|

시장보고서

상품코드

2073203

임상시험 매칭 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Clinical Trials Matching Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

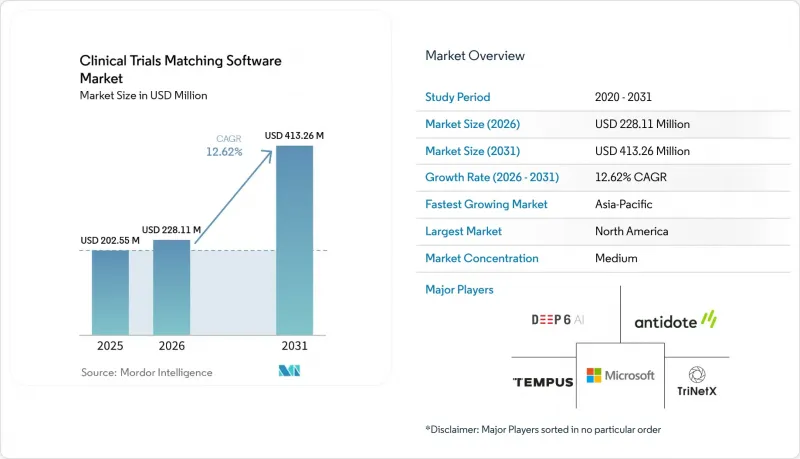

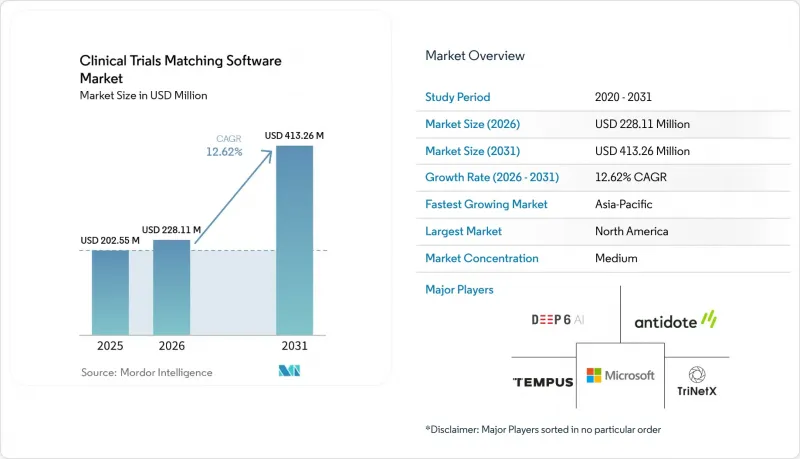

Mordor Intelligence에 의하면, 임상시험 매칭 소프트웨어 시장 규모는 2025년 2억 255만 달러, 2026년 2억 2,811만 달러에서 2031년까지 4억 1,326만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 12.62%를 나타낼 전망입니다.

본 보고서는 도입 형태(클라우드 기반, On-Premise형), 용도(피험자 모집, 실현 가능성 평가, 시험 시설 선정, 프로토콜 매칭, 피험자 참여 유도), 최종 사용자(제약·바이오기술 기업 등), 기술(인공지능 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 임상시험 매칭 소프트웨어 시장 동향 및 인사이트

EHR에서 임상시험에 이르기까지 AI 및 NLP를 활용함으로써 환자 식별에 소요되는 시간이 단축되고 있습니다.

AI를 활용한 EHR 마이닝과 NLP의 통합을 통해 임상시험 매칭 소프트웨어는 혁신을 이루고 있으며, 환자 등록 지연을 대폭 단축하고 있습니다. 환자 파일을 수동으로 확인하는 데는 11-26분이 소요되지만, AI와 NLP를 활용하면 구조화 데이터와 비구조화 데이터를 60초 이내에 분석할 수 있습니다. 2026년에 실시된 연구에서는 52명의 종양학 환자와 217건의 분자 표적이 정의된 네덜란드의 임상시험을 대상으로 TrialMatchAI의 검증이 이루어졌으며, 950쌍의 환자-기준 쌍에서 상위 20개 항목에 대한 리콜률 92.3%, 포함 정확도 88.8%, 거짓 양성률 1% 미만을 달성했습니다. 의사의 진료 기록이나 병리 기록에는 코드화된 필드보다 더 많은 자격 관련 데이터가 포함되어 있기 때문에 시장의 초점은 환자 추적 관리, 코디네이터 지원 및 환자 유지 워크플로로 점차 이동하고 있습니다. 매칭 결과를 아웃리치 도구와 통합하는 벤더는 속도와 안정성을 중시하는 임상시험 프로그램에서 경쟁 우위를 확보하고 있습니다.

정밀 종양학 및 바이오마커 기반 임상시험의 확대

정밀 종양학의 부상으로 인해, 임상시험 매칭 소프트웨어는 고도의 데이터 처리 기능으로 진화하고 있습니다. 이는 많은 종양학 연구에서 환자의 적격성을 판단하기 위해 바이오마커, 유전체, 단백체학 또는 조직학적 필터가 필요하기 때문입니다. 이러한 기준에 따라 적격 환자군이 선별되기 때문에 표준적인 진단 코드 검색의 유용성은 떨어지고 있습니다. Tempus AI가 2025년에 Deep 6 AI를 인수한 것은 바로 이러한 수요에 대응하기 위해서였습니다. Deep 6 플랫폼은 750개 이상의 의료기관과 3,000만 건의 환자 기록을 포괄하고 있어, 복잡한 임상시험의 매칭을 가능하게 합니다. 유전체 관련 데이터 세트를 보유한 업체들은 매우 복잡한 종양학 연구 분야에서 유리한 입지를 점하고 있는 반면, 기타 업체들은 뒤처져 있습니다. 후원자들이 좁게 정의된 환자 집단을 신속하게 파악하는 것을 우선시함에 따라, 이러한 격차는 더욱 확대될 것으로 예측됩니다.

분산된 의료 데이터 표준과 불완전한 EHR 아키텍처

분산된 데이터 아키텍처는 임상시험 매칭 소프트웨어 시장에서 여전히 주요 기술적 제약 요인으로 남아 있습니다. 첨단 의료 시스템조차도 다양한 공급업체, 데이터 모델, 구성을 병행하여 운영되고 있습니다. 예를 들어, 독일의 MIRACUM 네트워크는 Medizininformatik-Initiative를 통해 FHIR 기반의 피험자 모집 인프라를 개발했으나, 그럼에도 불구하고 병원 간 대규모 통합 작업이 필요했습니다. 유럽에서는 각국 고유의 데이터 소재지 관련 규제로 인해 국경을 넘는 클라우드 처리가 복잡해지고 있어, 공급업체들은 데이터를 현지에서 처리할 수밖에 없는 실정입니다. 중동 및 아프리카, 남미 일부 지역에서는 EHR 보급률이 낮아 AI를 활용한 매칭에 활용할 수 있는 데이터가 제한적이며, 스폰서 수요는 강하지만 시장 성장에는 편차가 나타나고 있습니다.

부문별 분석

2025년에는 신속한 온보딩, 여러 시설에 걸친 가시성, 실시간 피험자 등록 관리에 대한 수요가 증가함에 따라 클라우드 기반 솔루션이 임상시험 매칭 소프트웨어 시장의 68.60%를 차지했습니다. 클라우드 시스템은 로컬 인프라에 대한 요구 사항을 줄여주며, 지리적으로 분산된 테스트 팀에 통합된 대시보드를 제공합니다. 스폰서와 CRO는 여러 기관, 국가, 치료 프로그램에 걸쳐 워크플로우를 표준화하기 위해 클라우드 환경을 선호하여 도입하고 있습니다. 개인정보 보호 및 데이터 주권에 대한 우려가 커지고 있음에도 불구하고, 클라우드는 여전히 도입 환경의 기반이 되고 있습니다.

On-Premise형 도입은 2031년까지 연평균 성장률(CAGR) 14.24%를 나타낼 것으로 예측되며, 임상시험 매칭 소프트웨어 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. 이러한 성장은 일본, 독일, 중국 등 의료 데이터 처리가 엄격한 규제의 대상이 되는 국가들의 규정 준수 요건에 힘입어 이루어지고 있습니다. 각 벤더사는 병원 환경 내에서 작동하며, 외부로 전송되는 데이터를 익명화하거나 요약된 형태로만 제한하는 컨테이너화된 매칭 엔진을 개발함으로써 이 과제에 대응하고 있습니다. 업계에서는 균형 잡힌 접근 방식으로서 하이브리드 모델과 연방형 모델의 도입이 점점 더 확대되고 있습니다.

2025년에는 피험자 모집 및 사전 선별이 임상시험 매칭 소프트웨어 시장의 38.55%를 차지하고, 이는 해당 분야의 성숙도와 피험자 등록 일정에서 차지하는 중요한 역할을 반영합니다. 스폰서는 연구 비용, 마일스톤, 그리고 임상시험 기관의 생산성에 영향을 미칠 수 있는 등록 목표 미달을 방지하기 위해 이 기능을 우선시하고 있습니다. 첨단 매칭 플랫폼에서는 현재 다층적인 적격성 기준을 활용하여 선별을 진행하고 있으며, 이를 통해 피험자 모집과 사전 선별이 시장의 중심적인 위치를 계속 차지할 것이 보장되고, 구조화 데이터 및 서술형 데이터를 처리할 수 있는 도구에 대한 지속적인 투자가 정당화되고 있습니다.

임상시험 기관 선정 및 가동 준비 시장은 2031년까지 연평균 성장률(CAGR) 15.89%를 나타낼 것으로 예측되며, 임상시험 매칭 소프트웨어 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. AI를 활용한 실현 가능성 모델링은 프로토콜 수정 및 축소, 임상시험 기관의 승인률 향상 등 큰 이점을 가져다주고 있습니다. 스폰서들은 임상시험 기관 선정 과정을 강화하고, 피험자 모집 실패를 줄이며, 프로토콜 계획을 개선하기 위해 임상시험 주기의 초기 단계에서 소프트웨어를 도입하는 경향이 강해지고 있으며, 이에 따라 임상 개발 팀의 관심도 높아지고 있습니다.

지역별 분석

2025년, 북미는 임상시험 매칭 소프트웨어 시장을 독점하며 42.95%의 점유율을 차지했습니다. 이러한 우위는 해당 지역 내 전자건강기록(EHR)의 광범위한 보급, 임상시험 시설의 밀집된 분포, 그리고 구매 결정에 영향을 미치는 후원사 및 CRO의 본사가 집중되어 있는 데 기인합니다. 2024년 9월 FDA가 발표한 분산형 임상시험에 관한 지침에 따라, 개별 기관의 실질적인 피험자 모집 범위가 확대되었으며, 원격 참여에 대한 공식적인 절차가 확립되었습니다. 2025년 2월, Inovalon사는 AI를 활용한 “임상 연구 환자 찾기”를 발표했습니다. 이는 EHR과 연동되어 사전 선별 검사 및 실시간 환자 식별을 자동화합니다. 캐나다는 디지털 헬스 도입이 두드러지는 반면, 멕시코는 다양한 종양학 및 심혈관·대사 질환 임상시험 대상 집단을 타겟으로 하는 후원사들에게 여전히 중요한 시장으로 남아 있습니다.

유럽은 임상시험 매칭 소프트웨어 시장에서 2위의 규모를 자랑하며, 독일, 영국, 프랑스가 도입 및 시험 활동을 주도하고 있습니다. 해당 지역에서는 개인정보 보호 규제가 소프트웨어 아키텍처 및 조달 결정에 큰 영향을 미치고 있습니다. 각 벤더사는 각국 고유의 개인정보 보호 규정을 준수하기 위해 현지에서의 데이터 처리 및 연합형 모델을 점점 더 중요하게 여기고 있습니다. 독일의 MIRACUM 컨소시엄은 대학병원 전체를 대상으로 한 환자 모집을 위해 FHIR 표준을 준수하는 "recruIT" 인프라를 통해 이러한 추세를 구현하고 있습니다. 이 모델은 상용 벤더에 대한 기준을 높이며, 사용 편의성, 고급 분석 기능, 워크플로우의 가치 면에서 탁월함을 요구합니다. 스페인, 이탈리아 및 기타 유럽 국가들은 보다 광범위한 다국간 임상시험의 조정을 촉진하는 EU 임상시험 규정의 혜택을 누리고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.45%를 기록하며 성장할 것으로 예상되며, 임상시험 매칭 소프트웨어 시장에서 가장 두드러진 성장세를 보일 것으로 전망됩니다. 일본에서는 의약품 도입 지연을 해소하고 피험자 선별 과정을 신속하게 진행하기 위해 임상시험의 디지털화를 가속화하고 있습니다. 2025년 5월, 후지쯔는 도카이 국립 고등교육 및 연구 시스템과 제휴하여 1,800건의 환자 기록에서 얻은 비정형 임상 데이터를 90%의 정확도로 정형화하는 데 성공했으며, 이를 통해 피험자 후보 선정 시간을 3분의 1로 단축했습니다. 중국은 세계 시장 진출을 목표로 국내 플랫폼의 규모를 확대되고 있습니다. 한편, 아프리카와 남미의 신흥 시장은 규모는 작지만, Oracle이 짐바브웨, 르완다, 탄자니아 전역에서 실시하는 '아프리카 임상연구 네트워크'의 임상시험을 지원하고 있다는 점에서도 알 수 있듯이, 그 기세가 점점 더 거세지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.03According to Mordor Intelligence, the clinical trials matching software market size is projected to expand from USD 202.55 million in 2025 and USD 228.11 million in 2026 to USD 413.26 million by 2031, registering a CAGR of 12.62% between 2026 to 2031.

This report is Segmented by Deployment Mode (Cloud-Based, On-Premise), Application (Patient Recruitment, Feasibility, Site Selection, Protocol Matching, Patient Engagement), End User (Pharmaceutical and Biotechnology Companies, and More), Technology (Artificial Intelligence, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Clinical Trials Matching Software Market Trends and Insights

EHR-To-Trial AI And NLP Compressing The Patient Identification Window

AI-driven EHR mining and NLP integration are transforming clinical trial matching software by significantly reducing patient enrollment delays. Manual patient file reviews take 11 to 26 minutes, whereas AI and NLP can analyze structured and unstructured data in under 60 seconds. A 2026 study validated TrialMatchAI on 52 oncology patients and 217 molecularly defined Dutch trials, achieving a 92.3% top-20 recall rate, 88.8% inclusion accuracy, and a confabulation rate below 1% across 950 patient-criterion pairs. With more eligibility data in physician notes and pathology records than coded fields, the market focus is shifting toward patient follow-up, coordinator support, and retention workflows. Vendors integrating matching outputs with outreach tools are gaining a competitive edge in trial programs prioritizing speed and stability.

Expansion Of Precision Oncology And Biomarker-Driven Trials

The rise of precision oncology is pushing clinical trials matching software toward advanced data handling, as many oncology studies now require biomarker, genomic, proteomic, or histological filters for patient eligibility. These criteria narrow the eligible pool, reducing the utility of standard diagnosis code searches. Tempus AI's 2025 acquisition of Deep 6 AI addressed this need, with Deep 6's platform covering over 750 provider sites and 30 million patient records, enabling complex trial matching. Vendors with genomics-linked datasets are better positioned for high-complexity oncology studies, while others lag. This gap is expected to widen as sponsors prioritize faster identification of narrowly defined patient cohorts.

Fragmented Health Data Standards And Incomplete EHR Architecture

Fragmented data architecture remains a key technical limitation in the clinical trials matching software market. Even advanced health systems operate with diverse vendors, data models, and configurations. For example, Germany's MIRACUM network developed a FHIR-based recruitment infrastructure through the Medizininformatik-Initiative but still required significant integration efforts across hospitals. In Europe, country-specific data residency rules complicate cross-border cloud processing, pushing vendors toward localized data handling. In regions like the Middle East, Africa, and parts of South America, low EHR penetration limits the data available for AI-driven matching, leading to uneven market growth despite strong sponsor demand.

Other drivers and restraints analyzed in the detailed report include:

- Growth In Decentralized And Hybrid Trial Operating Models

- Rising Complexity Of Protocol Eligibility Criteria

- Clinician Trust Gaps In AI-Generated Eligibility Screening

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, cloud-based deployment held 68.60% of the clinical trials matching software market, driven by the need for faster onboarding, multi-site visibility, and real-time enrollment management. Cloud systems reduce local infrastructure requirements and provide centralized dashboards for geographically dispersed trial teams. Sponsors and CROs prefer cloud environments for standardizing workflows across multiple sites, countries, and therapeutic programs. Despite growing privacy and sovereignty concerns, cloud remains a cornerstone of the deployment landscape.

On-premise deployments are projected to grow at a 14.24% CAGR through 2031, making them the fastest-growing segment in the clinical trials matching software market. This growth is fueled by compliance requirements in countries like Japan, Germany, and China, where strict regulations govern health data processing. Vendors are addressing this by developing containerized matching engines that operate within hospital environments, sending only anonymized or summarized data externally. The industry is increasingly adopting hybrid and federated models as a balanced approach.

In 2025, patient recruitment and pre-screening accounted for 38.55% of the clinical trials matching software market, reflecting its maturity and critical role in enrollment timelines. Sponsors prioritize this function to avoid missed enrollment targets, which can impact study costs, milestones, and site productivity. Advanced matching platforms now screen using layered eligibility criteria, ensuring recruitment and pre-screening remain central to the market and justifying continued investment in tools capable of handling structured and narrative data.

Site selection and activation is projected to grow at a 15.89% CAGR through 2031, making it the fastest-growing application area in the clinical trials matching software market. AI-enhanced feasibility modeling has demonstrated significant benefits, such as reducing protocol amendments and improving site acceptance rates. Sponsors are increasingly adopting software earlier in the study cycle to enhance site selection, reduce recruitment failures, and improve protocol planning, drawing more attention from clinical development teams.

Complete Report Scope:

- By Deployment Mode

- Cloud-Based

- On-Premise

- By Application

- Patient Recruitment and Pre-Screening

- Trial Feasibility Assessment

- Site Selection and Activation

- Protocol Matching and Eligibility Screening

- Patient Engagement and Retention Support

- By End User

- Pharmaceutical and Biotechnology Companies

- Contract Research Organizations

- Medical Device Companies

- Hospitals and Health Systems

- Others

- By Technology

- Artificial Intelligence

- Machine Learning

- Natural Language Processing

- Big Data Analytics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America dominated the clinical trials matching software market, capturing 42.95% of the share. This dominance is attributed to the region's extensive EHR penetration, a high density of clinical trial sites, and the concentration of sponsor and CRO headquarters that influence purchasing decisions. The FDA's guidance in September 2024 on decentralized clinical trial elements expanded the practical enrollment radius for individual sites and formalized pathways for remote participation. In February 2025, Inovalon introduced its AI-driven Clinical Research Patient Finder, integrating with EHRs to automate pre-screening and real-time patient identification. Canada stands out for its robust digital health adoption, while Mexico remains significant for sponsors targeting diverse oncology and cardiometabolic trial populations.

Europe ranks as the second-largest player in the clinical trials matching software market, with Germany, the UK, and France leading adoption and trial activities. Privacy regulations significantly influence software architecture and procurement decisions in the region. Vendors increasingly favor local data processing and federated models to comply with country-specific privacy boundaries. Germany's MIRACUM consortium exemplifies this trend with its FHIR-compliant recruIT infrastructure for patient recruitment across university hospitals. This model raises the bar for commercial vendors, pushing them to excel in usability, advanced analytics, and workflow value. Spain, Italy, and other European nations benefit from the EU Clinical Trials Regulation, which facilitates broader multi-country trial coordination.

Asia-Pacific is projected to grow at a 15.45% CAGR through 2031, making it the fastest-growing region in the clinical trials matching software market. Japan is accelerating trial digitization to address drug lag and expedite candidate screening. Fujitsu's collaboration with Tokai National Higher Education and Research System in May 2025 structured unstructured clinical data from 1,800 patient records with 90% accuracy, reducing patient candidate selection time by a third. China is scaling domestic platforms for global registration, while emerging markets in Africa and South America, though smaller, are gaining traction, as demonstrated by Oracle's support for the Africa Clinical Research Network trial across Zimbabwe, Rwanda, and Tanzania.

- Advarra, Inc.

- Antidote Technologies, Inc.

- Aris Global

- BSI Business Systems Integration AG

- Castor EDC B.V.

- Clario

- Clinerion AG

- Deep 6 AI, Inc.

- Evidation Health, Inc.

- HealthMatch, Inc.

- IQVIA

- Medidata Solutions, Inc.

- Microsoft

- Oracle

- Reify Health, Inc.

- Teckro Limited

- Tempus AI, Inc.

- Trialbee AB

- TriNetX, LLC

- Veeva Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Complexity of Protocol Eligibility Criteria

- 4.2.2 Expansion of Precision Oncology and Biomarker-Driven Trials

- 4.2.3 Sponsor Shift Toward Faster Feasibility and Site Selection Workflows

- 4.2.4 Growth in Decentralized and Hybrid Trial Operating Models

- 4.2.5 EHR to Trial Matching Through AI and NLP Integration

- 4.2.6 Cross-Institution Patient Data Interoperability for Pre-Screening

- 4.3 Market Restraints

- 4.3.1 Fragmented Health Data Standards and Incomplete EHR Structure

- 4.3.2 Clinician Trust Gaps in AI-Generated Eligibility Matches

- 4.3.3 Limited Trial Awareness in Rare Disease and Niche Therapeutic Populations

- 4.3.4 Workflow Resistance from Sites That Lack Dedicated Research Operations Staff

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.2 By Application

- 5.2.1 Patient Recruitment and Pre-Screening

- 5.2.2 Trial Feasibility Assessment

- 5.2.3 Site Selection and Activation

- 5.2.4 Protocol Matching and Eligibility Screening

- 5.2.5 Patient Engagement and Retention Support

- 5.3 By End User

- 5.3.1 Pharmaceutical and Biotechnology Companies

- 5.3.2 Contract Research Organizations

- 5.3.3 Medical Device Companies

- 5.3.4 Hospitals and Health Systems

- 5.3.5 Others

- 5.4 By Technology

- 5.4.1 Artificial Intelligence

- 5.4.2 Machine Learning

- 5.4.3 Natural Language Processing

- 5.4.4 Big Data Analytics

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Advarra, Inc.

- 6.3.2 Antidote Technologies, Inc.

- 6.3.3 ArisGlobal LLC

- 6.3.4 BSI Business Systems Integration AG

- 6.3.5 Castor EDC B.V.

- 6.3.6 Clario

- 6.3.7 Clinerion AG

- 6.3.8 Deep 6 AI, Inc.

- 6.3.9 Evidation Health, Inc.

- 6.3.10 HealthMatch, Inc.

- 6.3.11 IQVIA Holdings Inc.

- 6.3.12 Medidata Solutions, Inc.

- 6.3.13 Microsoft Corporation

- 6.3.14 Oracle Corporation

- 6.3.15 Reify Health, Inc.

- 6.3.16 Teckro Limited

- 6.3.17 Tempus AI, Inc.

- 6.3.18 Trialbee AB

- 6.3.19 TriNetX, LLC

- 6.3.20 Veeva Systems Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment