|

시장보고서

상품코드

2073100

ESG 감사 및 보증 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)ESG Audit and Assurance Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

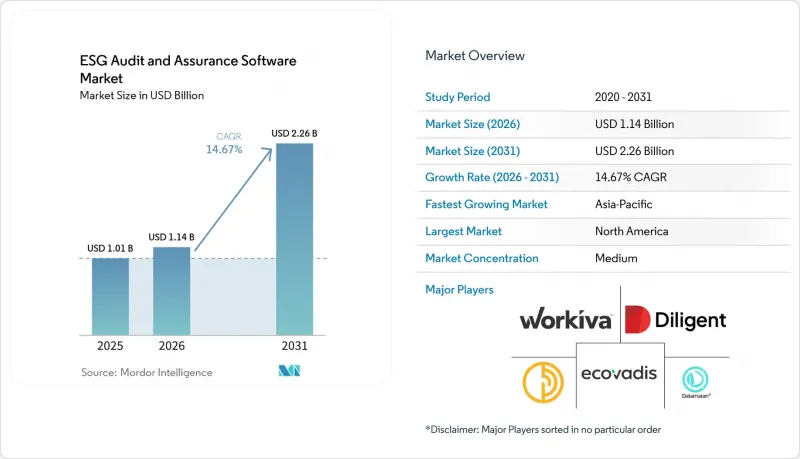

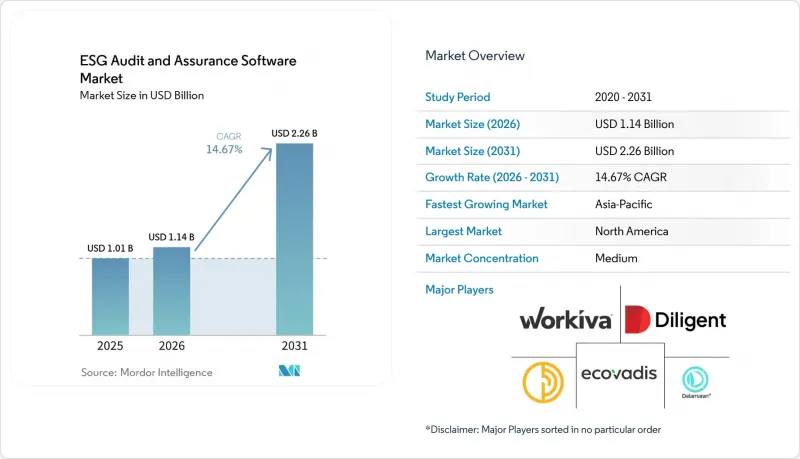

Mordor Intelligence에 의하면, ESG 감사 및 보증 소프트웨어 시장 규모는 2025년에 10억 1,000만 달러, 2026년에 11억 4,000만 달러여, 2031년까지 22억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 14.67%로 성장할 전망입니다.

본 보고서는 제공 형태(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 기업 규모(대기업 및 중소기업), 기능(ESG 데이터 수집·검증 등), 최종 이용 산업(IT 및 통신, 제조, 에너지 및 유틸리티 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 ESG 감사 및 보증 소프트웨어 시장 동향과 인사이트

ESG 공시 의무 제도의 확대

보고 및 보증 일정이 수작업으로 관리하기 어려울 정도로 복잡해짐에 따라, 현재 의무적인 공시 주기가 ESG 감사 및 보증 소프트웨어 시장의 직접적인 구매 요인으로 작용하고 있습니다. EU의 CSRD(기업 지속가능성 보고 지침) 일정, ‘옴니버스 I’을 둘러싼 적용 범위 재검토에 관한 논의, 그리고 ISSA 5000에 기반한 보증으로의 전환에 따라, 기업들은 일회성 보고 프로젝트가 아닌 지속적인 규정 준수 업무를 지원하는 시스템에 계속해서 주목하고 있습니다. 일본에서는 SSBJ 준비가 진행됨에 따라 이러한 수요가 더욱 증가하고 있으며, 각 벤더사는 이미 새로운 공시 구조에 맞춘 제품 출시를 추진하고 있습니다. 유럽에서는 각국이 이를 국내법에 반영하는 방식에 차이가 있더라도 수요가 감소하는 일은 없으며, 오히려 조달을 여러 단계로 분산시켜 미리 설정된 보증 워크플로의 가치를 높이고 있습니다. 그 결과, ESG 감사 및 보증 소프트웨어 시장은 단일 제출 시즌에 국한되지 않고 다양한 구매자층을 아우르며 활기를 띠고 있습니다.

감사 대응이 가능한 ESG 데이터에 대한 투자자 수요

규제가 아직 확정되지 않은 상황임에도 불구하고, 자산 보유자 및 자산 운용사가 ESG 정보의 추적 가능성과 일관성을 요구하게 되면서, 투자자들의 압력이 ESG 감사 및 보증 소프트웨어 시장을 뒷받침하고 있습니다. 조사에 따르면, 응답자들은 여전히 포괄성, 품질, 일관성 측면에서 부족한 점을 지적하고 있으며, 이는 원시 ESG 데이터만으로는 더 이상 기관 투자자의 의사결정에 충분하지 않음을 보여줍니다. 또한, 해당 조사에서는 규제 및 ISSB 기준에 부합하는 공시에 대한 강한 선호도가 드러났으며, 이는 원본 데이터를 문서화하고 보증 검토를 지원할 수 있는 소프트웨어의 가치를 입증해 줍니다. BNP 파리바의 조사에 따르면, 기관 투자자의 48%가 ESG 데이터 수집 및 분석을 위한 예산 배정을 늘릴 것으로 예상하는 반면, PwC의 보고서에 따르면 투자자의 78%가 지속가능성 정보와 참여도 향상을 연관 짓고 있는 것으로 나타났습니다. 이는 감사 대응형 공시 시스템의 상업적 타당성을 입증하는 것입니다. 그 결과, ESG 감사 및 보증 소프트웨어 시장은 규제뿐만 아니라 자본 시장 및 스튜어드십 요건에 의해 주도되는 제2 수요 채널로부터 혜택을 보고 있습니다.

통제, 통합 및 감사 추적과 관련된 높은 비용

도입 비용은 ESG 감사 및 보증 소프트웨어 시장에 있어 여전히 실질적인 제약 요인으로 작용하고 있습니다. 특히, ESG 워크플로우를 ERP, 인사, 조달, 재무 시스템과 연동해야 하는 첫 구매자의 경우 더욱 그렇습니다. 출처 자료에 따르면, 중견 기업의 첫해 비용은 5만 달러에서 20만 달러 사이이며, 연간 유지 비용으로 3만 달러에서 10만 달러가 추가로 발생하기 때문에 시스템 환경이 분산되어 있는 구매자에게는 진입 장벽이 높게 느껴집니다. 주요 과제는 라이선스 가격이 아니라 통합에 있습니다. 데이터 모델의 통합이나 커넥터 구축 작업으로 인해 도입 기간이 당초 프로젝트 계획을 크게 초과하는 경우가 많기 때문입니다. 은행 업계의 지속가능성 업무 프로세스에서도 유사한 문제가 지적되고 있으며, 자동화가 도입되기 전에는 수작업에 의한 문서 처리와 파편화된 증거 추적에 한 주기당 8-10주가 소요되었습니다. 따라서 ESG 감사 및 보증 소프트웨어 시장에서는 단순히 기능 목록이 풍부한 것뿐만 아니라, 미리 구축된 커넥터를 제공하여 보다 신속한 관리 증명(Proof of Control)을 실현할 수 있는 벤더가 유리한 입장에 있습니다.

부문별 분석

2025년, ESG 감사 및 보증 소프트웨어 시장에서 소프트웨어 솔루션이 75.21%의 점유율을 차지했습니다. 이는 대다수의 구매자가 정기적인 업데이트, 체계적인 관리, 그리고 내장된 감사 추적을 제공하는 플랫폼을 선호했음을 보여줍니다. 이는 일회성 도입 프로젝트가 아니라, 여러 프레임워크에 걸친 반복적인 공개 주기를 지원할 수 있는 시스템에 대한 실질적인 요구를 반영한 것입니다. Workiva는 2026년 1분기 매출이 전년 동기 대비 20% 증가한 2억 4,700만 달러를 기록했으며, 구독 및 지원 수익은 21% 증가했다고 보고했습니다. 이는 일회성 제공이 아니라, 지속적인 소프트웨어 이용에 대한 수요가 계속되고 있음을 시사합니다. 해당 보고서에 따르면, 총 유지율은 97%, 순 유지율은 112%로 나타나며, 플랫폼 사용자들은 도입 후 이용을 줄이는 대신 이용 범위를 확대하고 있는 것으로 알 수 있습니다.

서비스 부문은 2031년까지 연평균 성장률(CAGR) 17.12%를 나타낼 것으로 예측되며, 이는 많은 기업이 초기 도입 및 보증 기간 동안 직면하는 운영상의 부담을 반영한 것입니다. 구매 기업은 도입, 교육, 통제 검증, 감사 준비를 동시에 지원받아야 하므로, 자문 지원은 단순한 추가 옵션이 아니라 구매 결정의 일부가 되고 있습니다. Workiva가 2026년 3월에 발표한 GRC 제품 출시 소식에서 기업용 솔루션 제공을 위한 공동 파트너로 Deloitte Touche LLP가 언급되었으며, 이를 통해 소프트웨어 벤더가 제품 도입을 보증 및 통제 지원과 더욱 밀접하게 연계하고 있다는 사실이 부각되었습니다. 이에 따라 ESG 감사 및 보증 소프트웨어 시장에서 제공되는 서비스의 구성은 특히 구매자가 플랫폼의 기능과 보증 대응 능력을 단일 상용 솔루션으로 요구할 경우, 제공 생태계의 강점에 점점 더 의존하게 되고 있습니다.

2025년 ESG 감사 및 보증 소프트웨어 시장에서 클라우드 기반 솔루션의 도입 비중은 58.13%를 차지했으며, 관할 구역별로 규제가 변경될 때 신속하게 업데이트할 수 있는 플랫폼을 구매자들이 선호하는 경향이 뚜렷이 드러났습니다. 이 모델은 CSRD, ISSB 및 SSBJ 관련 활동에서 별도의 로컬 설치를 유지하지 않고도 통합된 워크플로우 관리가 필요한 기업에 적합합니다. 주요 벤더의 로드맵에 따르면, 지속적인 규제 매핑 및 대응 준비 현황의 업데이트는 클라우드 중심 환경에서 관리가 용이하다는 점이 밝혀졌습니다. 또한, 클라우드 도입은 업데이트 주기를 단축하고 로컬 시스템의 유지보수 부담을 줄임으로써 시장 전반의 동향과도 부합합니다.

하이브리드 도입은 2031년까지 연평균 성장률(CAGR) 18.23%로 확대될 것으로 예상되며, ESG 감사 및 보증 소프트웨어 시장에서 가장 빠르게 성장하는 모델이 될 전망입니다. 구매자는 기밀성이 높은 기록을 기존의 On-Premise 시스템 내에 보관하면서, 클라우드 기반의 거버넌스, 공개 및 증거 관리 워크플로를 도입하고자 할 때 이 접근 방식을 채택합니다. 벤더들의 전략은 이러한 혼합 인프라의 현실을 반영하고 있으며, 모든 산업 분야에서 완전한 클라우드 전환이 동일한 속도로 진행되지는 않을 것임을 시사하고 있습니다. 따라서 하이브리드형 성장의 초점은 근대화를 지연시키는 것보다는 기업이 재무 데이터 및 업무 데이터를 위해 이미 신뢰하고 있는 시스템 아키텍처에 ESG 관리 기능을 통합하는 데 맞추어져 있습니다.

지역별 분석

북미는 2025년 ESG 감사 및 보증 소프트웨어 시장 점유율의 36.53%를 차지하며, 해당 지역에서 주도적인 위치를 유지했습니다. 해당 지역은 BFSI(은행 및 금융 및 보험) 분야에서의 광범위한 도입, 감사에 대응 가능한 ESG 데이터에 대한 기관 투자자들의 강력한 압박, 그리고 연방 차원의 규제 제정이 여전히 논란의 대상이 되고 있음에도 불구하고 주 차원의 노력이 지속적으로 중요시된 컴플라이언스 환경의 혜택을 누렸습니다. 모건 스탠리의 2025년 '지속가능 신호' 조사에 따르면, 기관 투자자들은 지속가능성 데이터를 투자 프로세스, 리스크 관리 및 보고 워크플로우에 통합하고 있으며, 이는 데이터의 출처와 일관성을 문서화할 수 있는 시스템에 대한 지속적인 수요를 뒷받침하고 있습니다. 이러한 수요 기반 덕분에 북미의 ESG 감사 및 보증 소프트웨어 시장은 단일 규제 요인에 의존하지 않기 때문에 탄력성을 유지하고 있습니다. 투자자들의 면밀한 검토, 기업의 지배구조 요구 사항, 그리고 보증 대응 데이터 인프라로의 광범위한 전환이 맞물려 이 시장을 뒷받침하고 있습니다.

2025년, 유럽은 큰 점유율을 차지하며 ESG 감사 및 보증 소프트웨어 시장에서 여전히 구조적으로 가장 성숙한 보증 환경을 유지했습니다. CSRD의 제출 주기, 각국의 보증 요건, 그리고 여러 국가에 걸친 보고의 복잡성으로 인해 도입 시기가 그룹마다 달랐음에도 불구하고, 소프트웨어에 대한 수요는 여전히 활발했습니다. KPMG의 프랑스 내 ESG 감사 전문 부서와 유럽 주요 기업들의 체계적인 지속가능성 보증에 대한 광범위한 노력은 소프트웨어 도입이 단순한 공시 자료 작성에 그치지 않고 공식적인 검토 절차와 점점 더 밀접하게 연계되고 있음을 보여줍니다. 따라서 유럽은 제품의 심도, 증거의 질, 그리고 보증 워크플로의 준비 상태가 가장 직접적으로 시험받는 지역으로 남아 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 19.83%를 기록하며 성장할 것으로 전망되며, ESG 감사 및 보증 소프트웨어 시장에서 가장 두드러진 성장세를 보이는 지역입니다. 일본이 큰 기여를 하고 있는 이유는 각 벤더사가 이미 자사 제품을 SSBJ의 공시 요건에 부합하도록 조정했기 때문이며, 월터스 크루어(Wolters Kluwer)사는 2025년 CCH Tagetik이 새로운 기준에 완전히 부합하게 되었다고 발표했습니다. 인도, 한국, 호주에서도 상장 기업들이 체계적인 지속가능성 정보 공개 및 검토에 대한 기대가 높아지고 있어, 시장이 활기를 띠고 있습니다. 남미는 여전히 발전의 초기 단계에 있지만, 다국적 기업의 자회사들과 ISSB(국제 지속가능성 기준 위원회)에 부합하는 보고를 위한 움직임이 플랫폼 도입을 위한 명확한 로드맵을 제시하고 있습니다. 중동 및 아프리카에서도 증권거래소가 주도하는 공시 요건과 각국의 지속가능성 프로그램을 통해 그 기세가 커지고 있으며, 이에 따라 ESG 감사 및 보증 소프트웨어 시장의 지역적 기반이 기존의 중심지를 넘어 확대되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the ESG audit and Assurance Software Market size was USD 1.01 billion in 2025, USD 1.14 billion in 2026, and is forecast to reach USD 2.26 billion by 2031, growing at a CAGR of 14.67% during 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Functionality (ESG Data Collection and Validation, and More), End-Use Industry (IT and Telecom, Manufacturing, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global ESG Audit and Assurance Software Market Trends and Insights

Rising Mandatory ESG Disclosure Regimes

Mandatory disclosure cycles are now serving as direct buying triggers for the ESG Audit and Assurance Software Market, as reporting and assurance timelines have become too complex to manage manually. The EU CSRD timetable, the revised scoping debate around Omnibus I, and the move toward ISSA 5000-based assurance are keeping companies focused on systems that support recurring compliance work rather than one-off reporting projects. Japan is adding to this demand as SSBJ preparation continues, with vendors already positioning products around the new disclosure structure. In Europe, differences in local transposition have not reduced demand; instead, they have spread procurement across multiple waves and increased the value of preconfigured assurance workflows. As a result, the ESG Audit and Assurance Software Market remains active across diverse buyer cohorts rather than being tied to a single filing season.

Investor Demand for Audit-Ready ESG Data

Investor pressure is supporting the ESG Audit and Assurance Software Market, even where regulation remains unsettled, because asset owners and asset managers now expect ESG information to be traceable and consistent. Surveys reported that respondents continued to highlight gaps in coverage, quality, and consistency, indicating that raw ESG data is no longer sufficient for institutional decision-making. The same survey also showed strong preference for regulation- and ISSB-aligned disclosures, which underscores the value of software that can document source data and support assurance reviews. BNP Paribas found that 48% of institutional investors expected higher budget allocations for ESG data acquisition and analysis, while PwC reported that 78% of investors linked sustainability information to better engagement, reinforcing the commercial case for audit-ready disclosure systems. As a result, the ESG Audit and Assurance Software Market is benefiting from a second demand channel driven by capital markets and stewardship requirements, not just regulation.

High Cost of Controls, Integration, and Audit Trails

Implementation costs remain a real constraint on the ESG Audit and Assurance Software Market, especially for first-time buyers who must connect ESG workflows with ERP, HR, procurement, and finance systems. The source document states that first-year costs for a mid-size enterprise range from USD 50,000 to USD 200,000, while recurring annual costs add USD 30,000 to USD 100,000, which keeps the barrier high for buyers with fragmented system estates. The main pressure point is integration rather than license price because data model harmonization and connector work often extends deployment far beyond the original project plan. A similar problem was described in banking sustainability workflows, where manual document handling and disconnected evidence trails consumed 8-10 weeks per cycle before automation was introduced. This keeps the ESG Audit and Assurance Software Market tilted toward vendors that can provide prebuilt connectors and faster proof of control, not just broader feature lists.

Other drivers and restraints analyzed in the detailed report include:

- Shift from Spreadsheet-Based Reporting to Unified Platforms

- Cloud Adoption Among Mid-Market and SME Buyers

- ESG Data Fragmentation Across Enterprise and Supplier Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software solutions held 75.21% of the ESG Audit and Assurance Software Market share in 2025, indicating that most buyers preferred platforms that delivered recurring updates, structured controls, and built-in audit trails. This reflects the practical need for systems that can support repeated disclosure cycles across multiple frameworks rather than one-time implementation projects. Workiva reported Q1 2026 revenue of USD 247 million, up 20% year over year, with subscription and support revenue up 21%, pointing to continued demand for ongoing software access rather than episodic delivery. The same filing showed a 97% gross retention rate and a 112% net retention rate, indicating that platform users are expanding use after initial adoption rather than pulling back.

Services are projected to grow at a 17.12% CAGR through 2031, reflecting the operational burden many companies face during first deployment and assurance cycles. Buyers often need help with implementation, training, controls validation, and audit preparation simultaneously, making advisory support part of the buying decision rather than a separate add-on. Workiva's March 2026 GRC launch highlighted Deloitte and Touche LLP as a co-delivery partner for enterprise rollouts, illustrating how software vendors are tying product deployment more closely to assurance and controls support. This is making the offering mix in the ESG Audit and Assurance Software Market more dependent on the delivery ecosystem's strength, especially when buyers want platform functionality and assurance readiness within a single commercial motion.

Cloud-based deployment accounted for 58.13% of the ESG Audit and Assurance Software Market in 2025, underscoring buyers' preference for platforms that can be updated quickly as rules change across jurisdictions. This model suits companies that need centralized workflow control for CSRD, ISSB, and SSBJ-related activities without maintaining separate local installations. Roadmaps from major vendors show that ongoing regulatory mapping and readiness updates are easier to manage in cloud-oriented environments. Cloud deployment also aligns with the broader market direction by shortening update cycles and reducing the burden of local system maintenance.

Hybrid deployment is projected to expand at an 18.23% CAGR through 2031, making it the fastest-growing model in the ESG Audit and Assurance Software Market. Buyers adopt this approach when they want cloud-based governance, disclosure, and evidence workflows while keeping sensitive records inside existing on-premise systems. Vendor strategies reflect this mixed infrastructure reality, suggesting that full cloud migration will not happen at the same pace across all industries. Hybrid growth is therefore less about delaying modernization and more about fitting ESG controls into the system architecture companies already trust for financial and operational data.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small And Medium Enterprises

- By Functionality

- ESG Data Collection and Validation

- Audit Trail and Evidence Management

- ESG Controls Testing and Verification

- Analytics and Benchmarking

- Reporting and Disclosure Assurance

- Compliance and Regulatory Audit Management

- By End-Use Industry

- IT and Telecom

- BFSI

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Construction and Infrastructure

- Government and Public Sector

- Healthcare and Life Sciences

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held 36.53% of the ESG Audit and Assurance Software Market share in 2025, maintaining its leading regional position. The region benefited from deep BFSI adoption, strong institutional investor pressure for audit-ready ESG data, and a compliance environment in which state-level action continued to matter even as federal rulemaking remained contested. Morgan Stanley's 2025 Sustainable Signals survey showed that institutional investors were embedding sustainability data into investment processes, risk management, and reporting workflows, which supports continuing demand for systems that can document provenance and consistency. That demand base gives the ESG Audit and Assurance Software Market in North America resilience because it does not depend on a single regulatory trigger. A combination of investor scrutiny, enterprise governance needs, and the broader move toward assurance-ready data infrastructure is supporting it.

Europe contributed a significant share in 2025 and remained the most structurally developed assurance environment for the ESG Audit and Assurance Software Market. CSRD filing cycles, local assurance requirements, and multi-country reporting complexity continued to keep software demand active even as implementation timing shifted between cohorts. France's dedicated ESG audit practice at KPMG and the broader push toward structured sustainability assurance in large European companies show how software adoption is increasingly tied to formal review processes, not only disclosure preparation. Europe, therefore, remains the region where product depth, evidence quality, and assurance workflow readiness are tested most directly.

Asia-Pacific is projected to grow at a 19.83% CAGR through 2031, which makes it the fastest-growing geography in the ESG Audit and Assurance Software Market. Japan is a major contributor because vendors are already aligning products to SSBJ disclosure requirements, and Wolters Kluwer stated in 2025 that CCH Tagetik had achieved full compliance with the new standards. India, South Korea, and Australia are also adding momentum as listed entities face wider expectations for structured sustainability disclosure and review. South America is still in earlier stages of development, but multinational subsidiaries and the direction toward ISSB-linked reporting are creating a clearer entry path for platform adoption. The Middle East and Africa are also gaining traction through exchange-led disclosure requirements and national sustainability programs, which broaden the regional base of the ESG Audit and Assurance Software Market beyond its traditional centers.

- Workiva Inc.

- Diligent Corporation

- Datamaran Limited

- Persefoni AI, Inc.

- Greenstone+ Ltd.

- Benchmark Digital Partners LLC

- Enablon SA

- Sphera Solutions, Inc.

- Intelex Technologies ULC

- Cority Software Inc.

- Novisto Inc.

- EcoVadis SAS

- Watershed Technology, Inc.

- Plan A Solutions GmbH

- Novata Inc.

- FigBytes Inc.

- Coolset B.V.

- AuditBoard, Inc.

- NAVEX Global, Inc.

- Wolters Kluwer CCH Tagetik

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Mandatory ESG Disclosure Regimes

- 4.2.2 Investor Demand for Audit-Ready ESG Data

- 4.2.3 Shift From Spreadsheet-Based Reporting To Unified Platforms

- 4.2.4 Cloud Adoption Among Mid-Market And SME Buyers

- 4.2.5 AI-Assisted Data Validation And Exception Detection

- 4.2.6 Supply-Chain Traceability Requirements For Scope 3 Assurance

- 4.3 Market Restraints

- 4.3.1 High Cost of Controls, Integration, And Audit Trails

- 4.3.2 ESG Data Fragmentation Across Enterprise And Supplier Systems

- 4.3.3 Shortage of ESG Reporting, Controls, And Assurance Talent

- 4.3.4 Standards Volatility Requiring Frequent Reconfiguration

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Comptetive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small And Medium Enterprises

- 5.4 By Functionality

- 5.4.1 ESG Data Collection and Validation

- 5.4.2 Audit Trail and Evidence Management

- 5.4.3 ESG Controls Testing and Verification

- 5.4.4 Analytics and Benchmarking

- 5.4.5 Reporting and Disclosure Assurance

- 5.4.6 Compliance and Regulatory Audit Management

- 5.5 By End-Use Industry

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Construction and Infrastructure

- 5.5.7 Government and Public Sector

- 5.5.8 Healthcare and Life Sciences

- 5.5.9 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Netherlands

- 5.6.3.7 Russia

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workiva Inc.

- 6.4.2 Diligent Corporation

- 6.4.3 Datamaran Limited

- 6.4.4 Persefoni AI, Inc.

- 6.4.5 Greenstone+ Ltd.

- 6.4.6 Benchmark Digital Partners LLC

- 6.4.7 Enablon SA

- 6.4.8 Sphera Solutions, Inc.

- 6.4.9 Intelex Technologies ULC

- 6.4.10 Cority Software Inc.

- 6.4.11 Novisto Inc.

- 6.4.12 EcoVadis SAS

- 6.4.13 Watershed Technology, Inc.

- 6.4.14 Plan A Solutions GmbH

- 6.4.15 Novata Inc.

- 6.4.16 FigBytes Inc.

- 6.4.17 Coolset B.V.

- 6.4.18 AuditBoard, Inc.

- 6.4.19 NAVEX Global, Inc.

- 6.4.20 Wolters Kluwer CCH Tagetik

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment