|

시장보고서

상품코드

2072252

액체 생검 시장(제5판) : 기술별, 검체별, 순환 바이오마커별, 암종별, 용도별, 최종사용자별, 지역별 - 동향과 세계 예측(2026-2035년)Liquid Biopsy Market (5th Edition) by Type of Technology, Type of Sample, Type of Circulating Biomarker, Type of Cancer, Application, End-user and Geographical Regions - Trends and Global Forecasts, 2026-2035 |

||||||

액체 생검 시장 : 개요

Roots Analysis의 조사에 따르면, 액체 생검 시장 규모는 현시점 94억 9,000만 달러에서 2035년에는 334억 5,000만 달러로 성장할 것으로 추정되며, 2035년까지 예측 기간 동안 CAGR은 15.0%를 기록할 전망입니다.

액체 생검 시장 : 성장 및 동향

조직 생검은 오랫동안 전문가들로부터 암 진단의 ‘골드 스탠다드’로 여겨져 왔습니다. 그러나 환자의 불편감이나 통증, 합병증 위험 등 이 침습적 시술에 내재된 한계로 인해 그 보급은 제한되어 왔습니다. 이에 따라 지속적인 연구와 기술의 발전으로, 암 검출을 위한 신뢰할 수 있는 대안으로서 액체 생검이 등장했습니다.

액체 생검 기술은 암의 조기 발견 및 병세 모니터링에 있어, 비침습적이면서도 활용하기 쉬운 접근 방식을 제공합니다. 이러한 검사법에서는 혈액 검체나 소변, 혈장 등의 체액을 분석하여 유전자 변이 및 순환 종양 DNA(ctDNA), 무세포 DNA(cfDNA), 세포외 소포 등의 순환 바이오마커를 검출합니다. 그 결과, 이러한 비침습적 진단 솔루션은 특히 진행성 암 환자들에게서 암 치료를 점점 더 혁신하고 있습니다.

액체 생검 시장은 수많은 업계 관계자들의 연구 개발에 대한 막대한 투자의 뒷받침을 받아 강력한 성장을 이루고 있으며, 여전히 매우 역동적인 상황을 보이고 있습니다. 이러한 투자는 지속적인 과학적 진보를 활용하고 있으며, 액체 생검을 종양 진단 분야의 혁신 최전선에 위치시키고 있습니다. 이 분야의 발전이 지속되는 가운데, 액체 생검 및 기타 비침습적 진단 기술의 도입이 크게 확대될 것으로 예상되며, 이는 예측 기간 동안 시장 성장을 견인할 것으로 전망됩니다.

성장 요인 : 시장 확대를 전략적으로 촉진하는 요인

기술의 발전은 액체 생검의 임상적 유용성을 높이는 데 있어 매우 중요한 역할을 해왔습니다. 차세대 염기서열 분석(NGS) 및 디지털 PCR 기술의 획기적인 발전으로 인해, 이러한 검사의 민감도와 특이도가 크게 향상되어 극히 낮은 농도의 순환 종양 DNA(ctDNA) 및 순환종양세포(CTC)를 검출할 수 있게 되었습니다. 그 결과, 임상의들은 기존의 고형 조직 생검에 의존하지 않고도, 이전에는 검출할 수 없었던 치료에 활용할 수 있는 유전체 변이를 특정할 수 있게 되었습니다.

또한, AI와 첨단 생물정보학 도구의 통합을 통해 복잡한 액체 생검 데이터의 해석은 더욱 큰 변화를 맞이했습니다. 기계 학습 알고리즘은 신호 대 잡음 비율을 개선하여 유전적 및 후성유전적 패턴을 보다 정확하게 식별할 수 있게 해줍니다. 이 계산기를 통한 지원은 위양성 가능성을 낮출 뿐만 아니라, 임상적 의사결정을 신속하게 하고 전반적인 진단 효율을 향상시킵니다. 또한, 치료 과정에 대한 실시간 모니터링에 대한 수요가 증가함에 따라 종양 치료 현장에서 액체 생검의 도입이 가속화되고 있습니다. 액체 생검은 질환의 동적인 유전체 상태를 파악할 수 있기 때문에 종양 전문의는 치료 반응을 추적하고 새롭게 발생하고 있는 내성 변이를 조기에 탐지할 수 있게 됩니다. 이를 통해 치료 전략을 적시에 조정할 수 있으며, 궁극적으로는 환자의 예후 개선에 기여하게 됩니다.

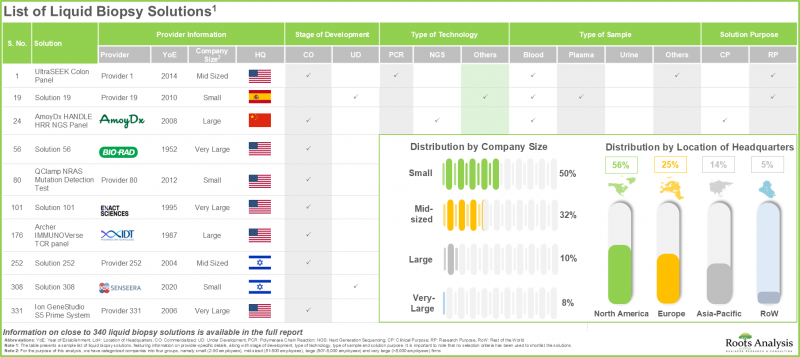

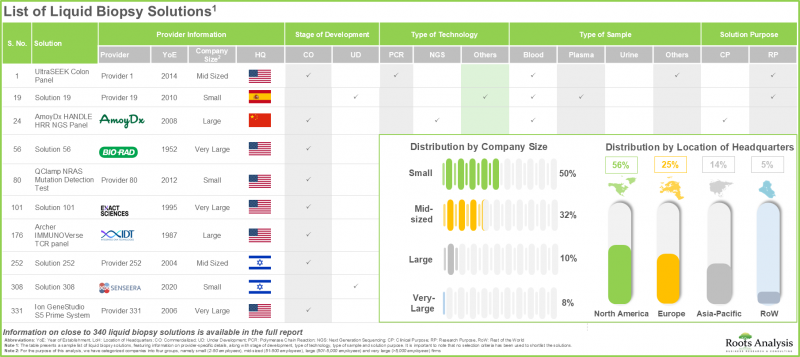

- 전 세계적으로 증가하는 암 조기 발견 솔루션에 대한 수요에 부응하기 위해 다양한 이해관계자들에 의해 340건에 가까운 액체 생검 솔루션이 이미 상용화되었거나 개발이 진행 중입니다.

- 액체 생검 솔루션의 약 90%는 어세이 키트로 구성되어 있으며, 그중 약 35%는 각종 암 검출에 중합효소 연쇄 반응(PCR) 기술을 채택하고 있습니다.

- 제휴 계약 건수가 가장 많았던 곳은 북미에 거점을 둔 기업이었으며, 특히 계약의 65% 이상이 같은 대륙 내 거래였고, 그 다음으로 대륙 간 거래(약 35%)가 뒤를 이었습니다.

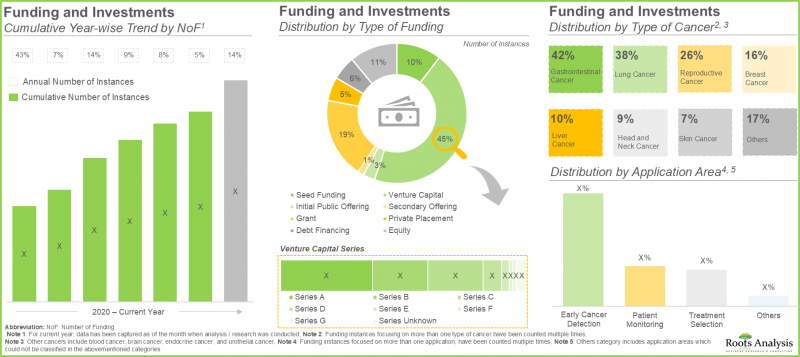

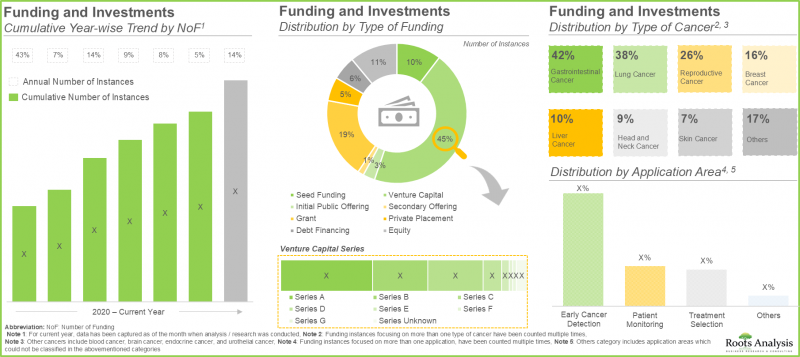

- 최근 몇 년간 자금 조달 활동 전체는 연평균 성장률(CAGR) 13.8%로 증가했으며, 그 대부분(45%)은 벤처 캐피털에 의한 것이었습니다.

- 몇몇 대형 제약사들이 액체 생검 솔루션 제공업체와의 제휴 및 이 업계에 대한 투자를 통해 이 분야에서 입지를 다지고 있습니다.

- 본 보고서에서는 액체 생검 분야의 약 100개 기업을 분석했습니다. 그 중 약 60%의 기업이 잠재적인 인수 대상으로 선정되었습니다.

- 암 치료 솔루션에 대한 수요 증가, 기술 발전, 지원적인 규제 체계를 고려할 때, 해당 시장은 당분간 꾸준한 성장을 이룰 것으로 예상됩니다.

- 액체 생검 시장은 2035년까지 연평균 성장률(CAGR) 15.0%로 성장할 것으로 전망됩니다. 특히, 차세대 염기서열 분석은 2035년까지 시장 점유율의 대부분을 차지할 것으로 예상됩니다.

- 북미의 액체 생검 시장은 2035년까지 가장 큰 점유율을 차지할 것으로 예상됩니다. 또한, 액체 생검 솔루션의 대부분은 암의 조기 진단을 목적으로 하고 있습니다.

- 다양한 종양성 질환에 대한 액체 생검 제품의 승인이 잇따르고 있는 가운데, 향후 몇 년 동안 시장은 상당한 성장을 이룰 것으로 전망됩니다.

본 보고서에서는 전 세계 액체 생검 시장을 조사하여, 시장 및 대상 질환에 대한 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 시장 규모 추정 및 전망, 각종 분류 및 지역별 상세 분석, 기술 및 제품 동향, 사례 연구, 자금 조달 동향, 경쟁 구도, 주요 기업 개요 등을 정리하고 있습니다.

목차

제1장 서문

제2장 조사 방법

제3장 경제적 및 기타 프로젝트 고유의 고려사항

제4장 거시경제 지표

제5장 주요 요약

제6장 소개

제7장 사례 연구 : 비침습적 암 검진 및 진단

제8장 시장 구도

제9장 제품 경쟁력

제10장 기업 개요 : 액체 생검 솔루션 프로바이더

제11장 파트너십과 협력 관계

제12장 자금 조달과 투자

제13장 대형 제약회사의 대처

제14장 주요 인수 대상

제15장 사례 연구 : 기타 비침습적 암 진단

제16장 시장 영향 분석

제17장 세계의 액체 생검 시장

제18장 액체 생검 시장 : 기술 유형별

제19장 액체 생검 시장 : 검체 유형별

제20장 액체 생검 시장 : 순환 바이오마커 유형별

제21장 액체 생검 시장 : 암 유형별

제22장 액체 생검 시장 : 응용 분야별

제23장 액체 생검 시장 : 최종사용자별

제24장 액체 생검 시장 : 지역별

제25장 결론

제26장 경영진 인사이트

제27장 부록 1 : 표형식 데이터

제28장 부록 2 : 기업 및 조직 리스트

KSM 26.07.03Liquid Biopsy Market: Overview

As per Roots Analysis, the liquid biopsy market is estimated to grow from USD 9.49 billion in the current year to USD 33.45 billion by 2035, at a CAGR of 15.0% during the forecast period, till 2035.

Liquid Biopsy Market: Growth and Trends

Tissue biopsy has long been regarded by experts as the gold standard for cancer diagnosis. However, the inherent limitations of this invasive procedure, including patient discomfort, pain, and the risk of complications have constrained its broader acceptance. In response, ongoing research and technological advancements have led to the emergence of liquid biopsy as a credible alternative for cancer detection.

Liquid biopsy technologies provide a minimally invasive and highly accessible approach to early cancer detection and disease monitoring. These assays analyze blood samples or other bodily fluids, such as urine or plasma, to detect genetic alterations and circulating biomarkers, including circulating tumor DNA (ctDNA), cell-free DNA (cfDNA), and extracellular vesicles. As a result, these non-invasive diagnostic solutions are increasingly transforming cancer care, particularly for patients with advanced-stage disease.

The liquid biopsy market is experiencing robust growth and remains highly dynamic, driven by significant investments in research and development by numerous industry players. These investments are leveraging ongoing scientific advancements, positioning liquid biopsy at the forefront of innovation in oncology diagnostics. With continued progress in this field, the adoption of liquid biopsy and other non-invasive diagnostic technologies is expected to expand substantially, thereby driving market growth over the forecast period.

Growth Drivers: Strategic Enablers of Market Expansion

Technological advancements have played a pivotal role in strengthening the clinical utility of liquid biopsy. Breakthroughs in next-generation sequencing (NGS) and digital PCR technologies have significantly enhanced the sensitivity and specificity of these assays, enabling the detection of extremely low concentrations of circulating tumor DNA (ctDNA) and circulating tumor cells (CTCs). As a result, clinicians can now identify actionable genomic alterations that were previously undetectable without relying on traditional solid tissue biopsies.

In addition, the integration of artificial intelligence (AI) and advanced bioinformatics tools has further transformed the interpretation of complex liquid biopsy data. Machine learning algorithms improve the signal-to-noise ratio, facilitating more precise identification of genetic and epigenetic patterns. This computational support not only reduces the likelihood of false positives but also accelerates clinical decision-making, enhancing overall diagnostic efficiency. Further, the growing demand for real-time treatment monitoring is reinforcing the adoption of liquid biopsy in oncology practice. By providing a dynamic genomic snapshot of the disease, liquid biopsy enables oncologists to track therapeutic response and detect emerging resistance mutations at an early stage. This allows for timely adjustments to treatment strategies, ultimately contributing to improved patient outcomes.

Market Challenges: Critical Barriers Impeding Progress

Despite significant progress in liquid biopsy technologies, several challenges continue to impede broader market adoption. One of the primary constraints is the substantial capital investment required for research and development. The high costs associated with advancing and validating novel diagnostic solutions often limit participation by smaller companies and can delay the commercialization of innovative technologies.

In addition to financial barriers, complexities related to data integration and interpretation present ongoing challenges. The large volumes of data generated through next-generation sequencing (NGS) necessitate robust bioinformatics infrastructure and expertise. Furthermore, the absence of standardized protocols for data analysis and clinical interpretation of genetic variants can result in inconsistencies in reporting. These limitations collectively hinder the seamless integration of liquid biopsy into routine clinical practice and slow its widespread adoption.

Liquid Biopsy Market: Key Insights

The report delves into the current state of the liquid biopsy market and identifies potential growth opportunities within industry. Some key findings from the report include:

- Close to 340 liquid biopsy solutions are either commercialized or being developed by various stakeholders in order to cater to the rising demand for early cancer detection solutions, across the globe.

- Around 90% of liquid biopsy solutions comprise of assay kits; of these, ~35% have employed polymerase chain reaction technique for the detection of various cancer indications.

- The maximum number of collaborations were signed by the players based in North America; notably, more than 65% of the agreements were intracontinental deals, followed by intercontinental deals (~35%).

- Over the years, the overall funding activity has increased at a CAGR of 13.8%; majority (45%) of the instances were related to venture capital.

- Several big pharmaceutical companies have marked their presence in this domain by either collaborating with liquid biopsy solution providers or by investing in this industry.

- We have analyzed close to 100 companies in liquid biopsy domain; of these, nearly 60% of the companies were identified as potential acquisition targets.

- Given the increasing demand for cancer solutions, technological advancements and supportive regulatory frameworks, the market is expected to witness a steady growth in the foreseen future.

- The liquid biopsy market is likely to grow at an annualized rate (CAGR) of 15.0%, till 2035; notably, the next generation sequencing is anticipated to capture the majority share in the market by 2035.

- The liquid biopsy market in North America is expected to capture maximum share by 2035; further, majority of the liquid biopsy solutions are intended for early diagnosis of cancer.

- Driven by ongoing approvals of liquid biopsy products for various oncological disorders, the market is likely to experience notable growth in the coming years.

Liquid Biopsy Market

The market sizing and opportunity analysis has been segmented across the following parameters:

By Type of Technology

- Next-Generation Sequencing

- Polymerase Chain Reaction

By Type of Sample

- Blood

- Other Samples

By Type of Circulating Biomarker

- Circulating Tumor DNA

- Cell Free DNA

- Cell Free RNA

- Exosomes

- Other Circulating Biomarkers

By Type of Cancer

- Breast Cancer

- Colorectal Cancer

- Prostate cancer

- Lung Cancer

- Bladder Cancer

- Melanoma

- Thyroid Cancer

- Gastric Cancer

- Head and Neck Cancer

- Leukemia

- Brain Cancer

- Liver Cancer

- Cervical Cancer

- Ovarian Cancer

- Oesophagus Cancer

- Pancreatic Cancer

- Nasopharyngeal cancer

- Sarcoma

By Application Area

- Early Diagnosis

- Patient Monitoring

- Recurrence Monitoring

By End-user

- Hospitals / Laboratories

- Research Institutes

- Other End-users

By Geographical Regions

- North America

- US

- Europe

- France

- UK

- Germany

- Italy

- Spain

- Asia-Pacific

- China

- India

- Japan

- Australia

Liquid Biopsy Market: Key Segments

Which Type of Technology Accounts for the Largest Share in the Liquid Biopsy Market?

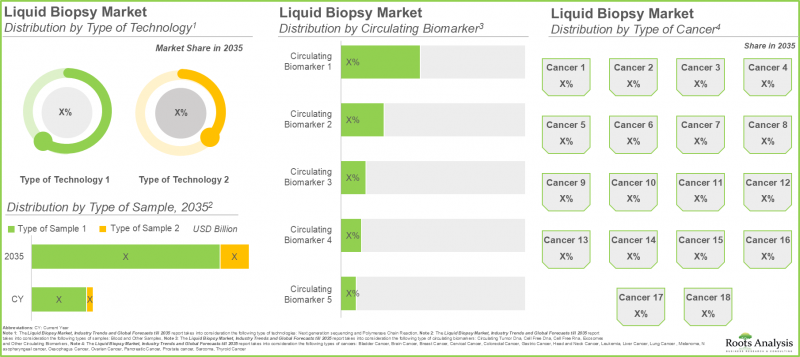

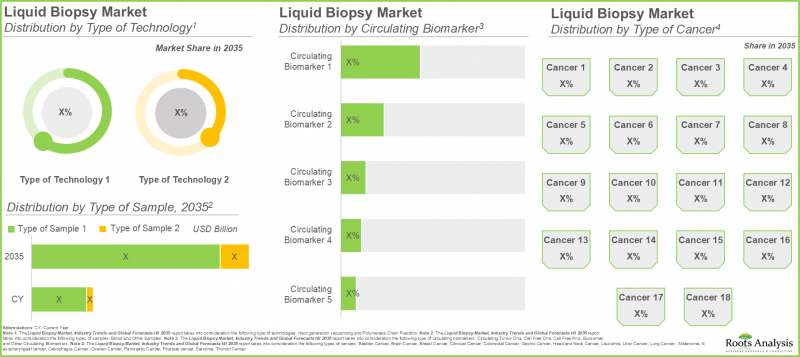

Based on the type of technology, the next-generation sequencing (NGS) segment is expected to account for approximately 53% of the total market share in the current year. This dominance is driven by its superior capability for high-throughput, multi-gene profiling, continued reductions in sequencing costs, and enhanced sensitivity in detecting rare genetic mutations, making it highly suitable for precision oncology applications. Furthermore, NGS is projected to witness robust growth at a CAGR of 17.1%, supported by the increasing demand for advanced, high-throughput diagnostic solutions in clinical oncology.

Regional Analysis: Fastest Growing Region in Liquid Biopsy Testing Domain

North America: Dominating the Market by Securing Highest Share

Regionally, North America is anticipated to maintain its leadership position, capturing nearly 55% of the global liquid biopsy market revenue in 2026. This can be attributed to the presence of a well-established pharmaceutical and biotechnology ecosystem, strong regulatory frameworks, and a high concentration of key liquid biopsy solution providers, all of which collectively drive market expansion in the region.

Which Type of Sample Accounts for the Largest Share in the Liquid Biopsy Market?

In terms of sample type, blood-based assays dominate the market, contributing approximately 89.5% of the total revenue. This is largely due to their minimally invasive nature and the widespread availability of established clinical infrastructure for blood-based biomarker analysis.

Which Type of Circulating Biomarker Accounts for the Largest Share in the Liquid Biopsy Market?

With respect to circulating biomarkers, circulating tumor DNA (ctDNA) currently holds the largest share, accounting for 44.8% of the market. Its ability to provide real-time insights into tumor dynamics throughout the patient care continuum underpins its widespread adoption. Looking ahead, the exosomes segment is expected to grow at a faster rate, with a projected CAGR of 16.5%, driven by their capacity to transport diverse molecular components and their enhanced stability across various body fluids.

Which Type of Cancer Accounts for the Largest Share in the Liquid Biopsy Market?

Based on the type of cancer, the breast cancer segment is projected to hold the largest market share at 28.8% in 2026. This is primarily due to the increasing global prevalence of breast cancer and the growing adoption of non-invasive diagnostic approaches for early detection and treatment monitoring. Additionally, nasopharyngeal cancer is anticipated to experience comparatively faster growth, supported by the high predictive value of plasma Epstein-Barr virus (EBV) DNA in monitoring treatment response and detecting minimal residual disease.

Which Application Area Accounts for the Largest Share in the Liquid Biopsy Market?

In terms of application, early diagnosis represents the largest segment, accounting for approximately 67.3% of the total market revenue. This is driven by an increasing emphasis on early cancer detection to improve clinical outcomes and reduce overall treatment costs. The segment is also expected to witness accelerated growth in the coming years, as early diagnostic capabilities enable timely interventions, improve survival rates, and facilitate personalized treatment strategies.

Which End-user Accounts for the Largest Share in the Liquid Biopsy Market?

Hospitals and laboratories constitute the leading end-user segment, capturing 75.4% of the overall market share. Their dominance is attributed to high testing volumes, availability of skilled personnel, and seamless integration with existing diagnostic workflows. This segment is also projected to grow at a steady pace, supported by ongoing investments in advanced diagnostic technologies and a rising patient population seeking comprehensive cancer screening services.

Example Players in Liquid Biopsy Market

- Amoy Diagnostics

- Biocartis

- DiaCarta

- Exact Sciences

- Gencurix

- GeneCast Biotechnology

- Integrated DNA Technologies

- Lucence

- MedGenome

- Medicover Genetics

- nRICH dx

- Precipio

- QIAGEN

- RGCC Group

- Screen Cell

- Singlera Genomics

- Thermo Fisher Scientific

Primary Research Overview

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders. The research report features detailed transcripts of interviews held with the following industry stakeholders:

- Director, Mid-sized Company, US

- Innovation Director, Mid-sized Company, Spain

- Founder and Chief Executive officer, Small-sized Company, India

- Founder, President and Chief Technology Officer, Small-sized Company, US

- Former Strategic Technology Advisor, Small-sized Company, Australia

- Founder and Medical Director, Small-sized Company, Germany

- Chief Executive officer, Small-sized Company, Australia

- Chief Operating Officer and Co-Founder, Small-sized Company, Canada

- Chief Medical Officer, Mid-sized Company, US

- Chairman, Small-sized Company, US

- Former Sales and Marketing Manager, Small-sized Company, Italy

- Former Marketing Director, Mid-sized Company, Belgium

- Former Founder, Small-sized Company, US

- Former Chief Executive Officer, Mid-sized Company, US

- Founder, Small-sized Company, Sweden

- Former Chief Executive Officer and Co-founder, Small-sized Company, US

- Chief Scientific Officer, Mid-sized Company, US

Liquid Biopsy Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the liquid biopsy market, focusing on key market segments, including [A] type of technology, [B] type of sample, [C] type of circulating biomarker, [D] type of cancer, [E] application, [F] end-user, and [G] geographical regions.

- Market Landscape: A comprehensive evaluation of liquid biopsy products, considering various parameters, such as [A] stage of development, [B] type of product, [C] type of sample, [D] type of technique, [E] type of circulating biomarker, [F] target disease indication, [G] and [H] application area. In addition, it provides a list of players engaged in manufacturing liquid biopsy products, along with the information on their [I] year of establishment, [J] company size (based on number of employees), [K] location of headquarters (region), [L] location of headquarters (country), [M] most active players (in terms of number of liquid biopsy products).

- Non-Invasive Cancer Screening and Diagnosis: An overview on the need for non-invasive cancer diagnostics and their importance; it also features different imaging techniques, screening assays and advanced approaches used for diagnosis of cancer along with their advantages and disadvantages.

- Company Profiles: In-depth profiles of key industry players manufacturing liquid biopsy products, focusing on [A] company overviews, [B] financial information (if available), [C] product portfolio, [D] recent developments and [E] an informed future outlook.

- Partnerships and Collaborations: An analysis of partnerships established in this sector, since 2020, based on several parameters, such as [A] year of partnership, [B] type of partnership, [C] type of partner, [D] type of circulating biomarker, [E] target disease indication, [F] most active players. This section also highlights the regional distribution of partnership activity in this market.

- Funding and Investment Analysis: A detailed evaluation of the investments made in the liquid biopsy domain, encompassing seed financing, venture capital, capital raised from IPOs, secondary offerings, grants / awards, other equity and debt financing, based on several parameters, such as [A] year of investment, [B] amount invested, [C] type of funding, [D] type of circulating biomarker, [E] target disease indication, [F] application area, [G] geography, [H] most active players (in terms of number of funding instances and amount invested) and [I] leading investors (in terms of number of funding instances).

- Product Competitiveness Analysis: A comprehensive competitive analysis of liquid biopsy products, examining factors, such as [A] supplier strength, [B] product competitiveness and [C] company size.

- Big Pharma Analysis: A comprehensive examination of various initiatives focused on liquid biopsy products undertaken by major pharmaceutical companies. This analysis covers various relevant parameters, such as [A] number of initiatives, [B] type of initiative, [C] stage of development, [D] type of product, [E] type of circulating biomarker, [F] target disease indication, and [G] application area.

- Key Acquisition Targets: A detailed analysis of the key acquisition targets, taking into consideration the historical trend of the acquisition activity of the players that have acquired other firms. It offers a means for other industry stakeholders to identify potential acquisition targets.

- Other Non-Invasive Cancer Diagnostics: A detailed overview of the various non invasive diagnostic tests other than liquid biopsies, being manufactured by various companies for cancer screening and early detection.

- Market Impact Analysis: The report analyzes various factors such as drivers, restraints, opportunities, and challenges affecting the market growth.

Key Questions Answered in this Report

- Which are the leading companies in the liquid biopsy market?

- Which region dominates the liquid biopsy market?

- What are the key trends observed in the liquid biopsy market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by liquid biopsy solution providers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1 PREFACE

- 1.1. Introduction

- 1.2. Report Coverage

- 1.3. Market Segmentation

- 1.4. Key Market Insights

- 1.5. Market Share Insights

- 1.6. Key Questions Answered

2 RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3 ECONOMIC AND OTHER PROJECT-SPECIFIC CONSIDERATIONS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4 MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Value and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

- 5.1. Liquid Biopsy Solutions: Market Landscape

- 5.2. Liquid Biopsy Solutions: Market Trends

- 5.3. Liquid Biopsy Solutions: Market Forecast and Opportunity Analysis

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Cancer Statistics and Burden of the Disease

- 6.3. Importance of Early Cancer Detection

- 6.4. Cancer Screening and Diagnosis

- 6.5. Conventional Invasive Cancer Diagnostic Tests

- 6.5.1. Biopsy

- 6.5.2. Fine Needle Aspiration Biopsy

- 6.5.3. Core Needle Aspiration Biopsy

- 6.5.4. Vacuum-Assisted Biopsy

- 6.5.5. Image Guided Biopsy

- 6.5.6. Sentinel Node Biopsy

- 6.5.7. Surgical Biopsy

- 6.5.8. Endoscopic Biopsy

- 6.5.9. Bone Marrow Biopsy

- 6.5.10. Endoscopy

- 6.6. Need for Non-Invasive Approaches

- 6.7. Liquid Biopsy: Diagnosing Circulating Biomarkers

- 6.7.1. Circulating Tumor Cells

- 6.7.2. Circulating Tumor DNA / Cell Free DNA

- 6.7.3. Exosomes

- 6.8. Costs and Benefits Associated with Liquid Biopsy and Non-Invasive Tests

- 6.9. Emerging Trends in Intellectual Property Related to Non-Invasive Cancer Diagnostics

- 6.10. Challenges Associated with Non-Invasive Cancer Diagnostics

- 6.11. Future Perspectives

7. CASE-STUDY: NON-INVASIVE CANCER SCREENING AND DIAGNOSIS

- 7.1. Chapter Overview

- 7.2. Diagnostic Imaging

- 7.2.1. Magnetic Resonance Imaging (MRI)

- 7.2.2. Mammography

- 7.2.3. Bone Scan

- 7.2.4. Computerized Tomography (CT) Scan

- 7.2.5. Integrated Positron Emission Tomography (PET)- CT Scan

- 7.2.6. Ultrasound

- 7.2.7. X-ray Radiography (Barium Enema)

- 7.3. Screening Assays

- 7.3.1. Circulating Tumor Marker Test

- 7.3.2. Digital Rectal Exam (DRE)

- 7.3.3. Fecal Occult Blood Test (FOBT)

- 7.3.4. Multigated Acquisition (MUGA) Scan

- 7.3.5. Papanicolaou Test and Human Papilloma Virus Test

- 7.4. Advanced Non-Invasive Approaches

- 7.4.1. Cytogenetic / Gene Expression Studies

- 7.4.2. Molecular Signature-based Non-Invasive Methods

- 7.4.3. Saliva-based Oral Cancer Diagnostics

- 7.4.4. Vital Staining

- 7.4.5. Optical Biopsy

- 7.4.6. Other Diagnostic Techniques

8. MARKET LANDSCAPE

- 8.1. Chapter Overview

- 8.2. Liquid Biopsy Solutions: Overall Market Landscape

- 8.2.1. Analysis by Stage of Development

- 8.2.2. Analysis by Type of Solution

- 8.2.3. Analysis by Type of Technology

- 8.2.4. Analysis by Type of Sample

- 8.2.5. Analysis by Type of Circulating Biomarker

- 8.2.6. Analysis by Type of Cancer

- 8.2.7. Analysis by Solution Purpose

- 8.2.8. Analysis by Application Area

- 8.3. Liquid Biopsy Market: Overall Developer Landscape

- 8.3.1. Analysis by Year of Establishment

- 8.3.2. Analysis by Company Size

- 8.3.3. Analysis by Location of Headquarters

- 8.3.4. Analysis by Most Active Players

9. PRODUCT COMPETITIVENESS ANALYSIS

- 9.1. Chapter Overview

- 9.2. Assumptions and Key Parameters

- 9.3. Methodology

- 9.4. Overview of Peer Groups

- 9.4.1. Peer Group I: Overview of Liquid Biopsy Assay Kits

- 9.4.2. Peer Group II: Overview of Liquid Biopsy Devices

- 9.4.3. Peer Group III: Overview of Liquid Biopsy Software and Other Solutions

- 9.5. Product Competitiveness Analysis

- 9.5.1. Liquid Biopsy Assay Kits

- 9.5.1.1. Liquid Biopsy Assay Kits Offered by Providers Based in North America

- 9.5.1.2. Liquid Biopsy Assay Kits Offered by Providers Based in Europe

- 9.5.1.3. Liquid Biopsy Assay Kits Offered by Providers Based in Asia-Pacific and RoW

- 9.5.2. Liquid Biopsy Devices

- 9.5.2.1. Liquid Biopsy Assay Kits Offered by Providers Based in North America

- 9.5.2.2. Liquid Biopsy Assay Kits Offered by Providers Based in Europe

- 9.5.2.3. Liquid Biopsy Assay Kits Offered by Providers Based in Asia-Pacific and RoW

- 9.5.3. Liquid Biopsy Software and Other Solutions

- 9.5.3.1. Liquid Biopsy Software and Other Solutions Offered by Providers

- 9.5.1. Liquid Biopsy Assay Kits

10. COMPANY PROFILES: LIQUID BIOPSY SOLUTION PROVIDERS

- 10.1. Chapter Overview

- 10.2. Amoy Diagnostics

- 10.2.1. Company Overview

- 10.2.2. Liquid Biopsy Portfolio

- 10.3. BioCartis

- 10.3.1. Company Overview

- 10.3.2. Liquid Biopsy Portfolio

- 10.4. DiaCarta

- 10.4.1. Company Overview

- 10.4.2. Liquid Biopsy Portfolio

- 10.5. Exact Sciences

- 10.5.1. Company Overview

- 10.5.2. Liquid Biopsy Portfolio

- 10.6. Gencurix

- 10.6.1. Company Overview

- 10.6.2. Liquid Biopsy Portfolio

- 10.7. Genecast Biotechnology

- 10.7.1. Company Overview

- 10.7.2. Liquid Biopsy Portfolio

- 10.8. Integrated DNA Technologies

- 10.8.1. Company Overview

- 10.8.2. Liquid Biopsy Portfolio

- 10.9. Lucence Diagnostics

- 10.9.1. Company Overview

- 10.9.2. Liquid Biopsy Portfolio

- 10.10. MedGenome

- 10.10.1. Company Overview

- 10.10.2. Liquid Biopsy Portfolio

- 10.11. Medicover Genetics

- 10.11.1. Company Overview

- 10.11.2. Liquid Biopsy Portfolio

- 10.12. nRichDx

- 10.12.1. Company Overview

- 10.12.2. Liquid Biopsy Portfolio

- 10.13. Precipio

- 10.13.1. Company Overview

- 10.13.2. Liquid Biopsy Portfolio

- 10.14. Qiagen

- 10.14.1. Company Overview

- 10.14.2. Liquid Biopsy Portfolio

- 10.15. RGCC

- 10.15.1. Company Overview

- 10.15.2. Liquid Biopsy Portfolio

- 10.16. ScreenCell

- 10.16.1. Company Overview

- 10.16.2. Liquid Biopsy Portfolio

- 10.17. Singlera Genomics

- 10.17.1. Company Overview

- 10.17.2. Liquid Biopsy Portfolio

- 10.18. Thermo Fisher Scientific

- 10.18.1. Company Overview

- 10.18.2. Liquid Biopsy Portfolio

11 PARTNERSHIPS AND COLLABORATIONS

- 11.1. Chapter Overview

- 11.2. Partnership Models

- 11.3. Liquid Biopsy Solutions: Partnerships and Collaborations

- 11.3.1. Analysis by Year of Partnership

- 11.3.2. Analysis by Type of Partnership

- 11.3.3. Analysis by Year and Type of Partnership

- 11.3.4. Analysis by Type of Partner

- 11.3.5. Analysis by Type of Circulating Biomarker

- 11.3.6. Analysis by Type of Cancer

- 11.3.7. Most Active Players: Analysis by Number of Partnerships

- 11.3.8. Analysis by Geography

- 11.3.8.1. Local and International Agreements

- 11.3.8.2. Intercontinental and Intracontinental Agreements

12 FUNDING AND INVESTMENTS

- 12.1. Chapter Overview

- 12.2. Funding Models

- 12.3. Liquid Biopsy Solutions: Funding and Investments

- 12.3.1. Analysis by Year of Funding

- 12.3.1.1. Cumulative Year-wise Trend of Funding Instances

- 12.3.1.2. Cumulative Year-wise Trend of Amount Invested

- 12.3.2. Analysis by Type of Funding

- 12.3.2.1. Analysis by Funding Instances

- 12.3.2.2. Analysis of Amount Invested by Year and Type of Funding

- 12.3.3. Analysis by Year and Type of Funding

- 12.3.4. Analysis by Type of Circulating Biomarker

- 12.3.5. Analysis by Type of Cancer

- 12.3.6. Analysis by Application Area

- 12.3.7. Most Active Players: Analysis by Number of Funding Instances

- 12.3.8. Most Active Players: Analysis by Amount Raised

- 12.3.9. Leading Investors by Number of Funding Instances

- 12.3.10. Analysis by Geography

- 12.3.1. Analysis by Year of Funding

13 BIG PHARMA INITIATIVES

- 13.1. Chapter Overview

- 13.2. Liquid Biopsy: List of Initiatives Undertaken by Big Players

- 13.2.1. Analysis by Year of Initiative

- 13.2.2. Analysis by Type of Initiative

- 13.2.3. Analysis by Year and Type of Initiative

- 13.2.4. Analysis of Big Pharma Players by Number of Initiatives

- 13.2.5. Analysis by Type of Partnership

- 13.2.6. Analysis of Big Pharma Player by Type of Initiative

- 13.2.7. Analysis of Big Pharma Player by Year of Initiative

- 13.2.8. Big Pharma Initiatives Summary

14 KEY ACQUISITION TARGETS

- 14.1. Chapter Overview

- 14.2. Scope and Methodology

- 14.3. Scoring Criteria and Key Assumptions

- 14.4. Potential Acquisition Targets: Liquid Biopsy Solution Providers

- 14.5. Concluding Remarks

15 CASE STUDY: OTHER NON-INVASIVE CANCER DIAGNOSTICS

- 15.1. Chapter Overview

- 15.2. Non-Blood-based Biomarker Detection Tests

- 15.3. Fecal Occult Blood Test (FOBT) and Fecal Immunochemical Tests (FIT)

- 15.4. Pigmented Lesion Assays

- 15.5. Stool DNA (sDNA)-based Tests

- 15.6. Volatile Organic Compound (VOC) Detection Tests

- 15.7. List of Other Non-Invasive Cancer Diagnostics

16 MARKET IMPACT ANALYSIS

- 16.1. Chapter Overview

- 16.2. Market Drivers

- 16.3. Market Restraints

- 16.4. Market Opportunities

- 16.5. Market Challenges

- 16.6. Conclusion

17 GLOBAL LIQUID BIOPSY MARKET

- 17.1. Chapter Overview

- 17.2. Assumptions and Methodology

- 17.3. Global Liquid Biopsy Market, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 17.3.1. Scenario Analysis

- 17.3.1.1. Conservative Scenario

- 17.3.1.2. Optimistic Scenario

- 17.3.1. Scenario Analysis

- 17.4. Key Market Segmentations

18 LIQUID BIOPSY MARKET, BY TYPE OF TECHNOLOGY

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Liquid Biopsy Market: Distribution By Type of Technology

- 18.3.1. Liquid Biopsy Market for Next Generation Sequencing, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 18.3.2. Liquid Biopsy Market for Polymerase Chain Reaction, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 18.4. Data Triangulation and Validation

19 LIQUID BIOPSY MARKET, BY TYPE OF SAMPLE

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Liquid Biopsy Market: Distribution By Type of Sample

- 19.3.1. Liquid Biopsy Market for Blood, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 19.3.2. Liquid Biopsy Market for Other Samples, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 19.4. Data Triangulation and Validation

20 LIQUID BIOPSY MARKET, BY TYPE OF CIRCULATING BIOMARKER

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Liquid Biopsy Market: Distribution By Type of Circulating Biomarker

- 20.3.1. Liquid Biopsy Market for Circulating Tumor DNA, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 20.3.2. Liquid Biopsy Market for Cell Free DNA, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 20.3.3. Liquid Biopsy Market for Cell Free RNA, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 20.3.4. Liquid Biopsy Market for Exosomes, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 20.3.5. Liquid Biopsy Market for Other Circulating Biomarkers, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 20.4. Data Triangulation and Validation

21 LIQUID BIOPSY MARKET, BY TYPE OF CANCER

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Liquid Biopsy Market: Distribution By Type of Cancer

- 21.3.1. Liquid Biopsy Market for Breast Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.2. Liquid Biopsy Market for Colorectal Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.3. Liquid Biopsy Market for Prostate cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.4. Liquid Biopsy Market for Lung Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.5. Liquid Biopsy Market for Bladder Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.6. Liquid Biopsy Market for Melanoma, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.7. Liquid Biopsy Market for Thyroid Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.8. Liquid Biopsy Market for Gastric Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.9. Liquid Biopsy Market for Head and Neck Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.10. Liquid Biopsy Market for Leukemia, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.11. Liquid Biopsy Market for Brain Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.12. Liquid Biopsy Market for Liver Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.13. Liquid Biopsy Market for Cervical Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.14. Liquid Biopsy Market for Ovarian Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.15. Liquid Biopsy Market for Oesophagus Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.16. Liquid Biopsy Market for Pancreatic Cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.17. Liquid Biopsy Market for Nasopharyngeal cancer, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.3.18. Liquid Biopsy Market for Sarcoma, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 21.4. Data Triangulation and Validation

22 LIQUID BIOPSY MARKET, BY APPLICATION AREA

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Liquid Biopsy Market: Distribution By Application Area

- 22.3.1. Liquid Biopsy Market for Early Diagnosis, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 22.3.2. Liquid Biopsy Market for Patient Monitoring, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 22.3.3. Liquid Biopsy Market for Recurrence Monitoring, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 22.4. Data Triangulation and Validation

23 LIQUID BIOPSY MARKET, BY END-USER

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Liquid Biopsy Market: Distribution By End-user

- 23.3.1. Liquid Biopsy Market for Hospitals / Laboratories, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 23.3.2. Liquid Biopsy Market for Research Institutes, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 23.3.3. Liquid Biopsy Market for Other End-users, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 23.4. Data Triangulation and Validation

24 LIQUID BIOPSY MARKET, BY GEOGRAPHICAL REGIONS

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Liquid Biopsy Market: Distribution By Geographical Regions

- 24.3.1. Liquid Biopsy Market for North America, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.3.1 Liquid Biopsy Market in the US, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.2. Liquid Biopsy Market for Europe, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.2.1 Liquid Biopsy Market in the France, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.2.2 Liquid Biopsy Market in the UK, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.2.3 Liquid Biopsy Market in the Germany, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.2.4 Liquid Biopsy Market in the Italy, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.2.5 Liquid Biopsy Market in the Spain, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.3. Liquid Biopsy Market for Asia-Pacific, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.3.1 Liquid Biopsy Market in the China, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.3.2 Liquid Biopsy Market in the India, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.3.3 Liquid Biopsy Market in the Japan, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.3.4 Liquid Biopsy Market in the Australia, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.3.1. Liquid Biopsy Market for North America, Historical Trends (Since 2021) and Forecasted Estimates (Till 2035)

- 24.4. Market Dynamics Assessment

- 24.4.1. Market Movement Analysis

- 24.4.2. Penetration-Growth (P-G) Matrix

- 24.5. Data Triangulation and Validation

25 CONCLUDING REMARKS

- 25.1 Chapter Overview

26 EXECUTIVE INSIGHTS

- 26.1. Chapter Overview

- 26.2. Company A

- 26.2.1. Interview Transcript: Director

- 26.3. Company B

- 26.3.1. Interview Transcript: Innovation Director

- 26.4. Company C

- 26.4.1. Interview Transcript: Founder & Chief Executive Officer

- 26.5. Company D

- 26.5.1. Interview Transcript: President and Chief Technology Officer

- 26.6. Company E

- 26.6.1. Interview Transcript: Strategic Technology Advisor

- 26.7. Company F

- 26.7.1. Interview Transcript: Founder And Medical Director

- 26.8. Company G

- 26.8.1. Interview Transcript: Chief Executive Officer

- 26.9. Company H

- 26.9.1. Interview Transcript: Chief Operating Officer

- 26.10. Company I

- 26.10.1. Interview Transcript: Chief Medical Officer

- 26.11. Company J

- 26.11.1. Interview Transcript: President and Chief Executive Officer

- 26.12. Company K

- 26.12.1. Interview Transcript: Sales and Marketing Manager

- 26.13. Company L

- 26.13.1. Interview Transcript: Marketing Director

- 26.14. Company M

- 26.14.1. Interview Transcript: Founder

- 26.15. Company N

- 26.15.1. Interview Transcript: Chief Executive Officer

- 26.16. Company O

- 26.16.1. Interview Transcript: Chief Scientific Officer

- 26.17. Company P

- 26.17.1. Interview Transcript: Chief Executive Officer and Co-founder

- 26.18. Company Q

- 26.18.1. Interview Transcript: Chief Scientific Officer