|

시장보고서

상품코드

2028469

크로마토그래피 시장(제2판) : 업계 동향과 세계 예측(-2035년) - 크로마토그래피 제품 유형별, 크로마토그래피 기기별, 액체 크로마토그래피별, 크로마토그래피 컴포넌트별, 최종사용자별 및 지역별Chromatography Market (2nd Edition): Industry Trends and Global Forecasts, till 2035 - Distribution by Type of Chromatography Product, Chromatography Instrument, Liquid Chromatography, Chromatography Component, End User and Geographical Regions |

||||||

크로마토그래피 시장 : 개요

세계의 크로마토그래피 시장 규모는 2035년까지 CAGR 6.53%로 확대하며, 현재 126억 5,000만 달러에서 2035년에는 223억 5,000만 달러에 달할 것으로 추정되고 있습니다.

크로마토그래피 시장 : 성장과 동향

크로마토그래피는 복잡한 혼합물의 분리, 식별 및 정제에 사용되는 널리 사용되는 분석 방법입니다. 20세기 초 미하일 츠베트(Mikhail Tsvet)에 의해 도입된 이후, 이 기술은 상당한 진전을 이루며 정확성, 효율성 및 적용성이 향상되었습니다. 크로마토그래피의 기본 원리는 이동상(액체 또는 기체)과 고정상(고체 또는 액체) 사이의 분석 대상 물질의 분포 차이를 기반으로 하며, 이를 통해 성분을 효과적으로 분리할 수 있습니다.

현재 크로마토그래피는 제약, 생명공학, 화학, 식품, 석유화학 등 다양한 산업 분야에서 널리 사용되고 있습니다. 특히 제약 산업에서 복잡한 시료의 정성 및 정량 분석을 지원하기 위한 크로마토그래피 시스템에 대한 수요가 크게 증가하고 있습니다. 이러한 성장은 주로 대규모 중개 연구, 정밀 종양학, 바이러스학, 백신 개발 등의 분야에서 크로마토그래피의 적용 확대에 의해 주도되고 있습니다.

또한 크로마토그래피는 법의학, 임상진단, 신약개발과 같은 신흥 분야에서도 점점 더 중요한 역할을 할 것으로 예상됩니다. 지속적인 기술 발전으로 크로마토그래피 시스템 및 장비의 적용 범위와 성능이 더욱 확대되어 다양한 산업 분야에서 혁신을 촉진하고 연구개발을 가속화할 것으로 예상됩니다.

성장 요인: 시장 확대의 전략적 원동력

크로마토그래피 시장은 첨단 검출 시스템, 인공지능, 소형화 플랫폼 통합 등 크로마토그래피 기술의 지속적인 발전에 힘입어 성장하고 있습니다. 이러한 기술은 크로마토그래피 산업의 연구 및 산업 분야에서의 응용 범위를 크게 확대했습니다. 연속 크로마토그래피 시스템의 등장으로 자동화된 고처리량 분리가 가능해져 운영 효율성이 더욱 향상되었습니다. 이를 통해 공정의 생산성을 향상시키는 동시에 총비용을 절감할 수 있습니다. 또한 기존 크로마토그래피 기법에 대한 환경적 우려가 커지면서 친환경 용매, 초임계 유체 등 지속가능한 대체 기술의 채택이 가속화되고 있습니다. 이러한 혁신은 시장의 주요 성장 요인으로 부상하고 있습니다.

시장 과제: 발전을 가로막는 심각한 장벽들

수많은 장점에도 불구하고 크로마토그래피는 그 보급을 방해할 수 있는 두드러진 도전에 직면해 있습니다. 주요 관심사는 결정화, 고해상도 한외여과, 고압 재접합 등 더 빠른 처리 시간과 높은 처리량을 제공하는 대체 분리 기술과의 경쟁 심화입니다.

액체 크로마토그래피-질량분석(LC-MS), 가스 크로마토그래피-질량분석(GC-MS)과 같은 고급 크로마토그래피 기술 및 하이브리드 기술에는 전문적인 지식과 기술이 요구됩니다. 또한 이러한 방법론에서는 방법 개발, 시료 준비, 데이터 분석과 같은 주요 작업에서 현장 지원이 필수적입니다. 또한 이러한 고도화된 시스템의 운영 및 유지보수에 필요한 숙련된 인력과 기술 인프라가 제한적이라는 점도 시장 진입을 가로막는 큰 장벽으로 작용하고 있습니다.

크로마토그래피 시장 : 주요 인사이트

이 보고서는 크로마토그래피 시장의 현황을 자세히 분석하고 업계의 잠재적인 성장 기회를 파악합니다. 보고서의 주요 조사 결과는 다음과 같습니다. :

- 현재 약 90여개 업체가 다양한 응용 분야에서 다양한 분석 대상 물질의 검출, 분리, 정제를 목적으로 하는 크로마토그래피 기기를 제공하고 있다고 주장하고 있습니다.

- 기업의 70%가 소분자 유기화합물부터 거대 생체고분자까지 다양한 화합물을 분리하기 위한 액체 크로마토그래피 기기를 제공하고 있습니다.

- 현재 약 95개 기업이 다양한 산업 분야에 크로마토그래피 수지, 컬럼, 매체, 멤브레인 등 다양한 유형의 크로마토그래피 소모품을 공급하고 있습니다.

- 크로마토그래피 분야의 이해관계자들은 복잡한 물질의 정성 및 정량 분석을 위해 다양한 유형의 소모품을 제공하고 있으며, 75% 이상의 기업이 고상으로서 멤브레인을 제공하고 있습니다.

- 크로마토그래피 분야에서 공개된 특허의 약 60%는 특허 출원이며, 특히 대부분(33%)은 지난 1년간 공개된 특허입니다.

- 증가하는 수요에 대응하기 위해 크로마토그래피 소모품 및 장비 공급업체들은 제품 포트폴리오를 확장하기 위해 적극적으로 노력하고 있습니다. 특히 2020년 이후 이 분야에서 눈에 띄는 인수합병이 잇따르고 있습니다.

- 크로마토그래피 기술의 지속적인 발전은 다양한 산업 분야의 분석 요구를 충족시키는 데 유용하다는 것이 입증되었으며, 이는 향후 크로마토그래피 시장을 꾸준히 견인할 것으로 예상됩니다.

- 복잡한 분자의 효율적인 검출, 분리 및 정제에 대한 수요가 증가함에 따라 크로마토그래피 기기 및 소모품 시장은 향후 10년간 연평균 6.53%의 성장률을 보일 것으로 예상됩니다.

- 예측된 시장 기회는 각 부문에 고르게 분포될 것으로 예상되며, 특히 프리패킹 컬럼 부문은 예측 기간 중 빠른 성장을 보일 것으로 예상됩니다.

- 미국의 주요 기업별 크로마토그래피 기기 및 소모품 분야의 급속한 기술 발전에 힘입어 크로마토그래피 시장은 CAGR 5.70%로 성장할 것으로 예상됩니다.

크로마토그래피 시장

시장 규모 및 기회 분석은 다음 매개 변수를 기반으로 세분화됩니다. :

크로마토그래피 제품 유형별

- 장비

- 소모품

- 기타 제품

크로마토그래피 기기 유형별

- 액체 크로마토그래피 기기

- 가스 크로마토그래피 기기

- 기타 크로마토그래피 기기

액체 크로마토그래피 유형별

- 고성능 액체 크로마토그래피(HPLC)

- 초고성능 액체 크로마토그래피(UHPLC)

- 크기 배제 크로마토그래피

- 플래시 크로마토그래피

- 기타 기법

크로마토그래피 구성요소 유형별

- 고정상

- 이동상

고정상 형태별

- 프리팩 컬럼

- 병/벌크 수지

- 기타 형식

최종사용자별

- 제약 및 생명공학 산업

- 학술-연구기관

- 기타

지역별

- 북미

- 북미

- 아시아태평양

- 라틴아메리카

- 중동 및 북아프리카

크로마토그래피 시장 : 주요 부문

크로마토그래피 제품 유형별 시장 점유율 분석 - 기기 부문이 크로마토그래피 시장을 주도하고 있습니다.

세계의 크로마토그래피 시장은 기기, 소모품 및 기타 제품으로 구분됩니다. 현재 장비 부문은 전체 시장의 약 70 %를 차지하고 있으며, 이는 주로 복잡한 혼합물의 분리, 정제 및 식별에 크로마토그래피 시스템을 광범위하게 사용했기 때문입니다. 이러한 우위는 분석 연구의 지속적인 발전과 정성적 및 정량적 인사이트를 모두 제공할 수 있는 고성능 장비에 대한 수요 증가로 인해 더욱 강화되고 있습니다.

크로마토그래피 기기 유형별 시장 점유율: 액체 크로마토그래피가 시장을 주도하다

액체 크로마토그래피 기기는 전체 시장의 65% 이상을 차지하고 있습니다. 이러한 장점은 복잡한 혼합물, 특히 가스 크로마토그래피와 같은 대체 방법으로는 분석이 어려운 극성 화합물이나 열 불안정성 화합물을 분리하는 데 효과적이기 때문입니다. 한편, 가스 크로마토그래피 분야는 비용 효율성과 조작의 용이성을 바탕으로 예측 기간 중 7.6%의 비교적 높은 CAGR로 성장할 것으로 예상됩니다.

액체 크로마토그래피 유형별 시장 점유율: UHPLC가 강력한 성장세를 보이고 있습니다.

액체 크로마토그래피 분야에서 시장은 고성능 액체 크로마토그래피(HPLC), 초고속 액체 크로마토그래피(UHPLC), 크기 제거 크로마토그래피, 플래시 크로마토그래피 및 기타 기술로 구성됩니다. 이 중 HPLC는 약 66%의 시장 점유율을 차지하고 있으며, 이는 주로 높은 정확도와 규제 준수가 필수적인 제약 및 생명공학 분야에서 중요한 역할을 담당하고 있기 때문입니다. 그러나 UHPLC 부문은 기존 크로마토그래피 기술 대비 빠른 분석 속도, 고해상도, 감도 향상 등의 장점에 힘입어 7.3%의 비교적 높은 CAGR로 성장할 것으로 예상됩니다.

크로마토그래피 구성 요소별 시장 점유율: 고정상 부문이 크로마토그래피 시장을 주도

구성 요소 유형에 따라 크로마토그래피 소모품 시장은 고정상과 이동상으로 분류됩니다. 고정상 부문은 효율적인 분석물 분리 및 정제에 있으며, 매우 중요한 역할을 담당하고 있으며, 현재 약 60%의 점유율로 시장을 독점하고 있습니다. 다른 요인으로는 고해상도, 선택적 상호작용, 비용 효율성 등을 들 수 있습니다. 반면, 이동상 부문은 용매 배합의 혁신과 LC-MS 및 GC-MS와 같은 첨단 하이브리드 기술과의 통합이 진행됨에 따라 8.7%의 높은 CAGR로 성장할 것으로 예상됩니다.

고정상 형태별 시장 점유율: 크로마토그래피 시장을 주도하는 프리패킹 컬럼

현재 프리팩 컬럼은 시장 점유율의 약 40%를 차지하고 있으며, 예측 기간 중 CAGR 8.0%로 성장할 것으로 예상됩니다. 이 시스템은 컬럼을 수동으로 채울 필요가 없어 준비 시간을 단축하고 전체 크로마토그래피 워크플로우의 생산성을 향상시키는 등 운영 효율성이 뛰어나다는 장점이 있습니다.

최종사용자별 시장 점유율: 제약 및 생명공학 분야가 크로마토그래피 시장을 주도

제약 및 생명공학 산업이 최종사용자 부문을 지배하고 있으며, 전체 시장의 약 75%를 차지하고 있습니다. 이는 주로 이러한 분야에서 크로마토그래피가 생체 분자 및 화학 물질의 분리, 식별 및 정제에 있으며, 매우 중요한 역할을 수행하기 때문입니다.

지역별 시장점유율: 아시아태평양이 더 높은 CAGR로 성장

북미는 크로마토그래피 시장에서 주도적인 위치를 유지할 것으로 예상되며, 올해 전체 시장의 약 40%를 차지할 것으로 예상되며, 당분간 그 우위가 지속될 것으로 보입니다. 이러한 선도적 지위는 미국내 주요 업계 진출 기업의 강력한 존재감과 AI 탑재 및 소형화된 크로마토그래피 시스템을 포함한 첨단 기술의 급속한 보급에 힘입어 지원되고 있습니다. 반면, 아시아태평양은 예측 기간 중 6.8%의 CAGR을 기록하며 가장 높은 성장률을 보일 것으로 예상됩니다. 이러한 성장은 비용 효율적인 크로마토그래피 솔루션의 가용성과 더불어 생명과학 분야의 분석 기술 혁신을 촉진하기 위한 정부 지원책에 의해 지원되고 있습니다.

크로마토그래피 시장의 주요 기업 사례

- Agilent Technologies

- Bio-Rad Laboratories

- Gilson

- JASCO

- MilliporeSigma

- Revvity(Previously known as PerkinElmer)

- Sartorius

- Shimadzu Scientific Instruments

- Thermo Fisher Scientific

크로마토그래피 시장 : 조사 범위

- 시장 규모 및 기회 분석 - 이 보고서는 의료기기 수탁제조 시장에 대한 상세한 분석을 통해 [A]크로마토그래피 유형, [B]크로마토그래피 기기 유형, [C]액체 크로마토그래피 유형, [D]크로마토그래피 구성요소 유형, [E]고정상 형태, [F]최종사용자, [G]지역 등 주요 시장 부문에 초점을 맞추고 있습니다. F] 최종사용자, [G] 지역과 같은 주요 시장 부문에 초점을 맞추고 있습니다.

- 크로마토그래피 기기 제공업체 시장 현황: 전체 크로마토그래피 기기 제공업체 시장에 대한 상세한 평가와 함께 [A]제공되는 크로마토그래피 기기, [B]제공되는 크로마토그래피 소모품 유형, [C]응용 분야, [D]회사 규모, [E]설립 연도, [F]본사 위치 등 여러 관련 매개 변수에 대한 정보를 제공합니다. [F] 본사 소재지 등 몇 가지 관련 파라미터에 대한 정보를 제공합니다.

- 기업 경쟁 분석 - [A] 기업의 강점, [B] 포트폴리오의 강점 등 다양한 관련 매개 변수를 기반으로 한 크로마토그래피 소모품 및 크로마토그래피 기기 공급 업체의 상세한 경쟁 분석.

- 크로마토그래피 소모품 제공업체 시장 현황: 크로마토그래피 소모품 제공업체 시장 현황에 대한 상세한 평가와 함께 [A]제공되는 분리 기술 유형, [B]제공되는 고체상 유형, [C]분석 대상 물질 유형, [D]회사 규모, [E]설립 연도, [F]본사 소재지 등 여러 매개 변수에 대한 정보를 제공합니다. 등 몇 가지 관련 파라미터에 대한 정보를 제공하고 있습니다.

- 기업 개요: 북미, 유럽, 아시아태평양에 기반을 둔 주요 기업의 상세한 프로필입니다. 이는 [A] 설립연도, [B] 본사 소재지, [C] 제품 포트폴리오, [D] 최근 동향, [E] 미래 전망 등 여러 가지 매개변수를 기반으로 합니다.

- 특허 분석 - [A] 특허 유형, [B] 공개 연도, [C] 출원 연도, [D] 특허권 및 특허 출원 건수, [E] 특허 관할권, [F] CPC 기호, [G] 특허 경과 기간, [H] 출원인 유형, [I] 개별 특허권자(지적재산권 포트폴리오 규모) 등 중요한 매개변수를 기반으로 합니다.

- 인수합병: 크로마토그래피 기업의 다양한 인수합병에 대해 [A] 계약 연도, [B] 계약 유형, [C] 지역, [D] 가장 활발한 플레이어, [E] 소유권 변경 매트릭스, [F] 주요 가치 동인, [G] 거래 배율(매출 기준)과 같은 관련 매개변수를 기반으로 상세한 분석을 수행합니다.

- 시장 영향 분석 - 시장 성장에 영향을 미칠 수 있는 요인에 대한 상세한 분석입니다. 또한 이 분야의 주요 촉진요인, 잠재적 제약, 새로운 기회, 기존 과제에 대한 식별 및 분석도 포함되어 있습니다.

목차

제1장 서문

제2장 조사 방법

제3장 경제적 및 기타 프로젝트 고유의 고려 사항

제4장 개요

제5장 서론

제6장 크로마토그래피 기기 공급업체 시장 구도

제7장 크로마토그래피 기기 공급업체 : 기업 경쟁력 분석

제8장 크로마토그래피 소모품 공급업체 시장 구도

제9장 기업 개요

제10장 특허 분석

제11장 합병·인수

제12장 시장 영향 분석 - 촉진요인, 저해요인, 기회, 과제

제13장 세계의 크로마토그래피 시장

제14장 크로마토그래피 시장 : 제품 유형별

제16장 크로마토그래피 시장 : 제공되는 소모품 형태별

제17장 크로마토그래피 시장 : 최종사용자별

제18장 크로마토그래피 시장 : 지역별

제19장 결론

제20장 경영 임원의 인사이트

제21장 부록 1 : 표형식 데이터

제22장 부록 2 : 기업 및 조직 리스트

KSA 26.05.20Chromatography Market: Overview

As per Roots Analysis, the global chromatography market is estimated to grow from USD 12.65 billion in the current year to USD 22.35 billion by 2035, at a CAGR of 6.53% during the forecast period, till 2035.

Chromatography Market: Growth and Trends

Chromatography is a widely adopted analytical technique used for the separation, identification, and purification of complex mixtures. Since its introduction by Mikhail Tsvet in the early 20th century, technology has undergone substantial advancements, enhancing its precision, efficiency, and applicability. The fundamental principle of chromatography is based on the differential distribution of analytes between a mobile phase (liquid or gas) and a stationary phase (solid or liquid), enabling effective component separation.

Currently, chromatography is extensively utilized across a broad spectrum of industries, including pharmaceuticals, biotechnology, chemicals, food, and petrochemicals. Notably, the pharmaceutical sector has witnessed a marked increase in demand for chromatography systems to support both qualitative and quantitative analysis of complex samples. This growth is primarily driven by the expanding application of chromatography in areas such as large-scale translational research, precision oncology, virology, and vaccine development.

Further, chromatography is expected to play an increasingly critical role in emerging domains such as forensic science, clinical diagnostics, and novel drug discovery. Continuous technological advancements are anticipated to further broaden the scope and capabilities of chromatography systems and instruments, thereby fostering innovation and accelerating research and development across multiple industries.

Growth Drivers: Strategic Enablers of Market Expansion

The chromatography market is propelled by ongoing advancements in chromatography technologies such as the integration of advanced detection systems, artificial intelligence, and miniaturized platforms. These technologies have significantly broadened the scope of applications across research and industrial domains within chromatography industry. The advent of continuous chromatography systems has further enhanced operational efficiency by enabling automated, high-throughput separations, thereby improving process productivity while reducing overall costs. Further, the increasing environmental concerns associated with conventional chromatography practices have accelerated the adoption of sustainable alternatives, including green solvents and supercritical fluids. These innovations are emerging as key growth drivers for the market.

Market Challenges: Critical Barriers Impeding Progress

Despite its numerous advantages, chromatography faces notable challenges that may hinder its widespread adoption. A primary concern is the growing competition from alternative separation technologies, including crystallization, high-resolution ultrafiltration, and high-pressure refolding which offer faster processing times and higher throughput capabilities.

Advanced and hyphenated chromatography techniques, including liquid chromatography-mass spectrometry (LC-MS) and gas chromatography-mass spectrometry (GC-MS), require specialized expertise. These methods also necessitate on-site support for key activities such as method development, sample preparation, and data interpretation. Furthermore, the limited availability of skilled personnel and technical infrastructure for the operation and maintenance of these advanced systems represents a key barrier to broader market penetration.

Chromatography Market: Key Insights

The report delves into the current state of the chromatography market and identifies potential growth opportunities within industry. Some key findings from the report include:

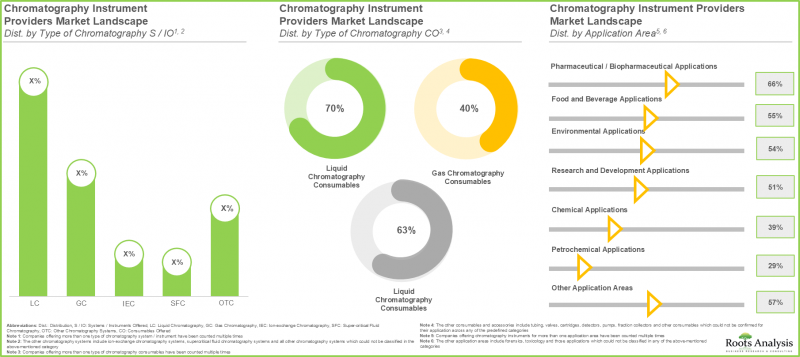

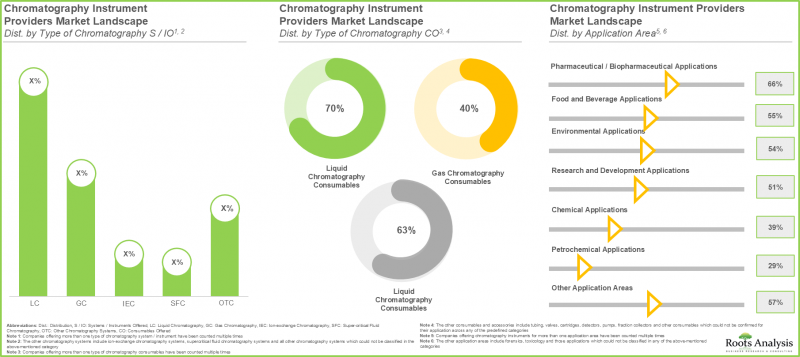

- Presently, close to 90 companies claim to offer chromatography instruments for the purpose of detection, separation and purification of different types of analytes across various application areas.

- 70% of the companies provide liquid chromatography instruments for the separation of a diverse range of compounds from small organic compounds to large biomacromolecules.

- Currently, around 95 companies offer different types of chromatography consumables, including chromatography resins, columns, media and membranes for a wide range of industries.

- Stakeholders engaged in the chromatography domain offer different types of consumables for qualitative and quantitative analysis of complex entities; more than 75% of the companies provide membranes as solid phases.

- Around 60% of the patents published in the chromatography domain are patent applications; notably, majority (33%) of the patents were published in the last year.

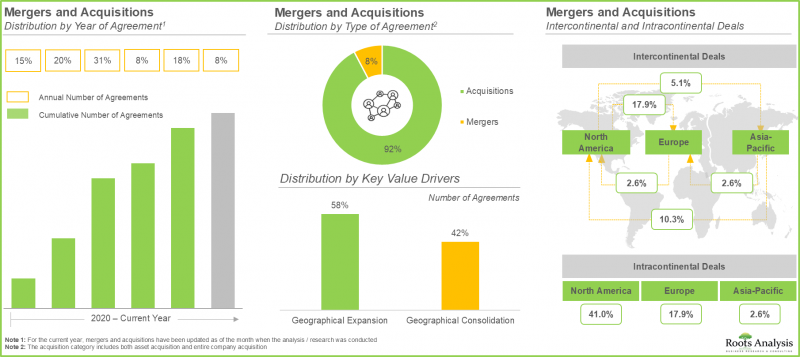

- To keep pace with the growing demand, chromatography consumables and instruments providers are actively expanding their product portfolio; notably the domain has witnessed notable mergers / acquisitions, since 2020.

- Ongoing advancements in chromatography techniques have proven useful in meeting the analytical demands across several industries; these are anticipated to drive the chromatography market at a steady pace in future.

- With growing demand for efficient detection, separation and purification of complex molecules, the market for chromatography instruments and consumables is likely to grow at a CAGR of 6.53% over the next decade.

- The projected opportunity is anticipated to be well distributed across different segments; prepacked columns segment is likely to grow at a faster pace during the forecasted period.

- Driven by the rapid technological advancements within chromatography instruments and consumables by prominent players in the US, the chromatography market is expected to grow at CAGR of 5.70%.

Chromatography Market

The market sizing and opportunity analysis has been segmented across the following parameters:

By Type of Chromatography Product

- Instruments

- Consumables

- Other Products

By Type of Chromatography Instrument

- Liquid Chromatography Instruments

- Gas Chromatography Instruments

- Other Chromatography Instruments

By Type of Liquid Chromatography

- High Performance Liquid Chromatography (HPLC)

- Ultra-high Performance Liquid Chromatography (UHPLC)

- Size-Exclusion Chromatography

- Flash Chromatography

- Other Techniques

By Type of Chromatography Component

- Stationary Phase

- Mobile Phase

By Format of Stationary Phase

- Prepacked Columns

- Bottles / Bulk Resins

- Other Formats

By End User

- Pharmaceutical and Biotechnology Industries

- Academic and Research Institutes

- Other End Users

By Geographical Regions

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and North Africa

Chromatography Market: Key Segments

Market Share Analysis by Type of Chromatography Product: Instruments Segment Dominates the Chromatography Market

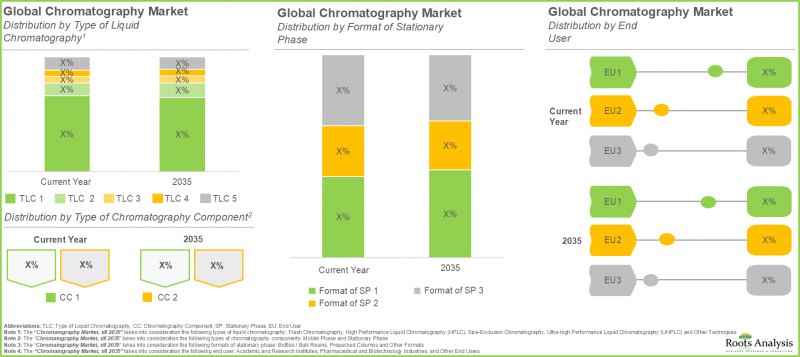

The global chromatography market is segmented into instruments, consumables, and other products. Currently, the instruments segment accounts for approximately 70% of the total market share, primarily driven by the extensive use of chromatography systems in the separation, purification, and identification of complex mixtures. This dominance is further supported by continuous advancements in analytical research and the growing demand for high-performance instrumentation capable of delivering both qualitative and quantitative insights.

Market Share by Type of Chromatography Instrument: Liquid Chromatography Leads the Market

Liquid chromatography instruments account for over 65% of the total market share. This dominance is driven by their effectiveness in separating complex mixtures, particularly polar and thermolabile compounds that are not easily analyzed using alternative methods such as gas chromatography. Meanwhile, the gas chromatography segment is anticipated to grow at a comparatively higher CAGR of 7.6% during the forecast period, driven by its cost-efficiency and ease of operation.

Market Share by Type of Liquid Chromatography: UHPLC to Exhibit Strong Growth

Within the liquid chromatography segment, the market comprises high-performance liquid chromatography (HPLC), ultra-high-performance liquid chromatography (UHPLC), size-exclusion chromatography, flash chromatography, and other techniques. Among these, HPLC holds the largest market share at approximately 66%, largely due to its critical role in pharmaceutical and biotechnology applications where high accuracy and regulatory compliance are essential. However, the UHPLC segment is expected to grow at a relatively higher CAGR of 7.3%, supported by its advantages in delivering faster analysis, enhanced resolution, and improved sensitivity compared to conventional chromatography techniques.

Market Share by Chromatography Component: Stationary Phase Segment Leads the Chromatography Market

Based on component type, the chromatography consumables market is categorized into stationary phase and mobile phase. The stationary phase segment currently dominates the market with a share of approximately 60%, owing to its pivotal role in achieving efficient analyte separation and purification. Additional contributing factors include high resolution, selective interactions, and cost-effectiveness. The mobile phase segment, however, is projected to grow at a higher CAGR of 8.7%, driven by innovations in solvent formulations and increasing integration with advanced hyphenated techniques such as LC-MS and GC-MS.

Market Share by Stationary Phase Format: Prepacked Columns at the Lead the Chromatography Market

Prepacked columns currently account for around 40% of the market share and are expected to grow at a CAGR of 8.0% over the forecast period. Their adoption is driven by operational efficiency, as they eliminate the need for manual column packing, thereby reducing preparation time and enhancing overall productivity in chromatographic workflows.

Market Share by End User: Pharmaceutical and Biotechnology Sectors Lead the Chromatography Market

The pharmaceutical and biotechnology industries dominate the end-user segment, contributing approximately 75% of the overall market share. This is primarily due to the critical role of chromatography in the separation, identification, and purification of biomolecules and chemical entities within these sectors.

Market Share by Geography: Asia-Pacific to Grow at a higher CAGR

North America is projected to maintain its leading position in the chromatography market, accounting for approximately 40% of the total share in the current year, with sustained dominance anticipated in the foreseeable future. This leadership is driven by the strong presence of key industry players in the United States, along with rapid adoption of advanced technologies, including AI-enabled and miniaturized chromatography systems. In contrast, the Asia-Pacific region is expected to register the highest growth rate, with a projected CAGR of 6.8% during the forecast period. This growth is supported by the availability of cost-effective chromatography solutions and favorable government initiatives aimed at promoting innovation in analytical technologies within the life sciences sector.

Example Players in Chromatography Market

- Agilent Technologies

- Bio-Rad Laboratories

- Gilson

- JASCO

- MilliporeSigma

- Revvity (Previously known as PerkinElmer)

- Sartorius

- Shimadzu Scientific Instruments

- Thermo Fisher Scientific

Chromatography Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the medical device contract manufacturing market, focusing on key market segments, including [A] type of chromatography [B] type of chromatography instrument, [C] type of liquid chromatography, [D] type of chromatography component, [E] format of stationary phase, [F] end user, and [G] geographical regions.

- Chromatography Instruments Providers Market Landscape: A detailed assessment of the overall chromatography instruments providers market landscape, along with information on several relevant parameters, such as [A] chromatography instruments offered, [B] type of chromatography consumables offered, [C] application area, [D] company size, [E] year of establishment and [F] location of headquarters.

- Company Competitiveness Analysis: An in-depth company competitiveness analysis of chromatography consumable and chromatography instrument providers based on various relevant parameters, such as [A] company strength, and [B] portfolio strength.

- Chromatography Consumables Providers Market Landscape: A detailed assessment of the overall chromatography consumables providers market landscape, along with information on several relevant parameters, such as [A] type of separation technique offered, [B] type of solid phase offered, [C] type of analyte, [D] company size, [E] year of establishment and [F] location of headquarters.

- Company Profiles: In-depth profiles of key companies based in North America, Europe and Asia-Pacific based on several parameters such as [A] year of establishment, [B] location of headquarters, [C] product portfolio, [D] recent developments and [E] an informed future outlook.

- Patent Analysis: A detailed analysis of the patents that have been filed / granted based on important parameters such as, [A] type of patent, [B] publication year, [C] application year, [D] number of granted patents and patent applications, [E] patent jurisdiction, [F] CPC symbols, [G] patent age, [H] type of applicant, and [I] individual patent assignees (in terms of size of intellectual property portfolio).

- Mergers and Acquisitions: A detailed analysis of various mergers and acquisitions of chromatography companies, based on several relevant parameters, such as [A] year of agreement, [B] type of agreement, [C] geography, [D] most active players, [E] ownership change matrix and [F] key value drivers and [G] deal multiples (based on revenues).

- Market Impact Analysis: An in-depth analysis of the factors that can impact the growth of the market. It also features identification and analysis of key drivers, potential restraints, emerging opportunities, and existing challenges in this domain.

Key Questions Answered in this Report

- Which are the leading companies in the chromatography market?

- Which region dominates the chromatography market?

- What are the key trends observed in the chromatography market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by chromatography instrument and consumable providers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Additional Benefits

- Complementary PPT Insights Pack

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Project Objectives

- 1.3. Scope of the Report

- 1.4. Inclusions and Exclusions

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Developers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. EXECUTIVE SUMMARY

5. INTRODUCTION

- 5.1. Chapter Overview

- 5.2. Overview of Chromatography

- 5.3. Principle of Chromatography

- 5.4. Types of Chromatography

- 5.5. Applications of Chromatography

- 5.6. Future Perspectives

- 5.7. Concluding Remarks

6. CHROMATOGRAPHY INSTRUMENTS PROVIDERS MARKET LANDSCAPE

- 6.1. Chapter Overview

- 6.2. Chromatography Instrument Providers: Overall Market Landscape

- 6.2.1. Analysis by Year of Establishment

- 6.2.2. Analysis by Company Size

- 6.2.3. Analysis by Location of Headquarters

- 6.2.4. Analysis by Company Size and Location of Headquarters

- 6.2.5. Analysis by Chromatography Instrument Offered

- 6.2.6. Analysis by Type of Mobile Phase Used

- 6.2.7. Analysis by Type of Chromatography Consumables Offered

- 6.2.8. Analysis by Scale of Operation

- 6.2.9. Analysis by Type of Industry Served

7. CHROMATOGRAPHY INSTRUMENTS PROVIDERS: COMPANY COMPETITIVENESS ANALYSIS

- 7.1. Chapter Overview

- 7.2. Assumptions and Key Parameters

- 7.3. Methodology

- 7.4. Chromatography Instrument Providers: Company Competitiveness Analysis

- 7.4.1. Small Companies Providing Chromatography Instruments

- 7.4.2. Mid-sized Companies Providing Chromatography Instruments

- 7.4.3. Large Companies Providing Chromatography Instruments

- 7.4.4. Very Large Companies Providing Chromatography Instruments

8. CHROMATOGRAPHY CONSUMABLES PROVIDERS MARKET LANDSCAPE

- 8.1. Chapter Overview

- 8.2. Chromatography Consumables Providers: Overall Market Landscape

- 8.2.1. Analysis by Year of Establishment

- 8.2.2. Analysis by Company Size

- 8.2.3. Analysis by Location of Headquarters

- 8.2.4. Analysis by Company Size and Location of Headquarters

- 8.2.5. Analysis by Type of Separation Technique Used

- 8.2.6. Analysis by Type of Solid Phase Offered

- 8.2.7. Analysis by Type of Consumable Format Offered

- 8.2.8. Analysis by Type of Analyte

- 8.2.9. Analysis by Application Area of Chromatography Consumables

9. COMPANY PROFILES

- 9.1. Chapter Overview

- 9.2. Agilent Technologies

- 9.2.1. Company Overview

- 9.2.2. Chromatography Product Portfolio

- 9.2.3. Recent Developments and Future Outlook

- 9.3. Bio-Rad Laboratories

- 9.3.1. Company Overview

- 9.3.2. Chromatography Product Portfolio

- 9.3.3. Recent Developments and Future Outlook

- 9.4. PerkinElmer

- 9.4.1. Company Overview

- 9.4.2. Chromatography Product Portfolio

- 9.4.3. Recent Developments and Future Outlook

- 9.5. Sartorius

- 9.5.1. Company Overview

- 9.5.2. Chromatography Product Portfolio

- 9.5.3. Recent Developments and Future Outlook

- 9.6. Shimadzu

- 9.6.1. Company Overview

- 9.6.2. Chromatography Product Portfolio

- 9.6.3. Recent Developments and Future Outlook

- 9.7. Thermo Fisher Scientific

- 9.7.1. Company Overview

- 9.7.2. Chromatography Product Portfolio

- 9.7.3. Recent Developments and Future Outlook

10. PATENT ANALYSIS

- 10.1. Chapter Overview

- 10.2. Scope and Methodology

- 10.3. Chromatography Instruments and Consumables: Patent Analysis

- 10.3.1. Analysis by Patent Publication Year

- 10.3.2. Analysis by Patent Application Year

- 10.3.3. Analysis of Granted Patents and Patent Applications by Publication Year

- 10.3.4. Analysis by Patent Jurisdiction

- 10.3.5. Analysis by CPC Symbols

- 10.3.6. Analysis by Type of Applicant

- 10.3.7. Leading Industry Players: Analysis by Number of Patents

- 10.3.8. Leading Non-Industry Players: Analysis by Number of Patents

- 10.3.9. Leading Individual Patent Assignees: Analysis by Number of Patents

- 10.4. Chromatography Instruments and Consumables: Patent Benchmarking Analysis

- 10.4.1. Analysis by Patent Characteristics

- 10.5. Chromatography Instruments and Consumables: Patent Valuation

- 10.6. Leading Patents by Number of Citations

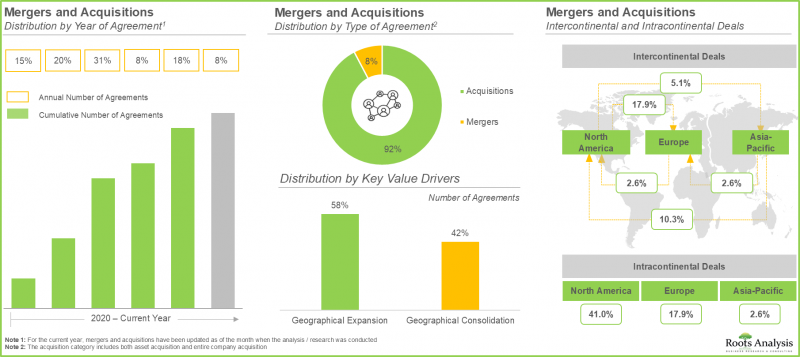

11. MERGERS AND ACQUISITIONS

- 11.1. Chapter Overview

- 11.2. Merger and Acquisition Models

- 11.3. Chromatography Instruments and Consumables: Mergers and Acquisitions

- 11.3.1. Analysis by Type of Deal

- 11.3.2. Analysis by Year of Deal

- 11.3.3. Analysis by Company Ownership

- 11.3.4. Analysis by Geography

- 11.3.4.1. Intercontinental and Intracontinental Deals

- 11.3.4.2. Local and International Deals

- 11.3.5. Most Active Players: Analysis by Number of Mergers and Acquisitions

- 11.3.6. Analysis by Key Value Drivers

- 11.3.7. Key Acquisitions: Deal Multiples

12. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 12.1. Chapter Overview

- 12.2. Market Drivers

- 12.3. Market Restraints

- 12.4. Market Opportunities

- 12.5. Market Challenges

- 12.6. Conclusion

13. GLOBAL CHROMATOGRAPHY MARKET

- 13.1. Chapter Overview

- 13.2. Assumptions and Methodology

- 13.3. Global Chromatography Market, Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 13.3.1. Scenario Analysis

- 13.4. Key Market Segmentations

- 13.5. Dynamic Dashboard

14. CHROMATOGRAPHY MARKET: DISTRIBUTION BY TYPE OF PRODUCT

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Chromatography Instruments: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 14.4. Chromatography Consumables: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 14.5. Other Accessories: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 14.6. Data Triangulation

- 14.6.1. Insights from Primary Research

- 14.6.2. Insights from Secondary Research

- 14.6.3. Insights from In-house Repository

15. CHROMATOGRAPHY MARKET: DISTRIBUTION BY TYPE OF CHROMATOGRAPHY INSTRUMENT

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Liquid Chromatography Instrument: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 15.4. Gas Chromatography Instrument: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 15.5. Other Instruments: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 15.6. Data Triangulation

- 15.6.1. Insights based on Primary Research

- 15.6.2. Insights based on Secondary Research

- 15.6.3. Insights from In-house Repository

16. CHROMATOGRAPHY MARKET: DISTRIBUTION BY TYPE OF CONSUMABLE FORMAT OFFERED

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Pre-Packed Columns: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 16.4. Bottles / Bulk Resins: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 16.5. Other Formats: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 16.6. Data Triangulation

- 16.6.1. Insights based on Primary Research

- 16.6.2. Insights based on Secondary Research

- 16.6.3. Insights from In-house Repository

17. CHROMATOGRAPHY MARKET: DISTRIBUTION BY END USER

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Pharmaceutical and Biopharmaceutical Companies: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 17.4. Academic / Research Institutes: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 17.5. Other Industries: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 17.6. Data Triangulation

- 17.6.1. Insights based on Primary Research

- 17.6.2. Insights based on Secondary Research

- 17.6.3. Insights from In-house Repository

18. CHROMATOGRAPHY MARKET: DISTRIBUTION BY GEOGRAPHY

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. North America: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 18.3.1. Chromatography Market for Chromatography Instruments

- 18.3.2. Chromatography Market for Chromatography Consumables

- 18.3.3. Chromatography Market for Other Accessories

- 18.4. Europe: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 18.4.1. Chromatography Market for Chromatography Instruments

- 18.4.2. Chromatography Market for Chromatography Consumables

- 18.4.3. Chromatography Market for Other Accessories

- 18.5. Asia-Pacific: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 18.5.1. Chromatography Market for Chromatography Instruments

- 18.5.2. Chromatography Market for Chromatography Consumables

- 18.5.3. Chromatography Market for Other Accessories

- 18.6. Rest of the World: Historical Trends (Since 2017) and Future Estimates (Till 2035)

- 18.6.1. Chromatography Market for Chromatography Instruments

- 18.6.2. Chromatography Market for Chromatography Consumables

- 18.6.3. Chromatography Market for Other Accessories

- 18.7. Data Triangulation

- 18.7.1. Insights based on Primary Research

- 18.7.2. Insights based on Secondary Research

- 18.7.3. Insights from In-house Repository