|

시장보고서

상품코드

2073122

심혈관 수복 및 재건 기기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cardiovascular Repair and Reconstruction Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

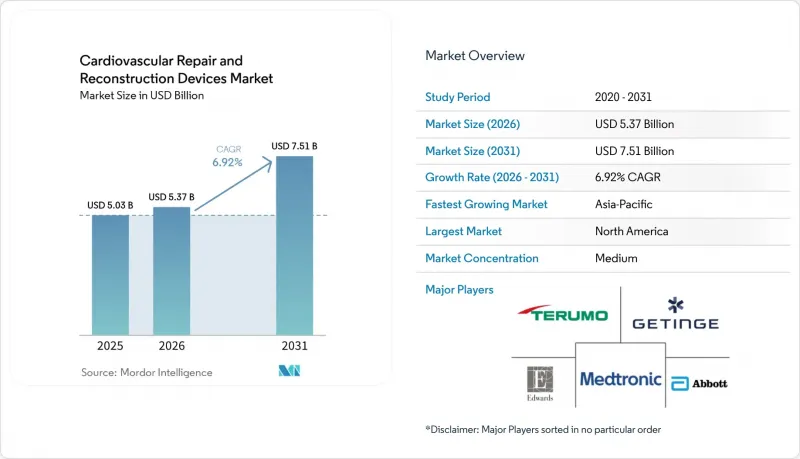

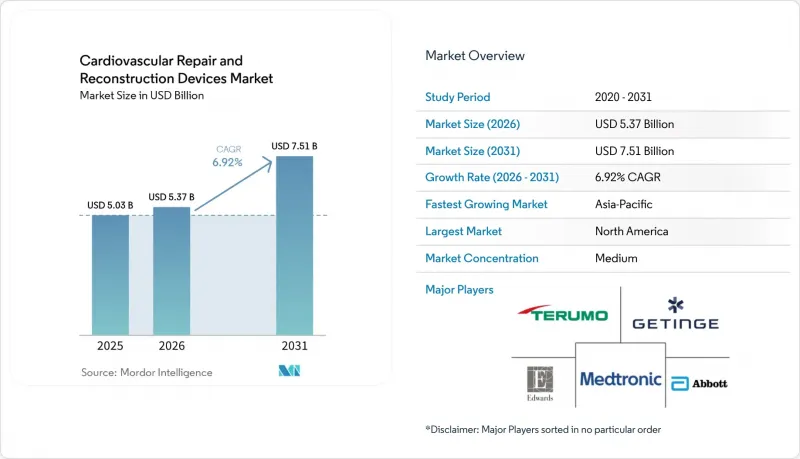

Mordor Intelligence에 의하면, 심혈관 수복 및 재건 기기 시장 규모는 2025년에 50억 3,000만 달러, 2026년에 53억 7,000만 달러되어, 2031년까지 75억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 6.92%로 성장할 전망입니다.

본 보고서는 제품별(심장 판막 수복, 혈관 이식편, 패치, 판막륜 성형술, LAAC), 소재별(생체 유래, 합성, 금속, 생체 흡수성 하이브리드), 용도별(관상동맥 질환, 심장 판막증, 말초 혈관 질환, 구조적 심장 질환), 최종 사용자(병원, 카테터실, 외래수술센터(ASC), 전문 심장 시설), 지역(북미, 유럽, 기타)별로 분류되어 있습니다. 예측 : 시장 규모(달러).

세계 심혈관 수복 및 재건 기기 시장 동향과 인사이트

구조적 심장 질환 및 혈관 질환의 부담 증가

심혈관 수복 및 재건 기기 시장은 여전히 규모가 크며, 환자 수의 절대적 증가세라는 이점을 누리고 있습니다. 2021년 기준으로 비류마티스성 심장판막증 환자 수는 전 세계적으로 2,840만 명에 달하며, 2035년까지 전 세계 유병률은 10만 명당 20.28명에 이를 것으로 예측됩니다. TAVI(경카테터 대동맥판막 치환술) 시행 건수는 2021년까지 연간 15만 건에 달했으나, 치료 가능한 판막 질환 환자 수는 여전히 훨씬 더 많으며, 많은 신흥국에서는 질환 자체의 존재가 아니라 치료 접근성 제한이 여전히 시행 건수 확대를 저해하고 있는 것으로 나타났습니다. 동남아시아와 라틴아메리카 전역에서 PCI 및 EP 절제술 시행 역량이 확대됨에 따라, 구조적 심장 질환 치료 프로그램 역시 다른 중재적 의료 서비스에서 이미 확인된 것과 유사한 병원 도입 과정을 밟을 가능성이 높다고 생각됩니다. 증례 수 증가와 연령 조정 사망률의 하락 사이에 나타나는 격차는 기기를 이용한 중재술이 신규 환자 관리에서 점점 더 큰 비중을 차지하고 있음을 보여주며, 이는 심혈관 수복 및 재건 기기 시장의 장기적인 수요를 직접 뒷받침하는 요인이 되고 있습니다.

경카테터 및 최소 침습적 치료로의 전환

심혈관 수복 및 재건 기기 시장은 경카테터 및 최소 침습적 수복으로의 뚜렷한 임상적 전환에 힘입어 성장하고 있습니다. 일본에서 12년간 진행된 코호트 연구에 따르면, TAVI의 30일 사망률은 2013년 2.8%에서 2024년에는 0.4%로 감소한 반면, 같은 기간 동안 연간 시술 건수는 4배로 증가했습니다. 이러한 치료 성과 개선에 힘입어, 지침의 적용 범위가 저위험 환자군으로 확대되었으며, 규제 당국 입장에서도 새로운 시스템을 승인하기 위한 보다 확고한 근거를 확보하게 되었습니다. 애보트사는 2025년 5월, 중증 승모판 고리 석회화에 대한 "Tendyne TMVR" 시스템에 대해 FDA 승인을 획득했습니다. 이로써, 그동안 외과적 치료나 경카테터 치료의 선택지가 극히 제한적이었던 환자군에게 치료의 길이 열렸습니다. 그 후, 에드워즈사는 2025년 12월, 최초의 경중격 경카테터 승모판 치환 요법으로 "SAPIEN M3" 시스템은 FDA 승인을 획득했으며, 해부학적으로 치료가 어려운 부위에서도 경피적 치료로의 전환이 진행되고 있음을 보여주었습니다. 또한, 독일은 여전히 유럽에서 TAVI 시술 건수가 가장 많은 국가이며, 이는 이미 의료 체계가 확립된 고소득 국가에서도 적응증의 확대에 따라 새로운 환자 사례가 계속해서 발생하고 있음을 보여줍니다.

첨단 밸브 및 그래프트 플랫폼의 높은 자본 집약도

심혈관 수복 및 재건 기기 시장은 여전히 자금 면에서 뚜렷한 장벽에 직면해 있습니다. 이는 첨단 밸브 시스템이나 그래프트 플랫폼의 조달 및 도입에 막대한 비용이 소요되기 때문입니다. 첨단 경카테터 판막 및 차세대 이식편 기술의 건당 이식 비용은 2만 5,000달러에서 5만 달러에 달하며, 이는 비용에 민감한 의료 시스템에서 도입을 제한하는 요인이 될 수 있습니다. 보스턴 사이언티피크(Boston Scientific)가 Acurate neo2 및 Acurate Prime 플랫폼이 FDA 승인을 받지 못함에 따라 2025년에 이들 제품의 전 세계 판매를 중단하기로 결정한 것은 특히 임상 투자 결과가 상업적 시장 진출로 이어지지 않을 경우 장기적인 개발 주기가 얼마나 높은 비용을 초래할 수 있는지를 보여줍니다. 중소득 국가 시장에서도 병원에는 하이브리드 수술실, 첨단 3D 영상 진단 시스템, 그리고 다양한 전문직으로 구성된 구조적 심장 질환 치료팀이 필요하지만, 이러한 시설 요건에 드는 비용은 대개 500만 달러 이상에 달할 전망입니다. 이러한 비용 구조는 폭넓은 제품 포트폴리오를 보유한 대형 제조업체의 입지를 강화시켜, 단일 제품으로 시장 진출기업이 심혈관 수복 및 재건 기기 시장에 혁신을 가져오기 어렵게 만들고 있습니다.

부문별 분석

2025년, 심장 판막 복원 기기는 심혈관 수복·재건 기기 시장에서 36.31%의 점유율을 차지하며, 해당 시장에서 가장 큰 제품 카테고리가 되었습니다. 이러한 위상은 대동맥판막 협착증, 승모판 역류증, 그리고 발전 단계에 있는 삼첨판 질환 분야에서 수행된 수술 건수가 많음을 반영하고 있습니다. 에드워즈 라이프사이언시스(Edwards Life Sciences)는 자사의 조직 생체 판막 "RESILIA"를 대상으로 한 COMMENCE 대동맥 연구에서 10년 시점에서 구조적 판막 퇴화 발생률이 97.9%였으며, 구조적 판막 퇴화로 인한 재수술률이 97.8%였습니다고 보고했습니다. 이는 밸브의 수명을 연장하기 위한 전략과, 더 젊은 수술 환자에게 폭넓게 적용할 수 있음을 뒷받침하는 것입니다. 좌심방귀개 폐쇄 기기(LAAC)는 2031년까지 연평균 성장률(CAGR)이 7.38%로, 가장 빠르게 성장하고 있는 제품 유형입니다. 이는 출혈 위험이 높은 심방세동 환자에서 LAAC가 장기 항응고 요법을 대체할 수 있는 기계적 치료 옵션이 될 수 있다는 근거에 뒷받침되고 있습니다.

2024년에 발표된 OPTION 임상시험에서는 카테터 절제술 후 36개월 동안 LAAC가 경구용 항응고 요법과 동등하거나 그 이상의 효과를 보였으며, 시술과 무관한 중증 출혈의 발생률도 낮은 것으로 나타났습니다. LAAC 분야의 제품 혁신도 가속화되고 있으며, 애보트사는 2026년 2월에 ““Amulet 360”에 관한 VERITAS 임상시험의 초기 결과가 양호했다고 보고한 한편, 보스턴 사이언티피크사의 'WATCHMAN Elite' IDE 시험은 2026년에 피험자 등록을 시작할 전망입니다. 이러한 경쟁 심화로 인해 시술 건수는 증가할 것이며, 향후 가격 면에서의 압박이 커질 것으로 예측됩니다. 혈관 이식편, 심혈관 패치 및 판막 고리 형성 시스템은 서로 상호 보완적인 해부학적 요구를 지속적으로 충족시키고 있으며, 생체 흡수성 도관 플랫폼이 EU에서 주요 임상시험 단계로 진입함에 따라 혈관 이식편에 대한 관심이 높아지고 있습니다.

2025년, 생체 조직은 33.24%의 점유율을 기록하며 심혈관 수복 및 재건 기기 시장에서 계속해서 주요 소재 기반으로서의 위상을 유지했습니다. 이러한 우위는 외과용 생체 판막, 심막 패치 및 조직공학을 이용한 혈관 구조물 분야에서 다년간 축적된 임상 사용 실적을 바탕으로 합니다. RESILIA 심막 조직 플랫폼은 10년 시점에서 구조적 판막 열화 발생률이 97.9%에 달하지 않음을 입증함으로써, 경쟁하는 생체 재료 제제에 비해 높은 내구성 기준을 확립하고 있습니다. 생체흡수성 및 하이브리드 소재는 가장 빠르게 성장하고 있는 소재 부문이며, 심혈관 수복 및 재건 기기 시장에서 해당 부문의 규모는 2031년까지 연평균 성장률(CAGR) 8.52%로 확대될 것으로 전망됩니다. 이는 임상의들이 흡수되기 전에 생체 조직의 재생을 돕는 임플란트에 큰 관심을 보이고 있기 때문입니다.

Xeltis사는 2026년, 자사의 aXess 수복용 혈관 접근 도관에 대한 12개월간의 주요 데이터를 발표하며, 기존의 ePTFE 동정맥 이식편과 비교했을 때 2차 개존율이 79%였으며, 재시술률이 60% 감소했음을 보여주었습니다. 또한, Xeltis사의 "Xabg" 복원용 관상동맥 우회로 컨듀이트에 대한 전임상 및 초기 임상 연구 역시, 현재 승인된 기성품이 없는 소경 우회로 치료 분야에서 향후 활용 가능성을 시사하고 있습니다. 합성 고분자 및 금속·합금은 여전히 특정 상황에서 필수적이며, ePTFE와 폴리에스터는 말초 우회 수술의 요구를 충족시키고, 니티놀과 코발트-크롬은 자가 팽창형 전달 프레임을 지탱하고 있습니다. 하이브리드 및 생체흡수성 소재 시스템으로의 전환은 관상동맥용 스캐폴드에 대한 연구에서도 두드러지게 나타났으며, PLLA와 PLGA의 혼합물은 기존의 PLA 플랫폼에 비해 혈관 치유가 개선된 것으로 나타났습니다.

지역별 분석

2025년, 북미는 심혈관 수복·재건 기기 시장 규모의 38.22%를 차지하며, 해당 시장에서 가장 규모가 큰 지역 블록으로 자리매김하고 있습니다. 미국이 이러한 위치를 주도하고 있는 이유는 전 세계 TAVR(경카테터 대동맥판막 치환술) 시술 건수의 절반 이상을 차지하고 있으며, 경카테터 치료 시술 건수에서도 계속해서 견조한 성장세를 보이고 있기 때문입니다. 또한, 이 지역은 주요 플랫폼의 첫 출시 시장으로서의 위상을 유지하고 있으며, 애보트사의 "Tendyne TMVR"는 2025년 5월에, 에드워즈사의 "SAPIEN M3" 승모판 치환 시스템은 2025년 12월에 미국에서 각각 승인되었습니다. 유럽은 2위를 차지하고 있으며, 독일은 유럽 대륙 내에서 가장 많은 TAVI 시술 건수를 기록하고 있습니다. EU의 MDR(의료기기 규정)에 따라 2026년부터 공동 임상 평가가 시작됨에 따라, 새로운 구조적 임플란트의 상용화까지 소요되는 기간이 기존 체계에 비해 길어지고 있으며, 이는 소규모 혁신 기업들에게 더 큰 부담이 되고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.65%를 기록하며 가장 빠르게 성장하고 있는 지역이며, 이 지역의 심혈관 수복 및 재건 기기 시장은 구조적 심장 질환 발생률 증가, 중재적 의료 인프라 확충, 그리고 새로운 기기 분류의 승인으로 인해 성장세가 가속화되고 있습니다. 한국과 호주는 기술 도입을 뒷받침하는 중재 심장학 네트워크와 보험 급여 제도가 확립되어 있어, 중요한 보급 거점이 되고 있습니다. 인도에서도 새로운 TAVR 시술 시스템이 현지 의료 기관에 도입되고, 의사들의 첨단 판막 치료에 대한 이해가 깊어짐에 따라 시술 건수가 증가하는 추세입니다. 아시아태평양의 많은 국가에서는 시술 보급률이 기저 질환을 앓고 있는 환자 수를 아직 따라잡지 못하고 있기 때문에 이 지역의 사업 기회는 여전히 크다고 할 수 있습니다.

남미와 중동 및 아프리카는 심혈관 수복 및 재건 기기 시장에서 점유율은 낮지만, 두 지역 모두 장기적으로 볼 때 큰 성장 잠재력을 지니고 있습니다. 브라질은 심장외과 병원이 집중되어 있고 TAVI 프로그램도 확립되어 있어, 남미 지역 수요를 주도하고 있습니다. 아르헨티나에서는 민간 의료 시스템을 통해, 특히 복잡도가 높은 구조적 심장 중재술의 시술 건수가 증가하고 있습니다. 중동에서는 GCC 국가들이 해외 의료 여행을 줄이기 위해 카테터 검사 수용 능력을 확대하고 있으며, UAE의 프로그램은 더 많은 사례와 더 복잡한 사례를 처리하고 있습니다. 남아프리카공화국은 아프리카 대륙에서 구조적 심장 질환 치료 건수가 가장 많은 국가로 기록되고 있어, 사하라 이남 아프리카에서 계속해서 핵심적인 위치를 차지하고 있습니다. 두 지역 모두에서 의료기기의 가격 책정은 여전히 장벽으로 작용하고 있으며, 이로 인해 하이브리드 조달 모델에 대한 의존도가 높아지면서 아시아태평양이나 북미에 비해 성장세가 둔화되고 있습니다. 따라서 각 제약사는 예산이 제한된 조달 환경에서 처방약 목록에 등재되기 위해 단계적인 제품 포트폴리오와 의료경제학적 근거를 더욱 중시하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the cardiovascular repair and reconstruction devices market size is projected to be USD 5.03 billion in 2025, USD 5.37 billion in 2026, and reach USD 7.51 billion by 2031, growing at a CAGR of 6.92% from 2026 to 2031.

This report is Segmented by Product (Heart Valve Repair, Vascular Grafts, Patches, Annuloplasty, LAAC), Material (Biological, Synthetic, Metal, Bioabsorbable Hybrid), Application (CAD, Heart Valve Disease, Peripheral Vascular, Structural Heart), End User (Hospitals, Cath Labs, Ascs, Specialty Cardiac), and Geography (North America, Europe, and More). Forecast: Value (USD).

Global Cardiovascular Repair and Reconstruction Devices Market Trends and Insights

Rising Burden of Structural Heart and Vascular Disease

The cardiovascular repair and reconstruction devices market is benefiting from a disease base that remains large and still rising in absolute volume. Non-rheumatic valvular heart disease recorded 28.4 million prevalent cases globally in 2021, and global incidence is projected to reach 20.28 per 100,000 by 2035. TAVI volumes reached 150,000 procedures annually by 2021, yet the treatable valve population remains much larger, which shows that access limits, not disease absence, still hold back volumes in many emerging settings. As PCI and EP ablation capacity expands across Southeast Asia and Latin America, structural heart programs are likely to follow the same hospital adoption path already seen in other interventional services. The gap between rising case counts and lower age-standardized mortality rates shows that device-based intervention is taking on a growing share of incremental patient management, which directly supports long-run demand in the cardiovascular repair and reconstruction devices market.

Shift Toward Transcatheter and Minimally Invasive Repair

The cardiovascular repair and reconstruction devices market is also being lifted by a clear clinical shift toward transcatheter and minimally invasive repair. In a 12-year Japanese cohort, 30-day TAVI mortality fell from 2.8% in 2013 to 0.4% in 2024, while annual case volume increased fourfold over the same period. This improvement in outcomes has supported guideline expansion into lower-risk patient groups and has given regulators a stronger basis for approving newer systems. Abbott received FDA approval in May 2025 for the Tendyne TMVR system for severe mitral annular calcification, which opened a patient group that had very limited surgical or transcatheter options before that point. Edwards then received FDA approval in December 2025 for the SAPIEN M3 system as the first transseptal transcatheter mitral replacement therapy, showing that even difficult anatomical positions are moving toward percutaneous treatment. Germany also remains the highest-volume TAVI country in Europe, which indicates that established high-income systems are still generating new volume as indications widen.

High Capital Intensity of Advanced Valve and Graft Platforms

The cardiovascular repair and reconstruction devices market still faces a clear funding barrier because advanced valve systems and graft platforms remain expensive to procure and deploy. Per-implant costs for advanced transcatheter valves and next-generation graft technologies range from USD 25,000 to USD 50,000, which can limit adoption in cost-sensitive health systems. Boston Scientific's 2025 decision to discontinue global sales of Acurate neo2 and Acurate Prime after the platforms failed to secure FDA clearance shows how costly long development cycles can become, especially when clinical investment does not convert into commercial access. In middle-income markets, hospitals also need hybrid operating suites, advanced 3D imaging systems, and multidisciplinary structural heart teams, and these facility requirements often amount to USD 5 million or more. This cost structure strengthens the position of large manufacturers with broad portfolios and makes it harder for single-product entrants to disrupt the cardiovascular repair and reconstruction devices market.

Other drivers and restraints analyzed in the detailed report include:

- Aging and Frailty-Driven Surgical Risk Profile

- Imaging-Guided Device Navigation and Procedure Planning

- Lengthy Regulatory Pathways for Class III Cardiovascular Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heart Valve Repair Devices held 36.31% of the cardiovascular repair and reconstruction devices market share in 2025, which made them the largest product category in the cardiovascular repair and reconstruction devices market. This position reflects strong procedure volumes across aortic stenosis, mitral regurgitation, and the developing tricuspid disease space. Edwards Lifesciences reported 97.9% freedom from structural valve deterioration and 97.8% freedom from reoperation due to structural valve deterioration at 10 years in the COMMENCE aortic trial for its RESILIA tissue bioprosthesis, which supports longer lifetime valve strategies and broader use in younger surgical patients. Left Atrial Appendage Closure Devices are the fastest-growing product type at 7.38% CAGR through 2031, supported by evidence that LAAC can act as a mechanical alternative to long-term anticoagulation in atrial fibrillation patients with high bleeding risk.

The OPTION trial published in 2024 showed LAAC was noninferior to oral anticoagulation after catheter ablation over 36 months and also delivered a lower rate of non-procedural major bleeding. Product innovation in LAAC is also accelerating, with Abbott reporting positive early VERITAS study results for Amulet 360 in February 2026 while Boston Scientific's WATCHMAN Elite IDE trial is expected to begin enrolling in 2026. This competitive build-out is likely to lift procedure volumes and place more pressure on pricing over time. Vascular Grafts, Cardiovascular Patches, and Annuloplasty Systems continue to serve complementary anatomical needs, and vascular grafts are drawing more attention as bioabsorbable conduit platforms move through EU pivotal development.

Biological Tissue captured 33.24% share in 2025, which kept it as the leading material base in the cardiovascular repair and reconstruction devices market. Its lead rests on long clinical use across surgical valve bioprostheses, pericardial patches, and tissue-engineered vascular constructs. The RESILIA bovine pericardial tissue platform has now shown 97.9% freedom from structural valve deterioration at 10 years, which sets a high durability threshold for competing biological formulations. Bioabsorbable and Hybrid Materials represent the fastest-growing material category, and this cardiovascular repair and reconstruction devices market size for the segment is projected to expand at 8.52% CAGR through 2031 because clinicians are showing stronger interest in implants that support native tissue regeneration before resorption.

Xeltis reported 12-month pivotal data for its aXess restorative vascular access conduit in 2026, showing 79% secondary patency and 60% fewer reinterventions than conventional ePTFE arteriovenous grafts. Preclinical and early clinical work on Xeltis' Xabg restorative coronary bypass conduit also points to future use in small-diameter bypass settings where no approved off-the-shelf option exists today. Synthetic Polymers and Metals and Alloys still remain essential in defined settings, with ePTFE and polyester serving peripheral bypass needs and nitinol or cobalt-chromium supporting self-expanding delivery frames. The shift toward hybrid and bioresorbable material systems is also visible in coronary scaffold research, where a PLLA and PLGA blend showed improved vessel healing versus conventional PLA platforms.

Complete Report Scope:

- By Product Type

- Cardiovascular Repair Devices

- Heart Valve Repair Devices

- Vascular Grafts

- Cardiovascular Patches

- Annuloplasty Systems

- Left Atrial Appendage Closure Devices

- By Material

- Biological Tissue

- Synthetic Polymers

- Metals and Alloys

- Bioabsorbable and Hybrid Materials

- By Application

- Coronary Artery Disease

- Heart Valve Disease

- Peripheral Vascular Repair

- Structural Heart Disease

- By End User

- Hospitals

- Cardiac Catheterization Laboratories

- Ambulatory Surgical Centers

- Specialty Cardiac Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 38.22% share of the cardiovascular repair and reconstruction devices market size in 2025, making it the leading regional block in the cardiovascular repair and reconstruction devices market. The United States anchors this position because it performs more than half of all TAVR implants globally and continues to post strong growth in transcatheter repair volumes. The region also remains the first launch market for major platforms, with Abbott's Tendyne TMVR approved in May 2025 and Edwards' SAPIEN M3 mitral replacement system approved in December 2025 in the United States. Europe holds the second-largest position, and Germany performs the highest TAVI volumes on the continent. Under EU MDR, and with joint clinical assessments starting in 2026, commercialization timelines for novel structural implants are lengthening compared with the earlier framework, which is a larger burden for smaller innovators.

Asia-Pacific is the fastest-growing region at 7.65% CAGR over 2026-2031, and the cardiovascular repair and reconstruction devices market there is gaining from rising structural disease incidence, broader interventional infrastructure, and approvals for newer device classes. South Korea and Australia serve as important adoption anchors because both have established interventional cardiology networks and reimbursement structures that support technology uptake. India is also gaining procedural momentum as newer TAVR delivery systems reach local centers and broaden physician familiarity with advanced valve therapy. The regional opportunity remains large because procedure penetration still trails the underlying disease base in many Asia-Pacific countries.

South America and the Middle East and Africa contribute smaller shares to the cardiovascular repair and reconstruction devices market, but both regions offer meaningful long-term room for expansion. Brazil leads South American demand through its concentration of cardiac surgery hospitals and established TAVI programs. Argentina adds procedure volume through its private healthcare system, especially for higher-complexity structural interventions. In the Middle East, GCC countries are expanding catheterization capacity to reduce outbound medical travel, and UAE programs are handling more cases and greater complexity. South Africa remains the anchor in sub-Saharan Africa because it records the highest structural heart procedural volumes on the continent. Device pricing remains a barrier in both regions, which keeps adoption tied to hybrid procurement models and slows growth relative to Asia-Pacific or North America. Manufacturers are therefore leaning more on tiered portfolios and health-economics arguments to gain formulary access in constrained purchasing environments.

- Abbott Laboratories

- Artivion, Inc.

- AtriCure

- Beckton Dickinson

- BIOTRONIK

- Boston Scientific

- Cardiac Dimensions, Inc.

- Cook Group

- Corcym S.r.l.

- Edward Lifesciences

- Getinge

- Jenavalve Technology

- LeMaitre Vascular

- LivaNova

- Medtronic

- MicroPort

- Neovasc Inc.

- Teleflex

- Terumo

- W. L. Gore and Associates, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Structural Heart and Vascular Disease

- 4.2.2 Shift Toward Transcatheter and Minimally Invasive Repair

- 4.2.3 Aging and Frailty-Driven Surgical Risk Profile

- 4.2.4 Imaging-Guided Device Navigation and Procedure Planning

- 4.2.5 Hospital Ambulatory Migration for Selected Cardiac Interventions

- 4.2.6 Demand for Durable, Reintervention-Reducing Implants

- 4.3 Market Restraints

- 4.3.1 High Capital Intensity of Advanced Valve and Graft Platforms

- 4.3.2 Lengthy Regulatory Pathways for Class III Cardiovascular Devices

- 4.3.3 Reimbursement Friction for Newer Structural Heart Technologies

- 4.3.4 Long-Term Evidence Requirements for Implant Durability and Patency

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Cardiovascular Repair Devices

- 5.1.2 Heart Valve Repair Devices

- 5.1.3 Vascular Grafts

- 5.1.4 Cardiovascular Patches

- 5.1.5 Annuloplasty Systems

- 5.1.6 Left Atrial Appendage Closure Devices

- 5.2 By Material

- 5.2.1 Biological Tissue

- 5.2.2 Synthetic Polymers

- 5.2.3 Metals and Alloys

- 5.2.4 Bioabsorbable and Hybrid Materials

- 5.3 By Application

- 5.3.1 Coronary Artery Disease

- 5.3.2 Heart Valve Disease

- 5.3.3 Peripheral Vascular Repair

- 5.3.4 Structural Heart Disease

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Cardiac Catheterization Laboratories

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Specialty Cardiac Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Artivion, Inc.

- 6.3.3 AtriCure, Inc.

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Biotronik SE and Co. KG

- 6.3.6 Boston Scientific Corporation

- 6.3.7 Cardiac Dimensions, Inc.

- 6.3.8 Cook Medical LLC

- 6.3.9 Corcym S.r.l.

- 6.3.10 Edwards Lifesciences Corporation

- 6.3.11 Getinge AB

- 6.3.12 JenaValve Technology, Inc.

- 6.3.13 LeMaitre Vascular, Inc.

- 6.3.14 LivaNova PLC

- 6.3.15 Medtronic plc

- 6.3.16 MicroPort Scientific Corporation

- 6.3.17 Neovasc Inc.

- 6.3.18 Teleflex Incorporated

- 6.3.19 Terumo Corporation

- 6.3.20 W. L. Gore and Associates, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space and Unmet-Need Assessment