|

시장보고서

상품코드

2073152

초음파 흡입기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Ultrasonic Aspirator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

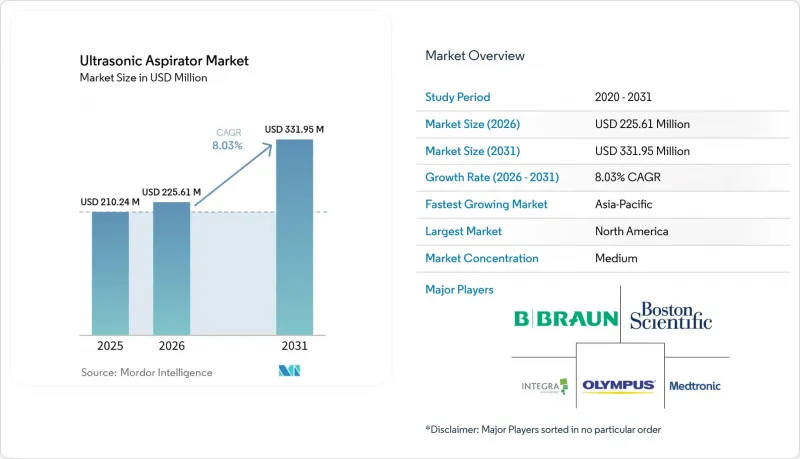

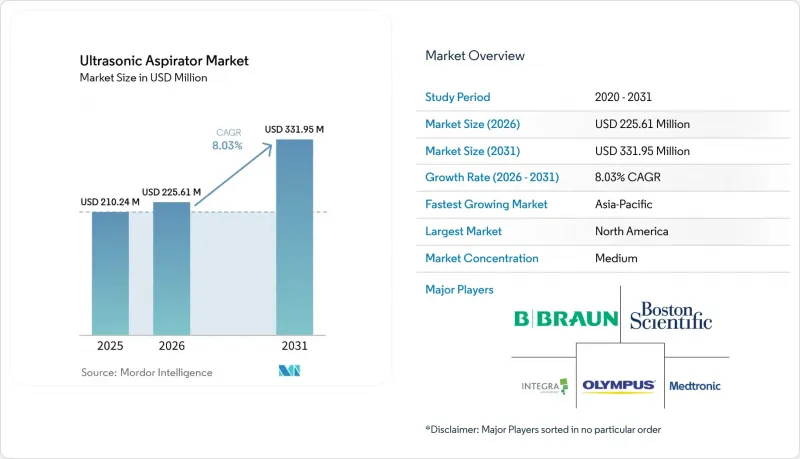

Mordor Intelligence에 의하면, 초음파 흡입기 시장 규모는 2025년에 2억 1,024만 달러로 평가되었고 2026년 2억 2,561만 달러에서 2031년까지 3억 3,195만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.03%를 나타낼 전망입니다.

본 보고서는 제품별(일체형, 독립형), 용도별(신경외과, 산부인과, 소화기, 심장, 교정외과, 뇌종양, 허혈성 뇌졸중, 외상성 뇌손상, 기타), 최종 사용자별(병원, 외래수술센터(ASC), 전문 클리닉, 기타), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 초음파 흡입기 시장 동향 및 인사이트

신경외과 및 종양외과 수술 건수 증가

초음파 흡입기 시장은 신경외과 및 종양외과 수술 건수 증가에 힘입어 계속해서 견조한 성장세를 보이고 있습니다. 이는 이 제품의 주요 이용 사례가 여전히 중요한 신경 구조 주변의 미세한 조직 제거와 관련되어 있기 때문입니다. 이러한 수요는 증가하는 질병 부담과 직접적인 관련이 있으며, 전 세계 뇌 및 중추신경계 암 유병자 수는 2021년에 975,279명에 달했고, 연령 조정 유병률은 2040년까지 10만 명당 12에서 13.5로 증가할 것으로 예측됩니다. 또한, 복잡한 종양 수술이 3차 의료기관에 집중되게 되면, 초음파 흡입기 시장도 그 혜택을 누리게 될 것입니다. 왜냐하면, 그러한 의료 기관들은 고성능 시스템을 도입하고, 훈련을 받은 팀을 유지하며, 확립된 플랫폼을 중심으로 업무 흐름을 표준화하는 경향이 강하기 때문입니다. 이러한 집중화로 인해 초음파 흡입기 시장 규모는 축소되겠지만, 보다 예측 가능한 고객 기반이 형성되어 서비스 계약, 소모품 수요 및 초기 콘솔 판매 이후의 고객 기반 확대에 대한 전망이 개선될 것입니다. 또한, 중증도가 높은 환자를 치료하는 병원은 시술과 관련하여 보다 철저한 지원과 신속한 문제 해결을 기대하는 경향이 있으므로, 공급업체 주도의 교육 및 임상 지원의 가치도 높아집니다. 그 결과, 질병 부담은 초음파 흡입기 시장의 시술 건수를 증가시킬 뿐만 아니라, 가장 중요한 구매처에서 수요에 대한 상업적 가치도 높여줍니다.

정밀성을 중시하는 저침습 수술로의 전환

초음파 흡입기 시장은 정밀성을 중시하는 저침습 수술로의 전환에 힘입어 성장하고 있습니다. 이 분야에서는 외과의사가 더 좁은 공간이나 취약한 혈관 및 신경 근처에서 선택적으로 조직을 분쇄해야 합니다. 복강경 자궁내막증 절제술에 관한 근거에 따르면, 불임 치료를 보존하는 수술에서 열 확산이 제한적인 CUSA의 안전한 사용이 보고되고 있습니다. 또한, 2025년에 실시된 또 다른 시뮬레이션 연구에서도 척수 내 종양 치료에 있어 초음파 흡입법의 안전성 프로파일이 입증되었습니다. 이 연구에서는 수술 시 온도가 조직 괴사의 임계치인 46°C보다 낮다는 사실이 밝혀졌습니다. 이는 초음파 흡입기 시장에 있어 중요한 의미를 지닙니다. 왜냐하면, 저침습 수술의 도입은 단순히 기존 수술 건수를 한 기구에서 다른 기구로 전환하는 데 그치지 않고, 정밀도나 조직 보존의 관점에서 흡입기 사용이 정당화되는 수술의 범위를 확대하기 때문입니다. 초음파 흡입기 시장은 다양한 전문 분야에 걸쳐 활용되면서 그 혜택을 누리고 있습니다. 왜냐하면 콘솔 한 대만 설치하면 뇌신경외과, 간 절제술, 산부인과 수술, 흉부외과 수술은 물론, 현재는 적절한 승인을 받은 경우 특정 심장 수술도 수행할 수 있기 때문입니다. 이러한 추세는 병원에 있어 플랫폼의 경제성을 높이고, 초음파 흡입기 시장에서 다기능 콘솔의 역할을 강화하고 있습니다.

높은 초기 투자 비용 및 수명 주기 소유 비용

높은 초기 투자 비용과 수명 주기 소유 비용은 초음파 흡입기 시장에서 여전히 가장 뚜렷한 제약 요인 중 하나입니다. 이는 총 비용이 콘솔의 기본 구매 가격을 훨씬 초과하기 때문입니다. 소유 비용에는 서비스 계약, 핸드피스 및 팁 교체, 소모품, 그리고 정식 교육이 포함되기 때문에 소규모 병원이나 특정 진료 분야에 특화된 외래 센터의 경우 경제적 판단을 내리기가 더욱 어려워집니다. 이 문제는 초음파 흡입기 시장 전체에 있어 중요한 사안이며, 그 도입은 종종 위원회의 심사에 달려 있지만, 위원회는 즉각적인 활용 가치를 입증하기 쉬운 다른 에너지 플랫폼과 흡입기를 비교하는 경향이 있기 때문입니다. 또한, 사례 수가 아직 증가 추세에 있는 판매 채널에서는 비용 압박이 더욱 두드러지게 나타납니다. 도입 초기 단계에서는 시설 측이 고정된 서비스 비용이나 연수 비용을 충분한 수의 처치에 분산시키는 데 어려움을 겪을 가능성이 있기 때문입니다. 실무적인 관점에서 볼 때, 공급업체가 유연한 자금 조달 계획, 재생 제품, 장기 보증, 또는 고객 차원의 예산 부담을 경감시켜 주는 간단한 유지비 모델을 제공함으로써 초음파 흡입기 시장은 더욱 빠르게 성장할 것입니다. 이러한 조치가 취해지지 않는다면, 임상적 수요가 존재하더라도 일부 고객은 구매 결정을 계속 미루게 될 것입니다.

부문별 분석

2025년 기준으로 통합형 시스템은 초음파 흡입기 시장 규모의 61.31%를 차지하고 있으며, 2031년까지 연평균 성장률(CAGR) 8.68%로 확대될 것으로 전망됩니다. 이러한 선도적인 입지는 전력 공급, 흡입, 세척, 핸드피스 제어를 단일 콘솔 내에 통합한 플랫폼에 대한 구매자의 선호도를 반영한 것으로, 이를 통해 호환성 관련 위험이 줄어들고 수술실 설정을 보다 예측하기 쉽게 만들어 줍니다. 인테그라사의 "CUSA Clarity"는 해당 모델의 대표적인 사례이며, 2025년 11월에 심장외과로의 적용 확대가 승인된 것은 이미 도입된 하나의 플랫폼이 시간이 지남에 따라 시술의 가치를 지속적으로 높여나갈 수 있음을 보여줍니다. 스트라이커사의 "Sonopet iQ" 또한, 이러한 통합의 방향성을 뒷받침하고 있습니다. 2025년 승인을 통해 학술 기관이나 고정밀 환경에 적합한 실시간 변조 기능과 무선 풋 컨트롤 기능이 추가되었기 때문입니다. 따라서 초음파 흡입기 시장에서는 통합형 시스템이 선호되고 있습니다. 그 이유는 콘솔 관리를 간소화할 뿐만 아니라, 다양한 전문 분야에서 활용하고, 교육을 표준화하며, 병원 전체의 서비스 지원을 위한 더 나은 기반을 구축할 수 있기 때문입니다.

초음파 흡입기 업계에서 독립형 시스템이 여전히 중요한 위치를 차지하고 있는 이유는 콘솔 전체를 교체하지 않고도 핸드피스를 업그레이드하거나 기존 인프라를 유지하고자 하는 병원 및 전문 의료 센터의 요구를 충족시키고 있기 때문입니다. 초음파 흡입기 시장의 이 분야 성장 속도는 완만하지만, 이러한 완만한 속도는 수요가 사라지고 있는 것이 아니라 장비 교체 시기에 기인한 것입니다. 북미와 유럽의 성숙한 시설에서는 여전히 구형 장비가 가동되고 있으며, 이러한 기존 장비 기반 덕분에 새로운 통합형 플랫폼으로의 즉각적인 전환이 아닌, 단계적인 업그레이드라는 실용적인 선택지가 유지되고 있습니다. 규제 체계 또한 두 제품 유형이 모두 존속하는 요인이 되고 있습니다. FDA 제품 코드 LFL 및 21 CFR Part 878에 해당하는 초음파 수술 기기는 구성과 관계없이 510(k) 절차를 통해 실질적 동등성을 입증해야 하기 때문입니다. 중기적으로는 초음파 흡입기 업계에서 통합형 시스템이 주도적인 위치를 유지하는 한편, 독립형 시스템은 규모는 작지만 여전히 견조한 교체 수요를 주축으로 한 틈새 시장을 유지해 나갈 것으로 보입니다.

지역별 분석

2025년, 북미는 초음파 흡입기 시장에서 38.16%의 점유율을 차지하며, 해당 시장에서 가장 큰 기여를 한 지역이 되었습니다. 이 지역은 학술적인 뇌신경외과 센터가 밀집해 있고, 수술 건수가 많으며, 공급업체들이 비교적 일관된 규제 논리에 따라 적응증을 확대하고 제품 기능을 개선할 수 있는 FDA 승인 절차의 혜택을 받고 있습니다. 북미의 초음파 흡입기 시장은 성숙한 도입 기반으로부터도 혜택을 받고 있습니다. 이는 신규 도입이 주춤해지더라도 구형 시스템의 교체 수요가 지속적인 설비 투자 주기를 뒷받침할 수 있기 때문입니다. 메드트로닉의 광범위한 뇌신경외과 플랫폼에서의 입지는 이미 확립된 내비게이션 및 영상 진단 고객 기반을 대상으로 흡입 기기를 교차 판매할 수 있는 실질적인 경로를 제공함으로써 이 지역에서의 입지를 더욱 공고히 하고 있습니다.

유럽은 오랜 기간 축적된 뇌신경외과 분야의 학술적 역량과 신경종양학 분야의 높은 기초 질환 부담이 맞물려, 초음파 흡입기 시장의 주요 축으로 자리매김하고 있습니다. 서유럽에서는 뇌 및 중추신경계 암의 연령 조정 발병률이 10만 명당 7.4로 세계에서 가장 높으며, 이것이 초음파 흡입 시술에 대한 꾸준한 수요를 뒷받침하고 있습니다. 독일은 수요와 의료기기 제조 역량 두 가지 측면에서 두각을 나타내고 있는 반면, 영국과 프랑스는 확고한 병원 네트워크를 갖춘 중요한 치료 거점으로 자리매김하고 있습니다. 따라서 유럽의 초음파 흡입기 시장은 조달 및 규정 준수 절차가 미국에 비해 다소 뒤처지는 경향이 있음에도 불구하고, 임상적 역량과 구조적 수요에 힘입어 성장하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.96%로 확대될 것으로 예상되며, 초음파 흡입기 시장 규모 측면에서 가장 빠르게 성장하는 지역이 될 전망입니다. 일본은 신경외과 분야의 막대한 수요 기반을 통해 시장에 기여하고 있으며, 아시아태평양의 고소득층에서는 뇌 및 중추신경계 암의 연령 조정 유병률이 10만 명당 36.4로 기록되고 있습니다. 중국은 다른 성장 양상을 보이고 있으며, 병원의 현대화와 의료기기의 현지화가 대규모 의료 네트워크 전반에 걸친 초음파 흡입기 시장의 확장을 주도하고 있습니다. 중동 및 아프리카 및 남미는 초음파 흡입기 시장에서 여전히 비교적 작은 비중을 차지하고 있으며, 이 지역의 성장은 재정적 여유가 있는 의료 시스템과 주요 도시 지역의 병원에 집중되어 있습니다. 이 지역들에는 여전히 성장 여지가 있지만, 유통업체에 대한 의존도, 교육의 제한, 승인 절차의 장기화 등이 북미, 유럽 및 선진 아시아태평양 시장과 비교했을 때 도입 속도를 늦출 가능성이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the ultrasonic aspirator market size was valued at USD 210.24 million in 2025 and is estimated to grow from USD 225.61 million in 2026 to reach USD 331.95 million by 2031, at a CAGR of 8.03% during the forecast period (2026-2031).

This report is Segmented by Product (Integrated, Standalone), Application (Neurosurgery, Gynecological, Gastrointestinal, Cardiac, Orthodontic Surgery, Brain Cancers, Ischemic Stroke, TBI, Other), End-User (Hospitals, Ascs, Specialty Clinics, Other), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Ultrasonic Aspirator Market Trends and Insights

Rising Neurological And Oncology Surgery Volumes

The ultrasonic aspirator market continues to draw durable support from rising neurological and oncology surgery volumes because the core use case remains tied to delicate tissue removal around critical neural structures. This demand is directly related to the growing disease burden, and global brain and central nervous system cancer prevalence reached 975,279 cases in 2021, with the age-standardized prevalence rate projected to increase from 12 to 13.5 per 100,000 by 2040.The ultrasonic aspirator market also benefits when complex tumor surgeries become more concentrated at tertiary centers, because those centers are more likely to purchase premium systems, maintain trained teams, and standardize workflows around established platforms. That concentration creates a smaller but more predictable customer base for the ultrasonic aspirator market, and it improves visibility for service contracts, disposable demand, and account expansion after the first console sale. It also raises the value of vendor-led training and clinical support, since hospitals that handle higher-acuity caseloads tend to expect stronger procedural coverage and faster troubleshooting. As a result, disease burden not only increases procedure counts in the ultrasonic aspirator market, but it also improves the commercial quality of demand inside the most important buying accounts.

Shift Toward Precision-Based Minimally Invasive Surgery

The ultrasonic aspirator market is also being lifted by the move toward precision-based minimally invasive surgery, where surgeons need selective tissue fragmentation in tighter spaces and near vulnerable vessels or nerves. The evidence for laparoscopic endometriosis excision, where investigators reported safe use of CUSA with limited thermal spread in fertility-preserving procedures. A separate 2025 simulation study also supported the safety profile of ultrasonic aspiration in intramedullary spinal cord tumor treatment by showing operating temperatures remained below the 46 °C tissue-necrosis threshold. That matters for the ultrasonic aspirator market because minimally invasive adoption does not simply shift existing case volume from one tool to another; it expands the number of procedures where aspirators can be justified on precision and tissue-preservation grounds. The ultrasonic aspirator market also gains from cross-specialty use, since one installed console can support neurosurgery, liver resection, gynecological surgery, thoracic surgery, and now selected cardiac procedures when the system holds the right clearances. This pattern strengthens platform economics for hospitals and reinforces the role of multifunction consoles in the ultrasonic aspirator market.

High Capital And Lifecycle Ownership Cost

High capital and lifecycle ownership costs remain one of the clearest limits on the ultrasonic aspirator market because the full expense reaches well beyond the base console purchase. The ownership includes service agreements, replacement handpieces and tips, consumables, and formal training, which makes the economic decision more difficult for smaller hospitals and focused outpatient centers. This issue matters across the ultrasonic aspirator market because adoption often depends on committee review, and committees tend to compare aspirators against other energy platforms that appear easier to justify on immediate utilization. Cost pressure is also more visible in channels where case volume is still building, since facilities may struggle to spread fixed service and training costs over enough procedures in the early years of adoption. In practical terms, the ultrasonic aspirator market expands faster when vendors offer flexible financing, refurbished platforms, longer warranties, or simpler recurring-cost models that reduce budget friction at the account level. Without that adaptation, some customers will continue to delay purchase decisions even when clinical demand is present.

Other drivers and restraints analyzed in the detailed report include:

- AI-Guided Surgical Workflow Integration

- Expansion Of Ambulatory And Day-Surgery Capacity

- Shortage Of Surgeons and or Staff Trained On Ultrasonic Tissue Fragmentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated systems held 61.31% share of the ultrasonic aspirator market size in 2025, and they are also projected to expand at an 8.68% CAGR through 2031. This leadership reflects buyer preference for consolidated platforms that combine power delivery, aspiration, irrigation, and handpiece control inside a single console, which lowers compatibility risk and makes operating room setup more predictable. Integra's CUSA Clarity is a clear example of that model, and its indication expansion into cardiac surgery in November 2025 showed how one installed platform can keep adding procedural value over time. Stryker's Sonopet iQ also supports this integrated direction, since its 2025 clearance added real-time modulation and wireless foot control features that fit academic and high-precision settings. The ultrasonic aspirator market, therefore, favors integrated systems not only because they simplify console management, but also because they create a better base for multi-specialty use, training standardization, and hospital-wide service support.

Standalone systems remain relevant in the ultrasonic aspirator industry because they serve hospitals and specialist centers that want to upgrade handpieces or preserve existing infrastructure without replacing the full console. Growth in this part of the ultrasonic aspirator market is slower, but the slower pace reflects replacement timing rather than disappearing need. Mature sites in North America and Europe still operate legacy equipment, and that installed base preserves a practical role for stepwise upgrades instead of immediate conversion to a new integrated platform. The regulatory framework also keeps both product types active, because ultrasonic surgical devices under FDA product code LFL and 21 CFR Part 878 still need to demonstrate substantial equivalence through the 510(k) route, regardless of configuration. Over the medium term, the ultrasonic aspirator industry is likely to keep integrated systems in the lead while allowing standalone systems to hold a narrower but still durable replacement-oriented niche.

Complete Report Scope:

- By Product

- Integrated

- Standalone

- By Application

- Neurosurgery

- Gynecological Surgery

- Gastrointestinal Surgery

- Cardiac Surgery

- Orthodontic Surgery

- Brain Cancers

- Ischemic Stroke

- Traumatic Brain Injury

- Other Applications

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 38.16% ultrasonic aspirator market share in 2025, which made it the largest regional contributor to the ultrasonic aspirator market. The region benefits from a dense concentration of academic neurosurgery centers, higher procedure intensity, and an FDA pathway that allows suppliers to expand indications and refresh product features with relatively consistent regulatory logic. The ultrasonic aspirator market in North America also gains from mature installed bases, because replacement demand from legacy systems can support recurring capital cycles even when first-time adoption moderates. Medtronic's broad neurosurgery platform presence strengthens this regional position further by giving the company a practical route to cross-sell aspiration tools into already established navigation and imaging accounts.

Europe remains a major pillar of the ultrasonic aspirator market because it combines long-standing academic neurosurgery capability with a high underlying disease burden in neuro-oncology. Western Europe recorded the world's highest brain and central nervous system cancer age-standardized incidence rate at 7.4 per 100,000, which supports a steady procedural need for ultrasonic aspiration. Germany stands out through both demand and device manufacturing depth, while the United Kingdom and France remain important treatment centers with established hospital networks. The ultrasonic aspirator market in Europe is therefore supported by clinical capability and structural demand, even though procurement and compliance processes can remain slower than in the United States.

Asia-Pacific is projected to expand at 9.96% CAGR through 2031, which makes it the fastest-growing regional portion of the ultrasonic aspirator market size. Japan contributes through a large neurosurgical need base, and the high-income Asia-Pacific cohort recorded a brain and central nervous system cancer age-standardized prevalence rate of 36.4 per 100,000. China adds a different growth pattern, with hospital modernization and device localization shaping how the ultrasonic aspirator market develops across large care networks. The Middle East and Africa and South America remain smaller parts of the ultrasonic aspirator market, with growth concentrated in better-funded health systems and major urban hospitals. These regions still offer room for expansion, but distributor dependence, training limitations, and longer approval pathways can slow the speed of adoption compared with North America, Europe, and advanced Asia-Pacific markets.

- B. Braun

- Biomedicon Systems India Pvt Ltd

- Bioventus Inc.

- Boston Scientific

- BOWA Medical

- Conmed

- Innosurge

- Integra LifeSciences

- Johnson & Johnson

- Karl Storz

- Medtronic

- Mectron S.p.A.

- META Dynamic, Inc.

- Nakanishi

- Olympus

- Richard Wolf

- Soring GmbH

- Stryker

- Toshbro Medicals Pvt. Ltd.

- Xcellance Medical Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Neurological and Oncology Surgery Volumes

- 4.2.2 Shift Toward Precision-Based Minimally Invasive Surgery

- 4.2.3 AI-Guided Surgical Workflow Integration

- 4.2.4 Expansion of Ambulatory and Day-Surgery Capacity

- 4.2.5 Replacement Demand From Aging Ultrasonic Surgical Installed Base

- 4.2.6 Budget Reallocation Toward High-Acuity Surgical Capital Equipment

- 4.3 Market Restraints

- 4.3.1 High Capital and Lifecycle Ownership Cost

- 4.3.2 Shortage of Surgeons and OR Staff Trained on Ultrasonic Tissue Fragmentation

- 4.3.3 Competitive Substitution From Established Energy and Suction Platforms

- 4.3.4 Lengthy Regulatory Approval and Hospital Procurement Cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Integrated

- 5.1.2 Standalone

- 5.2 By Application

- 5.2.1 Neurosurgery

- 5.2.2 Gynecological Surgery

- 5.2.3 Gastrointestinal Surgery

- 5.2.4 Cardiac Surgery

- 5.2.5 Orthodontic Surgery

- 5.2.6 Brain Cancers

- 5.2.7 Ischemic Stroke

- 5.2.8 Traumatic Brain Injury

- 5.2.9 Other Applications

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics

- 5.3.4 Other End-Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 B. Braun SE

- 6.3.2 Biomedicon Systems India Pvt Ltd

- 6.3.3 Bioventus Inc.

- 6.3.4 Boston Scientific Corporation

- 6.3.5 BOWA MEDICAL

- 6.3.6 ConMed Corporation

- 6.3.7 Innosurge

- 6.3.8 Integra LifeSciences Corporation

- 6.3.9 Johnson and Johnson Services, Inc.

- 6.3.10 KARL STORZ SE and Co. KG

- 6.3.11 Medtronic

- 6.3.12 Mectron S.p.A.

- 6.3.13 META Dynamic, Inc.

- 6.3.14 Nakanishi Inc.

- 6.3.15 Olympus Corporation

- 6.3.16 Richard Wolf GmbH

- 6.3.17 Soring GmbH

- 6.3.18 Stryker Corporation

- 6.3.19 Toshbro Medicals Pvt. Ltd.

- 6.3.20 Xcellance Medical Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment