|

시장보고서

상품코드

1562736

매출 기회의 부족과 법적 문제에도 불구하고 세계를 강타하고 있는 생성형 AI : 데이터센터의 골드 러시는 끝나는가? 이 열풍은 어디로 향하며, 데이터센터 수요는 어떻게 되는가?Will the Data Center Gold Rush Come to an End? Generative AI has Taken the World by Storm, despite the Lack of Proven Revenue Opportunities and Huge Legal Challenges, Where Does the Hype Head Next, and What Happens to Data Center Demand? |

||||||

데이터센터 수요와 특히 웹스케일 분야에서의 투자의 증가에 박차를 가하는 생성형 AI의 역할에 초점을 맞추고, 당사의 설비투자 예측의 지원 데이터를 제공합니다.

비주얼

생성형 AI는 그 모든 진화 형태가 투자 커뮤니티의 주목을 받고 있습니다. 초기 승자가 수십년간 지배할 수 있는 일생일대의 기회라는 인식이 팽배해 있습니다. 이런 일은 이전에도 다른 기술 혁신에서 일어난 적이 있으며, 대개 열광은 곧 가라앉는 경우가 많습니다. 생성형 AI는 지금 어디로 가고 있는 것일까? 생성형 AI는 거품이며, 보급을 위해 힘겨운 싸움을 벌이고 있습니다. 생성형 AI 툴은 흥미롭고 다양한 응용이 가능하지만, 심각한 법적 문제에 직면해 있으며, 킬러 앱도 없습니다.

지난 주, AI 데이터센터 및 관련 에너지 투자에 최대 1,000억 달러 규모의 자금을 조달하고 운용하는 펀드가 발표되었습니다. 이 새로운 펀드인 GAIIP(Global AI Infrastructure Investment Partnership)는 마이크로소프트와 AI 인프라에 기대를 걸고 있는 금융기관 3곳, 블랙록(BlackRock), 세계 인프라 파트너스(GIP), 아부다비에 본사를 둔 MGX(Global Infrastructure Partners)가 공동 출자한 펀드입니다.), 아부다비에 본사를 둔 MGX(MGX.)의 파트너십을 통해 탄생했습니다. 이번 제휴는 최근 수년간 발표된 수많은 사모펀드 주도의 데이터센터 투자에 추가되는 것입니다. 이러한 투자는 ChatGPT가 출시된 2022년 하반기부터 급증하고 있습니다. 디지털 인프라에 대한 자본 조달 및 투자 관리를 목적으로 하는 새로운 투자 수단은 2022년 말에서 2023년 초에 생성형 AI가 출시되기 전부터 존재해왔으며, 2024년 생성형 AI가 본격화되면서 더욱 가속화되고 있습니다.

데이터센터에 대한 지출이 급증하는 것은 새로운 뉴스가 아닙니다. 더 크고, 더 좋고, 더 많은 전력을 소비하는 새로운 데이터센터가 속속 발표되고 있습니다. 이러한 새로운 인프라에 자금을 지원하기 위해 새로운 금융 수단이 생겨나고 있습니다. 이로 인해 컴퓨터, 특히 현재 GPU 서버가 주류인 웹 스케일 데이터센터에서 널리 보급된 거대한 컴퓨터 클러스터가 실제로 얼마나 많은 전력을 소비하는지에 대한 인식이 더 널리 퍼지게 되었습니다. 2019년 이후 웹스케일 부문의 에너지 소비량은 두 배로 증가했으며, 지난 2년 동안 매년 15%씩 증가했습니다. 더 중요한 것은 코로나 이후 웹스케일 부문의 에너지 집약도가 감소하기는커녕 오히려 증가하고 있으며, 2021년에는 매출 100만 달러당 59MWh의 에너지가 소비되었고, 2022년에는 65MWh, 2023년에는 70MWh로 증가할 것으로 예상됩니다. 웹 스케일러는 그 규모를 활용하여 규모에서 효율성을 얻을 수 있으므로 주목할 만합니다. 발전 AI에 대한 큰 노력으로 에너지 집약도는 계속 증가할 것으로 보입니다. 저렴한 재생 전력에 대한 접근성 부족은 생성형 AI 시장이 직면한 많은 도전 과제 중 하나이지만, 이러한 도전에도 불구하고 데이터센터 지출은 웹스케일 시장에 힘입어 몇 분기 동안은 높은 수준을 유지할 것으로 보입니다. 이러한 새로운 AI 모델을 발전시키기 위한 경쟁은 현재 진행 중이며, 초기 승자가 수년간 우위를 점할 수 있다는 견해가 있습니다. 따라서 기술력 있는 개발자, 툴, 에너지 용량, 그리고 토지 확보에 대한 경쟁이 벌어지고 있습니다.

대상 범위

언급된 조직

|

|

목차

요약

서론

분석

- 웹스케일 설비투자는 24년 상반기에 급증하며, 생성형 AI가 호조인 전망을 촉진

- 웹 스케일러 상위 4사가 데이터센터 개발을 촉진

- 클라우드는 이제는 큰 수입원이 되고 있다.

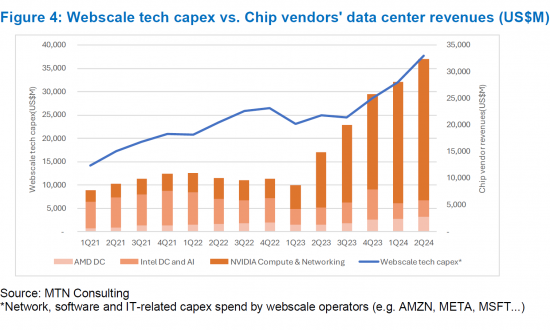

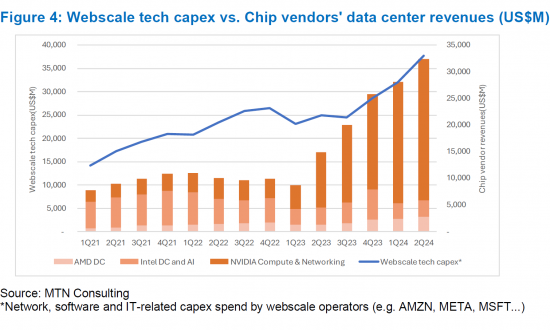

- 웹스케일 기술의 설비투자는 칩 벤더의 데이터센터 매출과 밀접하게 관계하고 있다.

- 웹스케일 시장의 에너지 소비 동향이 우려된다.

- 세계의 정치와 미중 무역 전쟁에 의한 개입

전망

부록

KSA 24.10.07This short brief is focused on data center demand and the role of generative AI in spurring an uptick in investments, particularly in the webscale sector. This brief supports our pending capex forecast update.

VISUALS

Generative AI (GenAI) in all its evolving flavors has captured the attention of the 'investment community' - there is a feeling that GenAI is a once in a lifetime opportunity where the early winners have the potential to dominate for decades. This has happened before with other technology breakthroughs and the hype usually dies down. Where is it going now? There is a strong argument that GenAI is a bubble which faces an uphill battle towards widespread adoption. The tools are interesting and do have a range of applications, but they also face serious legal challenges and lack a killer app. There's also support for the idea that the "smart money" already believes this but doesn't care, due to confidence in being able to sell others on the hype.

Last week a fund was announced to raise and manage up to $100 billion (B) in funding for AI data centers and related energy investments. The new fund, Global AI Infrastructure Investment Partnership (GAIIP), is a partnership between Microsoft and three financial institutions betting big on AI infrastructure: BlackRock, Global Infrastructure Partners (GIP), and Abu Dhabi-based MGX. The new partnership adds to a long list of private equity-driven investments in data centers announced over the last few years. These investments have spiked since late 2022, when ChatGPT was released. Even prior to GenAI rolling out in late 2022/early 2023, new investment vehicles were emerging to raise capital and manage investments in digital infrastructure. With GenAI gaining steam in 2024, that has accelerated.

It's not news that data center spending is surging thanks to widespread enthusiasm for GenAI. The announcements keep on coming: new data centers, bigger and better, consuming more power. New financial vehicles arising to fund all this new infrastructure. With this, a more widespread appreciation of how power-hungry computers actually are - especially the massive clusters of computers prevailing in webscale data centers, now dominated by GPU servers. Energy consumption has doubled in the webscale sector since 2019, growing 15% per year in each of the last two years. More important, since COVID, the webscale sector has become more energy intensive, not less; in 2021, 59 MWh of energy was consumed per US$1M in revenues. That figure grew to 65 in 2022 and 70 in 2023. This is notable, as webscalers are supposed to be able to exploit their size in order to get efficiencies from scale; it's going the opposite direction with data center power consumption. And energy intensity is likely to keep rising with big commitments to GenAI. Inadequate access to affordable, renewable power is one of many challenges faced by the GenAI market. Despite these challenges, data center spend is likely to remain elevated for a few quarters, driven by the webscale market. There is a race underway to train and evolve these new AI models. There is a feeling that the early winners will be able to preserve their advantage for many years. Hence there is a land grab underway: for skilled developers, for tools, for energy capacity, and for land.

Coverage

Organizations mentioned:

|

|

Table of Contents

Summary

Introduction

Analysis

- Webscale capex surged in 1H24 and GenAI is driving strong outlook

- Top four webscalers drive data center developments

- Cloud may have started as a side business but it's now big money

- Webscale tech capex closely tied to chip vendors' data center revenues

- Energy consumption trends in webscale market are concerning

- Global politics and the US-China trade war will intervene

Outlook

Appendix

Figures:

- Figure 1: Webscale sector capex and free cash flow margin trends through 2Q24

- Figure 2: Big data center spenders (webscale and CNNO) - annualized capex and YoY % change

- Figure 3: Cloud service revenues as a percent of total for key webscalers, 2018-24

- Figure 4: Webscale tech capex vs. Chip vendors' data center revenues (US$M)

- Figure 5: Energy intensity (MWh of energy consumption per $M in revenue)