|

시장보고서

상품코드

1958587

웨어러블 인젝터 시장(제8판) : 디바이스 유형별, 자동화 레벨별, 사용법별, 치료 영역별, 지역별 - 동향과 예측(-2035년)Wearable Injectors Market (8th Edition): Distribution by Type of Device, Degree of Automation, Usability, Therapeutic Area, and Geographical Regions - Trends and Forecast Till 2035 |

||||||

웨어러블 인젝터 시장 - 개요

세계 웨어러블 인젝터 시장 규모는 현재 68억 달러에서 2035년까지 130억 달러로 성장할 것으로 예상되며, 예측 기간(-2035년) 중 7.4%의 연평균 복합 성장률(CAGR)을 보일 것으로 추정됩니다.

웨어러블 인젝터 시장 - 성장 및 동향

자가면역질환, 심장질환, 암 환자 증가는 인구 증가와 고령화에 따라 의료시스템에 지속적인 부담을 주고 있습니다. 이에 따라 제약사들은 첨단 약물전달 기술을 통해 치료 순응도와 치료 결과를 향상시키는 환자 중심의 솔루션을 개발하고 있습니다. 신체 부착형 패치 펌프와 같은 웨어러블 인젝터는 대용량의 생물제제를 지속적 기초 투여, 볼러스 투여 또는 지속적 투여로 공급하여 투여를 용이하게 하고 순응도를 향상시킵니다. 통합된 안전 기능을 통해 바늘에 찔리는 사고를 최소화하고, 가정에서 사용시 편안함과 안정성을 보장합니다. 이러한 추세를 보여주는 사례로, BD는 최근 복잡한 생물제제의 피하 투여를 목적으로 하는 BD Libertas 웨어러블 인젝터를 이용한 복합 제품의 첫 번째 제약사 주도 임상시험 개시를 발표했습니다. 이는 재택치료에서 이러한 대용량, 환자 친화적인 시스템에 대한 신뢰가 높아지고 있음을 강조하는 것입니다.

이러한 발전으로 재택치료 환경에서 피하 투여의 수단으로 웨어러블 디바이스가 최적의 선택으로 떠오르고 있습니다. 또한 웨어러블 인젝터의 보급과 함께 제약회사와 의료기기 제조업체는 제품 라인에 첨단 기능을 통합하기 시작했습니다. 여기에는 인공지능 알고리즘, 지능형 건강 모니터링 기능을 갖춘 모바일 애플리케이션, 알림, 약물 투여 확인을 위한 시각적 또는 청각적 알림 등이 포함됩니다. 이 분야는 지속적인 발전을 거듭하고 있으며, 이러한 웨어러블 인젝터의 사용이 크게 증가하여 가까운 미래에 시장 확대를 촉진할 것으로 예측됩니다.

성장 요인: 시장 확대의 전략적 원동력

웨어러블 인젝터 시장 시장 성장 촉진요인으로는 당뇨병, 종양학, 자가면역질환 등 만성질환의 유병률 증가를 들 수 있습니다. 이는 생물제제 및 고용량 요법의 피하 투여 편의성에 대한 수요를 촉진하고 있습니다. 또한 재택의료의 보급으로 자가 투약이 가능해져 병원 방문 횟수가 줄어들고 환자의 자율성과 복약 순응도가 향상되고 있는 점도 시장 성장을 촉진하고 있습니다. 소형화, 실시간 모니터링을 위한 무선 연결, 디지털 헬스 플랫폼과의 통합과 같은 기술 발전은 시장 보급을 더욱 가속화하고 있습니다.

시장 과제: 발전을 가로막는 심각한 장벽들

웨어러블 인젝터의 보급을 가로막는 주요 이슈는 개발 및 생산 비용의 상승, 특히 상환 인프라가 취약한 신흥 시장에서의 개발 및 생산 비용 상승을 들 수 있습니다. 또한 엄격한 규제 요건으로 인해 이러한 장치의 승인이 지연되어 제조업체의 컴플라이언스 부담이 가중되고 있습니다. 기기 사용에 대한 교육 부족, 안전 및 편의성에 대한 우려와 같은 환자 관련 장벽도 기존 투여 방식과의 경쟁과 함께 보급에 걸림돌로 작용하고 있습니다.

웨어러블 인젝터 시장 - 주요 인사이트

이 보고서는 웨어러블 인젝터 시장의 현황을 상세하게 분석하고 업계의 잠재적인 성장 기회를 파악합니다. 주요 조사 결과는 다음과 같습니다.

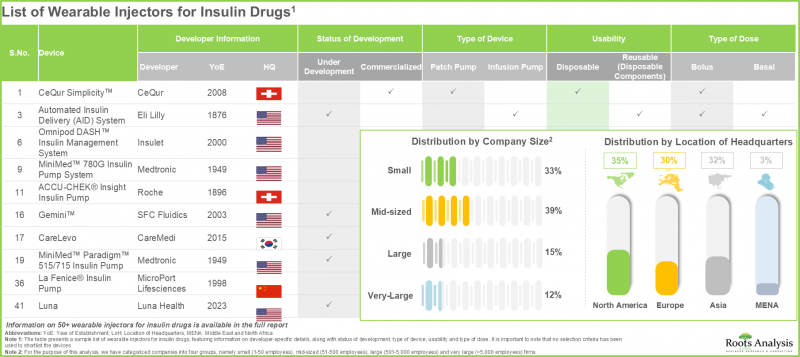

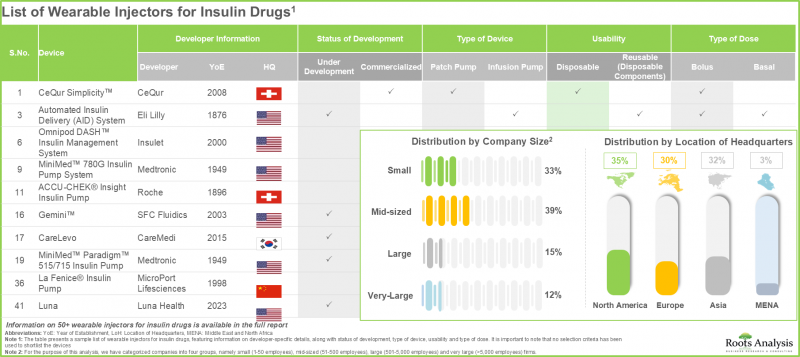

- 현재 시장 상황에서는 인슐린 약품용 웨어러블 인젝터가 50여 종 이상 존재합니다. 이러한 주사기를 개발하는 기업 중 비교적 높은 비율(약 40%)이 중견기업입니다.

- 인슐린 약물용 웨어러블 인젝터의 약 65%가 상용화되어 있으며, 그 중 대부분은 빈번한 투여가 필요한 환자를 대상으로 집중적인 기초 및 추가 인슐린 요법을 가능하게 하는 1형 당뇨병을 대상으로 하고 있습니다.

- 현재 시장 상황에서는 비인슐린 약물 투여용 웨어러블 인젝터를 개발하는 여러 기업이 전 세계에서 존재하며, 이들 기업의 대다수(64%)가 유럽에 본사를 두고 있습니다.

- 비인슐린 약물을 저장하는 카트리지를 채택한 웨어러블 인젝터는 약 70%를 차지합니다. 또한 약 85%의 디바이스가 블루투스 연결 기능을 갖추고 있으며, 첨단 모니터링 및 데이터 통합이 가능합니다.

- 비인슐린 약물 투여를 위해 전 세계에서 약 20가지에 가까운 약물과 기기 조합을 사용할 수 있습니다. 이들 장치의 55% 이상은 비교적 규모가 큰 기업이 자체적인 첨단 제조 역량을 활용하여 개발한 것입니다.

- 비인슐린 약물을 투여하는 약물-기기 조합의 60%가 상용화되어 있습니다. 특히 신경질환이나 종양질환의 치료에서 이러한 장치 조합이 널리 보급되고 있습니다.

- 웨어러블 인젝터 분야에서 공개된 특허의 약 70%는 특허 출원이며, 특히 특허의 대부분(약 75%)이 북미에서 공개되고 있습니다.

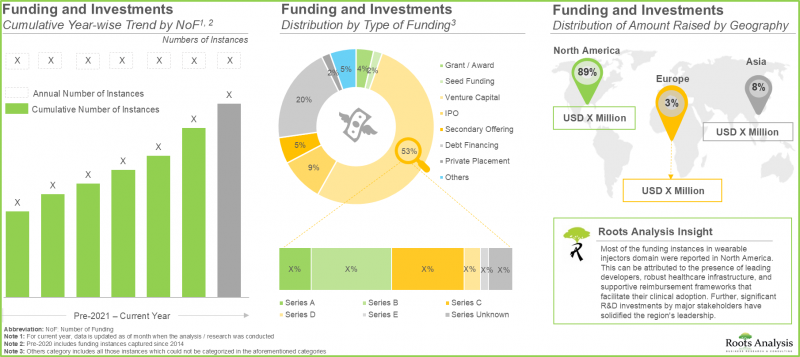

- 웨어러블 인젝터는 약물의 자가 투여를 가능하게 하고 의료 비용을 절감하는 등 다양한 장점을 가지고 있으며, 여러 투자자들이 자금을 지원하고 있으며, 2020년 이후 165억 달러 이상이 투자되고 있습니다.

- 지금까지 다양한 웨어러블 인젝터의 안전성과 유효성을 평가하기 위한 임상시험이 여러 건 등록되어 있습니다. 이러한 연구의 대부분은 미국 전역의 시설에서 수행되고 있습니다.

- 만성질환의 유병률 증가와 재택 및 환자 중심 치료 모델로의 전환을 배경으로 웨어러블 인젝터 시장은 향후 수년간 견고한 성장을 보일 것으로 예측됩니다.

- 패치형 펌프는 눈에 잘 띄지 않는 얇은 디자인, 뛰어난 환자 편의성, 보다 간편한 자가투약이 가능하므로 가장 큰 시장 점유율을 차지할 것으로 예측됩니다.

- 현재 인슐린 약제용 웨어러블 인젝터 시장의 대부분은 첨단 의료 인프라와 통합형 CGM 대응 펌프 기술의 보급으로 북미가 차지하고 있습니다.

- 북미 웨어러블 인젝터 시장은 만성질환의 유병률 증가와 이 지역의 유리한 상환 환경으로 인해 올해 가장 큰 점유율을 차지할 것으로 예측됩니다.

- 미국 웨어러블 인젝터 시장은 환자 중심의 대용량 주사기에 대한 수요 증가로 인해 예측 기간 중 더 높은 CAGR로 성장할 것으로 예측됩니다.

- 탄탄한 의약품 개발 파이프라인과 재택의료에 대한 관심이 높아짐에 따라 웨어러블 인젝터 시장은 향후 수년간 큰 폭의 성장이 예상됩니다.

웨어러블 인젝터 시장

시장 규모 및 기회 분석은 다음 매개 변수를 기반으로 세분화됩니다.

디바이스별 시장

- 패치 펌프

- 주입 펌프

자동화 수준별 시장

- 자동화/스마트 펌프

- 수동 펌프

용도별 시장 분석

- 일회용

- 재사용(일회용 부품)

치료 영역별 시장

- 종양 질환

- 순환기 질환

- 자가면역질환

- 신경질환

- 기타

지역별 시장

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 프랑스

- 독일

- 영국

- 이탈리아

- 스페인

- 기타 유럽

- 아시아

- 중국

- 인도

- 일본

- 파키스탄

- 기타 아시아 국가

- 중동 및 북아프리카

- 이집트

- 이스라엘

- 사우디아라비아

- 라틴아메리카

- 아르헨티나

- 브라질

웨어러블 인젝터 시장 - 주요 부문

주입 펌프 부문이 가장 큰 시장 점유율을 차지하고 있습니다.

인슐린 약물용 웨어러블 인젝터 시장은 패치 펌프, 주입 펌프 등 다양한 장치 유형으로 분류됩니다. 당사의 예측에 따르면 주입 펌프 카테고리는 웨어러블 인젝터의 기존 시장 점유율의 약 95%를 차지하고 있습니다. 이는 약물 투여에 있으며, 타의 추종을 불허하는 정확성과 적응성 등의 장점 때문입니다. 또한 패치 펌프 부문은 가정내 사용 및 자가 투여의 편의성 향상으로 인해 향후 더 높은 CAGR을 나타낼 것으로 예측됩니다. 눈에 잘 띄지 않는 디자인으로 당뇨병, 암 등의 지속적인 치료에 적합하며, 질병률 증가에 따라 빠른 보급이 기대됩니다.

북미: 최고 점유율을 확보하며 시장을 독점합니다.

북미는 웨어러블 인젝터 시장에서 가장 큰 규모(시장 점유율 약 70%)를 차지하고 있습니다. 첨단화된 의료 시스템, 높은 만성질환 유병률, 의료 지출에 대한 투자 증가 등 여러 요인이 이 지역 시장 성장을 이끄는 주요 요인으로 작용하고 있습니다.

비인슐린 기반 웨어러블 인젝터 시장은 종양 질환 부문이 주도하고 있습니다.

전체 시장은 치료 영역에 따라 암 관련 질환, 심장질환, 신경질환, 자가면역질환, 기타 각종 질환으로 세분화됩니다. 비인슐린 약물용 웨어러블 인젝터 시장 분석에 따르면 높은 암 발생률과 복잡한 생물제제 및 화학요법의 투여 정확도로 인해 종양 질환 부문이 시장을 주도하고 있습니다. 신경질환 부문은 예측 기간 중 더 높은 CAGR로 성장할 것으로 예측됩니다.

웨어러블 인젝터 시장 대표 진출기업

- Becton Dickinson(BD)

- Enable Injections

- Insulet

- Medtronic

- Tandem Diabetes Care

- West Pharmaceutical Services

- Ypsomed

웨어러블 인젝터 시장 - 조사 범위

- 시장 규모 및 기회 분석 : 이 보고서는 웨어러블 인젝터 시장에 대해(A) 기기 유형,(B) 자동화 수준,(C) 용도,(D) 치료 분야,(E) 지역적 지역 등 주요 시장 부문에 초점을 맞춘 상세한 분석을 수록했습니다.

- 비인슐린 약물용 웨어러블 인젝터 시장 현황: 비인슐린 약물용 웨어러블 인젝터 시장 현황,(A)장치 유형,(B)개발 현황,(C)약물전달 방식,(D)사용 편의성,(E)약물 저장 용량, 약물 분자 유형,(F)투여량 유형,(G)약품 용량,(H)주사 모드,(I)치료 영역,(J)약품 용기 유형,(K)약품 충전 모드,(H)주요 진출기업,(I)설립 연도,(J)기업 규모,(K)본사 소재지,(L)주요 기업 관련 정보를 포함합니다.

- 비인슐린 약물 디바이스 복합체 시장 현황: 비인슐린 약물 디바이스 복합체 시장 현황에서 웨어러블 인젝터의 전반적인 시장 현황에 대한 상세한 개요와 함께(A)디바이스 유형,(B)개발 현황,(C)약물전달 방식,(D)사용법,(E)약물 저수지 용량, 약물분자 유형,(F) 투여량 유형,(G) 약물 투여량,(H) 주사 방법,(I) 치료영역,(J) 약물 용기 유형,(K) 약물 충전 방법,(H) 가장 활발하게 진출한 기업,(I) 설립연도,(J) 기업 규모,(K) 본사 소재지,(L) 주요 기업 관련 정보를 포함합니다.

- 인슐린 약물용 웨어러블 인젝터 시장 현황: 인슐린 약물용 웨어러블 인젝터 시장의 전반적인 시장 현황에 대해 상세한 시장 개요를 제시합니다. 여기에는(A) 장비 유형,(B) 개발 현황,(C) 약물전달 방식,(D) 사용법,(E) 약물 저장소 용량, 약물 분자의 유형,(F) 투여량 유형,(G) 약물 투여량,(H) 주사 방법,(I) 치료 영역,(J) 약물 용기 유형,(K) 약물 충전 방법,(H) 가장 활발하게 진입한 기업,( I) 설립연도,(J) 기업 규모,(K) 본사 소재지,(L) 주요 기업 관련 정보 포함.

- 기업 개요: 북미, 유럽, 아시아태평양의 웨어러블 인젝터 제조업체의 주요 기업 개요을(A) 설립연도,(B) 본사 소재지,(C) 제품 포트폴리오,(D) 최근 동향,(E) 향후 전망에 따라 상세하게 분석합니다.

- 특허 분석 : 지난 10년간 웨어러블 인젝터 관련 출원 및 등록된 특허에 대해(A) 특허 유형,(B) 특허 공개 연도,(C) 관할권,(D) CPC 분류 기호,(E) 조직 유형,(F) 새로운 중점 분야,(G) 가장 활발하게 진입한 기업,(H) 특허 벤치마킹 분석,( I) 인사이트 있는 특허 평가 분석 등 여러 관련 매개변수를 기반으로 한 상세한 분석.

- 유망한 약물 후보: 가까운 미래에 웨어러블 인젝터와 함께 개발될 가능성이 높은 시판 중인 약물/치료제 및 파이프라인 후보에 대한 개요. 잠재적 후보물질(시판 중인 약물 및 임상 단계의 약물)에 대한 상세한 분석을 바탕으로(A) 약물 분자의 유형,(B) 개발 단계,(C) 적응증,(D) 투여 빈도,(E) 치료법의 유형,(F) 투여 방법,(G) 투여 경로 등 여러 가지 매개변수를 고려하여 식별합니다. 것입니다.

- 임상시험 분석 : 웨어러블 인젝터 관련 완료, 진행, 계획 중인 임상시험에 대해(A) 임상시험 모집 현황,(B) 임상시험 등록 연도,(C) 임상시험 단계,(D) 임상시험 설계,(E) 스폰서/협력기관 유형,(F) 주요 진입업체(등록 건수 기준),(G) 중점 분야,(H) 중점 치료 분야,(I) 지역적 범위 F) 주요 시장 진출기업(등록 시험 수 기준),(G) 중점 분야,(H) 치료 분야,(I) 지역적 범위.(G) 중점 영역,(H) 치료 영역,(I) 지역.

- 자금조달 및 투자 분석 : 해당 분야의 자금조달 및 투자 계약을(A) 자금조달 연도,(B) 자금조달 형태,(C) 투자 금액,(D) 지역,(E) 가장 활발하게 진출한 기업 등 관련 매개변수를 기준으로 분석합니다.

- SWOT 분석 : 커넥티드/스마트 약물전달 장치 개발에 관련된 다양한 단계(연구개발(R&D), 제품 제조 및 조립, 제품 유통, 마케팅 및 판매, 시판 후 조사)에 대해 각 단계별 비용 요구사항에 대한 정보와 함께 논의하고, 상세한 밸류체인 분석.

- 규제 현황 및 상환 환경: 북미(미국, 캐나다, 멕시코), 유럽(영국, 프랑스, 독일, 이탈리아, 스페인, 기타 유럽 국가), 아시아태평양 및 기타 지역(호주, 브라질, 중국, 중국, 인도, 이스라엘, 일본, 뉴질랜드, 싱가포르, 호주, 브라질, 중국, 인도, 이스라엘, 일본, 뉴질랜드, 싱가포르, 남아프리카공화국, 한국, 대만, 태국). 남아프리카공화국, 한국, 대만, 태국)의 의료기기 승인에 대한 규제 당국의 다양한 가이드라인에 대한 인사이트.

- 시장 영향 분석 : 웨어러블 인젝터 시장의 성장에 영향을 미칠 수 있는 요인에 대한 상세한 분석입니다. 주요 촉진요인, 잠재적 억제요인, 새로운 기회, 기존 과제에 대한 식별 및 분석도 포함됩니다.

목차

제1장 서문

제2장 조사 방법

제3장 시장 역학

제4장 거시경제 지표

제5장 개요

제6장 서론

제7장 비인슐린 약제용 웨어러블 인젝터 : 시장 구도

제8장 비인슐린약 약제와 디바이스 병용 : 시장 구도

제9장 인슐린 약제용 웨어러블 인젝터 : 시장 구도

제10장 제품 경쟁력 분석

제11장 웨어러블 인젝터 개발 기업 : 기업 개요

제12장 약물과 디바이스 조합 : 디바이스 개요

제13장 파트너십과 협업

제14장 주요인수 대상

제15장 특허 분석

제16장 웨어러블 인젝터 : 유망 약제 후보

제17장 임상시험 분석

제18장 자금조달과 투자 분석

제19장 SWOT 분석

제20장 사례 연구 : 디바이스 개발 공급망에서 계약 제조 조직의 역할

제21장 의료기기의 규제와 상환의 현황

제22장 시장 영향 분석 : 촉진요인, 억제요인, 기회, 과제

제23장 비인슐린 약제용 웨어러블 인젝터 시장

제24장 비인슐린 약제용 웨어러블 인젝터 시장(디바이스별)

제25장 비인슐린 약제용 웨어러블 인젝터 시장(사용법별)

제26장 비인슐린 약제용 웨어러블 인젝터 시장(치료 영역별)

제27장 비인슐린 약제용 웨어러블 인젝터 시장(지역별)

제28장 인슐린 약제용 웨어러블 인젝터 시장

제29장 인슐린 약제용 웨어러블 인젝터 시장(디바이스별)

제30장 인슐린 약제용 웨어러블 인젝터 시장(자동화 레벨별)

제31장 인슐린 약제용 웨어러블 인젝터 시장(지역별)

제32장 결론

제33장 이그제큐티브 인사이트

제34장 부록 I : 표 데이터

제35장 부록 II : 기업 및 조직 리스트

KSA 26.03.20Wearable Injectors Market: Overview

As per Roots Analysis, the global wearable injectors market is estimated to grow from USD 6.8 billion in the current year to USD 13.0 billion by 2035, at a CAGR of 7.4% during the forecast period, till 2035.

Wearable Injectors Market: Growth and Trends

The rise in autoimmune diseases, heart conditions, and cancer continues to put pressure on healthcare systems as the population grows and ages. In response, pharmaceutical companies are developing patient-focused solutions to enhance treatment adherence and outcomes through advanced drug delivery technologies. Wearable injectors, such as on-body patch pumps, provide sustained basal, bolus, or continuous doses of large-volume biologics, making administration easier and improving adherence. Their integrated safety features minimize needlestick injuries, while ensuring comfort and confidence when used at home. Illustrating this trend, BD recently announced the launch of the first clinical trial sponsored by a pharmaceutical company for a combination product using the BD Libertas wearable injector for the subcutaneous delivery of complex biologics. This highlights the increasing trust in these large-volume, patient-friendly systems for at-home care.

Due to this development, wearable devices have emerged as the favored option for administering drugs subcutaneously in home-care environments. In addition, the rise in popularity of on-body injectors has led pharmaceutical companies and medical device manufacturers to incorporate advanced features into their product lines. These features include artificial intelligence algorithms, mobile applications with intelligent health monitoring, reminders, and visual or audible notifications confirming drug delivery. With constant advancements occurring in this sector, it is anticipated that the usage of such on-body injectors will rise substantially, fueling market expansion in the foreseeable future.

Growth Drivers: Strategic Enablers of Market Expansion

The market drivers in the wearable injector's domain include rising prevalence of chronic diseases like diabetes, oncology, and autoimmune disorders, which fuels the demand for convenient subcutaneous delivery of biologics and high-volume therapies. In addition, the market is fueled by the growing preference for home healthcare enables self-administration, reducing clinic visits and enhancing patient autonomy and adherence. Technological advancements, including miniaturization, wireless connectivity for real-time monitoring, and integration with digital health platforms, further accelerate the market adoption.

Market Challenges: Critical Barriers Impeding Progress

Key challenges hindering the adoption of wearable injectors include rising development and production costs especially in emerging markets with weak reimbursement infrastructure. Further, stringent regulatory requirements delay approvals of these devices and raise compliance burdens for manufacturers. Patient-related barriers, such as lack of training on device use and concerns over safety or comfort, hinder widespread adoption alongside competition from established delivery methods.

Wearable Injectors Market: Key Insights

The report delves into the current state of the wearable injectors market and identifies potential growth opportunities within industry. Some key findings from the report include:

- The current market landscape features more than 50 wearable injectors for insulin drugs; a relatively higher proportion (~40%) of the companies developing such injectors are mid-sized players.

- About 65% of wearable injectors for insulin drugs are commercialized; of these, majority of devices are targeting Type I diabetes to enable intensive basal-bolus insulin regimens for patients requiring frequent dosing.

- The current market landscape features the presence of several companies developing wearable injectors for the delivery of non-insulin drugs worldwide; majority (64%) of these firms are headquartered in Europe.

- Around 70% of the wearable injectors utilize cartridges for storing non-insulin drugs; further, about 85% of the devices offer Bluetooth connectivity, enabling enhanced monitoring and data integration capabilities.

- Close to 20 drug-device combinations are available for delivering non-insulin drugs globally; over 55% of these devices have been developed by relatively larger players utilizing their advanced manufacturing capabilities.

- 60% of drug-device combinations for delivering non-insulin drugs are commercialized; notably, such device combinations are more popular for neurological and oncological disorders.

- Around 70% of the patents published in the wearable injectors domain are patent applications; notably, majority (~75%) of the patents have been published in North America.

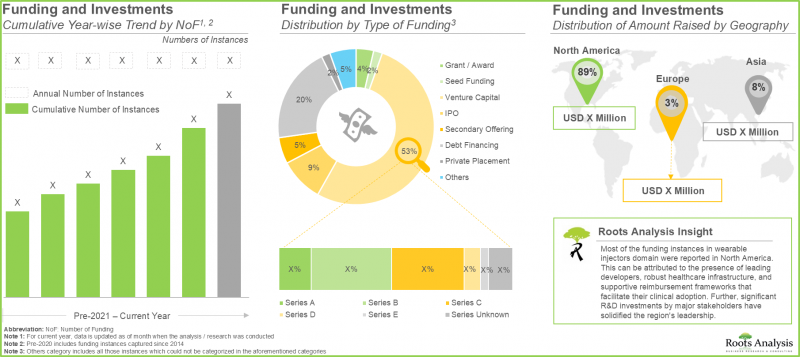

- Given various benefits of wearable injectors in enabling self-administration of drugs and reducing healthcare costs, several investors have extended financial support; over USD 16.5 billion has been invested since 2020.

- Several clinical trials have been registered till date to evaluate the safety and efficacy of various wearable injectors; majority of these studies have been conducted across various sites in the US.

- Driven by the rising prevalence of chronic diseases and the shift towards home-based, patient-centric care models, the wearable injectors market is anticipated to witness robust growth over the coming years.

- Patch pumps are expected to capture the largest market share due to their discreet low-profile design, superior patient comfort, and simpler self-administration.

- Currently, the majority share in the wearable injectors market for insulin is captured by North America owing to its advanced healthcare infrastructure and widespread adoption of integrated CGM-enabled pump technologies.

- The wearable injectors market in North America is expected to capture maximum share in current year, owing to the rising prevalence of chronic diseases and a favorable reimbursement landscape in this region.

- The wearable injectors market in the US is poised to grow at a higher CAGR over the forecast period, driven by the rising demand for patient-centric large-volume injectors.

- Given the robust drug development pipeline and rising focus on home-based care, the wearable injectors market is poised for substantial growth in the coming years.

Wearable Injectors Market

The market sizing and opportunity analysis has been segmented across the following parameters:

Market by Type of Device

- Patch Pumps

- Infusion Pumps

Market by Degree of Automation

- Automated / Smart Pump

- Manual Pumps

Market by Usability

- Disposable

- Reusable (Disposable Components)

Market by Therapeutic Area

- Oncological Disorders

- Cardiovascular Disorders

- Autoimmune Disorders

- Neurological Disorders

- Other Disorders

Market by Geographical Regions

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- Italy

- Spain

- Rest of Europe

- Asia

- China

- India

- Japan

- Pakistan

- Rest of Asia

- Middle East and North Africa

- Egypt

- Israel

- Saudi Arabia

- Latin America

- Argentina

- Brazil

Wearable Injectors Market: Key Segments

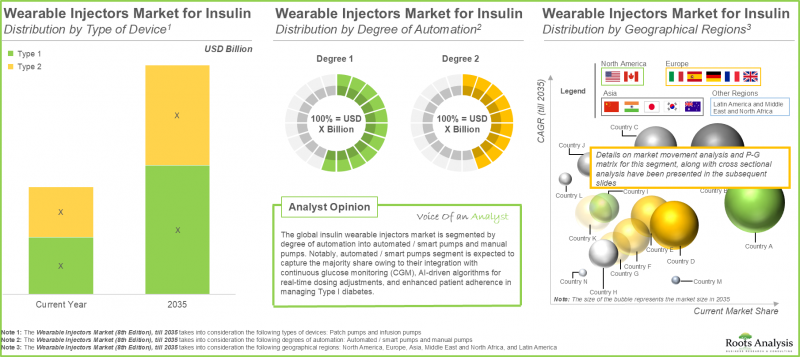

Infusion Pumps Segment Account for the Largest Market Share

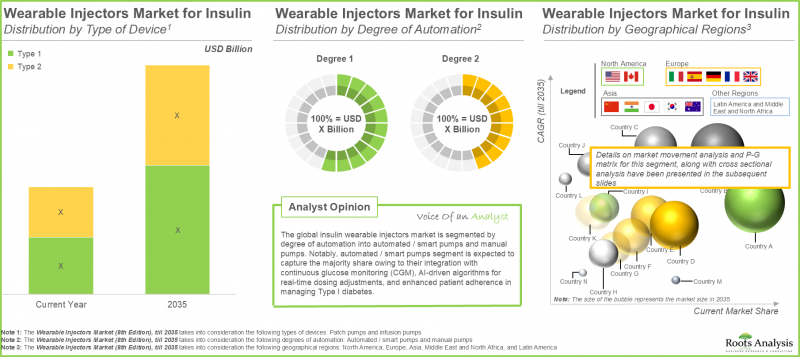

The overall market for wearable insulin injectors is divided into various device types, including patch pumps and infusion pumps. According to our projections, the infusion pumps category represents around 95% of the existing market share for wearable injectors. This is due to its advantages, including their unparalleled accuracy and adaptability in administering drugs. Further, the patch pumps segment is expected to experience a higher CAGR in the future, due to the fact that they provide enhanced convenience for home use and self-administration. Their discreet design is ideal for ongoing treatments (such as diabetes and cancer), facilitating swift adoption as disease rates increase.

North America: Dominating the Market by Securing Highest Share

North America accounts for largest wearable injectors market size (with nearly 70% of the market share). Several factors, such as advanced healthcare system, high prevalence of chronic diseases and increased investment in healthcare spending are some of the prominent factors driving the market growth in this region.

Oncological Disorders Segment Dominates the Non-Insulin Wearable Injectors Market

The overall market is divided into sub-segments according to therapeutic areas, which include cancer-related disorders, heart disorders, neurological issues, autoimmune conditions, and various other disorders. Based on our analysis of the non-insulin wearable injector market, the oncological disorders segment leads the market, owing to the significant incidence of cancer and the accuracy of these devices for administering complex biologics and chemotherapy. The segment for neurological disorders is expected to grow at a greater CAGR throughout the forecast period.

Primary Research Overview

Discussions with multiple stakeholders in this domain influenced the opinions and insights presented in this study. The market report includes transcripts of the following other third-party discussions:

- Chief Executive Officer, Small Company, US

- Chief Executive Officer, Mid Sized Company, US

- Chief Executive Officer, Small Company, Denmark

- Former President and Chief Executive Officer, Mid Sized Company, US

- Vice President and Chief Scientist, Large Company, Israel

- Former Vice President and General Manager, Biologics, Very Large Company, US

- Anonymous, Large Company, Switzerland

- Engineering Project Manager / Senior System Engineer, Small Company, Switzerland

- Vice President, Marketing and Alliance Management, Mid Sized Company, US

Example Players in Wearable Injectors Market

- Becton Dickinson (BD)

- Enable Injections

- Insulet

- Medtronic

- Tandem Diabetes Care

- West Pharmaceutical Services

- Ypsomed

Wearable Injectors Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the wearable injectors market, focusing on key market segments, including [A] type of device [B] degree of automation, [C] usability, [D] therapeutic area, and [E] geographical regions.

- Wearable Injectors for Non-Insulin Drugs Market Landscape: A detailed overview of the overall market landscape of wearable injectors for non-insulin drugs market landscape, along with information on several relevant parameters, such as [A] type of device, [B] status of development, [C] type of drug delivery, [D] usability, [E] drug reservoir volume, type of drug molecule, [F] type of dose, [G] dose of drug, [H] mode of injection, [I] therapeutic area, [J] type of drug container, [K] mode of drug filling, [H] most active players, [I] year of establishment, [J] company size, [K] location of headquarters and [L] leading players.

- Drug Device Combinations for Non-Insulin Drugs Market Landscape: A detailed overview of the overall market landscape of wearable injectors for drug device combinations for non-insulin drugs market landscape, along with information on several relevant parameters, such as [A] type of device, [B] status of development, [C] type of drug delivery, [D] usability, [E] drug reservoir volume, type of drug molecule, [F] type of dose, [G] dose of drug, [H] mode of injection, [I] therapeutic area, [J] type of drug container, [K] mode of drug filling, [H] most active players, [I] year of establishment, [J] company size, [K] location of headquarters and [L] leading players.

- Wearable Injectors for Insulin Market Landscape: A detailed overview of the overall market landscape of wearable injectors for insulin drugs market landscape, along with information on several relevant parameters, such as [A] type of device, [B] status of development, [C] type of drug delivery, [D] usability, [E] drug reservoir volume, type of drug molecule, [F] type of dose, [G] dose of drug, [H] mode of injection, [I] therapeutic area, [J] type of drug container, [K] mode of drug filling, [H] most active players, [I] year of establishment, [J] company size, [K] location of headquarters and [L] leading players.

- Company Profiles: In-depth profiles of leading players manufacturing wearable injectors in North America, Europe and Asia-Pacific based on [A] year of establishment, [B] location of headquarters, [C] product portfolio, [D] recent developments and [E] an informed future outlook.

- Patent Analysis: An in-depth analysis of patents that have been filed / granted related to wearable injectors over the last decade across several relevant parameters, such as [A] type of patent, [B] patent publication year, [C] jurisdiction, [D] CPC symbol, [E] type of organization, [F] emerging focus area, [G] most active players, [H] patent benchmarking analysis and [I] insightful patent valuation analysis.

- Likely Drug Candidates: An overview of marketed drugs / therapies and pipeline candidates that are likely to be developed in combination with wearable injectors in the near future, identified on the basis of an in-depth analysis of potential candidates (marketed drugs and clinical-stage drugs), taking into consideration multiple parameters, such as [A] type of drug molecule, [B] phase of development, [C] indication, [D] dosing frequency, [E] type of therapy, [F] method of administration and [G] route of administration.

- Clinical Trial Analysis: A detailed analysis of completed, ongoing and planned clinical trials related to wearable injectors based on several relevant parameters, such as [A] trial recruitment status, [B] trial registration year, [C] trial phase, [D] study design, [E] type of sponsor / collaborator, [F] leading players (based on the number of registered trials), [G] key focus area, [H] therapeutic area, and [I] geography.

- Funding and Investment Analysis: An analysis of funding and investment signed in the domain based on several relevant parameters, such as [A] year of funding, [B] type of funding, [C] amount invested, [D] geography, [E] and most active players.

- SWOT Analysis: An in-depth value chain analysis featuring a discussion on various steps involved in the development of connected / smart drug delivery devices, including research and development (R&D), product manufacturing and assembly, product distribution, marketing and sales, and post-market surveillance, along with the information on cost requirements across each of the aforementioned stages.

- Regulatory and Reimbursement Landscape: A discussion on the various guidelines established by regulatory bodies for medical device approvals across North America (US, Canada and Mexico), Europe (UK, France, Germany, Italy, Spain and rest of Europe), Asia-Pacific and rest of the world (Australia, Brazil, China, India, Israel, Japan, New Zealand, Singapore, South Africa, South Korea, Taiwan, and Thailand).

- Market Impact Analysis: An in-depth analysis of the factors that can impact the growth of wearable injectors market. It also features identification and analysis of key drivers, potential restraints, emerging opportunities, and existing challenges.

Key Questions Answered in this Report

- Which are the leading companies in wearable injectors market?

- Which region dominates the wearable injectors market?

- What are the key trends observed in the wearable injectors market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by wearable injectors developers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Additional Benefits

- Complementary PPT Insights Pack

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Introduction to Drug Delivery Devices

- 6.3. Conventional Parenteral Drug Delivery Devices

- 6.3.1. Needlestick Injuries

- 6.3.2. Incidence and Cost Burden

- 6.3.3. Prevention of Needlestick Injuries

- 6.3.4. Government Legislations for the Prevention of Needlestick Injuries

- 6.4. Emergence of Self-Administration Devices

- 6.4.1. Key Driving Factors

- 6.4.1.1. Rising Burden of Chronic Diseases

- 6.4.1.2. Healthcare Cost Savings

- 6.4.1.3. Need for Immediate Treatment in Emergency Situations

- 6.4.1.4. Growing Injectable Drugs Market

- 6.4.1.5. Need for Improving Medication Adherence

- 6.4.1. Key Driving Factors

- 6.5. Available Self-Injection Devices

- 6.5.1. Prefilled Syringes

- 6.5.2. Pen-Injectors

- 6.5.3. Needle-Free Injectors

- 6.5.4. Autoinjectors

- 6.5.5. Wearable Injectors

- 6.6. Regulatory Considerations

- 6.6.1. Medical Devices

- 6.6.2. Drug Device Combination Products

- 6.7. Future Perspectives

7. WEARABLE INJECTORS FOR NON-INSULIN DRUGS: MARKET LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Wearable Injectors for Non-Insulin Drugs: Overall Market Landscape

- 7.2.1. Analysis by Type of Device

- 7.2.2. Analysis by Status of Development

- 7.2.3. Analysis by Type of Drug Delivery

- 7.2.4. Analysis by Usability

- 7.2.5. Analysis by Drug Reservoir Volume

- 7.2.6. Analysis by Type of Drug Molecule

- 7.2.7. Analysis by Type of Dose

- 7.2.8. Analysis by Dose of Drug

- 7.2.9. Analysis by Mode of Injection

- 7.2.10. Analysis by Therapeutic Area

- 7.2.11. Analysis by Type of Drug Container

- 7.2.12. Analysis by Mode of Drug Filling

- 7.3. Wearable Injectors for Non-Insulin Drugs: Developer Landscape

- 7.3.1. Analysis by Year of Establishment

- 7.3.2. Analysis by Company Size

- 7.3.3. Analysis by Location of Headquarters

- 7.3.4. Leading Players: Analysis by Number of Wearable Injectors Developed for Non-Insulin

8. DRUG DEVICE COMBINATIONS FOR NON-INSULIN DRUGS: MARKET LANDSCAPE

- 8.1. Chapter Overview

- 8.2. Drug Device Combinations for Non-Insulin Drugs: Overall Market Landscape

- 8.2.1. Analysis by Type of Device

- 8.2.2. Analysis by Status of Development

- 8.2.3. Analysis by Type of Drug Delivery

- 8.2.4. Analysis by Usability

- 8.2.5. Analysis by Drug Reservoir Volume

- 8.2.6. Analysis by Type of Drug Molecule

- 8.2.7. Analysis by Type of Dose

- 8.2.8. Analysis by Dose of Drug

- 8.2.9. Analysis by Mode of Injection

- 8.2.10. Analysis by Therapeutic Area

- 8.2.11. Analysis by Type of Drug Container

- 8.2.12. Analysis by Mode of Drug Filling

- 8.3 Drug Device Combinations for Non-Insulin Drugs: Developer Landscape

- 8.3.1. Analysis by Year of Establishment

- 8.3.2. Analysis by Company Size

- 8.3.3. Analysis by Location of Headquarters

- 8.3.4. Device Developers: Distribution by Number of Drug Device Combination Developed

9. WEARABLE INJECTORS FOR INSULIN: MARKET LANDSCAPE

- 9.1. Chapter Overview

- 9.2. Wearable Injectors for Insulin: Overall Market Landscape

- 9.2.1. Analysis by Type of Device

- 9.2.2. Analysis by Status of Development

- 9.2.3. Analysis by Type of Insulin Delivery

- 9.2.4. Analysis by Type of Automated Insulin Delivery

- 9.2.5. Analysis by Type of Connectivity Feature

- 9.2.6. Analysis by Type of Feedback Mechanism

- 9.2.7. Analysis by Waterproofing Capability

- 9.2.8. Analysis by Usability

- 9.2.9. Analysis by Period of Use

- 9.2.10. Analysis by Type of Advanced Feature

- 9.2.11. Analysis by Type of Drug Container

- 9.2.12. Analysis by Mode of Drug Filling

- 9.2.13. Analysis by Type of Dose

- 9.2.14. Analysis by Type of Diabetes

- 9.2.15. Analysis by Availability of Connectivity Feature

- 9.3. Wearable Injectors for Insulin: Developer Landscape

- 9.3.1. Analysis by Year of Establishment

- 9.3.2. Analysis by Company Size

- 9.3.3. Analysis by Location of Headquarters

- 9.3.4. Leading Players: Analysis by Number of Wearable Injectors Developed for Insulin

10. PRODUCT COMPETITIVENESS ANALYSIS

- 10.1. Chapter Overview

- 10.2. Assumptions / Key Parameters

- 10.3. Methodology

- 10.4. Product Competitiveness Analysis

- 10.4.1. Product Competitiveness Analysis: Wearable Injectors for Non-Insulin Drugs

- 10.4.2. Product Competitiveness Analysis: Drug Device Combinations for Non-Insulin Drugs

- 10.4.3. Product Competitiveness Analysis: Wearable Injectors for Insulin

11. WEARABLE INJECTOR DEVELOPERS: COMPANY PROFILES

- 11.1. Chapter Overview

- 11.2. Key Players Developing Wearable Injectors for Non-Insulin

- 11.2.1. CCBio

- 11.2.1.1. Company Overview

- 11.2.1.2. Product Portfolio

- 11.2.1.3. Recent Developments and Future Outlook

- 11.2.2. E3D Elcam Drug Delivery Devices

- 11.2.3. Enable Injections

- 11.2.4. Gerresheimer

- 11.2.5. Sonceboz

- 11.2.6. Weibel CDS (Acquired by SHL Medical)

- 11.2.7. West Pharmaceuticals

- 11.2.1. CCBio

- 11.3. Key Players Developing Wearable Injectors for Insulin

- 11.3.1. CeQur

- 11.3.2. Debiotech

- 11.3.3. Eli Lilly

- 11.3.4. Insulet

- 11.3.5. Medtronic

- 11.3.6. Medtrum Technologies

- 11.3.7. PharmaSens

- 11.3.8. Roche

- 11.3.9. SOOIL Development

12. DRUG-DEVICE COMBINATIONS: DEVICE PROFILES

- 12.1. Chapter Overview

- 12.2. Neulasta(R) (pegfilgrastim) OnPro(TM) Kit

- 12.3. D-mine(R) Pump

- 12.4. Lasix(R) ONYU

- 12.5. The LUTREPULSE(R) System

- 12.6. ND0612L Next generation patch pump

- 12.7. Unnamed (Developed by Phillips Medisize)

- 12.8. FUROSCIX(R)

- 12.9. SMT-201 Pump

- 12.10. SMT-301 Pump

- 12.11. ULTOMRIS(R) Smartdose Injector (ravulizumab-cwvz)

- 12.12. EMPAVELI(R) Injector

- 12.13. SKYRIZI(R) On Body Injector (risankizumab)

- 12.14. VYALEV(TM) Pump (foscarbidopa and foslevodopa)

- 12.15. UDENYCA(R) on-body injector

- 12.16. ONAPGO(TM)

- 12.17. Remunity(R) Pump

- 12.18. G-Lasta(R) BodyPod

- 12.19. Sarclisa (isatuximab) On-Body Injector

13. PARTNERSHIPS AND COLLABORATIONS

- 13.1. Chapter Overview

- 13.2. Partnership Models

- 13.3. Wearable Injectors: Partnerships and Collaborations

- 13.3.1. Analysis by Year of Partnership

- 13.3.2. Analysis by Type of Partnership

- 13.3.3. Analysis by Year and Type of Partnership

- 13.3.4. Analysis by Type of Partner

- 13.3.5. Analysis by Type of Device

- 13.3.6. Most Active Players: Analysis by Number of Partnerships

- 13.3.7. Analysis by Geography

- 13.3.7.1. Local and International Agreements

- 13.3.7.2. Intercontinental and Intracontinental Agreements

14. KEY ACQUISITION TARGETS

- 14.1. Chapter Overview

- 14.2. Scope and Methodology

- 14.3. Scoring Criteria and Key Assumptions

- 14.4. Potential Acquisition Targets: Non-Insulin Drug Delivery Device Developers

- 14.5. Potential Acquisition Targets: Insulin Drug Delivery Device Developers

- 14.6. Concluding Remarks

15. PATENT ANALYSIS

- 15.1. Chapter Overview

- 15.2. Scope and Methodology

- 15.3. Wearable Injectors: Patent Analysis

- 15.3.1. Analysis by Type of Patent

- 15.3.2. Analysis by Patent Publication Year

- 15.3.3. Analysis by Patent Application Year

- 15.3.4. Analysis of Granted Patents and Patent Applications by Publication Year

- 15.3.5. Analysis by Jurisdiction

- 15.3.6. Analysis by Type of Applicant

- 15.3.7. Analysis by Patent Age

- 15.3.8. Analysis by CPC Symbol

- 15.3.9. Most Active Players: Analysis by Number of Patents

- 15.4. Wearable Injectors: Patent Benchmarking Analysis

- 15.4.1. Analysis by Patent Characteristics

- 15.5. Patent Valuation

- 15.6. Leading Patents by Number of Citations

16. WEARABLE INJECTORS: LIKELY DRUG CANDIDATES

- 16.1. Chapter Overview

- 16.2. Marketed Drugs

- 16.2.1. Most Likely Candidates for Delivery via Wearable Injectors

- 16.2.2. Likely Candidates for Delivery via Wearable Injectors

- 16.2.3. Less Likely Candidates for Delivery via Wearable Injectors

- 16.2.4. Least Likely Candidates for Delivery via Wearable Injectors

- 16.3. Clinical Stage Drugs

- 16.3.1. Most Likely Candidates for Delivery via Wearable Injectors

- 16.3.2. Likely Candidates for Delivery via Wearable Injectors

- 16.3.3. Less Likely Candidates for Delivery via Wearable Injectors

- 16.3.4. Least Likely Candidates for Delivery via Wearable Injectors

17. CLINICAL TRIAL ANALYSIS

- 17.1. Chapter Overview

- 17.2. Scope and Methodology

- 17.3. Wearable Injectors: Clinical Trial Analysis

- 17.3.1. Analysis by Trial Recruitment Status

- 17.3.2. Analysis by Trial Registration Year

- 17.3.3. Analysis of Enrolled Patient Population by Trial Registration Year

- 17.3.4. Analysis by Trial Phase

- 17.3.5. Analysis of Enrolled Patient Population by Trial Phase

- 17.3.6. Analysis by Trial Registration Year and Trial Recruitment Status

- 17.3.7. Analysis by Study Design

- 17.3.8. Analysis by Type of Sponsor / Collaborator

- 17.3.9. Analysis by Therapeutic Area

- 17.3.10. Most Active Players: Analysis by Number of Registered Trials

- 17.3.11. Most Popular Wearable Injectors: Analysis by Number of Registered Trials

- 17.3.12. Analysis by Geography

- 17.3.12.1. Analysis by Trial Recruitment Status and Geography

- 17.3.12.2. Analysis of Enrolled Patient Population by Trial Recruitment Status and Geography

18. FUNDING AND INVESTMENT ANALYSIS

- 18.1. Chapter Overview

- 18.2. Types of Funding

- 18.3. Wearable Injectors: Funding and Investment Analysis

- 18.3.1. Analysis by Year of Funding

- 18.3.2. Analysis of Amount Invested by Year

- 18.3.3. Analysis by Type of Funding

- 18.3.4. Analysis by Type of Device

- 18.3.5. Analysis of Amount Invested by Year and Type of Funding

- 18.3.6. Analysis of Amount Invested by Type of Device

- 18.3.7. Analysis by Target Disease Indication

- 18.3.8. Most Active Players: Analysis by Number of Funding Instances

- 18.3.9. Most Active Players: Analysis by Amount Invested

- 18.3.10. Leading Investors: Analysis by Number of Funding Instances

- 18.3.11. Analysis by Geography

19. SWOT ANALYSIS

- 19.1. Chapter Overview

- 19.2. SWOT Analysis

- 19.2.1. Strengths

- 19.2.2. Weaknesses

- 19.2.3. Opportunities

- 19.2.4. Threats

- 19.3. Wearable Injectors: Future Growth Opportunities

- 19.3.1. Rising Focus on Self-Administration of Drugs

- 19.3.2. Possibility of Integration with Mobile Applications

- 19.3.3. Potential Life Cycle Management Tool

- 19.3.4. Potential Usability for Multiple Therapeutic Areas

20. CASE STUDY: ROLE OF CONTRACT MANUFACTURING ORGANIZATIONS IN DEVICE DEVELOPMENT SUPPLY CHAIN

- 20.1. Chapter Overview

- 20.2. Device Development Supply Chain

- 20.3. Role of Contract Manufacturing Organizations (CMOs) in Device Development

- 20.4. List of CMOs

- 20.4.1. Geographical Distribution of CMOs

- 20.5. Medical Devices Design and Development Service Providers

21. REGULATORY AND REIMBURSEMENT LANDSCAPE FOR MEDICAL DEVICES

- 21.1. Chapter Overview

- 21.2. General Regulatory and Reimbursement Guidelines for Medical Devices

- 21.3. Regulatory and Reimbursement Landscape in North America

- 21.3.1. The US Scenario

- 21.3.1.1. Regulatory Authority

- 21.3.1.2. Review / Approval Process

- 21.3.1.3. Reimbursement Landscape

- 21.3.1.3.1. Payer Mix

- 21.3.1.3.2. Reimbursement Process

- 21.3.2. The Canadian Scenario

- 21.3.2.1. Regulatory Authority

- 21.3.2.2. Review / Approval Process

- 21.3.2.3. Reimbursement Landscape

- 21.3.2.3.1. Payer Mix

- 21.3.2.3.2. Reimbursement Process

- 21.3.3. The Mexican Scenario

- 21.3.3.1. Regulatory Authority

- 21.3.3.2. Review / Approval Process

- 21.3.3.3. Reimbursement Landscape

- 21.3.3.3.1. Payer Mix

- 21.3.1. The US Scenario

- 21.4. Regulatory and Reimbursement Landscape in Europe

- 21.4.1. Overall Scenario

- 21.4.1.1. Overall Regulatory Authority

- 21.4.1.2. Overall Review / Approval Process

- 21.4.2. The UK Scenario

- 21.4.2.1. Regulatory Authority

- 21.4.2.2. Review / Approval Process

- 21.4.2.3. Reimbursement Landscape

- 21.4.2.3.1. Payer Mix

- 21.4.2.3.2. Reimbursement Process

- 21.4.3. The French Scenario

- 21.4.3.1. Regulatory Authority

- 21.4.3.2. Review / Approval Process

- 21.4.3.3. Reimbursement Landscape

- 21.4.3.3.1. Payer Mix

- 21.4.3.3.2. Reimbursement Process

- 21.4.4. The German Scenario

- 21.4.4.1. Regulatory Authority

- 21.4.4.2. Review / Approval Process

- 21.4.4.3. Reimbursement Landscape

- 21.4.4.3.1. Payer Mix

- 21.4.4.3.2. Reimbursement Process

- 21.4.5. The Italian Scenario

- 21.4.5.1. Regulatory Authority

- 21.4.5.2. Review / Approval Process

- 21.4.5.3. Reimbursement Landscape

- 21.4.5.3.1. Payer Mix

- 21.4.5.3.2. Reimbursement Process

- 21.4.6. The Spanish Scenario

- 21.4.6.1. Regulatory Authority

- 21.4.6.2. Review / Approval Process

- 21.4.6.3. Reimbursement Landscape

- 21.4.6.3.1. Payer Mix

- 21.4.6.3.2. Reimbursement Process

- 21.4.1. Overall Scenario

- 21.5. Regulatory and Reimbursement Landscape in Asia-Pacific and Rest of the World

- 21.5.1. The Australian Scenario

- 21.5.1.1. Regulatory Authority

- 21.5.1.2. Review / Approval Process

- 21.5.1.3. Reimbursement Landscape

- 21.5.1.3.1. Payer Mix

- 21.5.1.3.2. Reimbursement Process

- 21.5.2. The Brazilian Scenario

- 21.5.2.1. Regulatory Authority

- 21.5.2.2. Review / Approval Process

- 21.5.2.3. Reimbursement Landscape

- 21.5.2.3.1. Payer Mix

- 21.5.2.3.2. Reimbursement Process

- 21.5.3. The Chinese Scenario

- 21.5.3.1. Regulatory Authority

- 21.5.3.2. Review / Approval Process

- 21.5.3.3. Reimbursement Landscape

- 21.5.3.3.1. Payer Mix

- 21.5.3.3.2. Reimbursement Process

- 21.5.1. The Australian Scenario

22. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 22.1. Chapter Overview

- 22.2. Market Drivers

- 22.3. Market Restraints

- 22.4. Market Opportunities

- 22.5. Market Challenges

- 22.6. Conclusion

23. WEARABLE INJECTORS MARKET FOR NON-INSULIN DRUGS

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Global Wearable Injectors Market for Non-Insulin Drugs, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 23.3.1. Scenario Analysis

- 23.3.1.1. Conservative Scenario

- 23.3.1.2. Optimistic Scenario

- 23.3.1. Scenario Analysis

- 23.4. Global Wearable Injectors Market for Non-Insulin Drugs, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 23.4.1. Scenario Analysis

- 23.4.1.1. Conservative Scenario

- 23.4.1.2. Optimistic Scenario

- 23.4.1. Scenario Analysis

- 23.5. Key Market Segmentations

24. WEARABLE INJECTORS MARKET FOR NON-INSULIN DRUGS, BY TYPE OF DEVICE

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Wearable Injectors Market for Non-Insulin Drugs: Distribution by Type of Device (By Value)

- 24.3.1. Wearable Patch Pump Market for Non-Insulin Drugs, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 24.3.2. Wearable Infusion Pump Market for Non-Insulin Drugs, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 24.4. Wearable Injectors Market for Non-Insulin Drugs: Distribution by Type of Device (By Volume)

- 24.4.1. Wearable Patch Pump Market for Non-Insulin Drugs, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 24.4.2. Wearable Infusion Pump Market for Non-Insulin Drugs, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 24.5. Data Triangulation and Validation

25. WEARABLE INJECTORS MARKET FOR NON-INSULIN DRUGS, BY USABILITY

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Wearable Injectors Market for Non-Insulin Drugs: Distribution by Usability (By Value)

- 25.3.1. Disposable Wearable Injectors Market for Non-Insulin Drugs, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 25.3.2. Reusable / Disposable Components Wearable Injectors Market for Non-Insulin Drugs, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 25.4. Wearable Injectors Market for Non-Insulin Drugs: Distribution by Usability (By Volume)

- 25.4.1. Disposable Wearable Injectors Market for Non-Insulin Drugs, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 25.4.2. Reusable / Disposable Components Wearable Injectors Market for Non-Insulin Drugs, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 25.5. Data Triangulation and Validation

26. WEARABLE INJECTORS MARKET FOR NON-INSULIN DRUGS, BY THERAPEUTIC AREA

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Wearable Injectors Market for Non-Insulin Drugs: Distribution by Therapeutic Area (By Value)

- 26.3.1. Wearable Injectors Market for Non-Insulin Drugs Targeting Oncological Disorders, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 26.3.2. Wearable Injectors Market for Non-Insulin Drugs Targeting Cardiovascular Disorders, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 26.3.3. Wearable Injectors Market for Non-Insulin Drugs Targeting Autoimmune Disorders, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 26.3.4. Wearable Injectors Market for Non-Insulin Drugs Targeting Neurological Disorders, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 26.3.5. Wearable Injectors Market for Non-Insulin Drugs Targeting Other Disorders, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 26.4. Wearable Injectors Market for Non-Insulin Drugs: Distribution by Therapeutic Area (By Volume)

- 26.4.1. Wearable Injectors Market for Non-Insulin Drugs Targeting Oncological Disorders, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 26.4.2. Wearable Injectors Market for Non-Insulin Drugs Targeting Cardiovascular Disorders, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 26.4.3. Wearable Injectors Market for Non-Insulin Drugs Targeting Autoimmune Disorders, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 26.4.4. Wearable Injectors Market for Non-Insulin Drugs Targeting Neurological Disorders, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 26.4.5. Wearable Injectors Market for Non-Insulin Drugs Targeting Other Disorders, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 26.5. Data Triangulation and Validation

27. WEARABLE INJECTORS MARKET FOR NON-INSULIN DRUGS, BY GEOGRAPHICAL REGIONS

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Wearable Injectors Market for Non-Insulin Drugs: Distribution by Geographical Regions (By Value)

- 27.3.1. Wearable Injectors Market for Non-Insulin Drugs in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 27.3.2. Wearable Injectors Market for Non-Insulin Drugs in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 27.3.3. Wearable Injectors Market for Non-Insulin Drugs in Asia, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 27.3.4. Wearable Injectors Market for Non-Insulin Drugs in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 27.3.5. Wearable Injectors Market for Non-Insulin Drugs in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 27.4. Wearable Injectors Market for Non-Insulin Drugs: Distribution by Geographical Regions (By Volume)

- 27.4.1. Wearable Injectors Market for Non-Insulin Drugs in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 27.4.2. Wearable Injectors Market for Non-Insulin Drugs in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 27.4.3. Wearable Injectors Market for Non-Insulin Drugs in Asia, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 27.4.4. Wearable Injectors Market for Non-Insulin Drugs in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 27.4.5. Wearable Injectors Market for Non-Insulin Drugs in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 27.5. Market Dynamics Assessment

- 27.5.1. Penetration Growth (P-G) Matrix

- 27.5.2. Market Movement Analysis

- 27.6. Data Triangulation and Validation

28. WEARABLE INJECTORS MARKET FOR INSULIN

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Global Wearable Injectors Market for Insulin, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 28.3.1. Scenario Analysis

- 28.3.1.1. Conservative Scenario

- 28.3.1.2. Optimistic Scenario

- 28.3.1. Scenario Analysis

- 28.4. Global Wearable Injectors Market for Insulin, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 28.4.1. Scenario Analysis

- 28.4.1.1. Conservative Scenario

- 28.4.1.2. Optimistic Scenario

- 28.4.1. Scenario Analysis

- 28.5. Key Market Segmentations

29. WEARABLE INJECTORS MARKET FOR INSULIN, BY TYPE OF DEVICE

- 29.1. Chapter Overview

- 29.2. Key Assumptions and Methodology

- 29.3. Wearable Injectors Market for Insulin: Distribution by Type of Device (By Value)

- 29.3.1. Wearable Patch Pump Market for Insulin, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 29.3.2. Wearable Infusion Pump Market for Insulin, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 29.4. Wearable Injectors Market for Insulin: Distribution by Type of Device (By Volume)

- 29.4.1. Wearable Patch Pump Market for Insulin, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 29.4.2. Wearable Infusion Pump Market for Insulin, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 29.5. Data Triangulation and Validation

30. WEARABLE INJECTORS MARKET FOR INSULIN, BY DEGREE OF AUTOMATION

- 30.1. Chapter Overview

- 30.2. Key Assumptions and Methodology

- 30.3. Wearable Injectors Market for Insulin: Distribution by Degree of Automation (By Value)

- 30.3.1. Automated / Smart Wearable Injectors Market for Insulin, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 30.3.2. Manual Wearable Injectors Market for Insulin, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 30.4. Wearable Injectors Market for Insulin: Distribution by Degree of Automation (By Volume)

- 30.4.1. Automated / Smart Wearable Injectors Market for Insulin, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 30.4.2. Manual Wearable Injectors Market for Insulin, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 30.5. Data Triangulation and Validation

31. WEARABLE INJECTORS MARKET FOR INSULIN, BY GEOGRAPHICAL REGIONS

- 31.1. Chapter Overview

- 31.2. Key Assumptions and Methodology

- 31.3. Wearable Injectors Market for Insulin: Distribution by Geographical Regions (By Value)

- 31.3.1. Wearable Injectors Market for Insulin in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.1.1. Wearable Injectors Market for Insulin in the US, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.1.2. Wearable Injectors Market for Insulin in Canada, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.2. Wearable Injectors Market for Insulin in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.2.1. Wearable Injectors Market for Insulin in Germany, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.2.2. Wearable Injectors Market for Insulin in the UK, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.2.3. Wearable Injectors Market for Insulin in Spain, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.2.4. Wearable Injectors Market for Insulin in France, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.2.5. Wearable Injectors Market for Insulin in Italy, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.2.6. Wearable Injectors Market for Insulin in Rest of Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.3. Wearable Injectors Market for Insulin in Asia, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.3.1. Wearable Injectors Market for Insulin in China, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.3.2. Wearable Injectors Market for Insulin in India, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.3.3. Wearable Injectors Market for Insulin in Japan, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.3.4. Wearable Injectors Market for Insulin in Pakistan, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.3.5. Wearable Injectors Market for Insulin in Rest of Asia, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.4. Wearable Injectors Market for Insulin in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.4.1. Wearable Injectors Market for Insulin in Brazil, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.4.2. Wearable Injectors Market for Insulin in Mexico, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.4.3. Wearable Injectors Market for Insulin in Argentina, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.5. Wearable Injectors Market for Insulin in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.5.1. Wearable Injectors Market for Insulin in Saudi Arabia, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.5.2. Wearable Injectors Market for Insulin in Israel, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.5.3. Wearable Injectors Market for Insulin in Egypt, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.3.1. Wearable Injectors Market for Insulin in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Value)

- 31.4. Wearable Injectors Market for Insulin: Distribution by Geographical Regions (By Volume)

- 31.4.1. Wearable Injectors Market for Insulin in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.1.1. Wearable Injectors Market for Insulin in the US, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.1.2. Wearable Injectors Market for Insulin in Canada, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.2. Wearable Injectors Market for Insulin in Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.2.1. Wearable Injectors Market for Insulin in Germany, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.2.2. Wearable Injectors Market for Insulin in the UK, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.2.3. Wearable Injectors Market for Insulin in Spain, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.2.4. Wearable Injectors Market for Insulin in France, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.2.5. Wearable Injectors Market for Insulin in Italy, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.2.6. Wearable Injectors Market for Insulin in Rest of Europe, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.3. Wearable Injectors Market for Insulin in Asia, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.3.1. Wearable Injectors Market for Insulin in China, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.3.2. Wearable Injectors Market for Insulin in India, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.3.3. Wearable Injectors Market for Insulin in Japan, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.3.4. Wearable Injectors Market for Insulin in Pakistan, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.3.5. Wearable Injectors Market for Insulin in Rest of Asia, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.4. Wearable Injectors Market for Insulin in Latin America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.4.1. Wearable Injectors Market for Insulin in Brazil, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.4.2. Wearable Injectors Market for Insulin in Mexico, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.4.3. Wearable Injectors Market for Insulin in Argentina, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.5. Wearable Injectors Market for Insulin in Middle East and North Africa, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.5.1. Wearable Injectors Market for Insulin in Saudi Arabia, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.5.2. Wearable Injectors Market for Insulin in Israel, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.5.3. Wearable Injectors Market for Insulin in Egypt, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.4.1. Wearable Injectors Market for Insulin in North America, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035) (By Volume)

- 31.5. Market Dynamics Assessment

- 31.5.1. Penetration Growth (P-G) Matrix

- 31.5.2. Market Movement Analysis

- 31.6. Data Triangulation and Validation