|

시장보고서

상품코드

2073151

감염증 체외진단 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Infectious Disease In Vitro Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

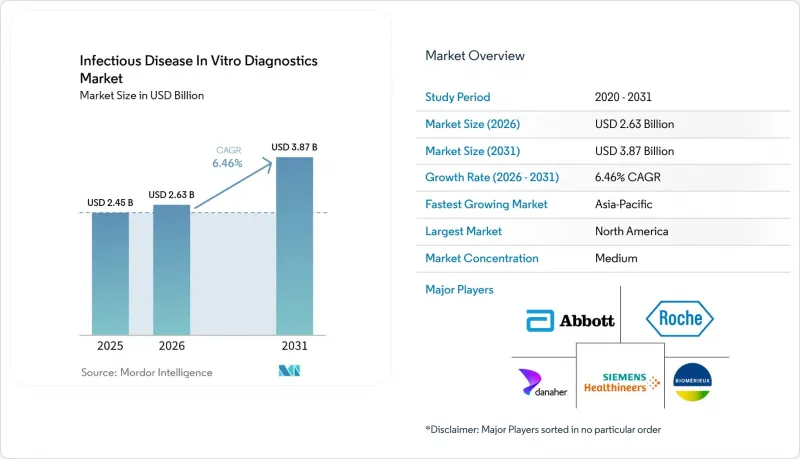

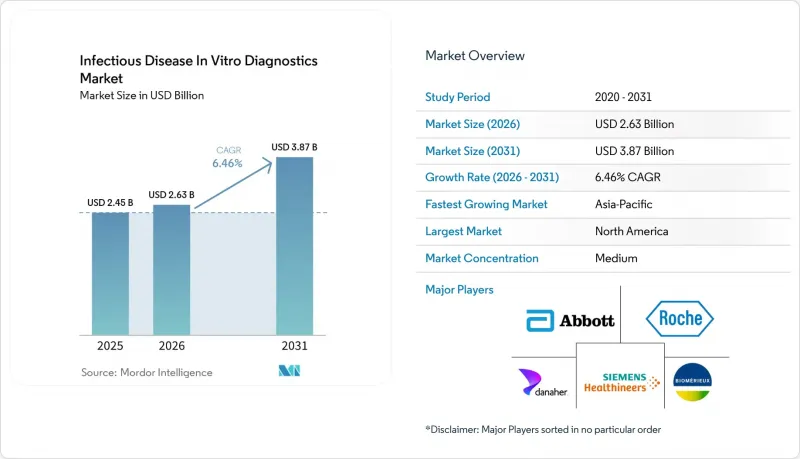

Mordor Intelligence에 의하면, 감염증 체외진단 시장 규모는 2025년에 24억 5,000만 달러, 2026년에 26억 3,000만 달러되어, 2031년까지 38억 7,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 6.46%로 성장할 전망입니다.

본 보고서는 제품별(시약, 기기, 소프트웨어), 검사 유형별(실험실, POC), 검체별(혈액/혈청, 소변, 기타), 질환별(간염 등), 기술별(면역진단, PCR, NGS, INAAT, 기타), 용도(진단, 스크리닝), 최종 사용자(진단실험실 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 감염증 체외진단 시약 시장 동향 및 인사이트

호흡기 감염증 및 혈류 감염증으로 인한 부담 증가

감염증 체외진단 시장은 병원과 지역 사회 모두에서 호흡기 감염증, 혈류 감염증, 요로 감염증 및 소화기 감염증이 여전히 존재하고 있기 때문에 계속해서 가장 강력한 기초 수요를 확보하고 있습니다. WHO의 “GLASS 2025” 보고서는 2016년부터 2023년까지 110개국에서 보고된 2,300만 건 이상의 세균학적으로 확인된 사례를 분석한 것으로, 몇 가지 주요 감염증 범주에서 항생제 내성 병원체의 비율이 정체되거나 증가하는 추세를 보이고 있는 것으로 나타났습니다. 이러한 추세는 감염증 체외진단 시장에 있어 중요한 의미를 지닙니다. 왜냐하면, 확정 진단률이 높은 환경은 검사 인프라가 잘 갖춰진 국가들에 집중되어 있는 반면, 질병 부담이 큰 지역에서는 여전히 진단이 미흡한 상태가 지속되고 있기 때문입니다. 이러한 격차로 인해 수요는 당장의 검사 건수뿐만 아니라 남아시아, 사하라 이남 아프리카, 그리고 라틴아메리카 일부 지역의 향후 검사 시설 확충으로도 이어지고 있습니다. 병원 내 감염은 새로운 수요층을 창출합니다. 이는 혈류 감염의 경우, 치료 시작 후 48시간 이내에 적절한 조치를 취하기 위해서는 신속한 병원체 확인과 조기 항생제 선정이 필요하기 때문입니다. 따라서 감염증 체외진단 시장은 감염 발생률의 상승은 물론, 보다 신속하고 신뢰할 수 있는 검사를 통한 임상 판단 지원에 대한 수요 증가라는 두 가지 요인의 혜택을 동시에 누리고 있습니다.

증후군 기반의 다항목 검사 플랫폼으로의 전환

병원들이 신속한 진단과 직원 및 장비 사용 시간의 효율화를 동시에 달성하고자 노력하는 가운데, 감염증 체외진단 시장에서는 증후군별 다항목 검사로의 명확한 전환이 나타나고 있습니다. QIAGEN사는 2026년 3월, QIAstat-Dx Rise 시스템용 소화기 계통 패널에 대해 FDA 승인을 획득했습니다. 또한, 보다 광범위한 QIAstat-Dx 플랫폼의 경우, 100개국 이상에 5,200대 이상의 장비가 도입되어 있습니다. 이러한 도입 실적이 중요한 이유는 호흡기계, 소화기계 및 신종 병원체 패널을 지원하는 플랫폼이 있다면 병원이 검사 항목을 통합하여 구매하고, 수년에 걸쳐 시약을 지속적으로 구매할 것을 약속할 수 있기 때문입니다. bioMerieux사는 2026년 3월, 현장 진단(Point-of-Care) 환경에서 15분 이내에 15종의 병원체를 검출할 수 있는 “BIOFIRE SPOTFIRE R/STplus 패널”에 대해 IVDR CE 마크를 취득했습니다. 다중 검사의 신속화는 항생제 적정 사용 촉진에도 기여합니다. 왜냐하면, 진료 과정의 초기 단계에서 병원체가 확인되면, 임상의는 광범위한 경험적 처방을 줄일 수 있기 때문입니다. 따라서 감염증 체외진단 시장은 단순히 검사 항목의 확충뿐만 아니라, 비용 관리, 처리 능력, 치료의 질과 같은 요소들을 이러한 플랫폼과 연계하는 새로운 구매 논리에 힘입어 혜택을 보고 있습니다.

분자진단 플랫폼 및 검사용 소모품의 높은 비용

감염증 체외진단 시장은 분자진단 시스템과 그 운영에 필요한 소모품 비용이라는 여전히 큰 진입 장벽에 직면해 있습니다. 다항목 증후군 패널은 단일 표적의 측면 유동 방식에 비해 검사당 비용이 5-10배 더 비싼 경우가 많아, 그로 인해 저소득 지역의 많은 1차 진료 및 지역 의료 현장에서는 현실적으로 구매 대상에서 제외되고 있습니다. ScienceDirect에 게재된 2026년 연구에서는 검체 채취부터 결과 도출까지 30분 미만이 소요되며, 검사당 비용이 1.5달러인 휴대용 마이크로플루이딕스 핵산 증폭 시스템이 소개되었습니다. 이러한 대비는 감염증 체외진단 시장의 상당 부분이, 감염증 부담이 크고 자원이 부족한 지역에서 보급 가능한 가격대에서 여전히 얼마나 멀리 떨어져 있는지를 보여줍니다. 병원이 광범위한 패널 검사 비용을 감당할 수 없는 경우, 더 저렴한 단일 표적 검사법으로 전환하는 경우가 많으며, 그 결과 동반 감염을 놓치거나 치료 선택지가 좁아질 우려가 있습니다. 시약 대여나 검사 건수에 따른 가격 책정은 어느 정도 도움이 되기는 하지만, 시장의 더 큰 확산을 가로막고 있는 합리적인 가격과의 격차는 아직 해소되지 못하고 있습니다.

부문별 분석

2025년, 시약, 키트 및 소모품은 매출의 48.31%를 차지하며, 감염증 체외진단 시장에서 가장 큰 제품 카테고리가 되었습니다. 이 지위는 장비가 종종 보조금을 받는 조건으로 도입되는 반면, 장기적인 소모품 구매가 수익원이 되는 비즈니스 모델을 반영하고 있습니다. 검사실에서 카트리지나 시약의 규격을 한 번 검증해 버리면, 재검증, 재교육, 계약 변경 등이 모두 교체 비용을 증가시키기 때문에 타사 제품으로 전환하는 데 큰 부담이 따릅니다. 이러한 구조를 통해 감염증 체외진단 시장에는 일회성 자본 설비 구매보다 변동성이 적은 안정적이고 지속적인 수익 구조가 형성되어 있습니다. 장비는 여전히 두 번째 주요 범주에 속하며, 고처리량 면역분석기, PCR 시스템, MALDI-TOF 플랫폼 및 자동 시료 처리 장치가 포함됩니다. 도입된 하드웨어에 따라 해당 시설이 장기적으로 어떤 검사 항목이나 워크플로우 형식을 지원할 수 있는지가 결정되기 때문에 이러한 시스템은 여전히 검사실의 구매 결정에 영향을 미치고 있습니다.

소프트웨어 및 서비스 시장은 2031년까지 연평균 성장률(CAGR) 8.35%를 나타낼 것으로 예측되지만, 연결성과 감시 시스템 통합의 중요성이 커짐에 따라 감염증 체외진단 시장에서 더욱 전략적인 역할을 수행하게 되었습니다. 검사 기관에서는 LIS 연결 모듈, 항생제 내성 데이터 링크 및 판정 지원 서비스를 개별적으로 구매하기보다는 보다 광범위한 계약의 일부로 평가하는 경향이 강해지고 있습니다. 이러한 변화로 인해 주요 공급업체들은 초기 장비 판매 이후에도 고객 유지를 강화할 수 있는 새로운 수단을 확보하게 될 것입니다. 또한, 단일 검사 방식이 아닌 하드웨어, 분석법, 워크플로우 소프트웨어를 다층적으로 결합한 패키지를 제공할 수 있는 기업의 입지도 강화될 것입니다. 감염증 체외진단 업계에서 검사 항목의 폭넓은 다양성과 서비스 통합을 모두 달성하고 있는 공급업체는 장비 가격 경쟁이 격화될 때에도 이익률을 유지하기 쉬운 입장에 있습니다. ISO 13485 및 FDA 제조 규정에 기반한 품질 시스템 요건 역시, 공급의 연속성을 저해하지 않으면서 규정 준수 비용을 감당할 수 있는 확고한 입지를 갖춘 공급업체의 우위를 더욱 공고히 하고 있습니다.

2025년에는 검사 사업이 매출의 61.68%를 차지했으며, 집중형 검사실이 감염증 체외진단 시장의 중심적인 위치를 계속 차지했습니다. HIV 바이러스 부하 모니터링, C형 간염 유전자형 판정, 결핵의 약물 내성 프로파일링, 성매개감염(STI)의 확정 진단과 같은 고도로 복잡한 검사는 여전히 병원의 중앙 검사실이나 독립된 참조 기관에 크게 의존하고 있습니다. 이러한 시설들은 검증된 품질 관리, 전문 인력, 그리고 첨단 정보 시스템의 통합을 바탕으로 운영되고 있어 경쟁 우위를 유지하고 있습니다. 한편, 현장 진단(Point-of-Care) 검사는 2031년까지 연평균 성장률(CAGR) 9.73%를 기록하며 성장할 것으로 예상되며, 감염증 체외진단 시장에서 가장 빠르게 성장하는 검사 유형이 될 전망입니다. 이러한 수요의 변화는 중앙 검사실을 대체하기보다는 특정 이용 사례를 더 신속하고 접근하기 쉬운 의료 현장으로 전환하는 데 중점을 두고 있습니다.

2025년 『Diagnostics』지에 실린 기사에서는 AI를 활용한 현장 진단 시스템이 프로토타입 환경에서 결과가 나오기까지 걸리는 시간을 15분에서 최단 2분으로 단축했다는 사실이 소개되었습니다. 2026년 세계보건기구(WHO)가 결핵에 대한 현장 분자진단을 지지함에 따라, 유행 지역에서의 분산형 검사 도입 근거가 더욱 확대되었습니다. DiaSorin사의 CLIA 면제 대상인 LIAISON NES 플랫폼 역시 규제 측면의 진전에 힘입어, 고도로 복잡한 검사 체계 하에서 운영되지 않는 응급 진료 클리닉이나 진료소에 분자 검사를 도입할 수 있음을 보여주었습니다. 이러한 변화는 속도와 편의성을 높여주지만, 확정 진단이나 대량 검사에서 중앙 검사실의 역할을 대체하는 것은 아닙니다. 감염증 체외진단 시장에서 가장 유력한 공급업체는 연계된 검사 메뉴 전략을 통해 환자 곁에서의 검사 환경과 집중형 검사 환경 모두에 대응할 수 있는 기업입니다. 이를 통해, 현장 진단(Point-of-Care)의 성장이 검사 시장의 전체 기반을 확대하는 것이 아니라 단순히 검사실의 수익을 잠식할 위험이 완화됩니다.

2025년에는 혈액, 혈청, 혈장이 매출의 52.42%를 차지했으며, 이 검체군은 감염증 체외진단 시장 규모에서 계속해서 중심적인 위치를 차지했습니다. 이 분야가 계속해서 견조한 성장세를 보이는 이유는 혈류 감염증 진단, HIV 모니터링, 간염 혈청학적 검사, 매독 선별검사가 혈액을 검체로 사용하는 임상 경로에 깊이 뿌리내리고 있기 때문입니다. 이러한 검사 중 상당수는 필수 산전 검사, 수혈 및 시술 전 선별 검사 체계에도 포함되어 있어, 그 수요가 단기적인 예산 변동의 영향을 덜 받는 경향이 있습니다. 소변은 요로 감염증의 진단, 성매개감염(STI)의 확정 진단, 그리고 새로운 결핵 검출법을 뒷받침하고 있기 때문에 여전히 두 번째로 중요한 검체 유형으로 남아 있습니다. 이러한 검체 구성은 감염증 체외진단 시장이 여전히 확립된 임상 진료 및 표준화된 처리 절차에 부합하는 검체 유형에 의존하고 있음을 보여줍니다.

그 밖의 검체 유형은 2031년까지 연평균 성장률(CAGR) 8.98%를 나타낼 것으로 예측되며, 감염증 체외진단 시장에서 가장 빠르게 확대될 카테고리가 될 전망입니다. HPV DNA 유전자형 분석에 관한 WHO 지침에서는 적절한 선별 검사 과정에서 자가 채취를 통한 자궁경부 검체 및 가정 내 채취를 권장하고 있으며, 이에 따라 진료소 내진 모델 이외의 검사 방식이 확대되고 있습니다. 또한, bioMerieux사는 비인두, 인두 및 전비강의 면봉 검체에 대응하는 “BIOFIRE SPOTFIRE R/STplus”패널의 유효성을 검증하고 있으며, 이를 통해 환자 근처에서 호흡기 계통 검사를 받을 수 있는 접근성이 향상되고 있습니다. 유연한 검체 채취 방식은 자가 채취, 외래 진료 환경에서의 활용, 그리고 인프라가 갖춰지지 않은 환경에서의 검사 워크플로우와 높은 호환성을 갖추고 있어, 이용 범위의 확대에 기여합니다. 또한, 이를 통해 감염증 체외진단 시장공급업체들은 채혈이나 병원 내 검체 처리에 대한 의존도가 낮은 선별 검사 프로그램이나 지역 사회를 대상으로 하는 유통 채널을 타겟으로 삼을 수 있게 됩니다. 장기적으로는 검체 접수 범위가 확대됨에 따라, 특정 질환 분야의 검사 접근성과 재검사 빈도 모두 향상될 것으로 예측됩니다.

지역별 분석

2025년, 북미는 매출의 40.86%를 차지하며 감염증 체외진단 시장에서 가장 규모가 큰 지역 부문이 되었습니다. 해당 지역은 알찬 보험 급여 범위, 자동화 분자진단 시스템 도입 기반의 확대, 그리고 복잡한 검사 워크플로우에 대응할 수 있는 병원 체계와 같은 장점을 갖추고 있습니다. CMS는 2026년 통합세출법에 따라 임상검사 요금표를 개정하여, 지급 삭감을 2026년 말까지 연기하는 한편, 2027년 이후 연간 삭감률을 15%로 상한을 설정했습니다. 이 정책으로 인해, 향후 상환 압박이 계속해서 사업 전망의 일부로 남아 있기는 하지만, 검사 기관의 경우 단기적인 전망은 서 있습니다. 또한, 2026년 4월에 발효된 CMS의 MolDX 지침에 따라, 증후군에 기반한 호흡기 및 소화기 패널 검사의 청구에 관한 ICD-10 기재 요건이 강화되었습니다. 이에 따라, 고객 계정 전반에 걸쳐 확고한 임상적 근거와 엄격한 코딩 관리를 지원할 수 있는 공급업체가 유리한 입장에 서게 됩니다. 캐나다와 멕시코는 금액 기준으로는 여전히 규모가 작지만, 두 나라 모두 더 광범위한 지역의 공중보건 우선순위에 부합하는 HIV, 결핵, HPV 검사 경로를 통해 수요를 지속적으로 확대되고 있습니다.

유럽은 감염증 체외진단 시장에서 여전히 2위의 규모를 유지하고 있으며, 중앙집권화된 병원 검사실 네트워크에 대한 의존도가 높은 상황이 지속되고 있습니다. 독일, 영국, 프랑스, 이탈리아, 스페인은 확립된 병원 조달 시스템과 분자진단 및 면역 분석 검사의 임상 현장에서의 광범위한 도입을 통해 해당 지역의 체계적인 검사량의 상당 부분을 차지하고 있습니다. IVDR는 검사 포트폴리오 전반에 걸쳐 입증 책임 강화 및 재등록 요건을 부과함으로써, 해당 지역 내 제품화에 가장 큰 영향을 미치는 정책 요인으로 계속 자리 잡고 있습니다. bioMerieux사가 2026년 3월에 취득한 BIOFIRE SPOTFIRE 호흡기·인후통 검사 패널의 CE 마크는 규모가 있는 기업들이 새로운 체계 하에서 자사의 검사 메뉴의 입지를 유지·확대하기 위해 어떤 움직임을 보이고 있는지를 보여줍니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.58%를 기록하며 성장할 것으로 예상되며, 감염증 체외진단 시장에서 가장 빠르게 성장하는 지역 부문이 될 전망입니다. 이 지역은 감염증으로 인한 부담이 큰 반면, 검사 인프라 확충과 현지용 진단약에 대한 규제 절차의 성숙도가 높아지고 있습니다. 인도에서는 2024년에 26.2 라크하 건의 결핵 사례가 보고되었으며, 이에 따라 분자 결핵 검사, 약물 내성 프로파일링, 그리고 2026년 WHO 지침에 부합하는 환자 측 검사 워크플로우에 대한 수요가 계속해서 견조한 양상을 보이고 있습니다. 중국 역시 여전히 중요한 시장이며, 2025년에는 중국의 체외진단(IVD) 매출의 41.8%를 감염증 검사가 차지했습니다. 이는 일부 진료 경로에서 HIV, B형 및 C형 간염, 매독, 결핵에 대한 선별 검사가 의무화되어 있다는 점이 배경에 있습니다. 정부가 지원하는 입찰 프로그램과 병원의 디지털화에 힘입어, 2급 및 3급 도시의 병원에서는 수작업 방식에서 자동화 플랫폼으로의 전환이 진행되고 있습니다. 중동 및 아프리카에서는 GCC 국가들의 고처리량 검사 시스템에 대한 투자와 사하라 이남 아프리카 전역의 기부자 지원에 의한 검사 네트워크 사이에서 여전히 양극화가 나타나고 있습니다. 남미에서는 성매개감염증(STI), 뎅기열, 간염에 대한 선별검사가 확대되면서 계속해서 혜택을 보고 있지만, 조달 체계의 분산과 환율 변동으로 인해 설비 투자 속도는 여전히 완만한 수준에 머물고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the infectious disease in vitro diagnostics market size is projected to be USD 2.45 billion in 2025, USD 2.63 billion in 2026, and reach USD 3.87 billion by 2031, growing at a CAGR of 6.46% from 2026 to 2031.

This report is Segmented by Product (Reagents, Instruments, Software), Testing Type (Lab, POC), Sample (Blood/Serum, Urine, Other), Disease (Hepatitis, and More), Technology (Immunodiagnostics, PCR, NGS, INAAT, Other), Application (Diagnostics, Screening), End User (Diagnostic Laboratories, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Infectious Disease In Vitro Diagnostics Market Trends and Insights

Rising Burden of Respiratory and Bloodstream Infections

The infectious disease in vitro diagnostics market continues to draw its strongest base demand from the persistence of respiratory, bloodstream, urinary, and gastrointestinal infections across both hospital and community settings. The WHO GLASS 2025 report analyzed more than 23 million bacteriologically confirmed cases reported by 110 countries from 2016 through 2023, and it showed that drug-resistant pathogen proportions were stable or rising across several major infection categories. This pattern matters for the infectious disease in vitro diagnostics market because high-confirmation settings are concentrated in countries with better laboratory infrastructure, while regions with heavier disease burden still remain underdiagnosed. That gap keeps demand tied not only to immediate test volumes but also to future laboratory build-out across South Asia, sub-Saharan Africa, and parts of Latin America. Hospital-acquired infections add a second layer of demand because bloodstream infections require rapid organism identification and earlier antimicrobial selection to guide the first 48 hours of treatment. The infectious disease in vitro diagnostics market, therefore, benefits from both higher infection incidence and a widening clinical need for faster and more reliable laboratory decision support.

Shift Toward Syndromic Multiplex Testing Platforms

The infectious disease in vitro diagnostics market is seeing a clear shift toward syndromic multiplex testing as hospitals try to combine faster diagnosis with tighter use of staff and instrument time. QIAGEN received FDA clearance in March 2026 for gastrointestinal panels on the QIAstat-Dx Rise system, and the broader QIAstat-Dx platform had more than 5,200 instruments installed across over 100 countries. That installed base matters because a platform that supports respiratory, gastrointestinal, and emerging pathogen panels allows hospitals to consolidate menu purchases and commit to repeat reagent spending over multi-year periods. bioMerieux received IVDR CE marking in March 2026 for its BIOFIRE SPOTFIRE R/STplus Panel, which can detect 15 pathogens in 15 minutes at the point of care. Faster multiplex testing also supports antibiotic stewardship because clinicians can reduce broad empirical prescribing when pathogen identification arrives earlier in the care cycle. The infectious disease in vitro diagnostics market is therefore gaining from a buying logic that now links these platforms to cost control, throughput, and treatment quality rather than to test menu expansion alone.

High Cost of Molecular Platforms and Assay Consumables

The infectious disease in vitro diagnostics market still faces a major access barrier from the cost of molecular systems and the consumables needed to run them. Multiplex syndromic panels often cost 5 to 10 times more per test than single-target lateral flow formats, which keeps many primary care and community settings in lower-income regions outside the practical buyer pool. A 2026 study indexed on ScienceDirect described a portable microfluidic nucleic acid amplification system with sample-to-answer results in under 30 minutes at a per-test cost of USD 1.5. That contrast shows how far much of the infectious disease in vitro diagnostics market still is from price points that can scale across high-burden low-resource settings. When hospitals cannot afford broad panel testing, they often substitute cheaper single-target methods that can miss co-infections and weaken treatment choice. Reagent rental and volume-linked pricing help at the margin, but they have not yet solved the affordability gap that limits wider market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Decentralized and Point-of-Care Testing Networks

- Rising Adoption of Automated Molecular and Immunoassay Workflows

- Stringent Regulatory Review and Local Validation Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents, kits, and consumables held 48.31% of revenue in 2025, which made them the largest product category in the infectious disease in vitro diagnostics market. Their position reflects a business model in which instruments are frequently placed under subsidized terms while long-term consumable purchasing drives the revenue stream. Once a laboratory validates a cartridge or reagent format, the switching burden becomes high because revalidation, retraining, and contract changes all raise replacement costs. That dynamic gives the infectious disease in vitro diagnostics market a stable, recurring layer that is less volatile than one-time capital equipment purchases. Instruments remained the second major category and covered high-throughput immunoanalyzers, PCR systems, MALDI-TOF platforms, and automated sample processors. These systems still shape laboratory buying decisions because installed hardware determines which menus and workflow formats a site can support over time.

Software and services are projected to grow at a 8.35% CAGR through 2031, but they moved into a more strategic role within the infectious disease in vitro diagnostics market as a result of connectivity and surveillance integration becoming more important. Laboratories are increasingly valuing LIS connectivity modules, antimicrobial resistance data links, and interpretation support services as part of broader contracts instead of stand-alone purchases. This shift gives large suppliers another way to deepen account retention after the initial instrument sale. It also strengthens the position of companies that can offer a multi-layer package of hardware, assays, and workflow software instead of a single test format. Within the infectious disease in vitro diagnostics industry, suppliers that pair menu breadth with service integration are better placed to defend margins when instrument pricing becomes more competitive. Quality system demands under ISO 13485 and FDA manufacturing rules also reinforce the advantage of established suppliers that can absorb compliance costs without disrupting supply continuity.

Laboratory testing accounted for 61.68% of revenue in 2025, which kept centralized laboratories at the core of the infectious disease in vitro diagnostics market. High-complexity workups such as HIV viral load monitoring, hepatitis C genotyping, tuberculosis resistance profiling, and STI confirmation still rely heavily on hospital core labs and independent reference facilities. These settings retain an advantage because they operate with validated quality controls, specialist staff, and deep information system integration. At the same time, point-of-care testing is projected to grow at a 9.73% CAGR through 2031, making it the fastest-growing testing type in the infectious disease in vitro diagnostics market. The demand shift is less about replacing central labs and more about moving selected use cases into faster and more accessible care settings.

A 2025 article in Diagnostics described AI-enhanced point-of-care systems that reduced time-to-result from 15 minutes to as little as 2 minutes in prototype settings. WHO support for near-point-of-care tuberculosis molecular diagnostics in 2026 further widened the case for decentralized testing in endemic regions. DiaSorin's CLIA-waived LIAISON NES platform also showed how regulatory progress can move molecular testing into urgent care clinics and physician offices that do not operate under high-complexity laboratory structures. These changes improve speed and convenience, but they do not remove the role of central laboratories for confirmatory and high-volume testing. Within the infectious disease in vitro diagnostics market, the strongest suppliers are those that can serve both near-patient and centralized settings with connected menu strategies. This also reduces the risk that point-of-care growth simply cannibalizes laboratory revenue rather than expanding the total testing base.

Blood, serum, and plasma represented 52.42% of revenue in 2025, which kept this sample group at the center of the infectious disease in vitro diagnostics market size. The category remains strong because bloodstream infection diagnosis, HIV monitoring, hepatitis serology, and syphilis screening are deeply embedded in blood-based clinical pathways. Many of these tests also sit inside mandatory antenatal, transfusion, and pre-procedure screening frameworks, which makes demand less sensitive to short-term budget changes. Urine remained the second meaningful sample type because it supports urinary tract infection diagnosis, STI confirmation, and newer tuberculosis detection approaches. This sample mix shows that the infectious disease in vitro diagnostics market still depends on specimen types that fit established clinical practice and standardized processing routes.

Other sample types are projected to grow at a 8.98% CAGR through 2031, making them the fastest-expanding category in the infectious disease in vitro diagnostics market. WHO guidance on HPV DNA genotyping endorsed self-collected cervical samples and home collection in appropriate screening pathways, which expands testing outside the clinic visit model. bioMerieux also validated its BIOFIRE SPOTFIRE R/STplus panels for nasopharyngeal, throat, and anterior nasal swabs, which improves access in near-patient respiratory testing. Flexible sampling helps widen utilization because it aligns better with self-collection, outpatient use, and low-infrastructure testing workflows. It also allows suppliers in the infectious disease in vitro diagnostics market to target screening programs and community channels that are less dependent on phlebotomy and hospital-based specimen handling. Over time, broader specimen acceptance should support both access and repeat testing frequency in selected disease areas.

Complete Report Scope:

- By Product and Service

- Reagents, Kits, and Consumables

- Instruments

- Software and Services

- By Type of Testing

- Laboratory Testing

- Point-of-Care Testing

- By Sample Type

- Blood, Serum, and Plasma

- Urine

- Other Sample Types

- By Disease Type

- Hepatitis

- HIV

- Hospital-Acquired Infections

- Mosquito-Borne Diseases

- HPV

- Chlamydia trachomatis

- Neisseria gonorrhea

- Tuberculosis

- Influenza

- Syphilis

- Other Infectious Diseases

- By Technology

- Immunodiagnostics

- Clinical Microbiology

- Polymerase Chain Reaction

- Isothermal Nucleic Acid Amplification Technology

- DNA Sequencing and Next-Generation Sequencing

- DNA Microarray

- Other Technologies

- By Clinical Application

- Diagnostics

- Screening

- By End User

- Diagnostic Laboratories

- Hospitals and Clinics

- Academic and Research Institutions

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 40.86% of revenue in 2025, which made it the largest regional segment in the infectious disease in vitro diagnostics market. The region benefits from deep reimbursement coverage, a large installed base of automated molecular systems, and hospital structures that can absorb complex testing workflows. CMS updated the Clinical Laboratory Fee Schedule under the Consolidated Appropriations Act of 2026, delaying payment reductions through the end of 2026 and capping annual cuts at 15% starting in 2027. That policy gives laboratories near-term visibility even though future reimbursement pressure remains part of the operating outlook. CMS MolDX guidance effective April 2026 also tightened ICD-10 documentation requirements for syndromic respiratory and gastrointestinal panel claims. This favors suppliers that can support strong clinical evidence and coding discipline across customer accounts. Canada and Mexico remain smaller in value terms, but both continue to build demand through HIV, tuberculosis, and HPV testing pathways that align with broader regional public health priorities.

Europe remained the second-largest region in the infectious disease in vitro diagnostics market and continued to rely heavily on centralized hospital laboratory networks. Germany, the United Kingdom, France, Italy, and Spain anchor most of the region's structured testing volume through established hospital procurement systems and broad clinical adoption of molecular and immunoassay menus. IVDR remains the single strongest policy force shaping commercialization in the region because it raises the burden of evidence and re-registration across assay portfolios. bioMerieux's March 2026 CE marking for BIOFIRE SPOTFIRE respiratory and sore throat panels showed how companies with scale are moving to preserve and extend their menu positions under the new framework.

Asia-Pacific is projected to grow at a 9.58% CAGR through 2031, making it the fastest-growing regional segment in the infectious disease in vitro diagnostics market. The region combines a high infectious disease burden with expanding laboratory infrastructure and maturing regulatory pathways for localized diagnostics. India recorded 26.2 lakh tuberculosis cases in 2024, which keeps demand strong for molecular TB testing, drug resistance profiling, and near-patient workflows aligned with 2026 WHO guidance. China also remains important because infectious disease testing accounted for 41.8% of the country's IVD revenue in 2025, supported by mandatory screening for HIV, hepatitis B and C, syphilis, and tuberculosis in several care pathways. Government-supported tender programs and hospital digitization are helping the shift from manual methods to automated platforms in Tier-2 and Tier-3 city hospitals. The Middle East and Africa remain split between high-throughput investment in GCC states and donor-backed testing networks across sub-Saharan Africa. South America continues to gain from STI, dengue, and hepatitis screening expansion, although procurement fragmentation and currency volatility still moderate capital investment speed.

- Abbott Laboratories

- Beckton Dickinson

- Bio-Rad Laboratories

- bioMerieux

- Co-Diagnostics

- Danaher

- DiaSorin

- Roche

- Grifols

- Hologic

- Meril Life Science

- Molbio Diagnostics Limited

- Orasure Technologies

- QIAGEN

- QuidelOrtho

- SD Biosensor, Inc.

- Seegene

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

- Trinity Biotech plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Respiratory and Bloodstream Infections

- 4.2.2 Shift Toward Syndromic Multiplex Testing Platforms

- 4.2.3 Expansion of Decentralized and Point-of-Care Testing Networks

- 4.2.4 Rising Adoption of Automated Molecular and Immunoassay Workflows

- 4.2.5 Integration of AI-Enabled Interpretation and Workflow Software

- 4.2.6 Increased Hospital Preparedness for Outbreak Surveillance and AMR Monitoring

- 4.3 Market Restraints

- 4.3.1 High Cost of Molecular Platforms and Assay Consumables

- 4.3.2 Stringent Regulatory Review and Local Validation Requirements

- 4.3.3 Reimbursement Pressure on Non-Urgent and Low-Volume Testing

- 4.3.4 Skilled Labor Shortages for Complex Diagnostics and Data Interpretation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product and Service

- 5.1.1 Reagents, Kits, and Consumables

- 5.1.2 Instruments

- 5.1.3 Software and Services

- 5.2 By Type of Testing

- 5.2.1 Laboratory Testing

- 5.2.2 Point-of-Care Testing

- 5.3 By Sample Type

- 5.3.1 Blood, Serum, and Plasma

- 5.3.2 Urine

- 5.3.3 Other Sample Types

- 5.4 By Disease Type

- 5.4.1 Hepatitis

- 5.4.2 HIV

- 5.4.3 Hospital-Acquired Infections

- 5.4.4 Mosquito-Borne Diseases

- 5.4.5 HPV

- 5.4.6 Chlamydia trachomatis

- 5.4.7 Neisseria gonorrhea

- 5.4.8 Tuberculosis

- 5.4.9 Influenza

- 5.4.10 Syphilis

- 5.4.11 Other Infectious Diseases

- 5.5 By Technology

- 5.5.1 Immunodiagnostics

- 5.5.2 Clinical Microbiology

- 5.5.3 Polymerase Chain Reaction

- 5.5.4 Isothermal Nucleic Acid Amplification Technology

- 5.5.5 DNA Sequencing and Next-Generation Sequencing

- 5.5.6 DNA Microarray

- 5.5.7 Other Technologies

- 5.6 By Clinical Application

- 5.6.1 Diagnostics

- 5.6.2 Screening

- 5.7 By End User

- 5.7.1 Diagnostic Laboratories

- 5.7.2 Hospitals and Clinics

- 5.7.3 Academic and Research Institutions

- 5.7.4 Other End Users

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Spain

- 5.8.2.6 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 India

- 5.8.3.4 Australia

- 5.8.3.5 South Korea

- 5.8.3.6 Rest of Asia-Pacific

- 5.8.4 Middle East & Africa

- 5.8.4.1 GCC

- 5.8.4.2 South Africa

- 5.8.4.3 Rest of Middle East & Africa

- 5.8.5 South America

- 5.8.5.1 Brazil

- 5.8.5.2 Argentina

- 5.8.5.3 Rest of South America

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 Bio-Rad Laboratories, Inc.

- 6.3.4 bioMerieux SA

- 6.3.5 Co-Diagnostics, Inc.

- 6.3.6 Danaher Corporation

- 6.3.7 DiaSorin S.p.A.

- 6.3.8 F. Hoffmann-La Roche Ltd.

- 6.3.9 Grifols, S.A.

- 6.3.10 Hologic, Inc.

- 6.3.11 Meril Life Sciences Pvt. Ltd.

- 6.3.12 Molbio Diagnostics Limited

- 6.3.13 OraSure Technologies, Inc.

- 6.3.14 QIAGEN N.V.

- 6.3.15 QuidelOrtho Corporation

- 6.3.16 SD Biosensor, Inc.

- 6.3.17 Seegene Inc.

- 6.3.18 Siemens Healthineers AG

- 6.3.19 Sysmex Corporation

- 6.3.20 Thermo Fisher Scientific Inc.

- 6.3.21 Trinity Biotech plc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment