금전적인 측면에만 그치지 않습니다. 『Cancer Imaging』지에 게재된 2025년 메디케어 청구 데이터 조사에 따르면, 지방에 거주하는 환자들의 PSMA-PET 이용률은 현저히 낮은 것으로 나타났으며, 특히 지방에 거주하는 흑인 환자들 사이에서 그 격차가 가장 두드러진 것으로 밝혀졌습니다. 이는 고도의 검사 실시 건수가 보험 가입자, 도시 지역 주민, 그리고 대학 병원과 연계된 환자층에 여전히 집중되어 있음을 의미합니다. 이러한 집중으로 인해 전립선암 진단 시장이 더 광범위한 인구 집단에서 이 질환이 실제로 미치는 역학적 부담을 어느 정도까지 반영할 수 있는지에 한계가 있습니다.

부문별 분석

2025년 기준으로 PSA 및 바이오마커 검사는 전립선암 진단 시장의 46.31%를 차지했으나, PSMA-PET 및 CT 영상 진단은 2031년까지 연평균 성장률(CAGR) 8.68%로 성장할 것으로 전망됩니다. PSA 검사는 확장성이 뛰어나고 비용이 저렴하며, 1차 진료 및 의뢰 경로에 널리 도입되어 있어 여전히 전립선암 진단 시장의 광범위한 검사량을 뒷받침하는 기반이 되고 있습니다. PSMA-PET는 그 역할이 병기 판정의 정확도 및 이후 치료법 선택과 더욱 밀접하게 연관되어 있기 때문에 지금까지와는 다른 위치를 차지하게 되었습니다. 『Journal of Nuclear Medicine』의 데이터에 따르면, 지침에 따른 지원이 강화된 결과, VA(재향군인부) 의료 시스템에서 고위험 및 극히 고위험 환자에 대한 PSMA-PET 사용률은 2023년 중반까지 70%에 달했습니다. MRI 및 mpMRI는 특히 임상적으로 중요한 질환의 검출을 유지하면서 불필요한 생검 건수를 줄이고자 하는 의료 시스템에서 생검 전 선별 도구로서의 가치를 지속적으로 높여가고 있습니다.

전립선암 진단 시장 전반에서 생검 및 조직병리학은 확정 진단, 악성도 분류 및 아형 평가에 있어 여전히 핵심적인 역할을 수행하고 있습니다. 더 중요한 변화는 영상 진단이 병리 진단 이후뿐만 아니라 생검 전이나 치료 방침 결정 시에도 더 강력한 임상적 권위를 갖게 되었다는 점입니다. PSMA-PET는 진단과 테라노스틱스(치료와 진단을 통합한 접근법)의 경로를 연결하기 때문에 단순한 영상 진단의 범위를 넘어 그 중요성이 커지고 있습니다. 이로 인해 전립선암 진단 업계는 임상적 근거, 추적자 공급, 보험 급여 및 의사 교육을 동시에 조화시킬 수 있는 공급업체에 대한 의존도가 높아지고 있습니다. 한편, PSA 및 관련 바이오마커 검사는 대상 인구의 폭과 재검사 빈도 면에서 다른 플랫폼이 따라올 수 없기 때문에 앞으로도 계속해서 가장 큰 기술 범주로 남을 가능성이 높다고 볼 수 있습니다.

2025년 전립선암 진단 시장 규모에서 혈액 유래 검체가 46.68%를 차지했으나, 조직 검체는 2031년까지 연평균 성장률(CAGR) 10.12%를 기록하며 가장 빠르게 성장하고 있는 검체 유형입니다. PSA 검사가 여전히 전립선암 진단 시장에서 가장 많은 정기 검사 건수를 차지하고 있으며, 또한 ctDNA가 진행성 암 관리에서 혈액의 역할을 확대함에 따라 혈액 검체는 계속해서 주류로서의 지위를 유지하고 있습니다. 조직 검체의 활용이 가속화되고 있는 이유는 치료법 선택이 점점 더 면역조직화학 및 유전체 프로파일링에 의존하게 되었으며, 이러한 방법은 반드시 체액 생검으로 대체될 수 있는 것은 아니기 때문입니다. 이에 따라 조직 검체는 기존의 확정 진단이라는 역할에서 특정 환자에 대한 지속적인 정밀 종양학의 역할로 전환되고 있습니다. 소변 검체를 이용한 진단법 또한 검체 채취의 장벽이 낮은 모델에 적합하며, 생검 전 위험도 선별을 정교화하는 데 도움이 될 가능성이 있어, 진단 과정의 말단 단계에서 분산형 접근법으로 주목받고 있습니다.

현재의 검체 구성은 단일하고 지배적인 검체 논리라기보다는 전립선암 진단 시장 내의 보다 다층적인 임상 경로를 반영하고 있습니다. 혈액은 선별 검사 및 정기적인 모니터링에서 여전히 주요한 진입점 역할을 하고 있습니다. 조직 검체는 치료 계획 수립이나 보다 신뢰할 수 있는 질환 분류를 위해 의사가 상세한 특성 평가가 필요한 경우 그 중요성이 커집니다. 소변 검사는 PSA 검사 결과와 침습적 검사 사이에 비침습적인 단계를 원하는 의료진에게 최적의 선택지인 반면, 타액 및 기타 생체 검체는 일상적인 사용이 제한적인 초기 단계의 선택지에 그치고 있습니다. 이러한 검체 구성은 여러 검체 유형에 걸쳐 사업을 전개하며, 전립선암 진단 업계에서 대량 검사와 높은 특이도를 겸비한 후속 의사결정을 모두 지원할 수 있는 기업에 유리하게 작용합니다.

지역별 분석

2025년, 북미는 전립선암 진단 시장 점유율의 43.64%를 차지하며, 금액 기준으로 가장 큰 기여를 한 지역이 되었습니다. 이 지역은 PSA 검사의 높은 보급률, 탄탄한 전문의 인프라, 그리고 유전체 분류법 및 첨단 영상 진단에 대한 지원을 점차 확대하고 있는 보험 급여 환경의 혜택을 누리고 있습니다. 미국에서만 2026년에는 33만 3,830건의 전립선암 신규 환자가 발생할 것으로 예상되며, 이에 따라 선별검사, 병기 분류, 경과 관찰에 이르는 매우 대규모의 검사 체계가 유지될 것입니다. 특정 유전체 분석 도구에 대한 CMS(미국 의료보험서비스센터)의 보험 적용 및 고위험 환자군에서의 PSMA-PET 보급이 확대됨에 따라, 전립선암 진단 시장에서 북미의 주도적 입지가 더욱 공고해지고 있습니다. 캐나다는 각 주의 암 대책 프로그램 간 협력을 통해 혜택을 누리고 있지만, 주요 학술 의료 센터를 제외하면 첨단 영상 진단 기술의 보급률은 여전히 낮은 실정입니다. 한편, 멕시코는 여전히 PSA 검사를 중심으로 하는 경향이 강하며, 첨단 영상 진단은 민간 의료기관 네트워크에 집중되어 있습니다.

유럽은 임상 측면에서 높은 수준을 유지하고 있지만, 선별 검사 방침, 보험 적용 범위, 도입 속도가 국가마다 크게 다르기 때문에 전립선암 진단 시장은 더욱 불균일한 상황에 놓여 있습니다. 독일의 고위험 병기 분류 프로토콜과 보다 광범위한 EU 규제 환경은 검증된 검사 포트폴리오를 보유한 확고한 입지공급업체에 유리하게 작용하고 있습니다. 영국에서 전립선 생검 전의 "MRI 우선" 접근법은 진단의 질을 유지하면서 불필요한 처치를 제한하는 모델로 널리 인정받게 되었습니다. 스웨덴 역시 표준화된 위험도 계층화 프로토콜을 활용한 지역 기반의 체계적인 전립선암 검진 프로그램을 통해 근거를 축적하고 있습니다. 프랑스, 스페인, 이탈리아에서는 체계적인 PSA 검사의 접근성이 확대되고 있으며, 롬바르디아주의 시범 사업 결과는 대규모 도시 지역에서 선별 검사 모델이 도입 초기 단계에서 명백한 과잉 진단을 초래하지 않으면서도 확대될 수 있음을 보여주고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역이며, 선별 검사 및 진단 인프라가 질병 부담에 발맞추어 발전함에 따라, 이 지역의 전립선암 진단 시장 규모는 2031년까지 연평균 성장률(CAGR) 9.96%로 확대될 것으로 전망됩니다. 중국 전립선암 환자의 60% 이상이 진행기로 진단되는 반면, 미국에서는 약 70%가 국소기 또는 국소 진행기로 진단되고 있어, 이 지역에서 선별 검사의 미비 및 병기 분류의 미흡이 얼마나 심각한지 여실히 드러나고 있습니다. 일본에서는 2025년 지침 개정에 따라 PSA를 이용한 개별 선별 검사로 전환되었으며, 중국에서는 전립선 건강 지수(Prostate Health Index)를 뒷받침하는 근거가 제시됨에 따라, 두 지역 모두에서 해당 검사의 보급 촉진에 기여하고 있습니다. 인도, 한국, 호주는 향후 더 큰 성장 잠재력을 지니고 있으며, 중동 및 아프리카 및 남미 지역에서는 민간 네트워크, 목표 지향적 파트너십, 그리고 첨단 영상 진단 및 분자 검사에 대한 선별적 투자의 견인 아래, 소규모 기반에서 지속적으로 성장하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the prostate cancer diagnostics market size was valued at USD 8.78 billion in 2025 and is estimated to grow from USD 9.42 billion in 2026 to reach USD 13.86 billion by 2031, at a CAGR of 8.03% during the forecast period (2026-2031).

This report is Segmented by Diagnostic Technology (PSA/Biomarker Testing, MRI/MpMRI, Biopsy, Molecular/Genomic Testing, PSMA PET/CT), Sample Type (Blood, Tissue, Urine, Saliva), Cancer Type, Stage, End User (Hospital Urology, Oncology Labs, Imaging Centers, Urology Clinics, Research), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Value (USD).

Global Prostate Cancer Diagnostics Market Trends and Insights

Rising Prostate Cancer Screening Volume

The prostate cancer diagnostics market is gaining from a broader rise in organized and semi-organized screening activity across several countries. Prostate cancer is now the most commonly diagnosed cancer in men in 118 of 185 countries, which supports the need for more routine testing pathways in both mature and under-screened health systems. Japan's 2025 clinical practice guidelines introduced the first weak recommendation in favor of PSA screening for middle-aged men, which marked a clear shift from the long period of uncertain official guidance. In the United States, the prostate cancer death rate fell by 50% between 1993 and 2022, which keeps the case for earlier detection central to screening decisions. Lombardy's multilevel screening pilot enrolled 8,558 men by June 2025 and recorded a 15.9% referral rate without evidence of overdiagnosis, which gives the prostate cancer diagnostics market a practical model for urban screening scale-up. Higher screening volume supports repeat demand for PSA reagents, follow-on biomarker work, imaging, and biopsy across the wider prostate cancer diagnostics market.

Expanding Reimbursement for Advanced Biomarker and Imaging Tests

The prostate cancer diagnostics market is also being lifted by coverage decisions that reduce ordering uncertainty for clinicians and laboratories. CMS updated its Local Coverage Determination for the Decipher Prostate Cancer Classifier Assay, effective July 3, 2025, and that decision covered use in localized prostate cancer patients with at least 10 years of life expectancy under NCCN-aligned criteria. Once a molecular test gains reimbursement, it becomes easier for similar tools to frame their own value in terms that payers already recognize. The same pattern matters for advanced imaging, because reimbursement changes shape referral behavior, budget planning, and vendor investment decisions across the prostate cancer diagnostics market. The direct effect is stronger in systems where coverage policy quickly translates into everyday clinical pathways, especially in the United States and other reimbursement-led markets. Over time, this creates a more stable commercial floor for the prostate cancer diagnostics market than clinical enthusiasm alone could provide.

High Out-of-Pocket Cost for Advanced Diagnostics

The prostate cancer diagnostics market still faces a clear affordability barrier in advanced testing categories. ASCO's 2025 guideline noted that ctDNA liquid biopsy tests are priced at USD 1,000 to USD 3,000 per test, and genomic classifiers often fall into a similar range. Those price levels can suppress both physician ordering and patient uptake outside strong reimbursement frameworks. Access differences are not only financial, because a 2025 Medicare claims study in Cancer Imaging found materially lower PSMA PET use among rural patients and the sharpest gap among Black patients in rural settings. This means advanced testing volume remains concentrated in insured, urban, and academically linked populations. That concentration limits how fully the prostate cancer diagnostics market can reflect the true epidemiological burden of disease across broader populations.

Other drivers and restraints analyzed in the detailed report include:

- Liquid Biopsy and Genomic Testing Uptake

- Variable Clinical Utility and PSA Overdiagnosis Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PSA and biomarker testing held 46.31% of the prostate cancer diagnostics market share in 2025, while PSMA PET and CT imaging is projected to grow at an 8.68% CAGR through 2031. PSA-based testing remains the broad volume base of the prostate cancer diagnostics market because it is scalable, low-cost, and widely embedded in primary care and referral pathways. PSMA PET has moved into a different position because its role is now tied more closely to staging quality and downstream treatment selection. Journal of Nuclear Medicine data showed that PSMA PET use among high-risk and very-high-risk patients in the VA system had risen to 70% by mid-2023 after guideline support strengthened. MRI and mpMRI continue to gain value as pre-biopsy triage tools, especially in health systems that want to reduce unnecessary biopsy volume while preserving detection of clinically significant disease.

Biopsy and histopathology still remain central to definitive diagnosis, grading, and subtype assessment across the prostate cancer diagnostics market. The more important change is that imaging now has stronger clinical authority before biopsy and around therapy decisions, rather than only after pathology. PSMA PET carries added relevance because it links diagnosis with theranostic pathways, which raises its importance beyond a single imaging event. This makes the prostate cancer diagnostics industry more dependent on vendors that can align clinical evidence, tracer supply, reimbursement, and physician education at the same time. At the same time, PSA and related biomarker tests are likely to remain the largest technology category because no other platform matches their population-level reach and repeat-testing frequency.

Blood-based samples represented 46.68% of the prostate cancer diagnostics market size in 2025, while tissue is the fastest-growing sample type with a 10.12% CAGR through 2031. Blood remains dominant because PSA testing still drives the highest routine volume in the prostate cancer diagnostics market, and ctDNA has widened the role of blood in advanced disease management. Tissue is growing faster because treatment selection increasingly depends on immunohistochemistry and genomic profiling that cannot always be replaced by liquid biopsy. This shifts tissue from a traditional confirmation role toward a recurring precision-oncology role in selected patients. Urine-based diagnostics are also drawing interest at the decentralized end of the pathway because they can fit low-friction collection models and may help refine pre-biopsy risk selection.

The sample mix now reflects a more layered clinical pathway inside the prostate cancer diagnostics market rather than a single dominant specimen logic. Blood remains the main entry point for screening and routine monitoring. Tissue becomes more important when physicians need deeper characterization for therapy planning or for higher-confidence disease classification. Urine fits best where providers want a noninvasive step between PSA signal and invasive workup, while saliva and other biospecimens remain early-stage options with limited routine use. This mix favors companies that can operate across more than one sample type and support both broad-volume testing and high-specificity downstream decisions in the prostate cancer diagnostics industry.

Complete Report Scope:

- By Diagnostic Technology

- PSA and Biomarker Testing

- MRI and mpMRI Imaging

- Biopsy and Histopathology

- Molecular and Genomic Testing

- PSMA PET and CT Imaging

- By Sample Type

- Blood

- Tissue

- Urine

- Saliva and Other Biospecimens

- By Cancer Type

- Prostatic Adenocarcinoma

- Small Cell Carcinoma

- Interstitial Cell Carcinoma

- Other Prostate Cancer Types

- By Stage

- Localized Prostate Cancer

- Recurrent and Advanced Prostate Cancer

- Castration-Resistant Prostate Cancer

- By End User

- Hospital Urology Departments

- Oncology Reference Laboratories

- Diagnostic Imaging Centers

- Urology Clinics

- Research and Academic Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 43.64% of the prostate cancer diagnostics market share in 2025, which made it the leading regional contributor by value. The region benefits from high PSA testing penetration, strong specialist infrastructure, and a reimbursement environment that is gradually expanding support for genomic classifiers and advanced imaging. The United States alone is expected to record 333,830 new prostate cancer cases in 2026, which sustains a very large testing base across screening, staging, and follow-up. CMS coverage for selected genomic tools and strong uptake of PSMA PET in higher-risk patients strengthen North America's leadership in the prostate cancer diagnostics market. Canada benefits from coordinated provincial cancer programs but still shows less advanced imaging depth outside major academic centers, while Mexico remains more PSA-centric with advanced imaging concentrated in private networks.

Europe remains clinically sophisticated, but the prostate cancer diagnostics market is more uneven there because screening policy, reimbursement depth, and implementation speed vary widely by country. Germany's high-risk staging pathways and the wider EU regulatory environment favor established vendors with validated assay portfolios. The United Kingdom's MRI-first approach before prostate biopsy has become a recognized model for limiting unnecessary procedures while preserving diagnostic quality. Sweden is also building evidence through region-based organized prostate cancer testing programs with standardized risk-stratified protocols. France, Spain, and Italy are expanding structured PSA access, and Lombardy's pilot results show that large urban screening models can scale without obvious overdiagnosis in early implementation.

Asia-Pacific is the fastest-growing region, and the prostate cancer diagnostics market size there is projected to rise at a 9.96% CAGR through 2031 as screening and diagnostic infrastructure catch up with disease burden. More than 60% of prostate cancer patients in China are diagnosed at advanced stages, while the United States diagnoses around 70% at localized or regional stages, which highlights the scale of under-screening and under-staging in the region. Japan's 2025 guideline shift toward individual PSA screening and Chinese evidence supporting the Prostate Health Index both support stronger test adoption in the region. India, South Korea, and Australia add further growth potential, while the Middle East and Africa and South America continue to expand from smaller bases with uptake led by private networks, targeted partnerships, and selective investment in advanced imaging and molecular testing.

- Abbott Laboratories

- Agilent Technologies

- Beckton Dickinson

- bioMerieux

- Danaher

- DiaSorin

- Exact Sciences

- Roche

- GE HealthCare Technologies Inc.

- Hologic

- Illumina

- LabCorp

- Lantheus Holdings, Inc.

- MDxHealth SA

- Myriad Genetics

- Opko Health

- Proteomedix AG

- QIAGEN

- Quest Diagnostics

- Siemens Healthineers

- Thermo Fisher Scientific

- Veracyte, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prostate Cancer Screening Volume

- 4.2.2 Shift Toward Multimodal Diagnostic Pathways

- 4.2.3 Expanding Reimbursement for Advanced Biomarker and Imaging Tests

- 4.2.4 Decentralization of Testing to Outpatient and Ambulatory Settings

- 4.2.5 AI-Enabled Imaging and Risk Stratification Adoption

- 4.2.6 Liquid Biopsy and Genomic Testing Uptake

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Cost for Advanced Diagnostics

- 4.3.2 Variable Clinical Utility and PSA Overdiagnosis Concerns

- 4.3.3 Limited Access to Advanced Diagnostics in Price-Sensitive Markets

- 4.3.4 Workflow and Integration Complexity Across Legacy Care Settings

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Diagnostic Technology

- 5.1.1 PSA and Biomarker Testing

- 5.1.2 MRI and mpMRI Imaging

- 5.1.3 Biopsy and Histopathology

- 5.1.4 Molecular and Genomic Testing

- 5.1.5 PSMA PET and CT Imaging

- 5.2 By Sample Type

- 5.2.1 Blood

- 5.2.2 Tissue

- 5.2.3 Urine

- 5.2.4 Saliva and Other Biospecimens

- 5.3 By Cancer Type

- 5.3.1 Prostatic Adenocarcinoma

- 5.3.2 Small Cell Carcinoma

- 5.3.3 Interstitial Cell Carcinoma

- 5.3.4 Other Prostate Cancer Types

- 5.4 By Stage

- 5.4.1 Localized Prostate Cancer

- 5.4.2 Recurrent and Advanced Prostate Cancer

- 5.4.3 Castration-Resistant Prostate Cancer

- 5.5 By End User

- 5.5.1 Hospital Urology Departments

- 5.5.2 Oncology Reference Laboratories

- 5.5.3 Diagnostic Imaging Centers

- 5.5.4 Urology Clinics

- 5.5.5 Research and Academic Institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Agilent Technologies, Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 bioMerieux SA

- 6.3.5 Danaher Corporation

- 6.3.6 DiaSorin S.p.A.

- 6.3.7 Exact Sciences Corporation

- 6.3.8 F. Hoffmann-La Roche AG

- 6.3.9 GE HealthCare Technologies Inc.

- 6.3.10 Hologic, Inc.

- 6.3.11 Illumina, Inc.

- 6.3.12 Laboratory Corporation of America Holdings

- 6.3.13 Lantheus Holdings, Inc.

- 6.3.14 MDxHealth SA

- 6.3.15 Myriad Genetics, Inc.

- 6.3.16 OPKO Health, Inc.

- 6.3.17 Proteomedix AG

- 6.3.18 QIAGEN N.V.

- 6.3.19 Quest Diagnostics Incorporated

- 6.3.20 Siemens Healthineers AG

- 6.3.21 Thermo Fisher Scientific Inc.

- 6.3.22 Veracyte, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment