|

시장보고서

상품코드

1849801

Fill Finish 의약품 수탁제조 시장 : 업계 동향과 세계 예측(-2035년) - Fill Finish 서비스 유형별, FDF별, API 역가별, 1차 포장 용기별, 지역별, 주요 기업Fill Finish Pharmaceutical Contract Manufacturing Market: Industry Trends and Global Forecasts, Till 2035 - Distribution by Type of Fill Finish Service Offered, FDF, API Potency, Primary Packaging Container, Geographical Regions and Leading Players |

||||||

세계의 Fill Finish 의약품 수탁제조 시장 규모는 2035년까지의 예측 기간 중 CAGR 4.8%로 확대하며, 현재 75억 달러에서 2035년까지 121억 달러로 성장할 것으로 예측됩니다.

Fill Finish 의약품 수탁제조 시장

시장 세분화에서는 시장 기회를 다음과 같은 부문으로 분류합니다.

Fill Finish 서비스 유형

- 무균 충전

- BFS(성형 동시 충전)

- 말단 멸균

FDF 유형

- 제네릭 FDF

- 오리지네이터 FDF

API 역가

- 저활성 API

- 고활성 API

1차 포장 용기 유형

- 앰플

- 카트리지

- 프리필드 시린지

- 바이알

- 기타

사업 규모

- 임상

- 상업

기업 규모

- 중소기업

- 대기업/초대기업

주요 지역

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 북아프리카

최종충전 의약품 수탁제조 시장 성장 및 동향

현재 저분자 의약품은 치료 파이프라인의 약 90%를 차지하고 있습니다. 조사에 따르면 매년 승인되는 신약의 약 60%가 저분자 의약품입니다. 이러한 추세는 효과적이고 개인화된 치료에 대한 수요 증가로 인해 이 분야가 빠르게 성장하고 있기 때문입니다. 또한 저분자는 특히 그 제조와 관련된 무균 충전-마무리 공정에서 다양한 과제를 안고 있습니다. 무균 충전-마무리 단계는 의약품 제조에서 중요한 단계입니다. 이 단계에서 무균 상태를 유지하는 것은 환자의 안전과 제품의 품질 및 유효성을 보장하기 위해 중요합니다. 또한 저분자를 사용하는 새로운 제제는 특수한 툴와 전문 지식이 필요하므로 제조 비용이 상승할 수 있습니다. 따라서 많은 제약회사들은 위탁 서비스 프로바이더에 최종 충진 업무를 아웃소싱하는 것을 선호하고 있습니다.

전문 지식과 효율적인 제조 공정의 필요성에 힘입어 파이프라인의 확대와 저분자 의약품의 복잡성 증가로 인해 제약 분야에서는 특수한 Fill Finish 제조 서비스에 대한 수요가 증가하고 있습니다.

Fill Finish 의약품 수탁제조 시장 주요 인사이트

이 보고서에서는 Fill Finish 의약품 수탁제조 시장의 현황을 살펴보고, 업계내 잠재적인 성장 기회를 파악합니다. 주요 조사 결과는 다음과 같습니다.

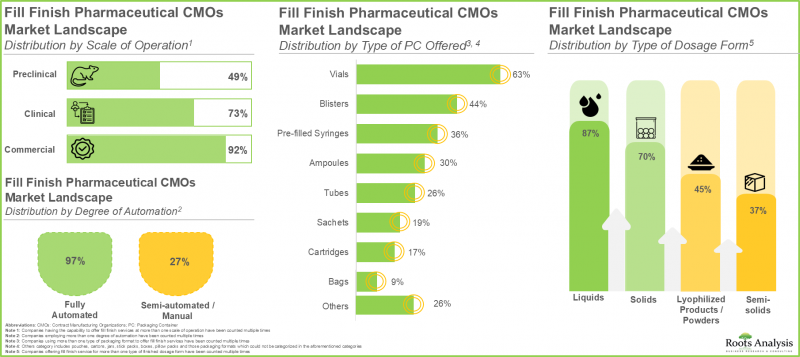

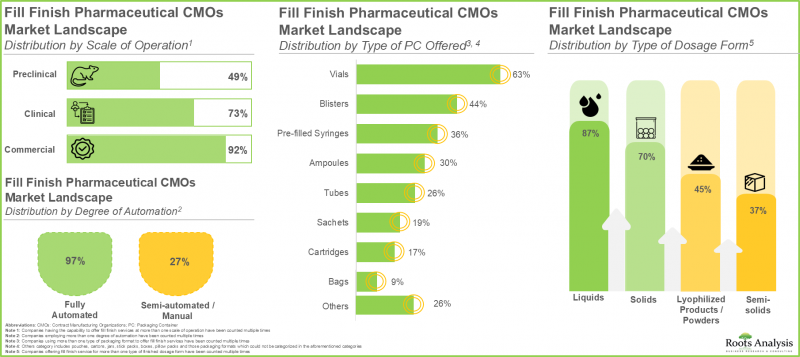

- 현재 약 390개 조직이 Fill Finish 의약품 수탁제조 서비스를 제공하고 있으며, 그 중 대부분의 수탁제조 조직이 무균 충전 서비스를 제공합니다.

- 바이알병(63%)이 가장 많이 채택된 1차 포장용기 형태로 부상하고 있습니다. 약 85%의 기업이 최종 제형으로 액체 제제를 채우는 데 필요한 역량을 보유하고 있습니다.

- 현재 최종충전제 CMO 시장 상황은 매우 파편화되어 있으며, 주요 지역별로 신규 진입기업과 기존 기업이 모두 존재하고 있습니다.

- 경쟁 우위를 확보하기 위해 업계 이해관계자들은 기존 역량을 적극적으로 업그레이드하고 새로운 역량을 추가하여 각자의 제품 포트폴리오를 강화하고 있습니다.

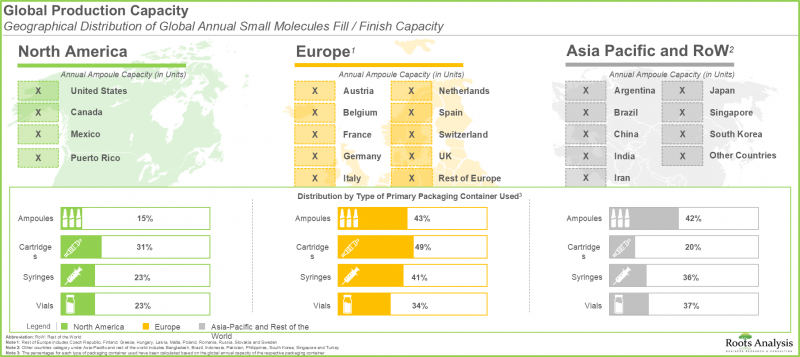

- 전 세계 의약품 Fill Finish 생산 능력은 전 세계 여러 시설에 잘 분산되어 있으며, 특히 대기업 및 초대형 기업이 총 생산 능력의 80%를 차지하고 있습니다.

- Fill Finish 의약품 수탁제조 시장은 2035년까지 안정적인 속도로 성장할 것으로 예상되며, 가까운 시일 내에 터미널 멸균이 시장의 대부분(40% 이상)을 차지할 것으로 예측됩니다.

- 장기적으로 앰플과 바이알 포장 형태가 Fill Finish 의약품 수탁제조 시장의 성장을 촉진할 것으로 보이며, 바이알 부문은 2035년까지 대부분의 점유율(50%)을 차지할 것으로 예측됩니다.

Fill Finish 의약품 수탁제조 시장 주요 부문

현재, 최종 멸균 부문이 Fill Finish 의약품 위탁 생산 시장에서 가장 큰 점유율을 차지하고 있습니다.

제공되는 Fill Finish 서비스 유형에 따라 시장은 무균 충전, BFS(성형 동시 충전), 말단 멸균으로 구분됩니다. 주목할 만한 점은 향후 10년 동안은 말단 멸균 분야가 시장을 독점할 가능성이 높다는 점입니다. 이는 말단 멸균이 무균성을 보장하고 신뢰성과 비용 효율성을 높인다는 사실에 기인합니다.

제네릭 FDF 부문이 Fill Finish 의약품 수탁제조 시장에서 가장 큰 점유율을 차지하고 있습니다.

FDF 유형별로 시장은 제네릭 FDF와 오리지널 FDF로 구분됩니다. 향후 10년간 제네릭 FDF 부문이 시장을 독점할 가능성이 높다는 점은 주목할 만합니다. 이는 경쟁력 있는 가격 책정, 비용 효율성, 수탁제조업체가 유지하는 품질 기준의 결과입니다.

현재, 저약리활성 API 부문이 Fill Finish 의약품 수탁제조 시장에서 가장 큰 점유율을 차지하고 있습니다.

API 역가별로 시장은 저역가 원약과 고역가 원약으로 구분됩니다. 수요가 높고, 제조 요건이 복잡하지 않고, 전체 제조 비용이 낮기 때문에 현재 Fill Finish 의약품 위탁 생산 시장은 저활성 API가 지배하고 있습니다.

프리필드 주사기 부문은 예측 기간 중 높은 CAGR로 성장할 것으로 예측됩니다.

1차 포장 용기 유형별로 시장은 앰플, 카트리지, 프리필드 시린지, 바이알, 기타 용기로 구분됩니다. 현재 앰플 부문이 Fill Finish 의약품 위탁 생산 시장에서 큰 비중을 차지하고 있다는 점은 주목할 만합니다.

사업 규모별로는 예측 기간 중 상업적 규모가 Fill Finish 의약품 수탁제조 시장을 독점할 가능성이 높음.

사업 규모에 따라 시장은 임상 규모와 상업 규모로 구분됩니다. 현재 상업적 규모의 저분자 Fill Finish 서비스에서 발생하는 매출이 Fill Finish 의약품 수탁제조 시장에서 가장 큰 비중을 차지하고 있다는 점은 주목할 만합니다.

대형/초대형 서비스 프로바이더가 Fill Finish 의약품 수탁제조 시장에서 가장 큰 점유율을 차지함.

기업 규모에 따라 시장은 중소기업과 대기업/초대형 기업으로 구분됩니다. 향후 10년간 대형/초대형 서비스 프로바이더가 Fill Finish 의약품 수탁제조 시장을 독점할 가능성이 높다는 점은 주목할 만합니다. 이는 이들 기업이 전문적이고 숙련된 인력, 혁신적인 충진/마무리 설비, 강력한 규제 능력을 보유하고 있기 때문입니다.

유럽이 가장 큰 시장 점유율을 차지

주요 지역별로는 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, 기타 지역으로 구분됩니다. 현재 유럽이 시장 점유율의 대부분을 차지하고 있지만, 세계 다른 지역 시장은 더 높은 CAGR로 성장할 것으로 예측됩니다.

Fill Finish 의약품 수탁제조 시장 진출기업 사례

- Alcami

- Amanta Healthcare

- Aurigene Pharmaceutical Services

- Batterjee Pharma

- Burrard Pharmaceuticals

- Curida

- Eriochem

- Fresenius Kabi

- GlaxoSmithKline

- Nextar Chempharma Solutions

- Pfizer CentreOne

- Plastikon Healthcare

- Procaps

- Recipharm

- ROMMELAG CMO

- Sharp

- Sypharma

- Teva Pharmaceuticals

- WuXi AppTec

Fill Finish 의약품 수탁제조 시장 조사 대상

- 시장 규모 및 기회 분석 : 이 보고서에서는(A) Fill Finish 서비스 유형,(B) FDF 유형,(C) API 역가,(D) 1차 포장 용기 유형,(E) 사업 규모,(F) 기업 규모,(G) 지역 등 주요 시장 부문에 초점을 맞추어 Fill Finish 의약품 수탁제조 시장(저분자)의 상세한 시장 규모를 추정하고 있습니다.

- 시장 상황: A)설립연도, B)기업 규모(직원수 기준), C)본사 소재지, D)제조시설 소재지, E)사업 규모, F)제공하는 Fill Finish 서비스 유형, G)제공하는 마무리 서비스 유형, H)포장 형태 유형, i)완제 형태 유형, J)자동화 정도 등 다양한 등 다양한 매개변수를 고려하여 Fill Finish 의약품 수탁제조에 종사하는 기업에 대한 종합적인 평가를 제공합니다.

- 경쟁 분석 : 이 보고서는 저분자 Fill Finish 의약품 수탁제조 업체(저분자)의 상세한 경쟁 분석에 초점을 맞추어 기업의 강점, 포트폴리오의 강점, 포트폴리오의 다양성 등의 요인을 검토하고 있습니다.

- 기업 개요: 북미, 유럽, 아시아태평양 및 기타 지역에 기반을 둔 주요 Fill Finish 의약품 수탁제조 업체들프로파일을 수록하고 있으며,(A) 기업 개요,(B) 재무 정보(가능한 경우),(C) 서비스 포트폴리오,(D) 최근 동향,(E) 정보에 기반한 미래 전망에 초점을 맞추었습니다. 에 초점을 맞추었습니다.

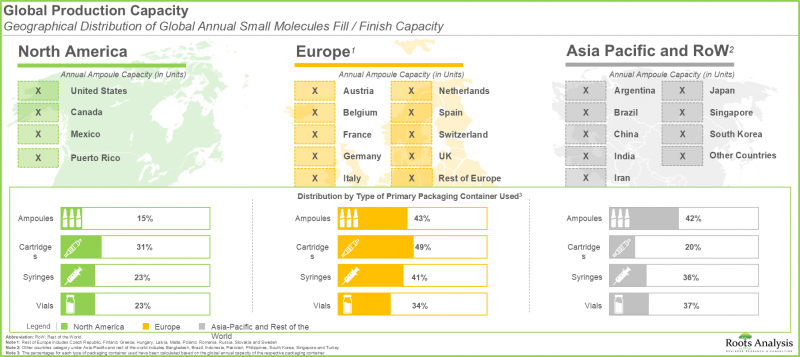

- 생산능력 분석 : 이 보고서는 세계 저분자 화합물의 연간 Fill Finish 용량 추정치를 제공합니다. 사용되는 다양한 포장 용기(앰플, 카트리지, 주사기, 바이알)의 가용 용량은(A) 기업 규모,(B) 주요 지역별로 구분되어 있습니다.

- 사례 연구 1: 이 보고서에는 무균 Fill Finish 공정에서 로봇/자동화 장비 사용의 이점에 대해 논의한 사례 연구가 수록되어 있습니다. 또한 제약 업무에 적합한 로봇을 제공하는 장비 제조업체의 리스트도 제공합니다.

- 사례 연구 2: 이 보고서에는 무균 Fill Finish 공정에서 포장 용기의 역할에 대한 사례 연구가 수록되어 있습니다. 또한 바로 사용할 수 있는 부품을 제공하는 공급업체 리스트도 제공합니다.

- 성장 촉진요인과 억제요인: 시장 성장에 영향을 미치는 촉진요인, 억제요인, 시장 성장 촉진요인, 과제 등 다양한 요인을 분석했습니다.

목차

제1장 서문

제2장 조사 방법

제3장 시장 역학

- 챕터 개요

- 예측 조사 방법

- 시장 평가 프레임워크

- 예측 툴과 테크닉

- 주요 고려사항

- 주요 시장 세분화

- 견고 품질 관리

- 제한 사항

제4장 경제적 및 기타 프로젝트 특유 고려 사항

제5장 개요

제6장 서론

- 챕터 개요

- 저분자화합물 Fill Finish 서비스의 서론

- 무균 충전

- 말단 멸균

- BFS(성형 동시 충전) 기술

- 저분자 관련 업무의 아웃소싱의 필요성

- 저분자화합물 업계에서 계약 제조업체의 역할

- Fill Finish 서비스 프로바이더 선택시 고려해야 할 중요한 점

- Fill Finish 서비스의 아웃소싱의 이점

- Fill Finish 업무의 아웃소싱의 리스크와 과제

- 향후 전망

제7장 시장 구도

- 챕터 개요

- 저분자 Fill Finish 서비스 프로바이더 : 시장 구도

제8장 기업 개요 : 북미의 서비스 프로바이더

- 챕터 개요

- 북미에 기반을 둔 저분자 Fill Finish 서비스 프로바이더

- Alcami

- Pfizer CentreOne

- Sharp Services

- 기타 기업

- Burrard Pharmaceuticals

- Plastikon Healthcare

제9장 기업 개요 : 유럽의 서비스 프로바이더

- 챕터 개요

- 유럽에 기반을 둔 저분자 Fill Finish 서비스 프로바이더

- Fresenius Kabi

- GlaxoSmithKline

- Recipharm

- 기타 기업

- Curida

- ROMMELAG CMO

제10장 기업 개요 : 아시아태평양의 서비스 프로바이더

- 챕터 개요

- 아시아태평양에 기반을 둔 저분자 Fill Finish 서비스 프로바이더

- Aurigene Pharmaceutical Services

- Sypharma

- WuXi AppTec

- 기타 기업

- Amanta Healthcare

제11장 기업 개요 : 기타 지역의 서비스 프로바이더

- 챕터 개요

- 기타 지역에 기반을 둔 저분자 Fill Finish 서비스 프로바이더

- Eriochem

- Teva Pharmaceutical Industries

- 기타 기업

- Batterjee Pharma

- Procaps

제12장 기업 경쟁력 분석

제13장 용량 분석

제14장 사례 연구 : FILL/FINISH 작업용 로봇 시스템

제15장 사례 연구 : 무균 Fill Finish용 바로 사용할 수 있는 포장 부품

제16장 시장 영향 분석 : 촉진요인, 제약 요인, 기회, 과제

제17장 세계의 Fill Finish 의약품 수탁제조 시장

제18장 Fill Finish 의약품 수탁제조 시장(제공되는 Fill Finish 서비스 유형별)

제19장 Fill Finish 의약품 수탁제조 시장(FDF 유형별)

제20장 Fill Finish 의약품 수탁제조 시장(API 효력별)

제21장 Fill Finish 의약품 수탁제조 시장(1차 포장 용기 유형별)

제22장 Fill Finish 의약품 수탁제조 시장(사업 규모별)

제23장 Fill Finish 의약품 수탁제조 시장(기업 규모별)

제24장 Fill Finish 의약품 수탁제조 시장(지역별)

제25장 Fill Finish 의약품 수탁제조 시장(주요 기업별)

제26장 결론

제27장 이그제큐티브 인사이트

제28장 부록 I : 표 데이터

제29장 부록 II : 기업 및 조직 리스트

KSA 25.11.05Fill Finish Pharmaceutical Contract Manufacturing Market: Overview

As per Roots Analysis, the global fill finish pharmaceutical contract manufacturing market is estimated to grow from USD 7.5 billion in the current year to USD 12.1 billion by 2035, at a CAGR of 4.8% during the forecast period, till 2035.

Fill Finish Pharmaceutical Contract Manufacturing Market

The market opportunity has been distributed across the following segments:

Type of Fill Finish Service Offered

- Aseptic Filling

- Blow-Fill-Seal

- Terminal Sterilization

Type of FDF

- Generic FDF

- Originator FDF

API Potency

- Low Potent API

- High Potent API

Type of Primary Packaging Container

- Ampoules

- Cartridges

- Prefilled Syringe

- Vials

- Other Containers

Scale of Operation

- Clinical

- Commercial

Company Size

- Small and Mid-sized Companies

- Large / Very Large Companies

Key Geographical Regions

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and North Africa

Fill Finish Pharmaceutical Contract Manufacturing Market: Growth and Trends

Currently, small molecule drugs constitute nearly 90% of the therapeutic pipeline. Research suggests that about 60% of the new drugs approved each year are small molecules. This trend stems from the rapid growth in this field, driven by the increasing demand for effective and personalized treatments. In addition, small molecules present various challenges, especially in the sterile fill-finish process involved in their production. The sterile fill-finish stage is a critical step in pharmaceutical manufacturing. It is important to maintain aseptic conditions during this phase for patient safety and to ensure the product's quality and effectiveness. Further, new formulations using small molecules need specialized tools and expertise, which can increase production costs. As a result, many drug developers prefer outsourcing their fill-finish operations to contract service providers.

Driven by the need for specialized knowledge and efficient production processes, the expanding pipeline and rising complexity of small molecule drugs have increased the demand for specialized fill-finish manufacturing services in the pharmaceutical sector.

Fill Finish Pharmaceutical Contract Manufacturing Market: Key Insights

The report delves into the current state of the fill finish pharmaceutical contract manufacturing market and identifies potential growth opportunities within the industry. Some key findings from the report include:

- Presently, close to 390 organizations offer fill finish pharmaceutical contract manufacturing services; of these, majority of the contract manufacturing organizations offer aseptic filling services.

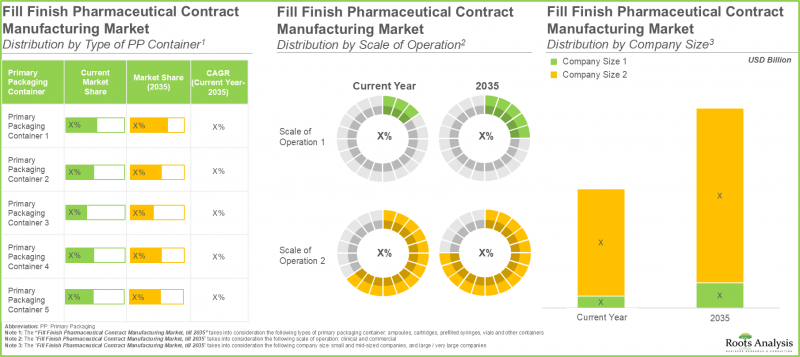

- Vials (63%) have emerged as the most adopted primary packaging container format; close to 85% of the players have the required capabilities to fill finish liquid formulations as the finished dosage form.

- The current market landscape of fill finish pharmaceutical CMOs is highly fragmented, featuring the presence of both new entrants and established players across key geographical regions.

- In pursuit of obtaining a competitive edge, industry stakeholders are actively upgrading their existing capabilities and adding new competencies in order to enhance their respective product portfolios.

- The global pharmaceutical fill finish capacity is well distributed across different facilities worldwide; notably, large and very large players account for 80% of the total capacity.

- The fill finish pharmaceutical contract manufacturing market is anticipated to grow at a steady rate, till 2035; terminal sterilization is expected to capture the majority share (over 40%) of the market in foreseeable future.

- In the long term, ampoules and vials packaging formats are likely to drive the growth of fill finish pharmaceutical contract manufacturing market; vials segment is expected to capture the majority share (~50%) by 2035.

Fill Finish Pharmaceutical Contract Manufacturing Market: Key Segments

Currently, Terminal Sterilization Segment Occupies the Largest Share of the Fill Finish Pharmaceutical Contract Manufacturing Market

Based on the type of fill finish service offered, the market is segmented into aseptic filling, blow-fill-seal and terminal sterilization. It is worth highlighting that the terminal sterilization segment is likely to dominate the market in the coming decade. This can be attributed to the fact that terminal sterilization offers sterility assurance, making it more reliable and cost-effective.

Generic FDF Segment Holds Maximum Share of the Fill Finish Pharmaceutical Contract Manufacturing Market

Based on the type of FDF, the market is segmented into generic FDF and originator FDF. It is worth highlighting that the generic FDF segment is likely to dominate the market in the coming decade. This is a result of competitive pricing, cost effectiveness and quality standards maintained by contract manufacturers.

Currently, Low Potent API Segment Occupies the Largest Share of the Fill Finish Pharmaceutical Contract Manufacturing Market

Based on the type of API by potency, the market is segmented into low potent API and high potent API. Owing to their higher demand, less complex manufacturing requirements and lower overall production costs, the current fill finish pharmaceutical contract manufacturing market is dominated by low potent API.

Prefilled Syringes Segment is Likely to Grow at a Higher CAGR During the Forecast Period

Based on the type of primary packaging container, the market is segmented into ampoules, cartridges, prefilled syringe, vials and other containers. It is worth highlighting that, at present, the ampoules segment holds the larger share of the fill finish pharmaceutical contract manufacturing market.

By Scale of Operation, Commercial Scale is Likely to Dominate the Fill Finish Pharmaceutical Contract Manufacturing Market During the Forecast Period

Based on the scale of operation, the market is segmented into clinical and commercial scale. It is worth highlighting that, at present, revenues generated from commercial scale small molecules fill finish services hold maximum share in the fill finish pharmaceutical contract manufacturing market.

Large / Very Large Service Providers Accounts for the Largest Share for the Fill Finish Pharmaceutical Contract Manufacturing Market

Based on the company size, the market is segmented into small and mid-sized companies and large / very large companies. It is worth highlighting that large / very large service providers are likely to dominate the fill finish pharmaceutical contract manufacturing market in the coming decade. This can be attributed to the fact that these companies have dedicated and skilled personnel, innovative fill / finish facilities and robust regulatory capabilities.

Europe Accounts for the Largest Share of the Market

Based on key geographical regions, the market is segmented into North America, Europe, Asia-Pacific, Latin America, Middle East and North Africa, and rest of the world. Currently, Europe captures the majority of the market share; however the market in rest of the world is expected to grow at a higher CAGR.

Example Players in the Fill Finish Pharmaceutical Contract Manufacturing Market

- Alcami

- Amanta Healthcare

- Aurigene Pharmaceutical Services

- Batterjee Pharma

- Burrard Pharmaceuticals

- Curida

- Eriochem

- Fresenius Kabi

- GlaxoSmithKline

- Nextar Chempharma Solutions

- Pfizer CentreOne

- Plastikon Healthcare

- Procaps

- Recipharm

- ROMMELAG CMO

- Sharp

- Sypharma

- Teva Pharmaceuticals

- WuXi AppTec

Fill Finish Pharmaceutical Contract Manufacturing Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features a detailed market size estimation for fill finish pharmaceutical contract manufacturing market (for small molecules), focusing on key market segments, including [A] type of fill finish service offered, [B] type of FDF, [C] API potency, [D] type of primary packaging container, [E] scale of operation, [F] company size and [G] geographical regions.

- Market Landscape: The report presents comprehensive evaluation of companies involved in fill finish pharmaceutical contract manufacturing, considering various parameters, such as [A] year of establishment, [B] company size (based on number of employees), [C] location of headquarters, [D] location of manufacturing facility, [E] scale of operation, [F] type of fill finish service offered, [G] type of finishing service offered [H] type of packaging format, [I] type of finished dosage form, [J] degree of automation.

- Company Competitiveness Analysis: The report highlights a detailed competitive analysis of fill finish pharmaceutical contract manufacturers (for small molecules), examining factors, such as company strength, portfolio strength and portfolio diversity.

- Company Profiles: The report features and in-depth profiles of key fill finish pharmaceutical contract manufacturers based in North America, Europe, Asia-Pacific and rest of the world focusing on [A] company overviews, [B] financial information (if available), [C] service portfolio, [D] recent developments and [E] an informed future outlook.

- Capacity Analysis: The report provides an estimation of global annual small molecules fill finish capacity. The available capacity for various packaging containers used (ampoules, cartridges, syringes and vials) has been segmented across [A] company size and [B] key geographical regions.

- Case Study 1: The report includes a case study discussing the advantages of using robotic / automated equipment for aseptic fill finish processes. In addition, it includes a list of equipment manufacturers providing robots suitable for pharmaceutical operations.

- Case Study 2: The report contains a case study featuring the role of ready-to-use packaging containers in aseptic fill finish operations. In addition, it provides a list of suppliers providing the ready-to-use components.

- Growth Drivers and Restraints: The report analyzes various factors such as drivers, restraints, opportunities, and challenges affecting market growth.

Key Questions Answered in this Report

- How many companies are currently engaged in this market?

- Which are the leading CMOs in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Key Market Segmentation

- 3.7. Robust Quality Control

- 3.8. Limitations

4. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.1. Time Period

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Introduction to Fill / Finish Services for Small Molecules

- 6.2.1. Aseptic Filling

- 6.2.2. Terminal Sterilization

- 6.2.3. Blow-Fill-Seal Technology

- 6.3. Need for Outsourcing Small Molecules-related Operations

- 6.4. Role of Contract Manufacturers in the Small Molecules Industry

- 6.5. Key Considerations while selecting a Fill / Finish Service Provider

- 6.6. Advantages of Outsourcing Fill / Finish Services

- 6.7. Risks and Challenges of Outsourcing Fill / Finish Operations

- 6.8. Future Perspectives

7. MARKET LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Small Molecules Fill / Finish Service Providers: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters

- 7.2.4. Analysis by Location of Fill / Finish Facilities

- 7.2.5. Analysis by Scale of Operation

- 7.2.6. Analysis by Type of Filling Service Offered

- 7.2.7. Analysis by Type of Finishing Service Offered

- 7.2.8. Analysis by Type of Packaging Format Used

- 7.2.9. Analysis by Type of Finished Dosage Form

- 7.2.10. Analysis by Degree of Automation

8. COMPANY PROFILES: SERVICE PROVIDERS IN NORTH AMERICA

- 8.1. Chapter Overview

- 8.2. Leading Small Molecules Fill / Finish Service Providers based in North America

- 8.2.1. Alcami

- 8.2.1.1. Company Overview

- 8.2.1.2. Small Molecules Fill / Finish Service Portfolio

- 8.2.1.3. Recent Developments and Future Outlook

- 8.2.2. Pfizer CentreOne

- 8.2.2.1. Company Overview

- 8.2.2.2. Small Molecules Fill / Finish Service Portfolio

- 8.2.2.3. Recent Developments and Future Outlook

- 8.2.3. Sharp Services

- 8.2.3.1. Company Overview

- 8.2.3.2. Small Molecules Fill / Finish Service Portfolio

- 8.2.3.3. Recent Developments and Future Outlook

- 8.2.1. Alcami

- 8.3. Other Leading Small Molecules Fill / Finish Service Providers based in North America

- 8.3.1. Burrard Pharmaceuticals

- 8.3.1.1. Company Overview

- 8.3.1.2. Small Molecules Fill / Finish Service Portfolio

- 8.3.2. Plastikon Healthcare

- 8.3.2.1. Company Overview

- 8.3.2.2. Small Molecules Fill / Finish Service Portfolio

- 8.3.1. Burrard Pharmaceuticals

9. COMPANY PROFILES: SERVICE PROVIDERS IN EUROPE

- 9.1. Chapter Overview

- 9.2. Leading Small Molecules Fill / Finish Service Providers based in Europe

- 9.2.1. Fresenius Kabi

- 9.2.1.1. Company Overview

- 9.2.1.2. Financial Information

- 9.2.1.3. Small Molecules Fill / Finish Service Portfolio

- 9.2.1.4. Recent Developments and Future Outlook

- 9.2.2. GlaxoSmithKline

- 9.2.2.1. Company Overview

- 9.2.2.2. Financial Information

- 9.2.2.3. Small Molecules Fill / Finish Service Portfolio

- 9.2.2.4. Recent Developments and Future Outlook

- 9.2.3. Recipharm

- 9.2.3.1. Company Overview

- 9.2.3.2. Small Molecules Fill / Finish Service Portfolio

- 9.2.3.3. Recent Developments and Future Outlook

- 9.2.1. Fresenius Kabi

- 9.3. Other Leading Small Molecules Fill / Finish Service Providers based in Europe

- 9.3.1. Curida

- 9.3.1.1. Company Overview

- 9.3.1.2. Small Molecules Fill / Finish Service Portfolio

- 9.3.2. ROMMELAG CMO

- 9.3.2.1. Company Overview

- 9.3.2.2. Small Molecules Fill / Finish Service Portfolio

- 9.3.1. Curida

10. COMPANY PROFILES: SERVICE PROVIDERS IN ASIA-PACIFIC

- 10.1. Chapter Overview

- 10.2. Leading Small Molecules Fill / Finish Service Providers based in Asia-Pacific

- 10.2.1. Aurigene Pharmaceutical Services

- 10.2.1.1. Company Overview

- 10.2.1.2. Small Molecules Fill / Finish Service Portfolio

- 10.2.1.3. Recent Developments and Future Outlook

- 10.2.2. Sypharma

- 10.2.2.1. Company Overview

- 10.2.2.2. Small Molecules Fill / Finish Service Portfolio

- 10.2.2.3. Recent Developments and Future Outlook

- 10.2.3. WuXi AppTec

- 10.2.3.1. Company Overview

- 10.2.3.2. Small Molecules Fill / Finish Service Portfolio

- 10.2.3.3. Recent Developments and Future Outlook

- 10.2.1. Aurigene Pharmaceutical Services

- 10.3. Other Small Molecules Fill / Finish Service Providers based in Asia-Pacific

- 10.3.1. Amanta Healthcare

- 10.3.1.1. Company Overview

- 10.3.1.2. Small Molecules Fill / Finish Service Portfolio

- 10.3.1. Amanta Healthcare

11. COMPANY PROFILES: SERVICE PROVIDERS IN REST OF THE WORLD

- 11.1. Chapter Overview

- 11.2. Leading Small Molecules Fill / Finish Service Providers based in Rest of the World

- 11.2.1. Eriochem

- 11.2.1.1. Company Overview

- 11.2.1.2. Small Molecules Fill / Finish Service Portfolio

- 11.2.1.3. Recent Developments and Future Outlook

- 11.2.2. Teva Pharmaceutical Industries

- 11.2.2.1. Company Overview

- 11.2.2.2. Small Molecules Fill / Finish Service Portfolio

- 11.2.2.3. Recent Developments and Future Outlook

- 11.2.1. Eriochem

- 11.3. Other Small Molecules Fill / Finish Service Providers based in Rest of the World

- 11.3.1. Batterjee Pharma

- 11.3.1.1. Company Overview

- 11.3.1.2. Small Molecules Fill / Finish Service Portfolio

- 11.3.2. Procaps

- 11.3.2.1. Company Overview

- 11.3.2.2. Small Molecules Fill / Finish Service Portfolio

- 11.3.1. Batterjee Pharma

12. COMPANY COMPETITIVENESS ANALYSIS

- 12.1. Chapter Overview

- 12.2. Assumptions and Key Parameters

- 12.3. Methodology

- 12.4. Small Molecules Fill / Finish Service Providers based in North America

- 12.5. Small Molecules Fill / Finish Service Providers based in Europe

- 12.6. Small Molecules Fill / Finish Service Providers based in Asia-Pacific and Rest of the World

13. CAPACITY ANALYSIS

- 13.1. Chapter Overview

- 13.2. Global Annual Small Molecules Fill / Finish Capacity for Ampoules (Number of Units)

- 13.2.1. Key Assumptions and Methodology

- 13.2.2. Analysis by Company Size

- 13.2.3. Analysis by Geography

- 13.2.3.1. Analysis of Small Molecules Fill / Finish Capacity for Ampoules in North America

- 13.2.3.2. Analysis of Small Molecules Fill / Finish Capacity for Ampoules in Europe

- 13.2.3.3. Analysis of Small Molecules Fill / Finish Capacity for Ampoules in Asia-Pacific and Rest of the World

- 13.3. Global Annual Small Molecules Fill / Finish Capacity for Cartridges (Number of Units)

- 13.3.1. Key Assumptions and Methodology

- 13.3.2. Analysis by Company Size

- 13.3.3. Analysis by Geography

- 13.3.3.1. Analysis of Small Molecules Fill / Finish Capacity for Cartridges in North America

- 13.3.3.2. Analysis of Small Molecules Fill / Finish Capacity for Cartridges in Europe

- 13.3.3.3. Analysis of Small Molecules Fill / Finish Capacity for Cartridges in Asia-Pacific and Rest of the World

- 13.4. Global Annual Small Molecules Fill / Finish Capacity for Prefilled Syringes (Number of Units)

- 13.4.1. Key Assumptions and Methodology

- 13.4.2. Analysis by Company Size

- 13.4.3. Analysis by Geography

- 13.4.3.1. Analysis of Small Molecules Fill / Finish Capacity for Prefilled Syringes in North America

- 13.4.3.2. Analysis of Small Molecules Fill / Finish Capacity for Prefilled Syringes in Europe

- 13.4.3.3. Analysis of Small Molecules Fill / Finish Capacity for Prefilled Syringes in Asia-Pacific and Rest of the World

- 13.5. Global Annual Small Molecules Fill / Finish Capacity for Vials (Number of Units)

- 13.5.1. Key Assumptions and Methodology

- 13.5.2. Analysis by Company Size

- 13.5.3. Analysis by Geography

- 13.5.3.1. Analysis of Small Molecules Fill / Finish Capacity for Vials in North America

- 13.5.3.2. Analysis of Small Molecules Fill / Finish Capacity for Vials in Europe

- 13.5.3.3. Analysis of Small Molecules Fill / Finish Capacity for Vials in Asia-Pacific and Rest of the World

14. CASE STUDY: ROBOTIC SYSTEMS IN FILL / FINISH OPERATIONS

- 14.1. Chapter Overview

- 14.2. Role of Robotic Systems in Fill / Finish Operations

- 14.2.1. Types of Robots Used

- 14.2.2. Key Considerations for Selecting Robotic Systems

- 14.3. Companies Providing Robots for use in the Pharmaceutical Industry

- 14.4. Companies Providing Isolator- based Aseptic Filling Systems

- 14.5. Small Molecules Fill / Finish Service Providers: List of Equipment Used

- 14.6. Concluding Remarks

15. CASE STUDY: READY-TO-USE PACKAGING COMPONENTS FOR ASEPTIC FILL / FINISH

- 15.1. Chapter Overview

- 15.2. Role of Ready-to-Use Packaging Components in Aseptic Fill / Finish Operations

- 15.2.1. Advantages of Ready-to-Use Packaging Components

- 15.2.2. Disadvantages of Ready-to-Use Packaging Components

- 15.3. Companies Providing Ready-to-Use Packaging Components

- 15.4. Concluding Remarks

16. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 16.1. Chapter Overview

- 16.2. Market Drivers

- 16.3. Market Restraints

- 16.4. Market Opportunities

- 16.5. Market Challenges

- 16.6. Conclusion

17. GLOBAL PHARMACEUTICAL FILL / FINISH MANUFACTURING MARKET

- 17.1. Chapter Overview

- 17.2. Assumptions and Methodology

- 17.3. Global Pharmaceutical Fill / Finish Manufacturing Market, till 2035

- 17.3.1. Scenario Analysis

- 17.3.1.1. Conservative Scenario

- 17.3.1.2. Optimistic Scenario

- 17.3.1. Scenario Analysis

- 17.4. Key Market Segmentations

18. PHARMACEUTICAL FILL / FINISH MANUFACTURING MARKET, BY TYPE OF FILL / FINISH SERVICE OFFERED

- 18.1. Chapter Overview

- 18.2. Assumptions and Methodology

- 18.3. Pharmaceutical Fill / Finish Manufacturing Market: Distribution by Type of Fill / Finish Service Offered, 2019, Current Year and 2035

- 18.3.1. Pharmaceutical Fill / Finish Manufacturing Market for Terminal Sterilization, till 2035

- 18.3.2. Pharmaceutical Fill / Finish Manufacturing Market for Aseptic Filling, till 2035

- 18.3.3. Pharmaceutical Fill / Finish Manufacturing Market for Blow-Fill-Seal, till 2035

- 18.4. Pharmaceutical Fill / Finish Manufacturing Market, by Type of Fill / Finish Services Offered: Market Dynamics Assessment

- 18.4.1. Penetration-Growth (P-G) Matrix

- 18.4.2. Data Triangulation and Validation

19. PHARMACEUTICAL FILL / FINISH MANUFACTURING MARKET, BY TYPE OF FDF

- 19.1. Chapter Overview

- 19.2. Assumptions and Methodology

- 19.3. Pharmaceutical Fill / Finish Manufacturing Market: Distribution by Type of FDF, 2019, Current Year and 2035

- 19.3.1. Pharmaceutical Fill / Finish Manufacturing Market for Generic FDF, till 2035

- 19.3.2. Pharmaceutical Fill / Finish Manufacturing Market for Originator FDF, till 2035

- 19.4. Pharmaceutical Fill / Finish Manufacturing Market, by Type of FDF: Market Dynamics Assessment

- 19.4.1. Penetration-Growth (P-G) Matrix

- 19.4.2. Data Triangulation and Validation

20. PHARMACEUTICAL FILL / FINISH MANUFACTURING MARKET, BY API POTENCY

- 20.1. Chapter Overview

- 20.2. Assumptions and Methodology

- 20.3. Pharmaceutical Fill / Finish Manufacturing Market: Distribution by API Potency, 2019, Current Year and 2035

- 20.3.1. Pharmaceutical Fill / Finish Manufacturing Market for Low Potent API, till 2035

- 20.3.2. Pharmaceutical Fill / Finish Manufacturing Market for High Potent API, till 2035

- 20.4. Pharmaceutical Fill / Finish Manufacturing Market, by API Potency: Market Dynamics Assessment

- 20.4.1. Penetration-Growth (P-G) Matrix

- 20.4.2. Data Triangulation and Validation

21. PHARMACEUTICAL FILL / FINISH MANUFACTURING MARKET, BY TYPE OF PRIMARY PACKAGING CONTAINER

- 21.1. Chapter Overview

- 21.2. Assumptions and Methodology

- 21.3. Pharmaceutical Fill / Finish Manufacturing Market: Distribution by Type of Primary Packaging Container, 2019, Current Year and 2035

- 21.3.1. Pharmaceutical Fill / Finish Manufacturing Market for Vials, till 2035

- 21.3.2. Pharmaceutical Fill / Finish Manufacturing Market for Ampoules, till 2035

- 21.3.3. Pharmaceutical Fill / Finish Manufacturing Market for Prefilled Syringes, till 2035

- 21.3.4. Pharmaceutical Fill / Finish Manufacturing Market for Cartridges, till 2035

- 21.3.5. Pharmaceutical Fill / Finish Manufacturing Market for Other Containers, till 2035

- 21.4. Pharmaceutical Fill / Finish Manufacturing Market, by Type of Primary Packaging Container: Market Dynamics Assessment

- 21.4.1. Penetration-Growth (P-G) Matrix

- 21.4.2. Data Triangulation and Validation

22. PHARMACEUTICAL FILL / FINISH MANUFACTURING MARKET, BY SCALE OF OPERATION

- 22.1. Chapter Overview

- 22.2. Assumptions and Methodology

- 22.3. Pharmaceutical Fill / Finish Manufacturing Market: Distribution by Scale of Operation, 2019, Current Year and 2035

- 22.3.1. Pharmaceutical Fill / Finish Manufacturing Market for Clinical Scale, till 2035

- 22.3.2. Pharmaceutical Fill / Finish Manufacturing Market for Commercial Scale, till 2035

- 22.4. Pharmaceutical Fill / Finish Manufacturing Market, by Scale of Operation: Market Dynamics Assessment

- 22.4.1. Penetration-Growth (P-G) Matrix

- 22.4.2. Data Triangulation and Validation

23. PHARMACEUTICAL FILL / FINISH MANUFACTURING MARKET, BY COMPANY SIZE

- 23.1. Chapter Overview

- 23.2. Assumptions and Methodology

- 23.3. Pharmaceutical Fill / Finish Manufacturing Market: Distribution by Company Size, 2019, Current Year and 2035

- 23.3.1. Pharmaceutical Fill / Finish Manufacturing Market for Small and Mid-sized Companies, till 2035

- 23.3.2. Pharmaceutical Fill / Finish Manufacturing Market for Large / Very Large Companies, till 2035

- 23.4. Pharmaceutical Fill / Finish Manufacturing Market, by Company Size: Market Dynamics Assessment

- 23.4.1. Penetration-Growth (P-G) Matrix

- 23.4.2. Data Triangulation and Validation

24. PHARMACEUTICAL FILL / FINISH MANUFACTURING MARKET, BY GEOGRAPHICAL REGIONS

- 24.1. Chapter Overview

- 24.2. Assumptions and Methodology

- 24.3. Pharmaceutical Fill / Finish Manufacturing Market: Distribution by Geographical Regions, 2019, Current Year and 2035

- 24.3.1. Pharmaceutical Fill / Finish Manufacturing Market in North America, till 2035

- 24.3.1.1. Pharmaceutical Fill / Finish Manufacturing Market in the US, till 2035

- 24.3.1.2. Pharmaceutical Fill / Finish Manufacturing Market in Canada, till 2035

- 24.3.1.3. Pharmaceutical Fill / Finish Manufacturing Market in Mexico, till 2035

- 24.3.1.4. Pharmaceutical Fill / Finish Manufacturing Market in Puerto Rico, till 2035

- 24.3.2. Pharmaceutical Fill / Finish Manufacturing Market in Europe, till 2035

- 24.3.2.1. Pharmaceutical Fill / Finish Manufacturing Market in France, till 2035

- 24.3.2.2. Pharmaceutical Fill / Finish Manufacturing Market in Germany, till 2035

- 24.3.2.3. Pharmaceutical Fill / Finish Manufacturing Market in Italy, till 2035

- 24.3.2.4. Pharmaceutical Fill / Finish Manufacturing Market in the UK, till 2035

- 24.3.2.5. Pharmaceutical Fill / Finish Manufacturing Market in Spain, till 2035

- 24.3.2.6. Pharmaceutical Fill / Finish Manufacturing Market in Rest of Europe, till 2035

- 24.3.3. Pharmaceutical Fill / Finish Manufacturing Market in Asia-Pacific, till 2035

- 24.3.3.1. Pharmaceutical Fill / Finish Manufacturing Market in India, till 2035

- 24.3.3.2. Pharmaceutical Fill / Finish Manufacturing Market in Japan, till 2035

- 24.3.3.3. Pharmaceutical Fill / Finish Manufacturing Market in China, till 2035

- 24.3.3.4. Pharmaceutical Fill / Finish Manufacturing Market in Rest of Asia-Pacific, till 2035

- 24.3.4. Pharmaceutical Fill / Finish Manufacturing Market in Middle East and North Africa, till 2035

- 24.3.5. Pharmaceutical Fill / Finish Manufacturing Market in Latin America, till 2035

- 24.3.6. Pharmaceutical Fill / Finish Manufacturing Market in Rest of the World, till 2035

- 24.3.1. Pharmaceutical Fill / Finish Manufacturing Market in North America, till 2035

- 24.4. Pharmaceutical Fill / Finish Manufacturing Market, by Geographical Regions: Market Dynamics Assessment

- 24.4.1. Penetration-Growth (P-G) Matrix

- 24.4.2. Data Triangulation and Validation

25. PHARMACEUTICAL FILL / FINISH MANUFACTURING MARKET, BY LEADING PLAYERS

- 25.1. Chapter Overview

- 25.2. Leading Industry Players

26. CONCLUSION

27. EXECUTIVE INSIGHT

- 27.1. Chapter Overview

- 27.2. Company A

- 27.2.1. Company Snapshot

- 27.2.2. Interview Transcript: Senior Executive Director, Global Sales and Marketing