|

시장보고서

상품코드

2073149

차량용 라우터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vehicle Mounted Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

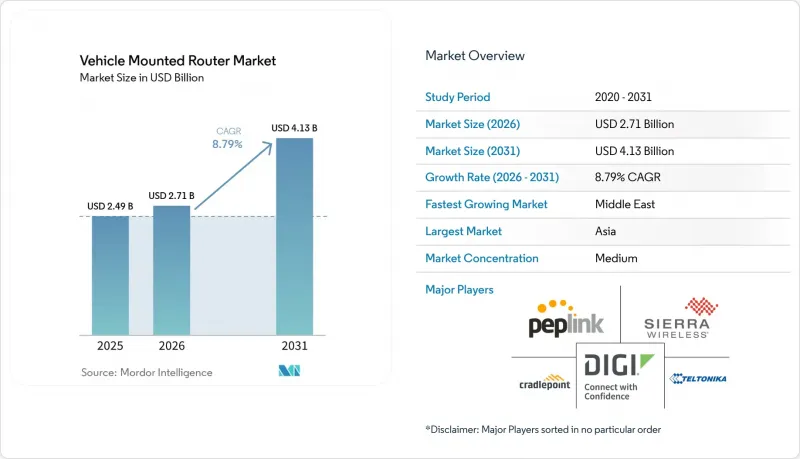

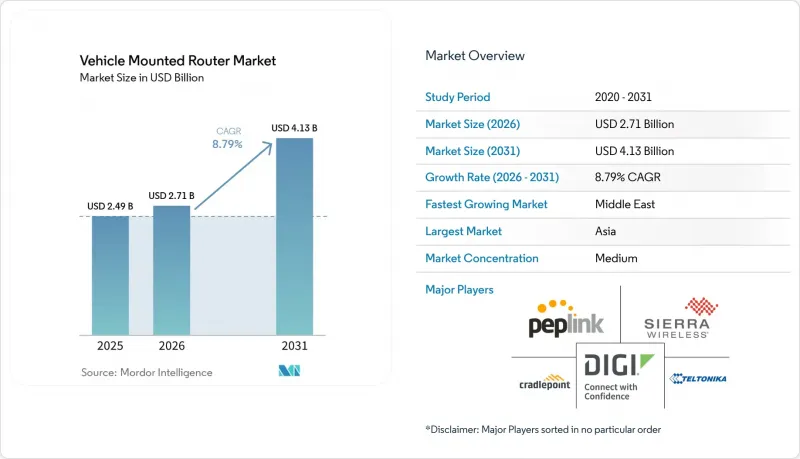

Mordor Intelligence에 의하면, 차량용 라우터 시장 규모는 2025년에 24억 9,000만 달러로 평가되었고 예측 기간(2026-2031년)에서 CAGR 8.79%로 확대되어 2026년 27억 1,000만 달러에서 2031년에는 41억 3,000만 달러에 이를 것으로 추정되고 있습니다.

본 보고서는 연결 기술(5G, 4G LTE, 5G/4G 듀얼, Wi-Fi 6 등), 용도(차량 함대 관리, 차량용 인포테인먼트, 공공 안전 및 긴급 대응 등), 차량 유형(승용차, 소형 상용차 등), 최종 사용자(OEM 탑재, 애프터마켓을 통한 사후 장착 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 차량용 라우터 시장 동향과 인사이트

5G V2X(Vehicle-to-Everything) 규격의 보급

3GPP 릴리스 16 및 17에서는 20밀리초 미만의 지연 시간과 99.999%의 신뢰성이라는 기준치가 공식적으로 규정됨에 따라 기술적 모호성이 해소되었고, 이에 따라 C-V2X 통합을 위한 OEM 차원의 노력이 가속화되고 있습니다. 중국의 정책에 따르면, 2026년까지 신차의 5G 보급률을 50%, 2030년까지 95%로 끌어올리겠다는 목표가 제시되어 있으며, 이에 따라 통신사 중복성과 장애 복구 기능을 갖춘 듀얼 5G 라우터에 대한 수요가 구조적으로 확대되고 있습니다. 유럽에서는 802.11p를 기반으로 하는 C-V2X에 대한 2024년 규제 조정이 이미 주요 OEM 각사의 2026년형 모델 플랫폼 도입 확약으로 이어지고 있습니다. 한편, 한국에서는 2024년부터 모든 신형 상용차에 CV2X 탑재가 의무화되어 있어, 일정한 기준이 되는 판매 대수가 확보되어 있습니다. 12개국에서 30건 이상의 실증 실험이 진행되었으며, 협업형 어댑티브 크루즈 컨트롤 및 위험 신호 등의 활용 사례가 입증되었습니다. 이러한 요인들이 복합적으로 작용하여 지속적인 업그레이드 주기를 만들어내고 있으며, 벤더 간의 경쟁은 인증 범위의 폭, 상호 운용성, 라이프사이클 관리 능력으로 옮겨가고 있습니다.

전자상거래 물류 분야에서 실시간 차량 텔레매틱스에 대한 수요 증가

아마존이나 DHL과 같은 대규모 차량 운영 업체들은 위치 정보, 운전자의 운전 행동, 콜드체인 매개변수 등 고빈도의 텔레매틱스 데이터를 약 30초 간격으로 스트리밍하고 있습니다. 이로 인해 대역폭 활용도가 크게 향상됨에 따라, 라우터는 중요도가 낮은 데이터를 억제하는 내장형 엣지 분석과 병행하여 듀얼 SIM의 장애 복구 기능을 동적으로 관리해야 합니다. 이 아키텍처는 실시간 시각화를 통해 체류 시간과 연료 도난을 줄여주지만, 운송업체의 데이터 비용을 대폭 증가시켜, 많은 경우 1기가바이트당 10달러를 초과함으로써 직접적인 운영 비용 측면에서 상충 관계를 초래하고 있습니다. Shipsy 등의 플랫폼에서 제공한 실증 데이터에 따르면, 일괄 처리에서 지속적인 데이터 전송으로 전환함으로써 야드 내 체류 시간이 최대 18% 단축되는 것으로 나타났습니다. 이와 동시에, 북미 및 유럽에서는 서비스 품질(QoS) 우선순위 지정이 의무화되어 있어, 안전상 중요한 경보가 대량의 텔레메트리 데이터보다 우선시되므로, 라우터 공급업체들은 펌웨어 수준에서 트래픽 셰이핑 및 정책 기반 라우팅을 통합해야 하는 압박을 받고 있습니다. 이러한 효율성 향상과 규제 준수가 결합됨에 따라, 비용 제약이 있는 중견 선단 운영 사업자들도 하드웨어 교체 주기를 유지하고 있습니다.

견고한 자동차용 라우터의 높은 총 소유 비용

듀얼 5G를 지원하는 견고한 라우터의 가격은 대당 4,600달러에 달하며, MIL-STD-810H 준수 검증, IP67 규격의 밀폐 구조, 다중 통신사 인증 등의 규정 준수 비용을 부품 명세서(BOM)에 포함하면, 동등한 4G LTE 하드웨어의 3배 이상의 비용이 듭니다. 이와 더불어, 엔지니어링 비용이 SKU당 50만 달러에 달하기도 하기 때문에 충분한 규모와 폭넓은 인증 실적을 갖춘 벤더로만 현실적인 공급업체 후보가 한정될 수밖에 없습니다. 비용 압박은 남미와 아프리카에서 특히 두드러지는데, 이 지역에서는 소규모 통신 사업자들이 산업용 라우터 대신 보호 케이스에 넣은 소비자용 핫스팟을 대체 수단으로 사용하는 경우가 많아, 초기 비용을 최대 80%까지 절감할 수 있는 반면, 고장률과 수명 주기 동안의 교체 비용이 현저히 높아지는 점을 감수하고 있습니다. 통신 관련 운영 비용(OPEX)도 문제를 더욱 심각하게 만들고 있습니다. 10대의 차량으로 구성된 차량 함대에서 차량 1대당월5GB의 데이터 통신량을 사용할 경우, 연간 약 6,000달러의 비용이 발생합니다. 이는 연비 향상, 가동 중단 시간 단축, 또는 텔레매틱스 도입에 따른 보험료 할인과 같은 정량화 가능한 이익으로 상쇄되지 않는 한, 투자 수익률(ROI)을 저해하게 됩니다.

부문별 분석

커넥티비티 모듈용 차량용 라우터 시장은 여전히 4G LTE가 주류를 이루고 있으며, 2025년에는 시장 점유율의 38.34%를 차지했습니다. 이는 Cat 4부터 Cat 12에 이르는 다양한 제품군이 더 낮은 총소유비용(TCO)으로 텔레매틱스의 대역폭 요구 사항 대부분을 충분히 충족시키기 때문입니다. 그러나 5G 모듈은 안전상 중요한 상황이 발생했을 때 50밀리초 미만의 장애 복구 시간을 확보하기 위해, 두 통신 사업자 간 병렬 연결을 유지하는 듀얼 5G 아키텍처로의 OEM 전환에 힘입어 2031년까지 연평균 성장률(CAGR) 14.26%를 기록하며 성장할 것으로 전망됩니다. 각 벤더사는 Wi-Fi 6 및 6E 무선 기능을 통합하고, 높은 대역폭이 필요한 인포테인먼트 트래픽을 셀룰러 네트워크에서 오프로드함으로써 주파수 대역 효율을 높이고 있습니다. 위성 하이브리드 라우터는 비용 제약으로 인해 광업이나 외딴 지역의 농업과 같은 틈새 시장에서의 도입 사례로만 국한되어 있습니다. 통신 사업자들이 전 세계적으로 3G 인프라를 단계적으로 폐지함에 따라 구형 기기가 도입 기반에서 점차 사라지고 있으며, 특히 도시 지역이나 급성장하는 물류 회랑에서는 고부가가치 5G 라우터의 도입을 구조적으로 뒷받침하는 교체 주기가 형성되고 있습니다.

2세대 듀얼 5G 라우터는 중파대인 C-밴드와 고주파인 mm파 스펙트럼에 걸친 동시 캐리어 어그리게이션을 위해 진화하고 있으며, 제어된 조건에서는 초당 10기가비트에 육박하는 최고 속도를 실현합니다. 물류 사업자에게 있어 이러한 구성은 2025년 2월 미국 대형 통신사의 약 7만 명 사용자에게 영향을 미쳤던 것과 같은 네트워크 장애에 대비한 운영상의 안전장치 역할을 합니다. 신호 품질이 저하되었을 때, 안전상 중요한 데이터 패킷에 동적으로 우선순위를 부여하기 위해 임베디드형 엣지 인텔리전스의 활용이 확대되고 있으며, 이를 통해 20밀리초 전후의 지연 임계값 준수가 보장되고 있습니다. 예측 기간 동안 반도체 비용의 감소와 더욱 표준화된 세계 인증 체계로 인해 4G 모듈과 5G 모듈 간의 가격 차이가 줄어들 것으로 예측됩니다. 이로 인해 5G 도입이 가속화되고, 차세대 차량용 라우터 보급에 있어 주요 연결 계층으로서의 입지가 강화될 것입니다.

2025년에는 물류 및 상업 운송 분야 전반의 기본적인 수요를 뒷받침하는 GPS 추적, 운전자 기록, 규정 준수 보고와 관련된 규제 요건에 힘입어, 차량 관리가 매출의 41.92%를 차지했습니다. 그러나 자율주행 데이터 업링크는 지각 및 의사결정 모델의 지속적인 개선을 위해 방대한 양의 에지 케이스 센서 로그를 전송해야 할 필요성에 힘입어, 2031년까지 연평균 성장률(CAGR) 15.61%를 기록하며 다른 모든 이용 사례를 능가하는 성장을 보일 것으로 전망됩니다. 이 워크로드에는 500 Mbps에 가까운 지속적인 업링크 버스트를 처리할 수 있는 라우터가 필요하며, 하드웨어 사양은 더 높은 처리량을 갖춘 모뎀과 고급 안테나 구성으로 발전하고 있습니다. 이와 동시에, 공공 안전 용도는 평균 이상의 성장세를 보이는 부문으로 자리 잡고 있습니다. 이는 실시간 동영상 스트리밍, 상황 인식 피드, 긴급 차량과 지휘 센터 간의 통합을 통해 지원되며, 이 모든 요소가 라우터 인프라에 대해 엄격한 지연 시간, 신뢰성 및 우선순위 요건을 부과하고 있습니다.

수요 측면에서는 인포테인먼트 서비스 가입자 수가 증가하고 있는 데 따라, 각 OEM 업체들은 공장 출하 단계에서 Wi-Fi 6 및 6E 모듈을 탑재하고 있습니다. 이를 통해 사용 가능한 로컬 네트워크로 고대역폭 컨텐츠를 오프로드함으로써, 셀룰러 백홀 비용을 절감하고 있습니다. 또한, 예측 유지보수 분석도 도입을 뒷받침하고 있으며, 차량 군에서는 지속적인 진단을 활용하여 예기치 못한 가동 중지 시간을 최소화하고 자산의 수명을 연장함으로써 영업이익률을 직접적으로 향상시키고 있습니다. 또한, 모바일 POS 시스템이나 정밀 농업과 같은 틈새 시장 용도는 비록 부분적이긴 하지만 수익 확대에 기여하고 있으며, 특히 용도 수준의 맞춤 설정이 가능한 오픈 펌웨어 환경을 지원하는 벤더에게 유리하게 작용하고 있습니다. 모든 업종에서 서비스 품질(QoS) 확보, 네트워크 슬라이싱 지원, 통합형 사이버 보안 모듈이 조달 기준의 최소 요건으로 자리 잡고 있으며, 이로 인해 프리미엄급 엔터프라이즈급 라우터와 대중화된 저가형 대체 제품이 명확하게 구분되고 있습니다.

지역별 분석

2025년, 아시아태평양은 커넥티드카 인프라의 대규모 구축과 규제 요건에 힘입어 전 세계 매출의 36.24%를 차지했습니다. 중국은 약 776만 대의 C-V2X 지원 차량을 보유하며 1위를 차지하고 있는데, 이는 산업 정책과 통신 생태계 구축 현황 간의 긴밀한 연계성을 반영하고 있습니다. 인도는 AIS 140 규격 준수를 통해 기여하고 있으며, 추적 및 안전 시스템 장착이 의무화된 약 450만 대의 상용차를 대상으로 하고 있습니다. 또한, 일본의 보조금 프로그램과 한국의 규제 시행도 긍정적인 요인으로 작용하고 있으며, 이러한 요인들이 맞물려 승용차 및 상용차 두 부문 모두에서 도입이 가속화되고 있습니다. 이 지역은 수직 통합된 공급망, 낮은 제조 비용, 그리고 적극적인 5G 구축 일정의 혜택을 누리고 있어, 지속적인 판매량 성장과 기술 표준화를 위한 구조적으로 유리한 환경이 조성되어 있습니다.

중동은 기반 규모가 작긴 하지만, 정부 주도의 인프라 구축 프로그램과 전략적인 디지털 전환 노력에 힘입어 2031년까지 연평균 성장률(CAGR) 11.24%라는 가장 높은 성장률을 나타낼 것으로 전망됩니다. 사우디아라비아는 커넥티드 모빌리티와 물류 최적화를 지원하기 위해 고속도로를 기반으로 한 5G 회랑에 대한 투자를 추진하고 있는 반면, 아랍에미리트(UAE)는 2028년까지 C-V2X 커버리지 100%를 달성하기 위한 국가 프로그램을 추진하고 있습니다. 북미는 FirstNet의 전국적 확장을 기반으로, 시범 도입에 대한 연방 정부의 재정 지원을 바탕으로 20%라는 높은 점유율을 유지하고 있지만, 5.9GHz 대역의 주파수 조정 문제가 도로변 인프라 확장의 걸림돌로 계속 작용하고 있습니다. 유럽은 20%대 중반의 점유율을 차지하고 있지만, 802.11p에서 C-V2X 규격으로의 전환으로 인해 투자 사이클이 일시적으로 정체되어 있어 단기적인 성장은 둔화되고 있습니다.

브라질, 남아프리카공화국 및 남미·아프리카 전역의 기타 신흥 시장은 5G 네트워크의 커버리지가 제한적이라는 점과 평균 판매 가격을 300달러 이하로 유지하려는 강한 가격 민감도로 인해 제약을 받고 있어, 총 시장 점유율이 한 자릿수 초반에 그치고 있습니다. 그러나 브라질의 전자 로그 기록 의무화나 남아프리카공화국의 유료 도로 텔레매틱스 실증 실험과 같은 규제 측면의 진전은 초기 단계의 구조적 수요 형성을 시사하고 있습니다. 통신 사업자들이 네트워크 구축 비용을 절감하고 멀티밴드 모뎀 기술의 비용 효율성이 향상됨에 따라, 해당 지역에서 연기되었던 연결 프로젝트들은 예측 기간 후반에 접어들면서 본격적인 구축 단계로 전환될 것으로 예측됩니다. 이러한 전환으로 인해, 단기적인 수익 창출에 제약이 있음에도 불구하고 도입 대수가 점차 확대되어 장기적인 시장 규모 성장에 기여하게 될 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the vehicle-mounted router market size was valued at USD 2.49 billion in 2025 and is estimated to grow from USD 2.71 billion in 2026 to USD 4.13 billion by 2031, at a CAGR of 8.79% during the forecast period (2026-2031).

This report is Segmented by Connectivity Technology (5G, 4G LTE, Dual 5G/4G, Wi-Fi 6 and More), Application (Fleet Management, In-Vehicle Infotainment, Public Safety and Emergency Response, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), End-User (OEM-Installed, Aftermarket Retrofit, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Vehicle Mounted Router Market Trends and Insights

Proliferation Of 5G Vehicle-To-Everything Standards

Releases 16 and 17 of 3GPP formalize sub-20 millisecond latency and 99.999% reliability thresholds, removing technical ambiguity and accelerating OEM-level commitment to C V2X integration. China's policy targets 50% 5G penetration in new vehicles by 2026 and 95% by 2030, structurally expanding demand for dual 5G routers with carrier redundancy and failover capabilities. Europe's 2024 regulatory alignment toward C V2X over 802.11p has already translated into model year 2026 platform commitments from major OEMs, while South Korea's mandate for C V2X in all new commercial vehicles from 2024 ensures baseline volume. Over 30 live pilots across 12 countries validate use cases such as cooperative adaptive cruise control and hazard signaling, collectively creating a sustained upgrade cycle and shifting vendor competition toward certification breadth, interoperability, and lifecycle management capabilities.

Rising Demand For Real-Time Fleet Telematics In E-Commerce Logistics

Large fleet operators such as Amazon and DHL stream high-frequency telematics, including location, driver behavior, and cold-chain parameters, at roughly 30-second intervals, which materially increases bandwidth utilization and forces routers to dynamically manage dual SIM failover alongside embedded edge analytics that suppress non-critical data. This architecture reduces detention times and fuel pilferage through real-time visibility but materially increases carrier data costs, often exceeding USD 10 per gigabyte, creating a direct operating expense trade-off. Empirical evidence from platforms such as Shipsy indicates up to 18% reduction in yard dwell time when transitioning from batch to continuous data transmission. In parallel, North America and Europe are enforcing Quality of Service prioritization, where safety-critical alerts override bulk telemetry, pushing router vendors to integrate traffic shaping and policy-based routing at the firmware level. This combination of efficiency gains and regulatory alignment sustains hardware refresh cycles, even among cost-constrained mid-market fleet operators.

High Total Cost Of Ownership For Ruggedized Automotive Routers

Dual 5G rugged routers are priced near USD 4,600 per unit, more than 3x the cost of comparable 4G LTE hardware once compliance costs such as MIL-STD-810H validation, IP67 sealing, and multi-carrier certification are included in the bill of materials. In parallel, engineering outlays can reach USD 500,000 per SKU, constraining the viable supplier base to vendors with sufficient scale and depth of certification. Cost pressure is most visible in South America and Africa, where smaller fleets often substitute industrial routers with consumer-grade hotspots placed in protective enclosures, capturing up to 80% upfront savings but accepting materially higher failure rates and lifecycle replacement costs. Connectivity opex compounds the issue: a 10-vehicle fleet consuming 5 GB per month per unit incurs roughly USD 6,000 annually, which compresses ROI unless offset by quantifiable gains such as fuel efficiency improvements, reduced downtime, or insurance premium discounts tied to telematics adoption.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption Of Connected Emergency Response Vehicles

- OEM Integration Of Over-The-Air Software Update Capabilities

- Interoperability Challenges Among Multi-Carrier Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The vehicle-mounted router market for connectivity modules remains anchored in 4G LTE, which accounted for 38.34% of the market in 2025, as Cat 4 to Cat 12 variants sufficiently meet most telematics bandwidth requirements at a lower total cost of ownership. However, 5G modules are projected to grow at a 14.26% CAGR through 2031, driven by OEM migration toward dual 5G architectures that maintain parallel connections across two carriers to ensure sub-50 millisecond failover during safety-critical events. Vendors are increasingly integrating Wi-Fi 6 and 6E radios to offload high-bandwidth infotainment traffic from cellular networks, improving spectrum efficiency. Satellite hybrid routers remain limited to niche deployments such as mining and remote agriculture due to cost constraints. As telecom operators phase out 3G infrastructure globally, legacy devices are exiting the installed base, triggering a replacement cycle that structurally supports higher-value 5G router adoption, particularly in urban and high-growth logistics corridors.

Second-generation dual 5G routers are advancing toward simultaneous carrier aggregation across the mid-band C-band and high-frequency millimeter-wave spectrum, enabling peak speeds approaching 10 gigabits per second under controlled conditions. For logistics operators, this configuration functions as operational insurance against network disruptions, such as the February 2025 outage that impacted approximately 70,000 users on a major United States carrier. Embedded edge intelligence is increasingly used to dynamically prioritize safety-critical data packets when signal quality deteriorates, ensuring compliance with latency thresholds near 20 milliseconds. Over the forecast horizon, declining semiconductor costs and more standardized global certification frameworks are expected to compress the price differential between 4G and 5G modules, accelerating adoption and reinforcing 5G as the primary connectivity layer for next-generation vehicle-mounted router deployments.

Fleet management accounted for 41.92% of revenue in 2025, anchored by regulatory mandates around GPS tracking, driver logging, and compliance reporting that sustain baseline demand across logistics and commercial transport. However, autonomous driving data uplink is set to outpace all other use cases with a 15.61% CAGR through 2031, driven by the need to transmit high volume edge case sensor logs for continuous refinement of perception and decision models. This workload requires routers capable of sustained uplink bursts near 500 Mbps, pushing hardware specifications toward higher throughput modems and advanced antenna configurations. In parallel, public safety applications represent an above average growth segment, supported by real time video streaming, situational awareness feeds, and command center integration in emergency vehicles, all of which impose stringent latency, reliability, and prioritization requirements on router infrastructure.

On the demand side, rising infotainment subscriptions are incentivizing OEMs to embed Wi Fi 6 and 6E modules at the factory level, reducing cellular backhaul costs by offloading high bandwidth content to local networks where available. Predictive maintenance analytics further reinforce adoption, as fleets leverage continuous diagnostics to minimize unplanned downtime and extend asset life cycles, directly improving operating margins. At the margin, niche applications such as mobile point of sale systems and precision agriculture contribute a fragmented but expanding revenue tail, particularly favoring vendors that support open firmware environments for application level customization. Across all verticals, quality of service enforcement, network slicing compatibility, and integrated cybersecurity modules are becoming baseline procurement criteria, effectively separating premium, enterprise grade routers from commoditized low cost alternatives.

Complete Report Scope:

- By Connectivity Technology

- 5G

- 4G LTE

- Dual 5G/4G

- Wi-Fi 6 and 6E

- Satellite Hybrid

- Rest of Connectivity Technology

- By Application

- Fleet Management

- In-Vehicle Infotainment

- Public Safety and Emergency Response

- Autonomous Driving Data Uplink

- Predictive Maintenance

- Rest of Application

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Emergency and Specialty Vehicles

- Rest of Vehicle Type

- By End-User

- OEM-Installed

- Aftermarket Retrofit

- Mobility-as-a-Service Providers

- Rest of End-User

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Asia Pacific accounted for 36.24% of global revenue in 2025, supported by the large-scale deployment of connected vehicle infrastructure and regulatory mandates. China leads with approximately 7.76 million C V2X-enabled vehicles, reflecting strong alignment between industrial policy and telecom ecosystem readiness. India contributes through AIS 140 compliance, covering about 4.5 million commercial vehicles with mandated tracking and safety systems. Additional momentum comes from subsidy programs in Japan and regulatory enforcement in South Korea, which collectively accelerate adoption across both passenger and commercial segments. The region benefits from vertically integrated supply chains, lower manufacturing costs, and aggressive 5G rollout timelines, creating a structurally favorable environment for sustained volume growth and technology standardization.

The Middle East is projected to record the fastest growth at 11.24% CAGR through 2031, albeit from a smaller base, driven by government-backed infrastructure programs and strategic digital transformation initiatives. Saudi Arabia is investing in highway-based 5G corridors to support connected mobility and logistics optimization, while the United Arab Emirates is advancing national programs to achieve 100% C-V2X coverage by 2028. North America maintains a high 20% share, anchored by FirstNet's nationwide footprint and supported by federal funding for pilot deployments, although spectrum coordination challenges in the 5.9 GHz band continue to slow roadside infrastructure expansion. Europe holds a mid-20 % share, but near-term growth is moderated by the transition from 802.11p to C V2X standards, creating a temporary pause in investment cycles.

Brazil, South Africa, and other emerging markets across South America and Africa together represent a low single-digit share, constrained by limited 5G network coverage and strong price sensitivity that caps average selling prices below USD 300. However, regulatory developments such as electronic logging mandates in Brazil and toll road telematics pilots in South Africa indicate early-stage structural demand formation. As telecom operators reduce network deployment costs and multi-band modem technologies become more cost-efficient, deferred connectivity projects in these regions are expected to convert into active deployments toward the latter half of the forecast period. This transition will incrementally expand the installed base and contribute to long term market volume growth despite near term monetization constraints.

- Sierra Wireless, Inc.

- Cradlepoint, Inc.

- Peplink International Limited

- Digi International Inc.

- Teltonika Networks UAB

- Advantech Co., Ltd.

- NetModule AG

- Perle Systems Limited

- Kontron AG

- LILEE Systems, Inc.

- Teldat Group

- InHand Networks Co., Ltd.

- MOXA Inc.

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Viprinet Europe GmbH

- CalAmp Corp.

- MikroTikls SIA (MikroTik)

- CommScope Holding Company, Inc.

- Proscend Communications Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of 5G Vehicle-to-Everything Standards

- 4.2.2 Rising Demand for Real-Time Fleet Telematics in E-Commerce Logistics

- 4.2.3 Increasing Adoption of Connected Emergency Response Vehicles

- 4.2.4 OEM Integration of Over-the-Air Software Update Capabilities

- 4.2.5 Regulatory Mandates for eCall and Intelligent Transport Systems

- 4.2.6 Emergence of Edge-Enabled Content Delivery for In-Vehicle Infotainment

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Ruggedized Automotive Routers

- 4.3.2 Interoperability Challenges Among Multi-Carrier Networks

- 4.3.3 Data Privacy and Cybersecurity Concerns Limiting Adoption

- 4.3.4 Supply Chain Constraints of Automotive-Grade Chipsets

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Connectivity Technology

- 5.1.1 5G

- 5.1.2 4G LTE

- 5.1.3 Dual 5G/4G

- 5.1.4 Wi-Fi 6 and 6E

- 5.1.5 Satellite Hybrid

- 5.1.6 Rest of Connectivity Technology

- 5.2 By Application

- 5.2.1 Fleet Management

- 5.2.2 In-Vehicle Infotainment

- 5.2.3 Public Safety and Emergency Response

- 5.2.4 Autonomous Driving Data Uplink

- 5.2.5 Predictive Maintenance

- 5.2.6 Rest of Application

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Emergency and Specialty Vehicles

- 5.3.5 Rest of Vehicle Type

- 5.4 By End-User

- 5.4.1 OEM-Installed

- 5.4.2 Aftermarket Retrofit

- 5.4.3 Mobility-as-a-Service Providers

- 5.4.4 Rest of End-User

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sierra Wireless, Inc.

- 6.4.2 Cradlepoint, Inc.

- 6.4.3 Peplink International Limited

- 6.4.4 Digi International Inc.

- 6.4.5 Teltonika Networks UAB

- 6.4.6 Advantech Co., Ltd.

- 6.4.7 NetModule AG

- 6.4.8 Perle Systems Limited

- 6.4.9 Kontron AG

- 6.4.10 LILEE Systems, Inc.

- 6.4.11 Teldat Group

- 6.4.12 InHand Networks Co., Ltd.

- 6.4.13 MOXA Inc.

- 6.4.14 Cisco Systems, Inc.

- 6.4.15 Huawei Technologies Co., Ltd.

- 6.4.16 Viprinet Europe GmbH

- 6.4.17 CalAmp Corp.

- 6.4.18 MikroTikls SIA (MikroTik)

- 6.4.19 CommScope Holding Company, Inc.

- 6.4.20 Proscend Communications Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment