|

시장보고서

상품코드

2073119

화이트박스 스위치 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)White Box Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

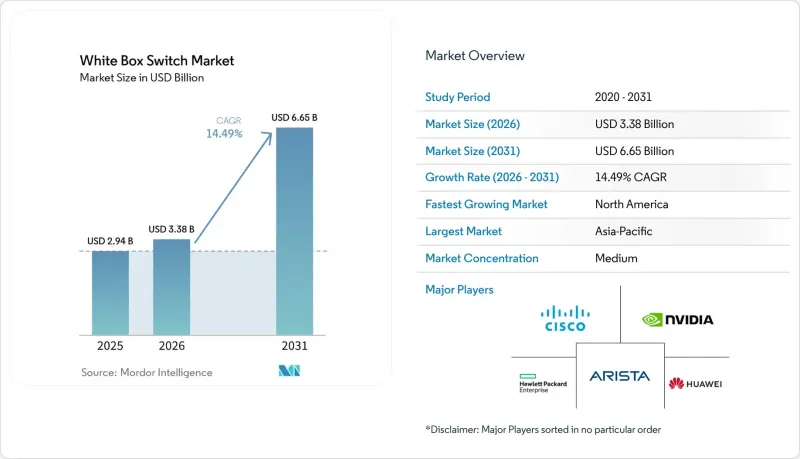

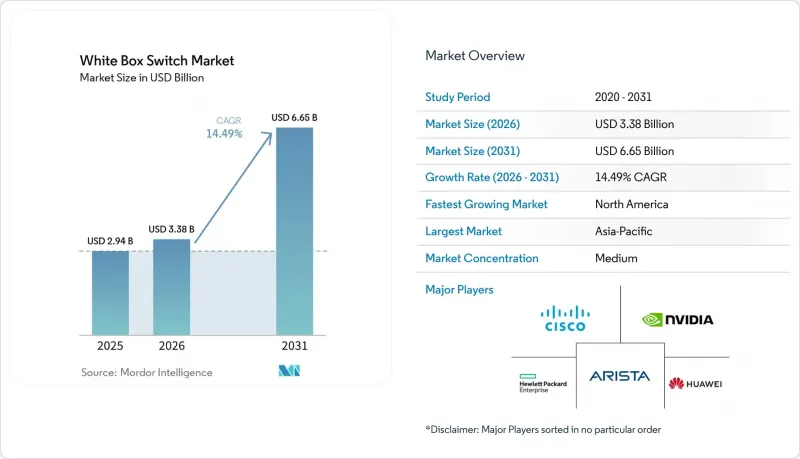

Mordor Intelligence에 의하면, 화이트박스 스위치 시장 규모는 2025년에 29억 4,000만 달러로 평가되었고 2026년 33억 8,000만 달러에서 2031년까지 66억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 14.49%를 나타낼 전망입니다.

본 보고서는 포트 속도(10/25GbE, 40 GbE, 100 GbE, 200/400 GbE, 800 GbE), 스위치 계층(액세스, 디스트리뷰션, 코어), 최종 사용자 산업(클라우드 서비스 제공업체, 통신 사업자 등), 도입 환경(하이퍼스케일 등), 네트워크 운영 체제(SONiC 등), 구성 요소(하드웨어, NOS, 서비스), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 화이트박스 스위치 시장 동향 및 인사이트

하이퍼스케일 데이터센터의 확대

Meta, Google, Microsoft, Amazon 등의 하이퍼스케일러들은 ODM이 제조하는 자사 사양의 스위치 섀시를 대규모로 지속적으로 도입하고 있으며, 이로 인해 OEM 브랜드의 프리미엄이 제거되고, 실리콘 로드맵에 맞춘 18-24개월이라는 보다 신속한 설계 업데이트 주기가 가능해졌습니다. 2026년을 목표로 한 설비 투자 계획에서는 AI 클러스터 구축에 수백억 달러가 배정되어 있으며, 각 클러스터에서는 고대역폭·저지연 패브릭을 지원하기 위해 수천 개의 800 GbE 스파인 포트가 필요한 것으로 파악되고 있습니다. 광 모듈을 통합하고 액체 냉각을 지원하는 ODM은 첨단 ASIC 공급을 우선적으로 확보할 수 있으므로, 상품화까지의 기간을 단축하고 이익률을 높일 수 있습니다. 이와 동시에, 2030년까지 아시아태평양의 생산 능력이 북미를 추월할 것으로 전망됨에 따라, 각 업체들은 베트남과 인도에 있는 제조 거점을 확대되고 있습니다. 이러한 다양화를 통해 지정학적 및 무역상의 불확실성 속에서도 공급망의 집중 위험이 완화되고 납기 일정이 안정화됩니다.

400G 및 800G 이더넷 포트 속도로의 전환

2024년 IEEE 802.3df의 승인으로 800 GbE 도입과 관련된 규격상의 불확실성이 해소됨에 따라, ASIC 공급업체들의 로드맵이 가속화되어 12개월의 샘플링 기간 내에 102.4 Tbps급 디바이스가 실현될 전망입니다. 각 하이퍼스케일러 기업들은 스파인 계층의 업그레이드를 우선시하고, 기존에 100 GbE로 운영되던 리프 계층에 400 GbE 칩을 단계적으로 도입함으로써 패브릭 전체의 비트당 비용을 최적화하고 있습니다. 2026년까지 30kW에 육박하는 랙 밀도를 지원하는 수냉식 섀시가 상용화될 전망이며, 한편 리니어 플러그형 광학 장치를 통해 모듈의 전력 소비가 약 50% 감소하여 전반적인 에너지 효율이 향상될 것입니다. 동시에 OSFP 포트의 리드타임이 약 16주로 단축되어, 네트워크 패브릭 구축과 GPU 클러스터 도입 간의 연계가 더욱 긴밀해졌습니다. 기존 OEM 업체들은 SONiC 지원 시스템을 점점 더 많이 제공하고 있으며, 이는 성능 측면에서의 차별화가 개방적이고 분산된 하드웨어 모델로 수렴되고 있음을 보여줍니다.

네트워크 팀의 통합 및 운영상의 복잡성

화이트박스 도입으로 인해 네트워크 운영은 CLI 기반의 워크플로우에서 리눅스, 컨테이너화, 그리고 Docker 및 CI/CD 파이프라인과 같은 자동화 스택으로 전환되고 있으며, 이는 결코 간과할 수 없는 기술 격차를 초래하고 있습니다. 조기 도입 기업들은 컨테이너화된 라우팅 기능의 디버깅과 스위치 추상화 인터페이스(SAI) 계층의 유지보수 과정에서 학습 곡선이 가파르다는 점을 지적하고 있으며, 이는 초기 도입 시 운영 위험을 높이고 있습니다. 상용 SONiC 배포판은 지원 및 도구를 제공하지만, DevOps 성숙도가 낮은 조직에서 발생하는 문화적 저항을 완전히 해소해 주지는 않습니다. 중소규모 기업들은 운영상의 복잡성이 낮은 통합형 네트워크 솔루션을 선호하기 때문에 하이퍼스케일 환경 이외의 곳에서의 도입은 여전히 제한적입니다. 훈련 프로그램이나 관리형 서비스를 통해 이러한 과제는 부분적으로 완화되지만, 기능 출시 주기가 빠르기 때문에 팀은 지속적인 업데이트 관리를 해야만 하며, 많은 사람들이 이를 순수한 효율성 향상이라기보다는 운영상의 추가 부담으로 여기고 있습니다.

부문별 분석

2025년, 100 GbE 부문은 매출 점유율 46.23%를 유지했습니다. 이는 엔터프라이즈 및 레거시 데이터센터 패브릭에서의 도입 실적을 반영한 것이지만, 그 추세는 빠르게 고대역폭 아키텍처로 전환되고 있습니다. 800 GbE용 화이트박스 스위치 시장은 고밀도 64포트 OSFP 스파인 구성을 가능하게 하는 102.4 Tbps ASIC의 상용화에 힘입어, 2026년부터 2031년까지 연평균 성장률(CAGR) 26.24%로 성장할 것으로 전망됩니다. 이러한 플랫폼들은 AI 클러스터의 처리량 및 지연 시간 요구 사항을 충족하면서도 비트당 비용 경쟁력을 유지하고 있습니다. 하이퍼스케일러들이 확장 가능하고 비차단형 패브릭을 우선시함에 따라, 800 GbE는 초기 도입 단계에서 본격적인 보급 단계로 전환되며, 중간 업그레이드 경로를 대체하고 있습니다.

이러한 가속화로 인해 기존의 업그레이드 주기가 단축되면서, 통신 사업자들은 AI 워크로드의 확장에 대응하기 위해 400 GbE 리프 계층으로의 업그레이드를 건너뛰고 800 GbE 스파인 계층으로 직접 전환하는 사례가 늘고 있습니다. 그 결과 발생하는 수요 급증은 시판용 실리콘의 판매량을 끌어올려 생태계의 경제성을 향상시킵니다. 전력 효율이 뛰어난 리니어 플러그형 광학 장치는 모듈의 에너지 소비를 줄여 운영 비용을 직접 절감합니다. 한편, 수냉식 섀시는 30 kW를 초과하는 랙의 열적 제약을 해소하여 더 높은 포트 밀도를 실현합니다. 각 벤더사는 이미 이러한 아키텍처에 대한 레퍼런스 설계를 사전에 검증하고 있으며, 이를 통해 도입 기간을 단축하는 동시에 화이트박스 환경에서의 차세대 고속 스위칭으로의 신속한 전환을 가속화하고 있습니다.

2025년에는 액세스 플랫폼이 매출의 39.62%를 차지하며, 엔터프라이즈 캠퍼스 및 엣지 환경에서의 광범위한 도입을 반영하고 있지만, 성장세는 부가가치가 더 높은 코어 부문으로 이동하고 있습니다. 각 하이퍼스케일러 기업들이 800 GbE 및 새롭게 등장한 1.6 Tbps 포트를 중심으로 스파인 아키텍처를 재설계함에 따라, 코어 스위치 시장은 연평균 성장률(CAGR) 15.83%로 확대될 것으로 전망됩니다. 이러한 업그레이드를 통해 여러 개의 레거시 섀시를 더 적은 수의 고밀도 시스템으로 통합함으로써 코어 계층의 점유율이 확대되고, 공간 효율과 전력 효율이 향상됩니다. 그 결과, 성능 향상이 워크로드의 확장성이나 지연 시간에 민감한 용도에 직접적인 영향을 미치는 네트워크 계층의 상위 단계로 자본 배분이 이동하고 있습니다.

동시에, PVST+ 및 802.1X 지원을 포함한 SONiC의 엔터프라이즈용 기능 세트가 확충됨에 따라 액세스 계층의 이용 사례에 대한 점진적인 확산이 진행되고 있으며, 각 ODM 업체들은 캠퍼스 구축을 위해 비용 효율성이 뛰어난 Marvell 기반 1 GbE PoE 스위치를 출시할 수 있게 되었습니다. 그러나 예산의 우선순위는 여전히 AI 기반 인프라에 쏠려 있으며, 이 분야에서 비차단형 스파인 패브릭이 최고의 성능과 경제적 효과를 제공합니다. 그 결과, 액세스 계층에서의 도입이 대상 시장을 확대하는 한편, 증분 수익의 대부분은 코어 스위칭에 집중되어 있어, 화이트박스 스위치 시장에서 그 전략적 중요성이 더욱 높아지고 있습니다.

지역별 분석

2025년 수요 중 북미가 39.47%를 차지했습니다. 이는 버지니아주, 오리건주, 아이오와주에 위치한 하이퍼스케일 데이터센터 클러스터가 주도하고 있으며, 이들 클러스터는 화이트박스 스위치의 대규모 도입을 지속적으로 추진하고 있습니다. 2026년 설비 투자 계획은 600억 달러를 초과하며, 그 대부분은 고밀도 컴퓨팅 부하를 유지하기 위해 800 GbE 스파인 계층과 수냉식 랙 환경이 필요한 AI 인프라에 할당될 예정입니다. 이와 동시에 기업 내 도입도 점차 확대되고 있으며, 금융 서비스 및 미디어 등 업계에서는 소프트웨어 라이선스 비용을 절감하고 운영의 유연성을 높이기 위해 SONiC 기반 패브릭의 시범 도입이 진행되고 있습니다. 하이퍼스케일 시장의 우위와 기업 내 도입 확대가 맞물리면서, 화이트박스 스위치 시장에서 북미의 입지가 주요 수익원으로서 더욱 공고해지고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 디지털 인프라에 대한 정부의 강력한 지원책과 주요 경제권에서의 5G 구축 가속화에 힘입어 연평균 성장률(CAGR) 15.21%로 확대될 것으로 전망됩니다. 데이터 현지화 정책과 클라우드 도입 확대가 지역 내 데이터센터용량에 대한 수요를 견인하고 있으며, 관리형 코로케이션 용량은 2030년까지 23,900 MW를 넘어 미국을 추월할 것으로 전망됩니다. 공급 측면에서는 대만을 거점으로 하는 ODM 기업들이 비용 면에서의 우위, 세제 혜택, 그리고 지정학적 분산화를 활용하기 위해 베트남과 말레이시아로 제조 거점을 확대되고 있습니다. 이러한 현지 생산 체제를 통해 리드타임이 단축되고 공급망의 회복력이 강화됨에 따라, 하이퍼스케일 시장과 신흥 엔터프라이즈 시장 모두에서 화이트박스 스위칭 솔루션의 도입이 가속화될 것입니다.

유럽의 성장은 규제, 지속가능성에 대한 우선순위, 그리고 통신 사업자가 주도하는 네트워크 혁신 이니셔티브에 의해 형성되고 있습니다. 통신 사업자들은 에너지 효율이 뛰어난 400 GbE 스위칭 플랫폼과 리니어 플러그형 광학 장치의 조합을 우선적으로 채택하고 있으며, 이를 통해 전력 소비를 최대 30%까지 절감함으로써 지역의 탄소 배출 감축 목표를 달성할 수 있게 됩니다. 통신 사업자들이 벤더의 다양화와 비용 관리를 추구하는 가운데, Open RAN 프로그램은 분산형 네트워크의 도입을 더욱 가속화하고 있습니다. 영국이나 독일 등 여러 국가에서는 정부의 주도적인 자금 지원을 통해 오픈 인프라 모델로의 전환이 촉진되고 있습니다. 한편, 남미, 중동 및 아프리카 등의 신흥 지역에서는 도입이 초기 단계에 있거나 시범 도입이 증가하고 있어, 화이트박스 스위치 시장이 기존 지역을 넘어 서서히 확대되고 있는 것으로 나타났습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the white box switch market size was valued at USD 2.94 billion in 2025 and estimated to grow from USD 3.38 billion in 2026 to reach USD 6.65 billion by 2031, at a CAGR of 14.49% during the forecast period (2026-2031).

This report is Segmented by Port Speed (10/25 GbE, 40 GbE, 100 GbE, 200/400 GbE, 800 GbE), Switch Layer (Access, Distribution, Core), End User Industry (Cloud Service Providers, Telecom Operators, and More), Deployment Environment (Hyperscale, and More), Network Operating System (SONiC, and More), Component (Hardware, NOS, Services), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global White Box Switch Market Trends and Insights

Hyperscale Data Center Expansion

Hyperscalers such as Meta, Google, Microsoft, and Amazon continue to deploy self-specified switch chassis manufactured by ODMs at scale, removing OEM brand premiums and enabling faster 18-24 month design refresh cycles aligned with silicon roadmaps. Capital expenditure programs entering 2026 allocate tens of billions of dollars (USD tens of billions) toward AI cluster buildouts, each demanding thousands of 800 GbE spine ports to support high-bandwidth, low-latency fabrics. ODMs that integrate optics and support liquid cooling secure priority access to advanced ASIC supply, shortening commercialization timelines and improving margin capture. At the same time, Asia-Pacific capacity is projected to surpass North America by 2030, prompting vendors to expand manufacturing footprints in Vietnam and India. This diversification reduces supply chain concentration risk and stabilizes delivery timelines amid geopolitical and trade uncertainties.

Transition to 400G and 800G Ethernet Port Speeds

The ratification of IEEE 802.3df in 2024 removed standards uncertainty for 800 GbE deployments, accelerating ASIC vendor roadmaps toward 102.4 Tbps-class devices within a 12-month sampling window. Hyperscalers prioritize spine-layer upgrades, cascading 400 GbE silicon into leaf tiers that previously operated at 100 GbE, thereby optimizing cost per bit across fabrics. Liquid-cooled chassis are expected to be commercialized by 2026 to support rack densities approaching 30 kW, while linear pluggable optics reduce module power consumption by approximately 50%, improving overall energy efficiency. Concurrently, OSFP port lead times have compressed to around 16 weeks, enabling tighter synchronization between network fabric rollouts and GPU cluster deployments. Incumbent OEMs are increasingly offering SONiC-compatible systems, indicating that performance differentiation is converging toward open, disaggregated hardware models.

Integration and Operational Complexity for Network Teams

White box deployments shift network operations from CLI-based workflows to Linux, containerization, and automation stacks such as Docker and CI/CD pipelines, creating a non-trivial skills gap. Early adopters highlight steep learning curves when debugging containerized routing functions or maintaining Switch Abstraction Interface layers, increasing operational risk during initial rollouts. Commercial SONiC distributions provide support and tooling, but they do not fully offset cultural resistance in organizations lacking DevOps maturity. Adoption outside hyperscale environments remains constrained, as smaller enterprises prefer integrated networking solutions with lower operational complexity. Although training programs and managed services partially mitigate these challenges, the rapid release cadence of features forces teams to manage continuous updates, which many view as incremental operational overhead rather than net efficiency gains.

Other drivers and restraints analyzed in the detailed report include:

- Cost Optimization via Hardware-Software Disaggregation

- AI and Machine Learning Workloads Demand Low-Latency Fabrics

- Limited Vendor Support and Warranty Ecosystem

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 100 GbE tier retained a 46.23% revenue share in 2025, reflecting its installed base across enterprise and legacy data center fabrics, but momentum is shifting rapidly toward higher bandwidth architectures. The white box switch market for 800 GbE is projected to grow at a 26.24% CAGR between 2026 and 2031, supported by the commercialization of 102.4 Tbps ASICs that enable dense 64-port OSFP spine configurations. These platforms meet the throughput and latency requirements of AI clusters while maintaining competitive cost per bit. As hyperscalers prioritize scalable, non-blocking fabrics, 800 GbE transitions from early deployment to volume adoption, displacing intermediate upgrade paths.

This acceleration compresses traditional upgrade cycles, with operators increasingly bypassing 400 GbE leaf upgrades and moving directly to 800 GbE spine layers to align with AI workload scaling. The resulting surge in demand strengthens merchant silicon volumes and improves ecosystem economics. Power-efficient linear pluggable optics reduce module energy consumption, directly lowering operating expenditure, while liquid-cooled chassis remove thermal constraints in racks exceeding 30 kW, enabling higher port density. Vendors are already pre-validating reference designs for these architectures, shortening deployment timelines and accelerating a rapid shift toward next-generation high-speed switching in white-box environments.

Access platforms accounted for 39.62% of revenue in 2025, reflecting their broad deployment across enterprise campus and edge environments, but growth is shifting toward higher-value core layers. Core switches are projected to expand at a 15.83% CAGR as hyperscalers redesign spine architectures around 800 GbE and emerging 1.6 Tbps ports. These upgrades increase core-layer share by consolidating multiple legacy chassis into fewer, higher-density systems, improving space and power efficiency. As a result, capital allocation is moving upward in the network hierarchy, where performance gains directly influence workload scalability and latency-sensitive applications.

At the same time, SONiC's expanding enterprise feature set, including PVST+ and 802.1X support, is enabling gradual penetration into access-layer use cases, allowing ODMs to introduce cost-effective Marvell-based 1 GbE PoE switches for campus deployments. However, budget prioritization remains skewed toward AI-driven infrastructure, where non-blocking spine fabrics deliver the highest performance and economic impact. Consequently, while access-layer adoption broadens the addressable market, the majority of incremental revenue growth is concentrated in core switching, reinforcing its strategic importance in the white-box switch market.

Complete Report Scope:

- By Port Speed

- 10/25 GbE

- 40 GbE

- 100 GbE

- 200/400 GbE

- 800 GbE

- By Switch Layer

- Access Switches

- Distribution Switches

- Core Switches

- By End User Industry

- Cloud Service Providers

- Telecom Operators

- Enterprises

- Government & Public Sector

- By Deployment Environment

- Hyperscale Data Centers

- Enterprise Data Centers

- Edge Data Centers

- By Network Operating System (NOS)

- SONiC

- Cumulus Linux

- Pica8 PicOS

- Other NOS

- By Component

- Hardware

- Network Operating System (NOS)

- Services

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- North Africa

- Rest of Africa

- North America

Geography Analysis

North America accounted for 39.47% of demand in 2025, anchored by hyperscale data center clusters in Virginia, Oregon, and Iowa, which continue to drive high-volume deployments of white-box switches. Capital expenditure plans exceed USD 60 billion in 2026, largely directed toward AI infrastructure that requires 800 GbE spine layers and liquid-cooled rack environments to sustain high-density compute loads. In parallel, enterprise adoption is gradually expanding, with sectors such as financial services and media piloting SONiC-based fabrics to reduce software licensing costs and improve operational flexibility. This combination of hyperscale dominance and incremental enterprise uptake reinforces North America's position as the primary revenue contributor in the white box switch market.

Asia-Pacific is the fastest-growing region, projected to expand at a 15.21% CAGR, supported by strong government incentives for digital infrastructure and accelerating 5G deployment across major economies. Data localization policies and rising cloud adoption are driving demand for regional data center capacity, with managed colocation expected to exceed 23,900 MW by 2030, surpassing the United States. At the supply level, Taiwan-based ODMs are expanding manufacturing into Vietnam and Malaysia to leverage cost advantages, tax incentives, and geopolitical diversification. This localized production capability reduces lead times and strengthens supply chain resilience, enabling faster adoption of white box switching solutions across both hyperscale and emerging enterprise markets.

Europe's growth is shaped by regulatory and sustainability priorities, as well as telecom-driven network transformation initiatives. Operators are prioritizing energy-efficient 400 GbE switching platforms combined with linear pluggable optics, which can reduce power consumption by up to 30% and align with regional carbon-reduction targets. Open RAN programs are further accelerating the adoption of disaggregated networking as carriers seek vendor diversification and cost control. Government-backed funding in countries such as the United Kingdom and Germany is supporting the transition toward open infrastructure models. Meanwhile, emerging regions, including South America, the Middle East, and Africa, are at early stages of adoption but are seeing increasing pilot deployments, indicating gradual expansion of the white box switch market beyond established geographies.

- Accton Technology Corporation

- Quanta Cloud Technology Inc.

- Hon Hai Precision Industry Co., Ltd.

- Celestica Inc.

- Delta Electronics, Inc.

- Alpha Networks Inc.

- Edgecore Networks Corporation

- Asterfusion Data Technologies Co., Ltd.

- Lanner Electronics Inc.

- Wistron Corporation

- Inventec Corporation

- Super Micro Computer, Inc.

- MITAC Holdings Corporation

- Netberg Ltd.

- Interface Masters Technologies, Inc.

- UfiSpace Co., Ltd.

- Radisys Corporation

- Advantech Co., Ltd.

- Silicom Ltd.

- Flex Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale Data Center Expansion

- 4.2.2 Transition to 400G and 800G Ethernet Port Speeds

- 4.2.3 Cost Optimization via Hardware-Software Disaggregation

- 4.2.4 AI and Machine Learning Workloads Demand Low-Latency Fabrics

- 4.2.5 Sustainability Targets Driving Energy-Efficient Switching

- 4.2.6 Open Source NOS Ecosystem Maturation

- 4.3 Market Restraints

- 4.3.1 Integration and Operational Complexity for Network Teams

- 4.3.2 Limited Vendor Support and Warranty Ecosystem

- 4.3.3 Supply Chain Volatility of Merchant Silicon

- 4.3.4 Security Concerns in Open Networking Environments

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Port Speed

- 5.1.1 10/25 GbE

- 5.1.2 40 GbE

- 5.1.3 100 GbE

- 5.1.4 200/400 GbE

- 5.1.5 800 GbE

- 5.2 By Switch Layer

- 5.2.1 Access Switches

- 5.2.2 Distribution Switches

- 5.2.3 Core Switches

- 5.3 By End User Industry

- 5.3.1 Cloud Service Providers

- 5.3.2 Telecom Operators

- 5.3.3 Enterprises

- 5.3.4 Government & Public Sector

- 5.4 By Deployment Environment

- 5.4.1 Hyperscale Data Centers

- 5.4.2 Enterprise Data Centers

- 5.4.3 Edge Data Centers

- 5.5 By Network Operating System (NOS)

- 5.5.1 SONiC

- 5.5.2 Cumulus Linux

- 5.5.3 Pica8 PicOS

- 5.5.4 Other NOS

- 5.6 By Component

- 5.6.1 Hardware

- 5.6.2 Network Operating System (NOS)

- 5.6.3 Services

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Australia

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 North Africa

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accton Technology Corporation

- 6.4.2 Quanta Cloud Technology Inc.

- 6.4.3 Hon Hai Precision Industry Co., Ltd.

- 6.4.4 Celestica Inc.

- 6.4.5 Delta Electronics, Inc.

- 6.4.6 Alpha Networks Inc.

- 6.4.7 Edgecore Networks Corporation

- 6.4.8 Asterfusion Data Technologies Co., Ltd.

- 6.4.9 Lanner Electronics Inc.

- 6.4.10 Wistron Corporation

- 6.4.11 Inventec Corporation

- 6.4.12 Super Micro Computer, Inc.

- 6.4.13 MiTAC Holdings Corporation

- 6.4.14 Netberg Ltd.

- 6.4.15 Interface Masters Technologies, Inc.

- 6.4.16 UfiSpace Co., Ltd.

- 6.4.17 Radisys Corporation

- 6.4.18 Advantech Co., Ltd.

- 6.4.19 Silicom Ltd.

- 6.4.20 Flex Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment