|

시장보고서

상품코드

2073097

TCFD 기후 공시 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)TCFD Climate Disclosure Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

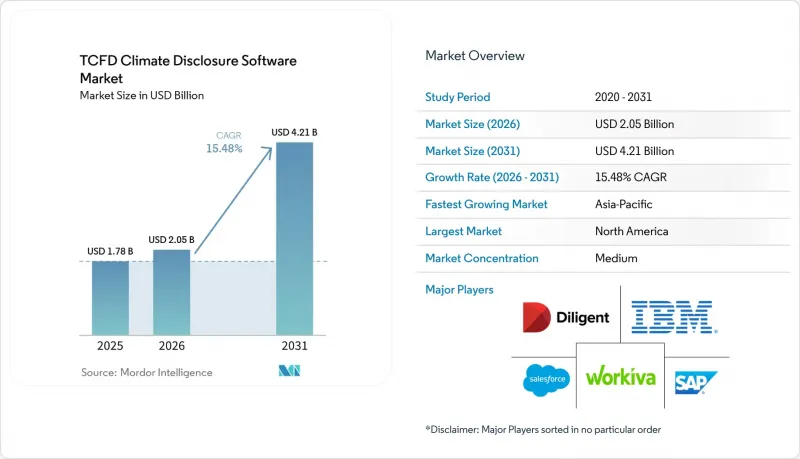

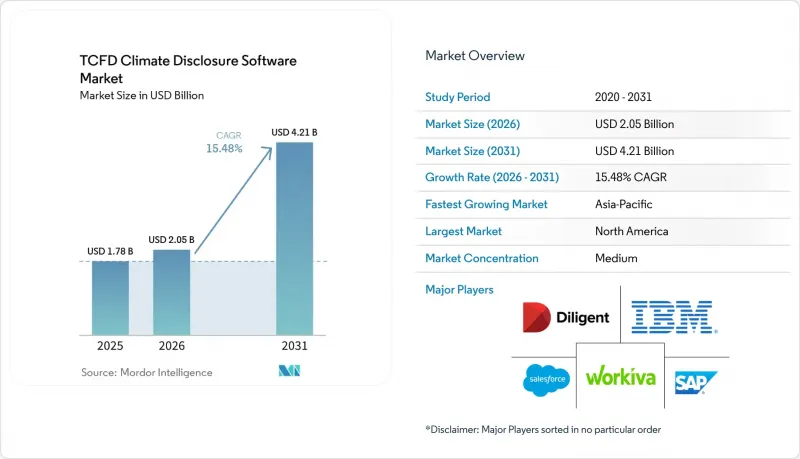

Mordor Intelligence에 의하면, TCFD 기후 공시 소프트웨어 시장 규모는 2025년에 17억 8,000만 달러, 2026년에 20억 5,000만 달러되어, 2031년까지 42억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 15.48%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 기업 규모(대기업 및 중소기업), 용도(공시 데이터 관리, 공시 보고 등), 최종 사용자 산업(공업 제조 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 TCFD 기후 공시 소프트웨어 시장 동향 및 인사이트

자본 시장 전반에 걸친 기후 변화 정보 공시 의무화 확대

TCFD 기후 공시 소프트웨어 시장은 주요 자본 시장 전반에 걸쳐 의무적인 보고 규정이 확산됨에 따라 가장 직접적인 성장 동력을 얻고 있습니다. CSRD(유럽 지속가능성 보고 지침)에 따라, EU 내 최대 규모의 공익 기업은 2024 회계연도부터 ESRS(유럽 지속가능성 보고 기준)에 부합하는 보고를 실시하게 되었으며, 2026년에 개정된 적용 기준의 변경으로 인해 현재 대상 범위에 남아 있는 최대 기업들을 중심으로 지출이 집중되고 있습니다. 캘리포니아주의 SB 253 법안은 미국 내 새로운 수요층을 창출하는 것으로, 해당 주에서 사업을 영위하며 연간 기업 매출이 10억 달러를 초과하는 기업에 대해 스코프 1 및 스코프 2 배출량의 공개를 의무화하고 있습니다. 캘리포니아주 대기자원국(CARB)은 2025년 9월의 잠정 목록에서 약 2,600개의 사업체를 선정했습니다. TCFD 기후 공시 소프트웨어 시장에서도 많은 제출 기한이 짧은 기간에 집중되어 있어, 구매 유예 기간이 단축되고 있습니다. 이로 인해 기업들은 플랫폼 도입을 결정하기 전에 제품의 성숙을 기다릴 수 있는 시간이 줄어들고 있습니다. 이러한 상황으로 인해 TCFD 기후 공시 소프트웨어 시장에서는 수동 설정이 아닌 네이티브 형식으로 CSRD, ESRS, ISSB S1 및 S2, GRI, TCFD, SASB에 대한 매핑을 이미 지원하는 벤더가 확실히 선호되고 있습니다. 그 결과, 폭넓은 프레임워크에 대한 지원은 단순한 제품 기능에 그치지 않고, 단기적인 구매 결정 요인이 되고 있습니다.

투자자 및 규제 당국의 면밀한 검토에 대비한 감사 대응이 가능한 데이터 추적 기록

TCFD 기후 공시 소프트웨어 시장은 서술형 지속가능성 보고에서 구조화되고 검증된 정보 공개로 전환됨에 따라 재편되고 있습니다. SEC의 기후 관련 규정에서는 대규모 가속 제출 기업에 대한 스코프 1 및 스코프 2 배출량 보고와 관련해, 2025 회계연도부터 제3자에 의한 인증이 의무화되었습니다. 이에 따라 데이터 계보(데이터 리니지)와 증거 관리가 소프트웨어 선정의 핵심이 되고 있습니다. 영국 중앙은행과 프루덴셜 규제 당국도 2025년에 유사한 방향성을 제시하며, 은행 및 보험사에 대한 정량화된 기후 관련 재무적 영향에 대한 감독상의 기대치를 높였습니다. 이로 인해 추적 가능하고 버전 관리가 이루어지는 데이터 흐름에 대한 필요성이 커지고 있습니다. TCFD 기후 공시 소프트웨어 시장에서 이는 구매 결정의 근거를 바꾸고 있습니다. 왜냐하면 플랫폼은 더 이상 단순히 ESG 데이터를 얼마나 잘 수집할 수 있는지에 그치지 않고, 보증 절차의 마찰을 얼마나 줄일 수 있는지에 대해서도 평가받게 되었기 때문입니다. 구조화된 역할 기반 시스템에 증거를 보관하는 기업은 외부 검증자의 부담을 줄일 수 있으며, 이는 도입 후 감사 업무의 부담 경감으로 이어집니다. 이로 인해 TCFD 기후 공시 소프트웨어 시장에서 프리미엄 가격 책정의 정당성을 주장하기가 더 쉬워졌습니다. 왜냐하면 소프트웨어 설계가 단순한 보고의 편의성뿐만 아니라 규정 준수 비용에도 영향을 미치게 되었기 때문입니다.

공급업체 및 포트폴리오 네트워크 전반에 분산된 기후 데이터

TCFD 기후 공시 소프트웨어 시장은 여전히 근본적인 제약에 직면해 있습니다. 바로, 신뢰도가 가장 낮은 데이터가 대개 보고 대상 기업 외부에 존재한다는 점입니다. Sphera는 2025년 조사에서 스코프 3에 대해 보고하는 기업의 57%가 공급업체별 데이터를 부분적인 정보원으로만 활용하고, 많은 공백을 업계 평균 계수로 메우고 있음을 밝혔습니다. 이로 인해 보고 플랫폼이 아무리 정교하더라도 정확도에는 한계가 생깁니다. 즉, TCFD 기후 공시 소프트웨어 시장은 워크플로우, 계산, 검증 프로세스를 자동화할 수는 있지만, 그것만으로는 업스트림 공정에서 발생하는 측정 품질 저하 문제를 완전히 해결할 수는 없습니다. 그 결과, 하류 보고서는 배출량을 직접 측정하지 않고 여전히 추정에 의존하는 공급업체에 계속 의존하고 있기 때문에 공시의 질에는 한계가 생깁니다. GHG 프로토콜 및 WBCSD의 상호운용성 노력에 힘입어 데이터 교환의 기술적 기반은 점차 개선되고 있지만, 1차 공급업체 데이터의 근본적인 확보 가능성에 대해서는 여전히 장기적인 전환 기간이 필요한 과제로 남아 있습니다. 이 때문에 제품의 기능은 지속적으로 향상되고 있음에도 불구하고, 데이터의 신뢰성 문제는 TCFD 기후 공시 소프트웨어 시장의 제약 요인으로 남아 있습니다.

부문별 분석

2025년, TCFD 기후 공시 소프트웨어 시장에서 소프트웨어가 매출 점유율의 71.43%를 차지하며 시장을 독점했습니다. 이는 플랫폼 라이선싱이 여전히 핵심 비즈니스 모델임을 뒷받침합니다. TCFD 기후 공시 소프트웨어 시장의 주요 공급업체들은 데이터 양, 대상 기업수, 그리고 현재 운영 중인 보고 프레임워크에 연동된 SaaS 구독 모델을 계속해서 채택하고 있습니다. 이 모델이 효과적인 이유는 기후 데이터를 재무 및 리스크 관리 프로세스에 연계하는 기업은 해당 시스템을 중심으로 관리 체계, 업무 흐름, 내부 승인 프로세스가 구축되면 동일한 시스템을 계속 사용하는 경향이 있기 때문입니다. 소프트웨어 계층의 강점은 템플릿의 정기적인 업데이트, 데이터 가져오기, 권한 관리, 그리고 여러 기준에 걸친 공개 매핑의 필요성을 반영하고 있습니다. 실용적인 관점에서 보더라도, 소프트웨어는 보고, 검증, 감사 준비가 일체화된 운영 환경을 구축하기 위해 여전히 가치 제안의 핵심을 이루고 있습니다.

서비스 부문은 TCFD 기후 공시 소프트웨어 시장에서 여전히 가장 빠르게 성장하고 있는 분야로, 2031년까지 연평균 성장률(CAGR)이 17.67%를 나타낼 것으로 전망됩니다. 수요가 증가하고 있는 배경에는 구매자가 도입 지원, 배출량 데이터 통합, 워크플로우 설계, 보증 준비, 그리고 기준의 변화에 따른 지속적인 설정 변경을 필요로 하고 있기 때문입니다. GHG 프로토콜의 스코프 3 개정 과정 역시 이러한 필요성을 더욱 높이고 있습니다. 기업은 배출 데이터의 분류 방법과 품질 수준별 검증 방법을 재검토해야 하기 때문입니다. 이로 인해, 특히 여러 사업체나 공시 체계를 보유한 대규모 보고 그룹의 경우, 최초 가동일로부터 상당한 시간이 지난 후에도 도입 후 작업이 계속될 것입니다. 그 결과, 기후 변화 정보 공개 소프트웨어 업계에서는 소프트웨어 판매와 전문 서비스 간의 연계가 더욱 강화되고 있으며, 공급업체들은 개별 라이선스 대신 번들형 서비스를 제공하는 방향으로 나아가고 있습니다.

2025년에는 클라우드 기반 솔루션이 TCFD 기후 공시 소프트웨어 시장에서 66.28%의 점유율을 차지하며 시장을 주도했습니다. 이는 확장성과 컨텐츠의 신속한 업데이트에 대한 구매자들의 강한 선호도를 반영하고 있습니다. 벤더가 고객 측의 IT 주기를 기다리지 않고도 공시 템플릿이나 규제 매핑을 업데이트할 수 있기 때문에 클라우드 제공은 TCFD 기후 공시 소프트웨어 시장에서 표준적인 선택지로 자리 잡고 있습니다. 이는 끊임없이 변화하는 규제 환경에서 중요한 의미를 지닙니다. 이는 구매자가 수작업에 의존하는 우회 방안이 아니라, 가동 중인 시스템에서 최신 CSRD, ISSB 및 ESRS 컨텐츠를 필요로 하기 때문입니다. 또한, 클라우드 모델은 여러 사업 부문이나 관할 구역에 걸쳐 통합된 보고를 원하는 기업의 인프라 부담을 줄여줍니다. 따라서 속도, 표준화 및 유지보수 부담 경감을 중시하는 조직에게 있어 가장 실용적인 선택지로서 우위를 유지하고 있습니다.

하이브리드 시장 규모는 2031년까지 연평균 성장률(CAGR) 17.21%로 확대될 것으로 예상되며, 이는 클라우드 도입이 확대되는 상황에서도 관리상의 우려가 여전히 중요한 문제임을 보여줍니다. 구매자는 기밀성이 높은 재무 기록과 일부 Scope 3 산정을 통제된 환경 내에 보관하는 한편, 협업 및 공개 워크플로우에는 클라우드 계층을 활용하기 위해 하이브리드 설계를 채택하고 있습니다. Quentic사는 보고의 투명성과 현지화, 그리고 관리상의 요구 사항 사이에서 균형을 맞추어야 하는 기업들에게 있어, 독일의 데이터 거버넌스에 대한 기대가 이러한 접근 방식의 매력을 높일 가능성이 있다고 지적했습니다. On-Premise형 도입은 TCFD 기후 공시 소프트웨어 시장에서 여전히 일정한 역할을 수행하고 있으며, 주로 데이터 주권이 특히 중요시되는 정부 기관이나 규제가 엄격한 금융 분야에서 볼 수 있습니다. SAP의 제품 전략도 이와 유사한 경향을 보이고 있으며, 모든 고객에게 단일 아키텍처를 강요하기보다는 기업 통합에 대한 다양한 선택지를 계속해서 지원하고 있습니다.

지역별 분석

2025년, 북미는 TCFD 기후 공시 소프트웨어 시장 점유율의 36.14%를 차지하며, 지역별로는 가장 큰 기여도를 보였습니다. 이 지역의 TCFD 기후 공시 소프트웨어 시장을 주도하고 있는 것은 미국이며, 미국에서는 SEC의 기후 관련 규정에 따라 2025 회계연도부터 대규모 가속 공개 기업에 대해 배출량 공개 및 입증 요건이 부과되게 되었습니다. 캘리포니아주의 SB 253 및 SB 261에 따라, 대상 구매자층이 SEC 등록 기업을 넘어 확대됨에 따라, 유연한 템플릿 라이브러리와 강력한 다중 프레임워크 매핑 기능을 갖춘 플랫폼이 우위를 점하는 2단계 규정 준수 환경이 조성되었습니다. 북미의 TCFD 기후 공시 소프트웨어 시장은 규제 변화에도 불구하고 지속되는 투자자들의 압력으로부터도 혜택을 받고 있으며, 이로 인해 단순한 규제 기반 수요 패턴보다 도입 기반이 더욱 견고해지고 있습니다.

유럽은 2026년 CSRD 적용 범위 개정 이후에도 TCFD 기후 공시 소프트웨어 시장의 주요 중심지로 자리매김하고 있습니다. 2026년 2월의 지침에 따라, 적용 대상은 직원수 1,000명 이상이며 순매출액이 4억 5,000만 유로(약 4억 8,600만 달러)를 초과하는 기업으로 한정되었으나, 그 반면 적용 대상에 남은 최대 규모의 기업들에 규정 준수 관련 지출이 집중되는 결과가 되었습니다. 이 지역의 기후 변화 정보 공개 소프트웨어 시장은 여전히 투자자의 실사, 은행의 계약 조항 요건, 공공 조달에 따른 압력, 그리고 중소기업(VSME) 관련 공급업체 데이터 요청의 혜택을 받고 있으며, 이러한 요인들이 법적 적용 범위의 축소를 상쇄하며 소프트웨어 투자를 활발하게 유지하고 있습니다. Quentic, Greenomy, Emitwise 등 유럽 벤더들은 ESRS(환경·사회·지배구조 보고 기준)에 부합하는 기능의 심도 및 현지화 측면에서 계속해서 경쟁을 펼치고 있는 반면, GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정) 및 감독 체계는 하이브리드형 및 관리형 도입 모델에 대한 관심을 더욱 높이고 있습니다.

아시아태평양은 TCFD 기후 공시 소프트웨어 시장에서 2031년까지 19.32%라는 지역별 최고 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 해당 지역의 TCFD 기후 공시 소프트웨어 시장은 자발적인 지속가능성 보고에서 의무적이고 기준에 기반한 공개로의 급속한 전환에 힘입어 성장하고 있습니다. 일본의 SSBJ 프레임워크는 이러한 전환의 핵심 요소 중 하나이며, NEC는 2026년 4월, AI를 활용한 공시 자료 작성을 통해 수작업 방식에 비해 작업량을 93% 줄였습니다고 보고했습니다. 싱가포르는 2025년부터 상장 기업에 대해 ISSB 기준을 준수하는 보고를 의무화했습니다. 또한, 중국의 CSDS 시험 기준에 따라 2026년 4월까지 300개 이상의 상장 기업이 첫 보고서를 제출함에 따라, 해당 지역의 공식 구매자 기반이 확대되고 있습니다. 남미, 중동 및 아프리카는 기후 변화 정보 공개 소프트웨어 시장에서 여전히 초기 단계에 있지만, 브라질의 ISSB 준수를 위한 노력, 사우디아라비아의 '비전 2030'에 기반한 ESG 방향성과 UAE의 탄소중립 관련 보고 활동이 향후 조달을 위한 기반을 마련해 나가고 있습니다. 그 결과, 이 지역의 현재 수요는 국가별로 차이가 있지만, 향후 전망은 급속히 밝아지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the TCFD climate disclosure software market size is projected to be USD 1.78 billion in 2025, USD 2.05 billion in 2026, and reach USD 4.21 billion by 2031, growing at a CAGR of 15.48% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Disclosure Data Management, Reporting Disclosure, and More), End User Industry (Industrial Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global TCFD Climate Disclosure Software Market Trends and Insights

Rising Mandatory Climate Disclosure Compliance Across Capital Markets

The TCFD climate disclosure software market is being pushed most directly by the spread of mandatory reporting rules across major capital markets. The CSRD brought the largest EU public-interest entities into ESRS-aligned reporting for fiscal year 2024, and the revised 2026 threshold changes are now concentrating spending among the largest companies that remain in scope. California SB 253 added another domestic demand layer in the United States, requiring companies operating in the state with more than USD 1 billion in annual revenue to publicly disclose Scope 1 and Scope 2 emissions. CARB identified around 2,600 entities on its preliminary list in September 2025. The TCFD climate disclosure software market is also seeing shorter buying windows because many filing deadlines now cluster within a narrow period, which leaves enterprises less time to wait for product maturity before committing to a platform. This has given the TCFD climate disclosure software market a clear preference for vendors that already support CSRD, ESRS, ISSB S1 and S2, GRI, TCFD, and SASB mappings in native form rather than through manual configuration. As a result, broad framework coverage has become a near-term buying factor, not just a product feature.

Audit-Ready Data Trails For Investor and Regulator Scrutiny

The TCFD climate disclosure software market is also being reshaped by the move from narrative sustainability reporting to structured and assured disclosure. SEC climate rules linked Scope 1 and Scope 2 emissions reporting for large accelerated filers to third-party attestation from fiscal year 2025, which makes data lineage and evidence control central to software selection. The Bank of England and the Prudential Regulation Authority moved in the same direction in 2025 by raising supervisory expectations for quantified climate-related financial impacts in banks and insurers, which increases the need for traceable and version-controlled data flows. In the TCFD climate disclosure software market, this changes the buying case because platforms are now evaluated on how well they reduce assurance friction rather than only on how well they collect ESG data. Companies that store evidence in a structured, role-based system can lower the burden on external attestors, which supports lower audit effort after deployment. That has made premium pricing easier to defend in the TCFD climate disclosure software market because software design now affects compliance cost, not just reporting convenience.

Fragmented Climate Data Across Supplier and Portfolio Networks

The TCFD climate disclosure software market still faces a fundamental limitation: the weakest data often sits outside the reporting enterprise. Sphera found in 2025 that 57% of companies reporting on Scope 3 used supplier-specific data only as a partial source and filled many gaps with industry-average factors, which limits precision even when reporting platforms are sophisticated. This means the TCFD climate disclosure software market can automate workflows, calculations, and validation layers, but it cannot, on its own, fully address poor upstream measurement quality. The result is a ceiling on disclosure quality because downstream reports remain dependent on suppliers that still estimate emissions rather than measure them directly. Interoperability efforts from the GHG Protocol and WBCSD are improving the technical basis for exchange, but the underlying availability of primary supplier data remains a longer-term transition. This keeps data credibility as a restraint on the TCFD climate disclosure software market, even as product capabilities continue to improve.

Other drivers and restraints analyzed in the detailed report include:

- Shift From Annual Reporting to Continuous Climate Data Monitoring

- Scoping Pressure From Scope 3 Value Chain Data Requirements

- High Implementation and Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software dominated the TCFD climate disclosure software market with a 71.43% revenue share in 2025, which confirms that platform licensing remains the core commercial model. The largest providers in the TCFD climate disclosure software market continue to rely on SaaS subscription structures that are tied to data volume, entity count, and active reporting frameworks. This model works well because enterprises that connect climate data to finance and risk processes tend to stay on the same system once controls, workflows, and internal approvals are built around it. The strength of the software layer also reflects the need for recurring template updates, data ingestion, permissions management, and disclosure mapping across multiple standards. In practical terms, software remains the center of the value proposition because it creates the operating environment where reporting, validation, and audit preparation come together.

Services is still the faster-moving part of the TCFD climate disclosure software market, with a projected CAGR of 17.67% through 2031. Demand is rising because buyers need implementation support, emissions data integration, workflow design, assurance preparation, and recurring configuration changes as standards evolve. The GHG Protocol Scope 3 revision process adds to that need because companies must revisit how emissions data is classified and supported across quality tiers. This keeps post-deployment work active long after the first go-live date, especially for large reporting groups with multiple entities and disclosure frameworks. The climate disclosure software industry is therefore seeing a closer link between software sales and expert services, and that is pushing vendors toward bundled offerings rather than stand-alone licenses.

Cloud-based deployment led the TCFD climate disclosure software market with a 66.28% share in 2025, reflecting strong buyer preference for scalability and faster content updates. Cloud delivery has become the default path in the TCFD climate disclosure software market because vendors can update disclosure templates and regulatory mappings without waiting for client-side IT cycles. This matters in a rule environment that keeps changing, since buyers need current CSRD, ISSB, and ESRS content in working systems instead of manual workarounds. The cloud model also reduces infrastructure burden for companies that want centralized reporting across multiple business units and jurisdictions. It has therefore stayed ahead as the most practical option for organizations that value speed, standardization, and lower maintenance effort.

Hybrid deployment is projected to expand at a 17.21% CAGR through 2031, which shows that control concerns remain important even as cloud adoption rises. Buyers are using hybrid designs to keep sensitive financial records and some Scope 3 calculations inside controlled environments while still using cloud layers for collaboration and disclosure workflows. Quentic highlighted how German data governance expectations can raise the appeal of this approach for companies that must balance reporting transparency with localization and control needs. On-premises deployment still has a role in the TCFD climate disclosure software market, mainly in government and highly regulated financial settings where data sovereignty carries extra weight. SAP's product path shows the same pattern because it continues to support enterprise integration choices instead of forcing all customers into a single architecture.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Disclosure Data Management

- Reporting and Regulatory Disclosure

- Assurance, Verification, and Audit Readiness

- Disclosure Analytics and Performance Insights

- Climate Risk and Scenario Analysis

- By End User Industry

- Industrial Manufacturing

- Energy and Utilities

- Banking, Financial Services, and Insurance

- Retail and Consumer Goods

- Information Technology and Telecom

- Healthcare and Life Sciences

- Government and Public Sector

- Transportation and Logistics

- Other End User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held 36.14% of the TCFD climate disclosure software market share in 2025, making it the largest regional contributor. The regional TCFD climate disclosure software market is led by the United States, where SEC climate rules brought large accelerated filers into emissions disclosure and attestation requirements from the fiscal year 2025. California SB 253 and SB 261 widened the addressable buyer base beyond SEC registrants, which created a two-layer compliance environment that rewards platforms with flexible template libraries and strong multi-framework mapping. The North American TCFD climate disclosure software market also benefits from investor pressure that remains active even when regulation shifts, which gives adoption a more durable base than a rule-only demand pattern.

Europe remains a major center for the TCFD climate disclosure software market even after the 2026 CSRD scope revision. The February 2026 directive narrowed the mandatory perimeter to companies with more than 1,000 employees and net turnover above EUR 450 million, or approximately USD 486 million, but it also concentrated compliance spending among the largest remaining in-scope entities. The regional climate disclosure software market still benefits from investor due diligence, bank covenant requirements, public procurement pressure, and VSME-related supplier data requests, which keep software investment active beyond the reduced statutory boundary. European vendors such as Quentic, Greenomy, and Emitwise continue to compete on ESRS-native depth and localization, while GDPR and supervisory frameworks support a stronger interest in hybrid and controlled deployment models.

Asia-Pacific is projected to record the fastest regional CAGR at 19.32% through 2031 in the TCFD climate disclosure software market. The regional TCFD climate disclosure software market is being lifted by rapid movement from voluntary sustainability reporting toward mandatory and standards-based disclosure. Japan's SSBJ framework is a major part of that shift, and NEC reported in April 2026 that AI-assisted disclosure preparation cut man-hours by 93% compared with manual processes. Singapore moved listed issuers into ISSB-aligned reporting from 2025, and China's CSDS trial standards brought the first reports by April 2026 for more than 300 listed companies, which expands the region's formal buyer base. South America and Middle East, and Africa remain earlier-stage parts of the climate disclosure software market, but Brazil's ISSB alignment efforts, Saudi Arabia's ESG direction under Vision 2030, and the UAE net-zero related reporting activity are building the foundation for later procurement. The result is a region where present demand is uneven by country, but the forward pipeline is strengthening quickly.

- Workiva Inc.

- Salesforce, Inc.

- International Business Machines Corporation

- SAP SE

- Diligent Corporation

- Persefoni AI, Inc.

- Wolters Kluwer N.V.

- Sphera Solutions, Inc.

- Enablon, a Wolters Kluwer business

- Novisto Inc.

- Watershed Technologies, Inc.

- Microsoft Corporation

- Oracle Corporation

- Intelex Technologies ULC

- Quentic GmbH

- EcoVadis SAS

- Cority Software Inc.

- Benchmark Digital Partners LLC

- Nasdaq, Inc.

- Greenomy SA

- Emitwise Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Mandatory Climate Disclosure Compliance Across Capital Markets

- 4.2.2 Audit-Ready Data Trails For Investor and Regulator Scrutiny

- 4.2.3 Shift From Annual Reporting to Continuous Climate Data Monitoring

- 4.2.4 Scoping Pressure From Scope 3 Value Chain Data Requirements

- 4.2.5 AI-Assisted Scenario Analysis for Transition Risk Planning

- 4.2.6 Integration Demand With ERP, EHS, and GRC Systems

- 4.3 Market Restraints

- 4.3.1 Fragmented Climate Data Across Supplier and Portfolio Networks

- 4.3.2 High Implementation and Integration Complexity

- 4.3.3 Inconsistent Framework Harmonization Across Jurisdictions

- 4.3.4 Model Risk and Liability Concerns in Forward-Looking Disclosures

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Disclosure Data Management

- 5.4.2 Reporting and Regulatory Disclosure

- 5.4.3 Assurance, Verification, and Audit Readiness

- 5.4.4 Disclosure Analytics and Performance Insights

- 5.4.5 Climate Risk and Scenario Analysis

- 5.5 By End User Industry

- 5.5.1 Industrial Manufacturing

- 5.5.2 Energy and Utilities

- 5.5.3 Banking, Financial Services, and Insurance

- 5.5.4 Retail and Consumer Goods

- 5.5.5 Information Technology and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Government and Public Sector

- 5.5.8 Transportation and Logistics

- 5.5.9 Other End User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workiva Inc.

- 6.4.2 Salesforce, Inc.

- 6.4.3 International Business Machines Corporation

- 6.4.4 SAP SE

- 6.4.5 Diligent Corporation

- 6.4.6 Persefoni AI, Inc.

- 6.4.7 Wolters Kluwer N.V.

- 6.4.8 Sphera Solutions, Inc.

- 6.4.9 Enablon, a Wolters Kluwer business

- 6.4.10 Novisto Inc.

- 6.4.11 Watershed Technologies, Inc.

- 6.4.12 Microsoft Corporation

- 6.4.13 Oracle Corporation

- 6.4.14 Intelex Technologies ULC

- 6.4.15 Quentic GmbH

- 6.4.16 EcoVadis SAS

- 6.4.17 Cority Software Inc.

- 6.4.18 Benchmark Digital Partners LLC

- 6.4.19 Nasdaq, Inc.

- 6.4.20 Greenomy SA

- 6.4.21 Emitwise Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Assessment

- 7.2 Scenario-Ready Disclosure Workflows For Private Markets

- 7.3 Assurance-First Vendor Bundling For Regulated Industries

- 7.4 Cross-Border Disclosure Harmonization For Multinational Groups

- 7.5 Investor-Grade Climate Narrative Automation